UMI - FEN: 9% Yield From Energy Midstream MLPs Not Worth It

2023-03-15 10:17:21 ET

Summary

- The First Trust Energy Income & Growth ETF is a closed-end fund ("CEF") that focuses on publicly traded energy MLPs.

- FEN currently charges a total expense fee of 1.44%, which is arguably quite high despite the relatively high level of income and "managing away" the K-1 complications for investors.

- However, without a K-1 issuance, some investors may miss the tax advantages that are often the primary investment thesis supporting energy MLPs in the first place.

- Top holdings in the FEN ETF include Enterprise Products Partners, Magellan Midstream Partners, and Energy Transfer.

The First Trust Energy Income & Growth ETF ( FEN ) is a CEF that seeks a high level of after-tax total return by investing at least 85% of assets in publicly-traded energy sector MLPs (master-limited partnerships) and energy-related public companies. FEN currently yields ~9% and trades at a 12.3% discount to NAV. The fund is most highly concentrated in companies that transport petroleum products, companies in natural gas transmission (pipelines, LNG export, etc.), and companies in the business of electrical power generation & transmission. Investors looking for a high level of income from the energy midstream sector, and don't want the hassle of a K-1 at tax time, the FEN ETF is worth considering.

Investment Thesis

As most of you know - at least if you have been reading my SA work - the U.S. is now not only the #1 petroleum producer in the world, but last July the U.S. also became the #1 LNG exporter on the planet as well. The FEN ETF's top holdings are in companies that benefit from shale oil production growth in the U.S. because that oil production also comes with a lot of associated gas production - be it dry-gas or natural gas liquids ("NGLs"). In addition, much of that "dry-gas" is subsequently liquefied and exported as LNG. Indeed, over the first 6-months of last year, U.S. LNG exports averaged a whopping 11.1 Bcf/d:

EIA

The point here is that if you are bullish on U.S. shale production growth, you pretty much have to be bullish on the midstream MLPs - at least when it comes to NGLs and LNG volume growth. And while price always impacts commodity-based MLPs (sooner or later), many MLPs have long-term MVCs (minimum volume contracts) that are relatively commodity price-insensitive.

With that as background, let's take a look at the FEN ETF to see how it has positioned investors for success going forward.

Top-10 Holdings

The First Trust FEN ETF's top-10 holdings are shown below (as of 1/31/2023) and equate to what I consider to be a moderately concentrated 53.3% of the portfolio:

First Trust

NOTE: the 2022 Annual Report is the last full list of holdings I could find on the First Trust webpage - and that was as of Nov. 30, 2022.

