DSGX - FedEx: Does Not Compare Well To Peers Despite The Announced Restructuring

2023-04-14 08:00:00 ET

Summary

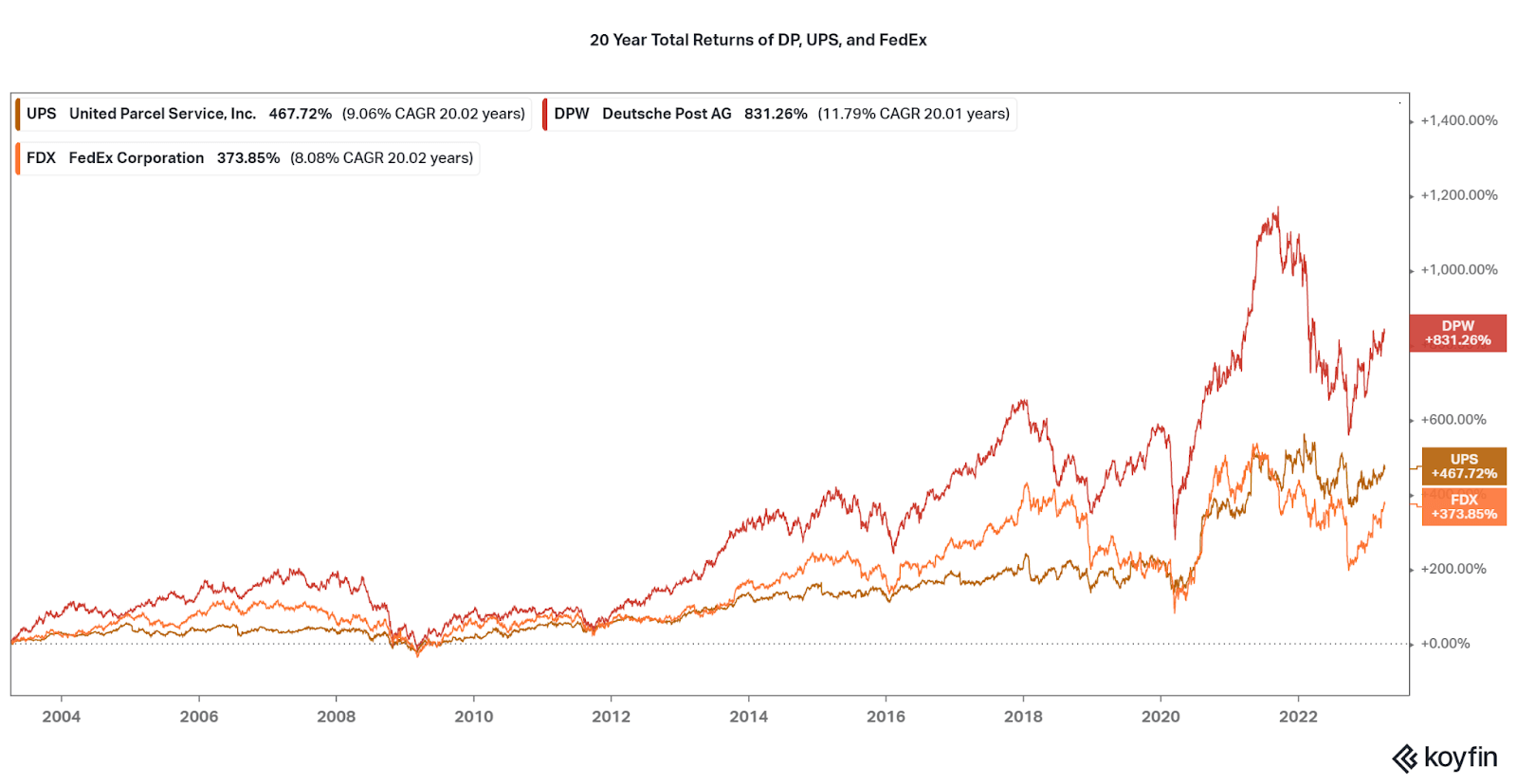

- FedEx has underperformed financially, and for shareholders, for the past two decades.

- Now, the company has announced a restructuring plan that is more "status quo" than reinventive.

- Investing in FedEx's moves to be in line with peers is not a good strategy in my view.

- Instead, I believe DHL and UPS remain far better short and long-term investments.

Introduction

UPS ( UPS ) and FedEx Corporation ( FDX ) are undisputed titans in the US's parcel logistics market, with Deutsche Post's DHL ( DPSGY ) uniquely positioned as the world's largest logistics company by revenue. Each company has distinct advantages, but for most investors, the best choice for an investment will be the lowest risk entity. Sure you can try to trade around sentiment and news, but a long-term investment in quality can lead to stable, market beating returns. This is especially true as logistics remains a cyclical, but essential, industry.

In fact, I chose Deutsche Post ((DP)) for inclusion in my high quality Craton Index . Since one period of financial underperformance in a bear market can cause investors to significantly underperform for years to come, quality is key. So, despite recent announcements by FedEx - a restructuring and raised dividend - some weaknesses will continue to harm returns. Therefore, I believe that current investors should sell after the recent 50% run these past 6 months, and reallocate to the stronger peers. But as always, each investor must consider all of their goals and circumstances when making an investment, so I will attempt to showcase as many data points as possible.

FDX Operational Qualities vs Peers

The biggest differences between FedEx and peers are the proportion of last-mile delivery, global presence, and financial safety. For the former, there is high capex and fuel costs associated with deliveries. For peers, a focus on international shipments and diversified freight services in all economies dissipates cyclicality. Despite all offering similar total returns over the past 10 years, rivals DHL and UPS have shown better secular opportunities over the past 20 years. This is the result of both better business economics, management, and increased diversification. Then as the financials show, FedEx fails to have a flexible balance sheet to drive meaningful operational improvements to fix the business issues, and in turn allow for market leading returns for investors.

{kind=link}

With DHL, FedEx, and UPS being the three primary parcel firms in the US, one would expect that all companies have similar business operations. However, DP only has about 50% of revenues related to express or delivery services (Express, Post & Parcel Germany, and eCommerce Solutions segments). Comparatively, UPS earns over 60% of their revenues from US domestic parcel delivery and express services, while FedEx earns 85% from their Express and Ground services (although with more international exposure than UPS). The question of the benefits of combining FedEx Express and FedEx Ground are unclear, at best.

Compiled by Author from Company Websites.

FedEx's Restructuring Plan

Announced at the recent DRIVE Investor Event, FDX announced that the company is looking to streamline their subsidiaries into a more consolidated and streamlined Federal Express Corporation entity. While the freight subsidiary will remain independent, the two largest operating segments of Express and Ground will unite under a single banner and organizational structure. This is to align themselves more with the closest peer UPS, who reports their revenues as US, International, and Supply Chain Services. However, rival Deutsche Post remains split into multiple units, and offers competitive financials, indicating that a consolidation alone may not be the issue.

2023 DP Business Profile

The restructuring of FedEx will require far more than layoffs and reducing redundancy in the corporate environment. While each key form of logistics involves the delivery of goods from one location to another, there are distinct differences. To understand the impacts, we have to look at each segment's key traits.

-

Express: Time definite delivery services (next-day, same-day, two-day, etc) are where FedEx shines, with a leading fleet of cargo aircraft, warehouses, and delivery vehicles. These services have the benefit of being higher margin, but face issues with cyclical levels of volume due to consumer spending. This leads to earnings being more volatile than peers. There are also significant CAPEX costs associated with servicing their fleets, energy demand, and warehousing (which will be targeted with the restructuring). DHL also dominates international routing, preventing FedEx from benefiting from emergent growth opportunities abroad except with bolt-on acquisitions (which is an issue due to leverage).

-

Last-mile Delivery: Parcel delivery to the end-customer. This segment is where rival UPS takes more market share and is less volatile in performance than FDX. This is due to the fact that non-time definite deliveries volumes are more stable though time, despite being lower margin in nature. One issue is that this industry is saturated, with organic growth reliant on global/US GDP rather than acquisitions or production upgrades. There is also competition with Amazon, who are moving to provide third-party delivery services to capitalize on the growing e-commerce trend.

-

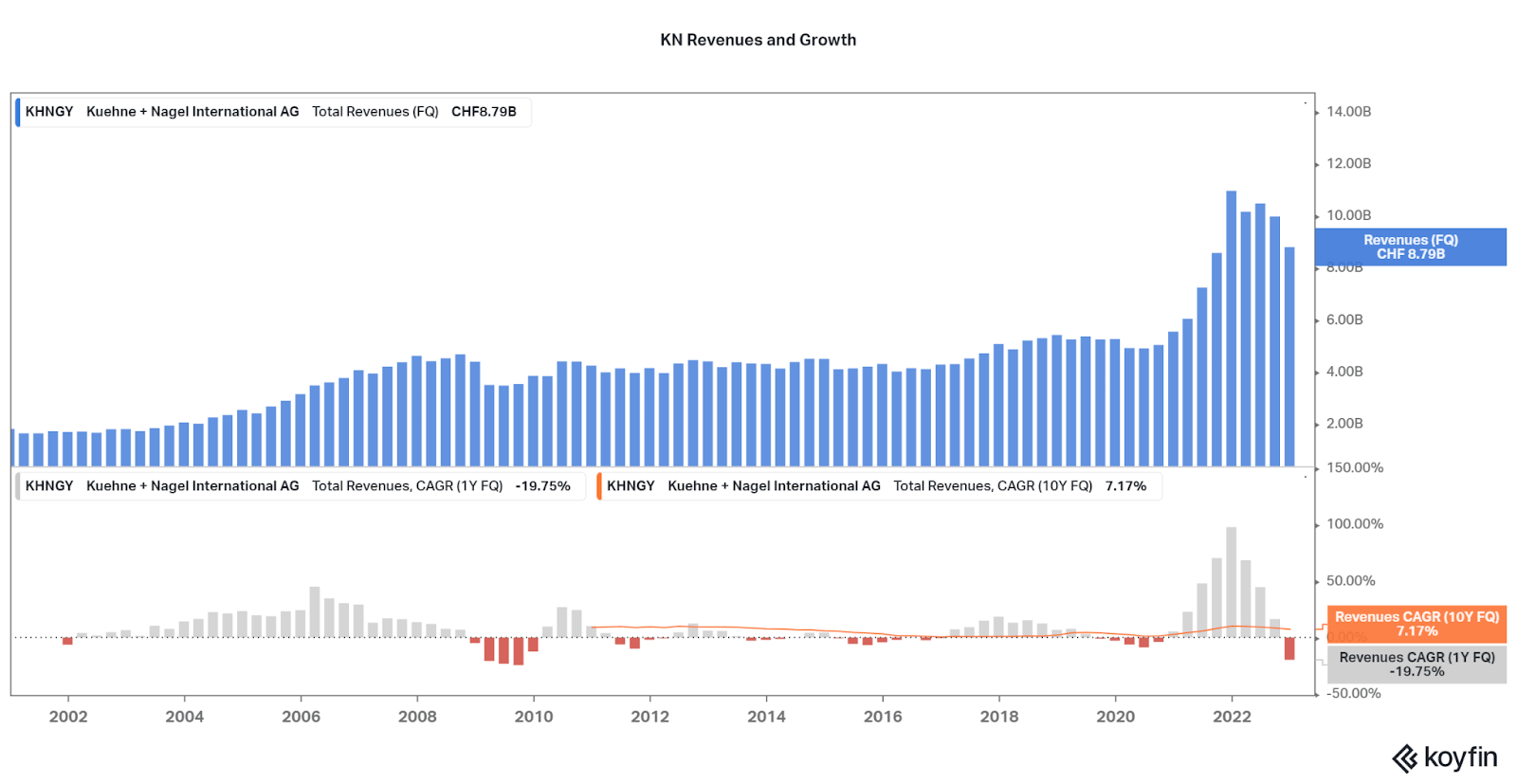

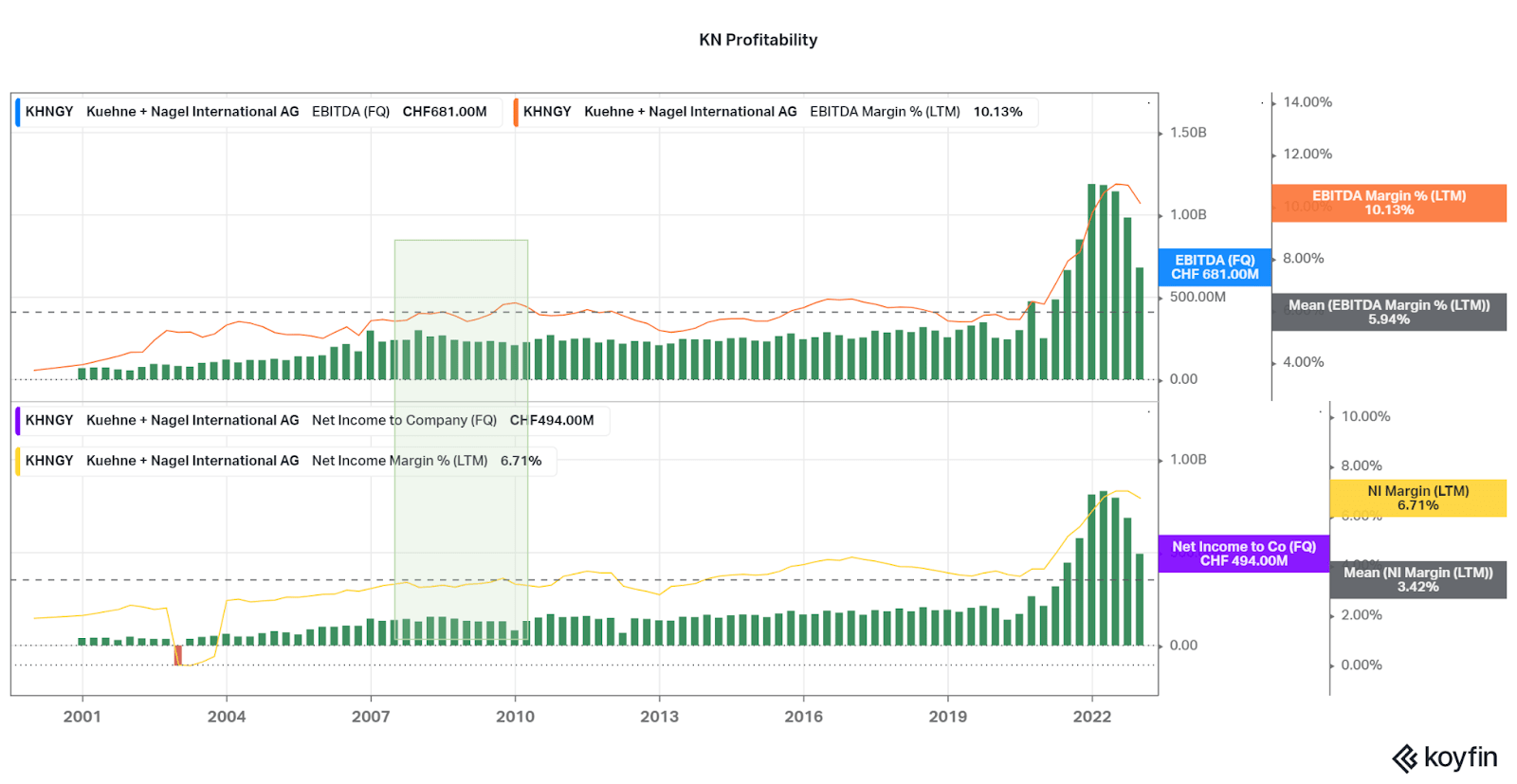

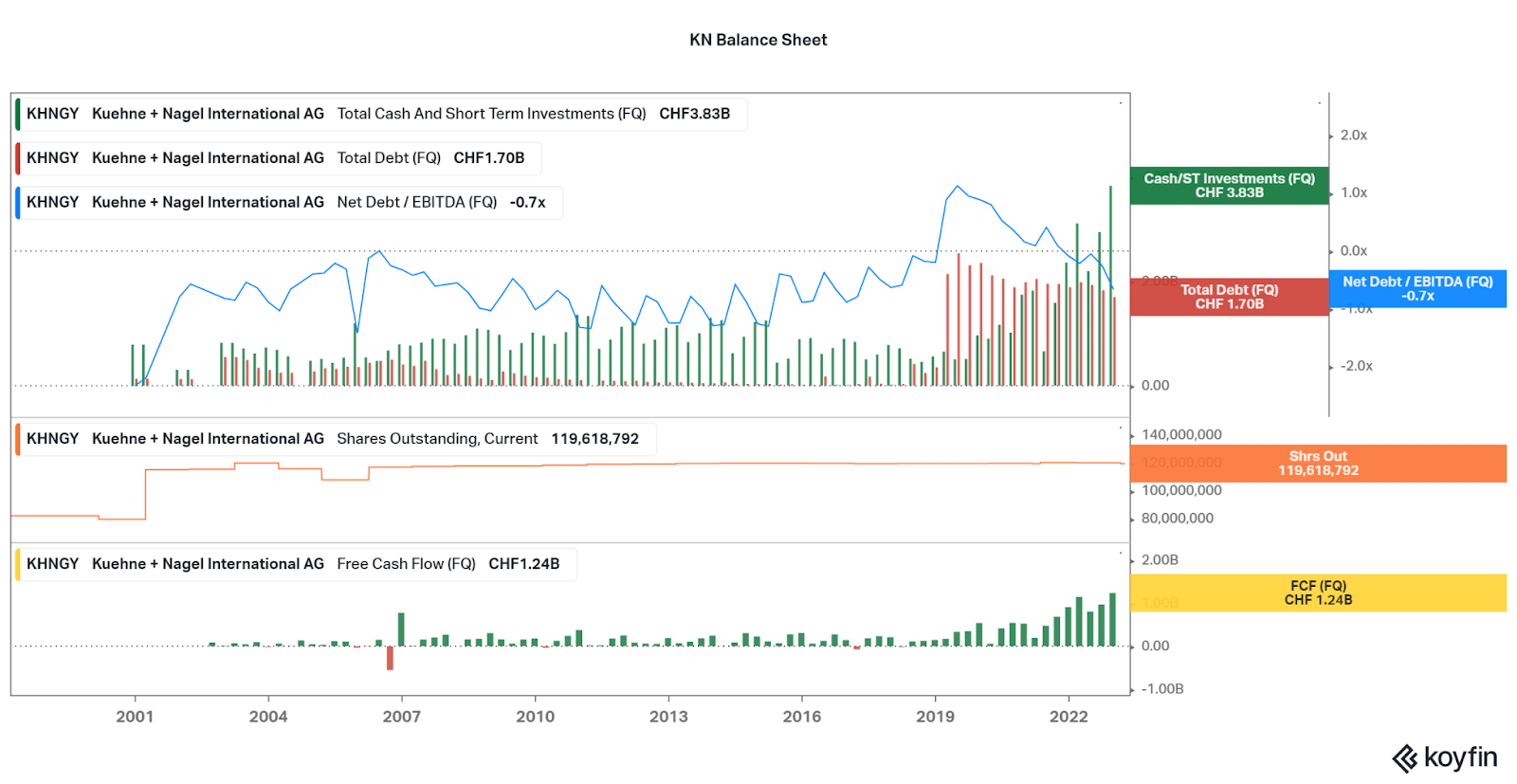

Freight: These services typically involve the movement of goods between one point and another, with third-parties providing the first and last-mile delivery services. Financial performance is extremely reliant on volume and transportation costs, but can be an area of growth due to the heterogeneous nature of the industry (largest player Kuehne + Nagel holds no more than ~10% total market share). Optimization can involve supply chain management technology integration (mostly software and automation) to drive efficiency.

FDX has laid out a few examples of where they can begin to drive cost savings via consolidation. First, the use of company-owned intermodal containers (for multiple forms of transportation such as rail and truck), can allow for the company to take advantage of the most lucrative path with ease. Facilitating easier transfer from one mode of transport to another will be the driving force between the Express and Ground consolidation, as Express involves air cargo, but rail is seen as most cost-effective. Further developments were reported by Freight Waves :

There will be more mixing and matching at FedEx than it has seen before, and little will be left on the table. For example, FedEx Ground, which hopes to save $1.2 billion through fiscal year 2025, expects to nearly double the portion of miles it moves via rail to 15%, John Smith said. Virtually all of the volumes will move in company-owned double-stack boxes, Smith said.

Another main objective is to attain what is called the "one van, one neighborhood" proposition. Today, it is commonplace for FedEx Express and Ground vans to circle a neighborhood several times per day, sometimes within hours of each other. "If you've ever seen a Ground and Express truck in your neighborhood on the same day, or watched them pass each other on the street, you know what we're trying to accomplish," said Smith.

The air express and international business, which aims to save $1.3 billion in Drive-related costs by FY 2025, will focus on flying more balanced lanes and leveraging outside partners for nonurgent flights, said Richard Smith. The company is parking planes, cutting aircraft and flight hours, and looking for ways it could substitute truck service for a second air leg on lower-priority international flights, he said.

The problem is, these investments can still be made regardless of the subsidiary's distinction, and UPS and DHL highlight their success in either optimization ((UPS)) or diversification (DHL). In fact, I find that many of the announced changes only showcase how FedEx has worse management, with issues such as having too many personnel and costly assets, a lack of technological advantages (supply chain management), and subpar route optimization. With up to $4 billion in cost savings suggested to be available by 2025, the question is whether Federal Express has the ability to even meet these significant goals.

FedEx DRIVE Presentation FedEx DRIVE Presentation

Unfortunately, there is evidence that FDX may not have the experience to fulfill their current mission. In the next section I will highlight the financial underperformance that can be used as a redflag for investors, but that is not all. Operationally, one of the major risks FDX's poor integration of the European Express segment TNT. And again, consultants and market participants wonder whether FedEx has the management expertise to drive these improvements.

I expect that some change will drive positive change within the organization, but the chance of target goals being directly met are low. This is especially with a bear market already damaging profitability across the sector, and I will highlight the financial differences between select peers now.

FedEx Financial Comparisons

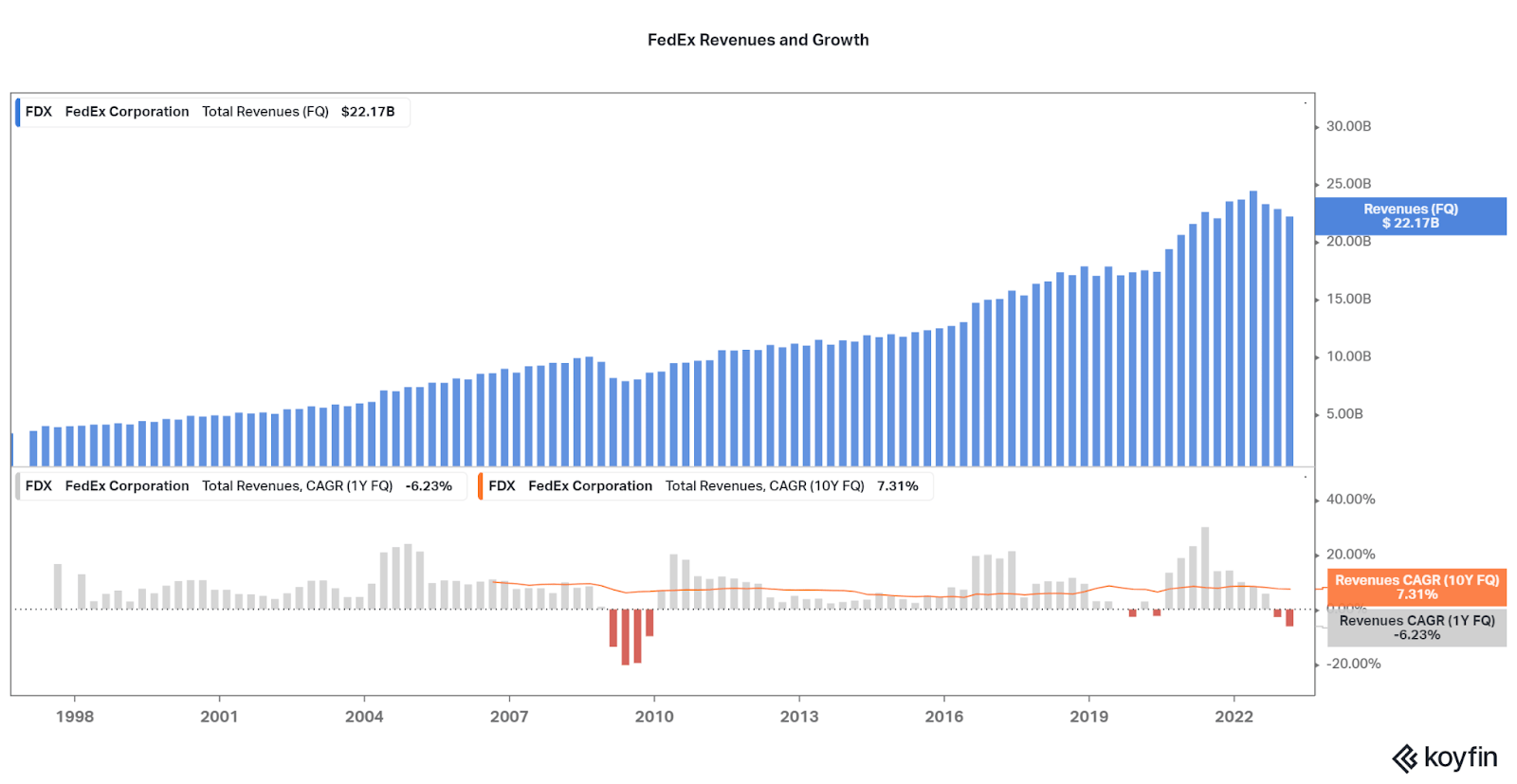

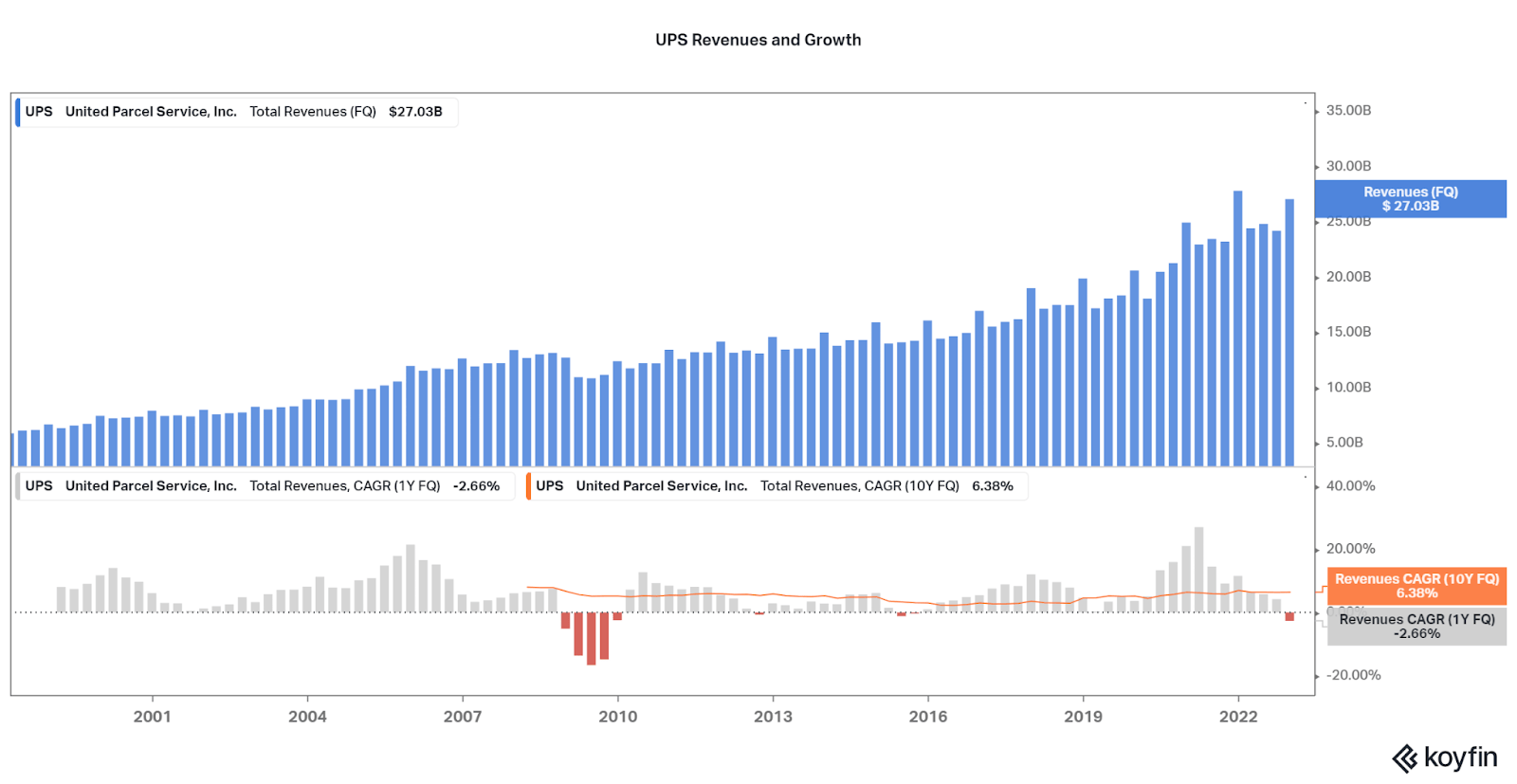

To put data behind the claims of FedEx' underperformance, I collected three sets of charts to analyze the peer group. And for further financial comparison, I also added the main freight and supply chain competitor, Kuehne + Nagel (KHNGY) to this analysis. The first series, a look at long-term revenue growth, is more insightful about the industry dynamics of cyclicality. All companies see ebbs and flows of growth, but are fairly resilient during recessions due to the necessity of logistics. However, freighters are more volatile than more express and delivery focused companies such as UPS and FDX. This is certainly where FedEx looks in-line, or even superior to peers, but growth is not the issue being addressed with the restructuring process.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

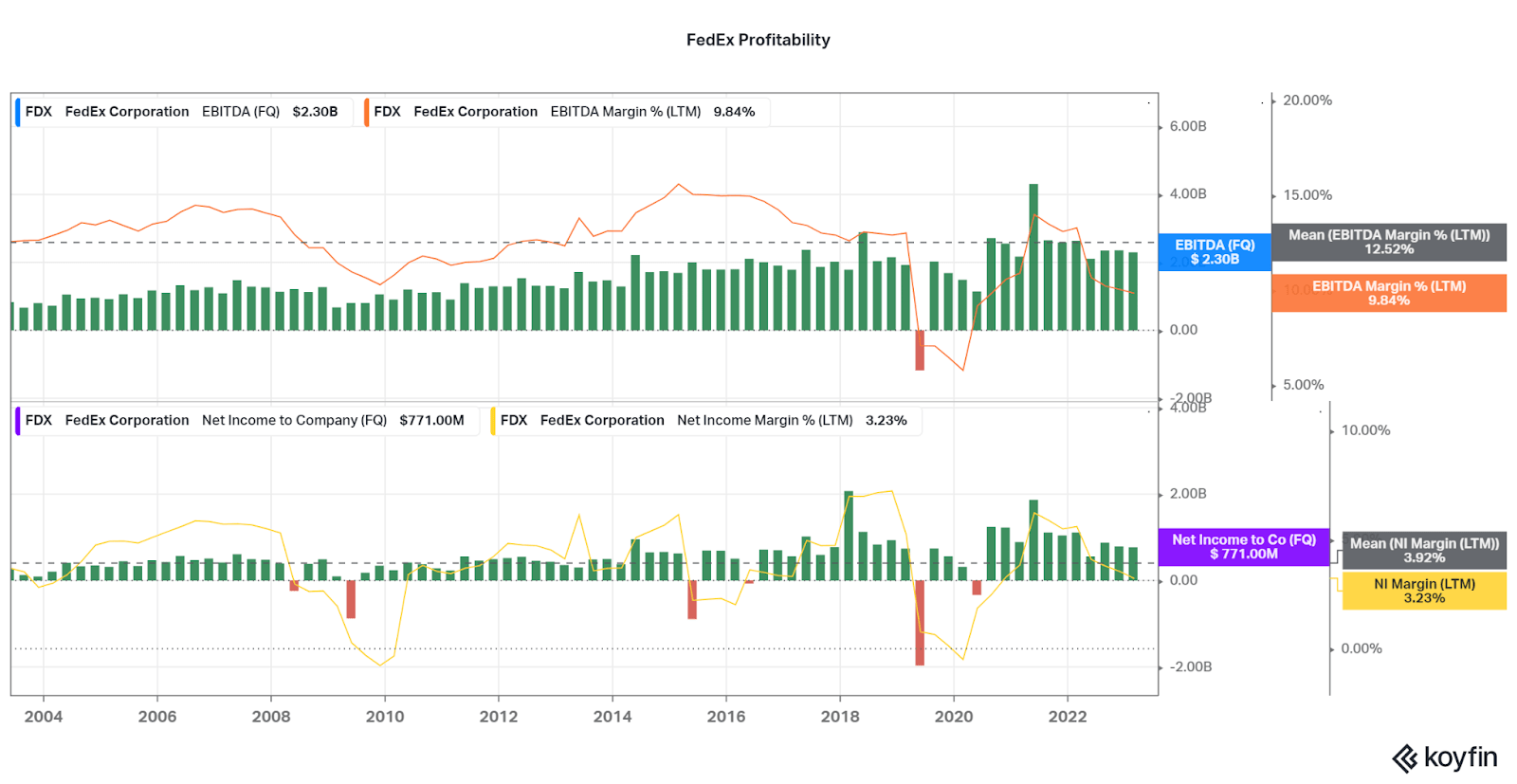

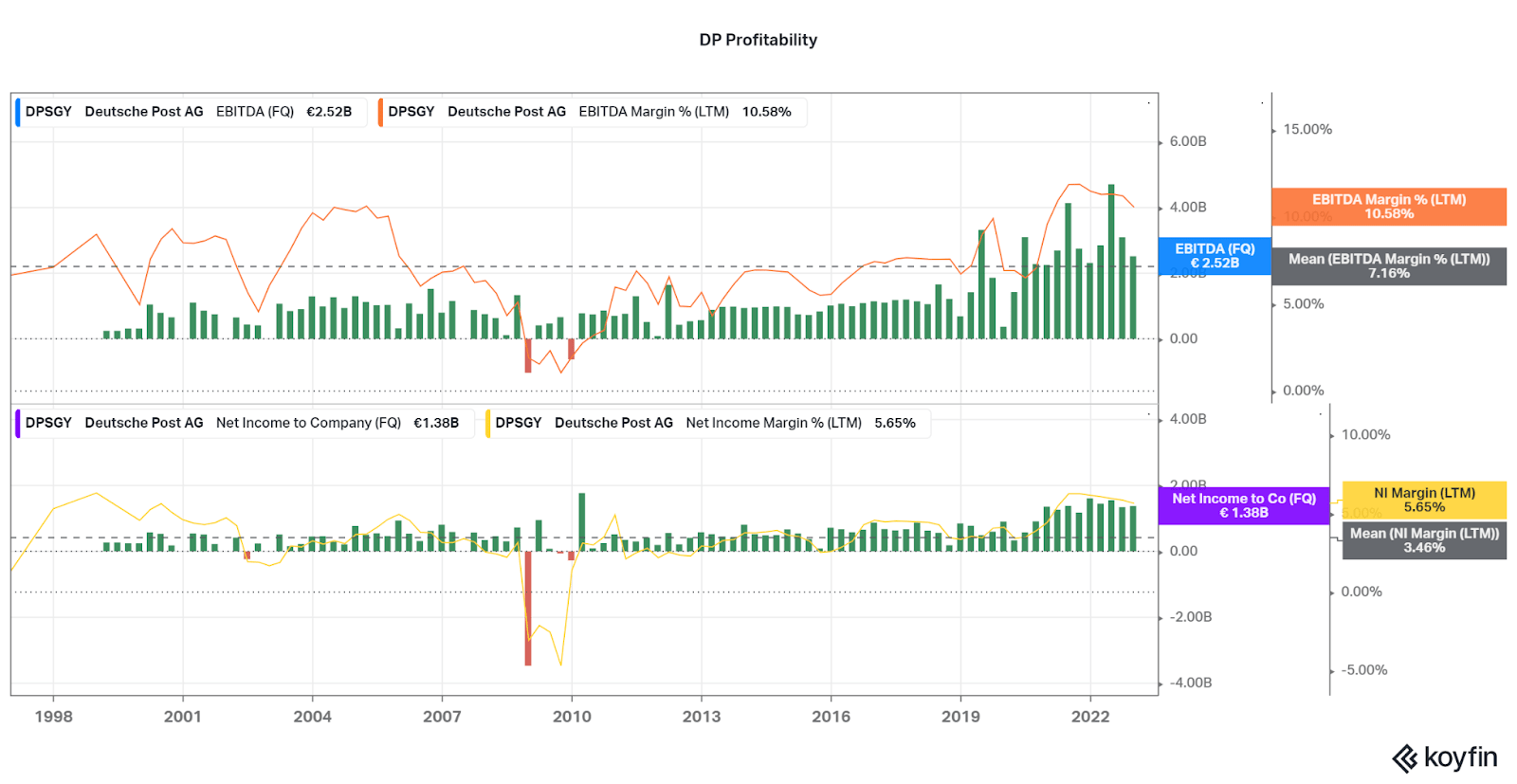

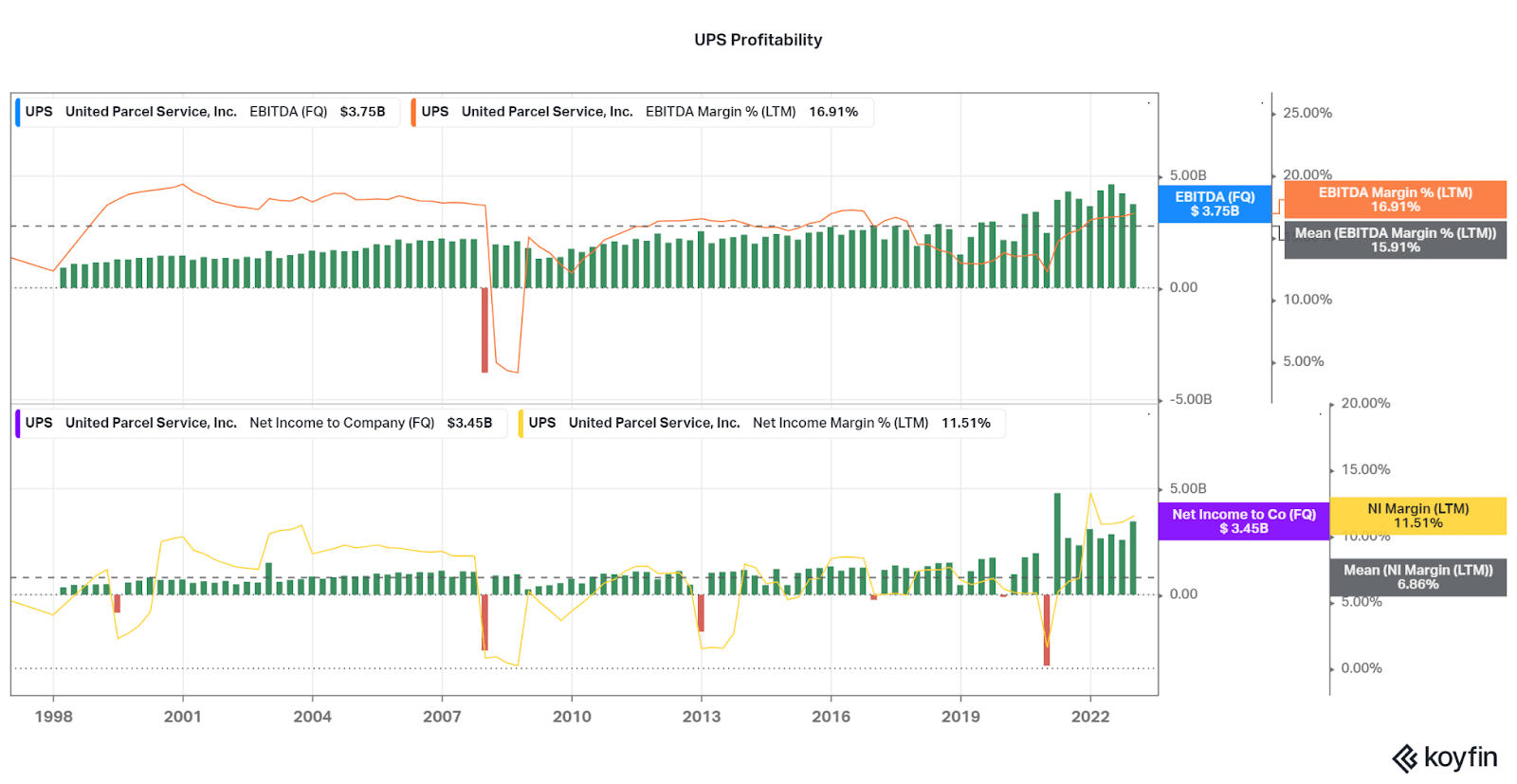

Poor Profitability is Basis for Restructuring

Although boasting a favorable growth profile, FedEx has had weakness in their profit margins over the past five years. Over the past 20 years, the company had EBITDA margins of 12.5% (LTM), but this has been difficult to meet since 2018, even with a favorable bull market in 2021. This also contrasts with peers who have seen improving profitability over the past few years. FedEx is also lacking in consistency on the bottom line, with the Net Income Margin (LTM) fluctuating often. As an example, I highlight how global freight forwarder Kuehne + Nagel was very consistent in generating profits during the financial crisis, even as revenues fell.

Being unable to drive profitable growth is where FedEx starts to look less enticing for investors when peers have been more consistent. The data also suggests that issues are on the managerial front, as DHL, UPS, and K+N each offer further consistency, particularly in regards to net income generation. This has also been an issue for years, so for those looking for fundamental changes may be left searching. Investors must hope that this new restructuring will begin to both improve and stabilize performance moving forward, but this will only bring FDX in-line with peers.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

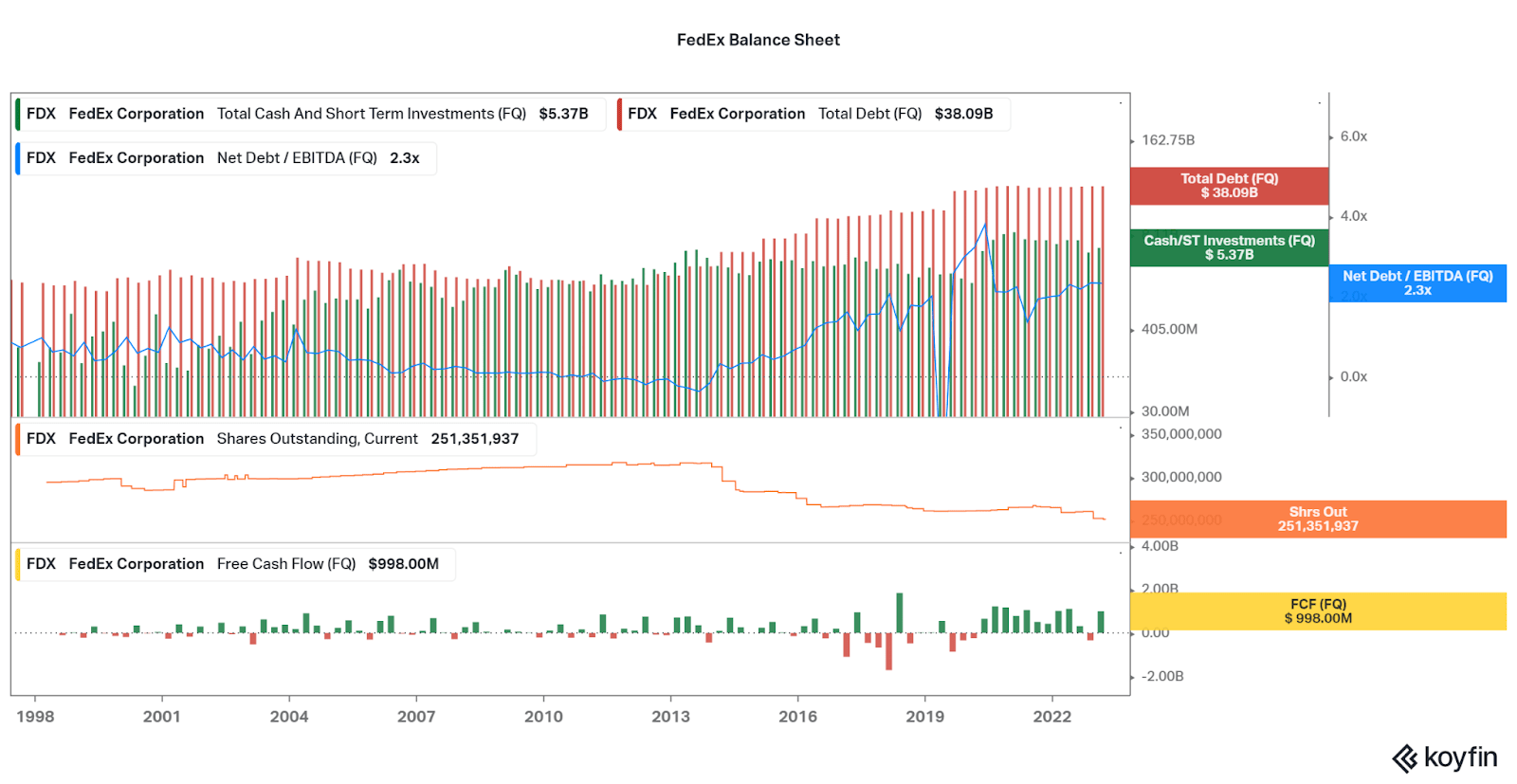

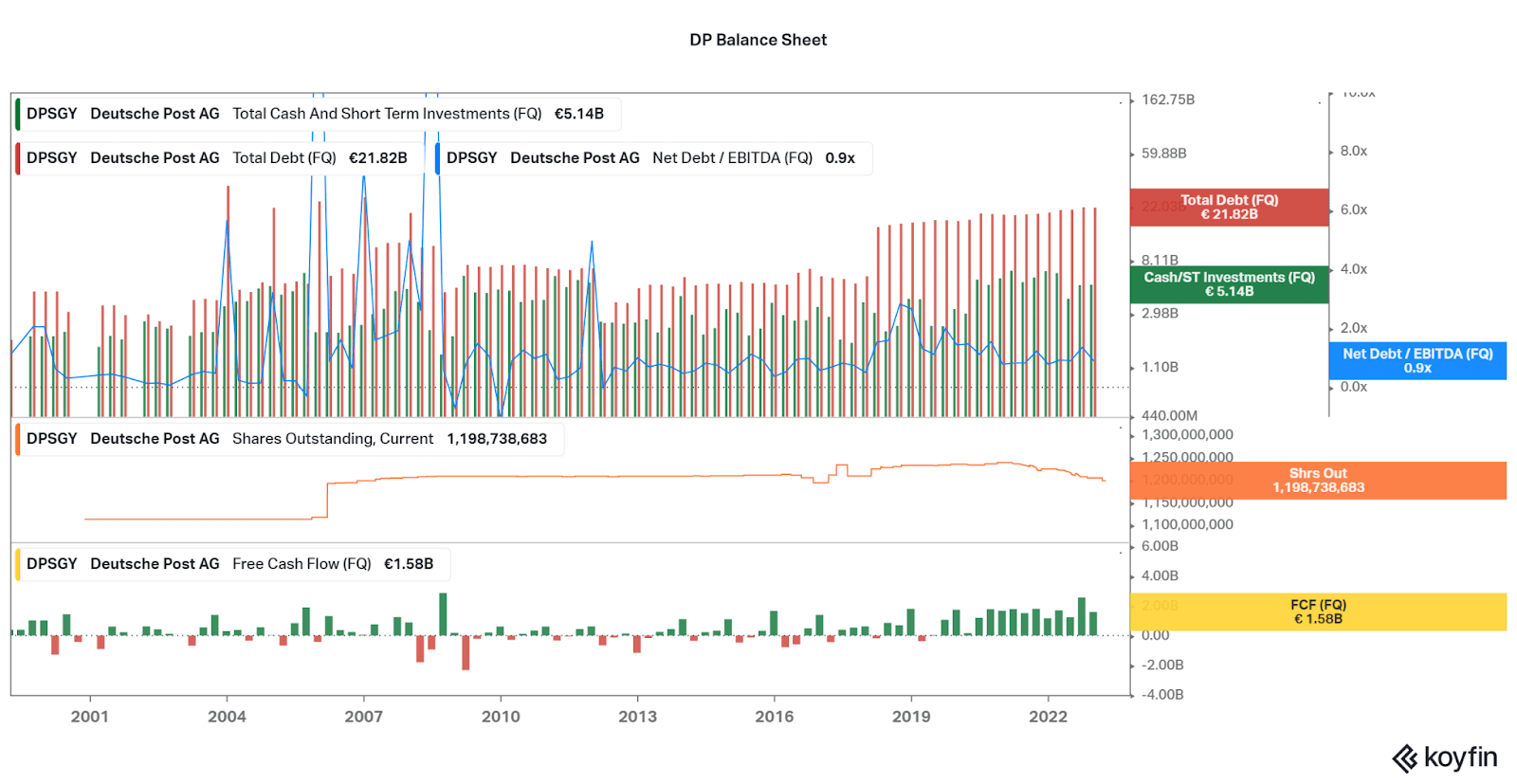

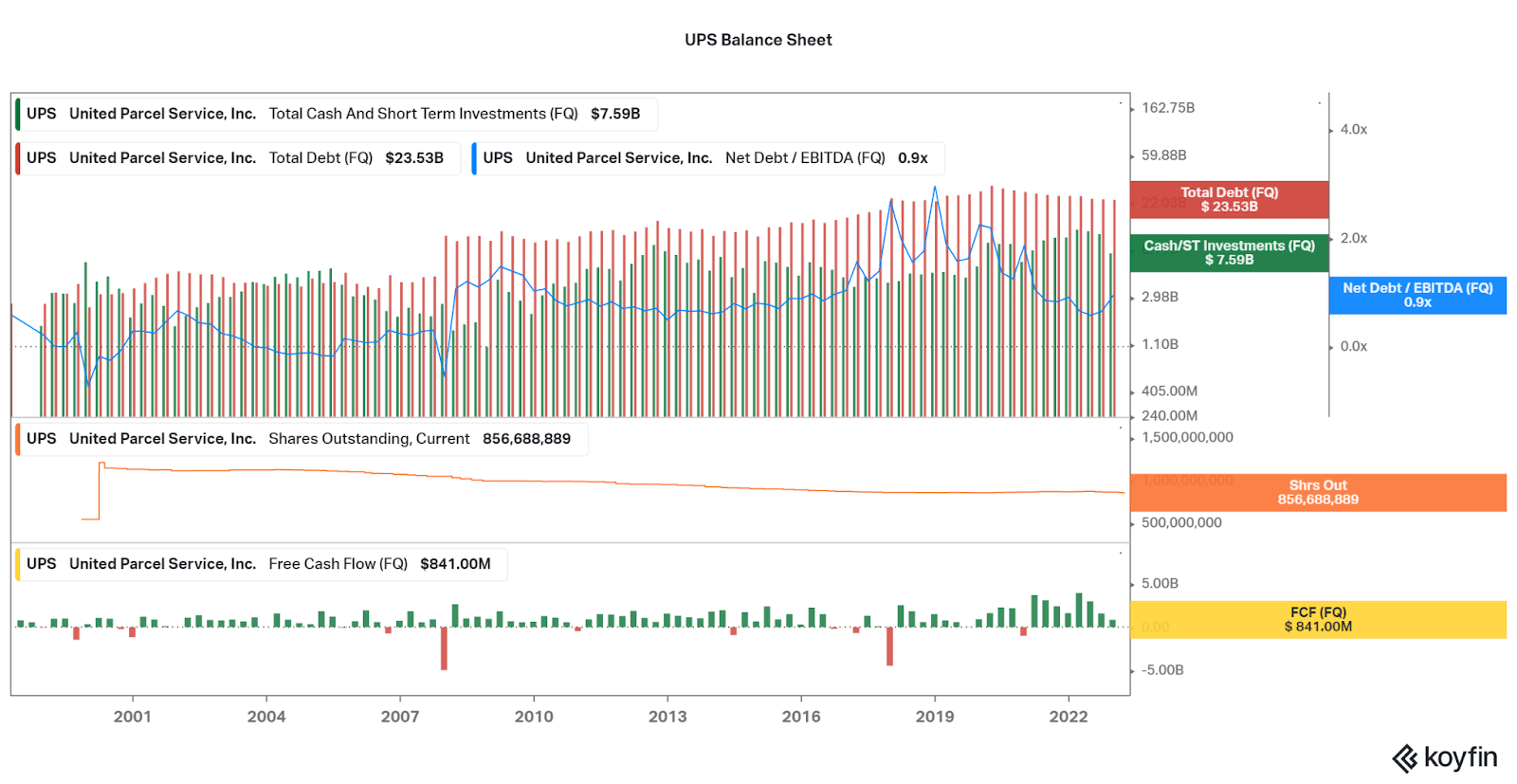

Must Allocate Restructuring Profits to Balance Sheet

As shown, FedEx has had difficulty in the past with generating steady profits. This has had a detrimental effect on the balance sheet. When compared to peers, the primary issue is excessive leverage due to debt. In fact, FedEx has almost double the debt of both UPS and DHL. This issue has risen over the past five to ten years, adding further evidence of mismanagement as of late. While all four companies saw a peak in leverage during the pandemic or in 2019, FedEx is the only peer who has been unable to reduce debt or leverage over the past 4-8 quarters.

This weak balance sheet causes multiple issues. First, FDX has less flexibility for a prolonged bear market that may occur as trade volumes plummet with rising inflation and interest rates. Sure, management expects a further $4-6 billion in savings over the next few years, but this will not be enough to reduce debt to a manageable level. I believe that with the potential for higher profitability, the first goal for profit allocation should be debt reduction to be in-line with peers. This will allow for the credit rating to improve and that will reduce interest expenses while boosting positive sentiment. Instead, we see continued focus on pleasing investors in the short-term with buybacks and dividend increases, which do nothing to solve structural issues. But more on that later.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Safety and Risk

For now, I will continue to discuss the importance of safety in terms of investment performance. Earlier, I stated how I chose Deutsche Post/DHL for my stalwart-led Craton Index. The holdings are all leaders in their segment, and offer the best fundamentals of their peers. This led to outperforming the market when backtested over more than a decade. Unfortunately, FedEx does not perform as well as DHL, or even the equally strong UPS. The fundamental issues of risk prevent me from being able to recommend FDX, especially during a weak economic state.

I am not the only researcher with a view that FedEx does not offer the same stability and opportunity as peers. As I discussed above, the key issue is the lower quality balance sheet, and even volatile earnings of late. This is crucial considering we are entering a global economic slowdown. There are already huge declines in volumes across the logistics industry, and FedEx reported 20% lower earnings YoY in their Q3 earnings. While a rebound is expected in the years to come, the major risk for shareholders is the losses and underperformance in the near-term.

As discussed by the credit ratings agencies Moody's and Fitch , who both rate UPS and DP/DHL higher than FedEx, competitive advantage, financial flexibility, and diversification will be necessary to manage and outcompete over the next few years. Even UPS is facing headwinds due to competition, while DP/DHL is doing well to improve their position abroad. The importance of a strong and flexible financial position will be relevant in 2023 and 24.

There is a slew of risk factors that are detrimental to the entire logistics industry, and are factors for the poor performance of the pre-pandemic era. First and foremost, reputational risks are always on the front stage for delivery companies. Whether it is viral video of deliveries being thrown or damaged, or time-definite deliveries failing to be met, a few negative instances can significantly impact a company. There is extensive data on the issues, but one key analysis highlights how software companies like Descartes ( DSGX ) are benefiting from the weak logistics industry :

'This past year's growth slowdown in ecommerce and home delivery has resulted in a 6% improvement in delivery performance versus the 2022 study; however, 67% of the consumers surveyed still experienced a delivery failure in the three-month evaluation period,' said Chris Jones, EVP, Industry and Services at Descartes. 'What's more, 68% of those affected by delivery problems took some form of action that translated into negative consequences for the retailer or delivery company (see Figure 1), indicating that the pandemic grace period is over and consumers are becoming intolerant of poor delivery performance.'

There is also the elephant in the room: Amazon ( AMZN ). The e-commerce company is a huge disruption to the global logistics industry, and the big 3 delivery companies must battle the ample capitalization of Amazon. One of the biggest risks is of Amazon providing third-party logistics services due to their extensive network. Per the Wall St. Journal :

Amazon's published rates appeared to be 4% to 5% below those on the trucking spot market, where companies book last-minute transportation, Citi analyst Christian Wetherbee said in a Monday research note. "Marginal discounts on certain lanes is common practice," he said, adding that at a 4% to 5% discount to spot rates "Amazon could very well be making money on this offering."

Sanford C. Bernstein & Co. analyst David Vernon said in a research note that traditional freight companies face a bigger competitive threat, however, if Amazon acts as a "not-for-profit truck brokerage," offering money-losing rates for capacity it buys on the spot market, rather than using the platform to sell excess capacity "it has bought to run its supply chain."

"Past entrants to the brokerage space have used discounting to achieve market share and Amazon is likely to do the same," Cowen Inc. analyst Jason Seidl said in a Monday research note.

Supply Chain Dive

Thankfully for now, Amazon's rapidly growing market share percentage mostly accounts only for their own traffic and deliveries, but rising competition across e-commerce solutions for FedEx, UPS, and DHL will be costly and difficult. Of the four groups, FedEx is currently weakest to maneuver, and recent pledges to focus on shareholders instead of operations is not the best decision in my eyes. Included is the recent increase in dividend by 10%, even as the company enters a bear market. This will take billions in cash flows that may be better served for other shareholder benefits, such as combatting the extensive environmental risks. As highlighted by logistics firm Kuehne + Nagel, there are plenty of areas of investment that are needed in the years to come.

Kuehne + Nagel FedEx Q3 Report

Conclusion

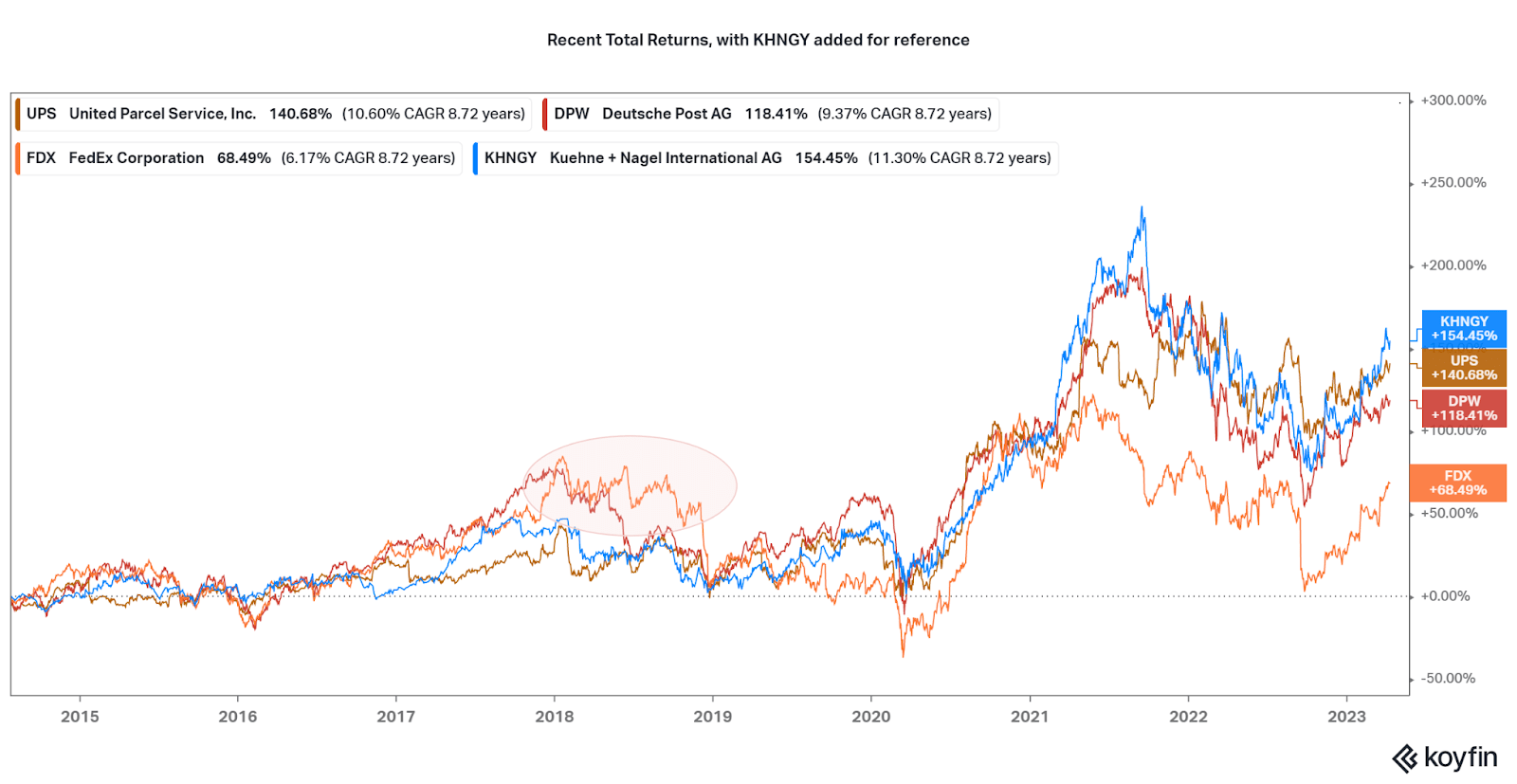

While FedEx has merits as the leading express parcel delivery company in the world, structural issues do not allow investors to capitalize on the issues. The breakdown began in late 2018, a small bear market that was exacerbated by continued underperformance of their TNT Express acquisition, the rise of Amazon 3rd-party services, and volatile earnings. Since then, FedEx has underperformed peers by a wide margin and issues remain. I am sure many still believe there may be at least a valuation play to consider, but when Deutsche Post is cheaper across all metrics, it is clear that FedEx does not offer an enticing valuation.

{kind=link}

{kind=link}

Therefore, I do not believe that the recent restructuring plans will be a catalyst for change at FedEx. Investors will be best suited to sell and reallocate to a separate company, most favorably DPSGY or UPS (although UPS remains too expensive for my taste). Either way, the industry is currently in a significant bear cycle with volumes declining rapidly. This means there is some time to consider your personal goals and opportunities, but I do not believe that FDX will offer any opportunity for outperformance or safety in the coming years, but I will certainly be following their progress.

Thanks for reading. Feel free to share your thoughts below.

For further details see:

FedEx: Does Not Compare Well To Peers, Despite The Announced Restructuring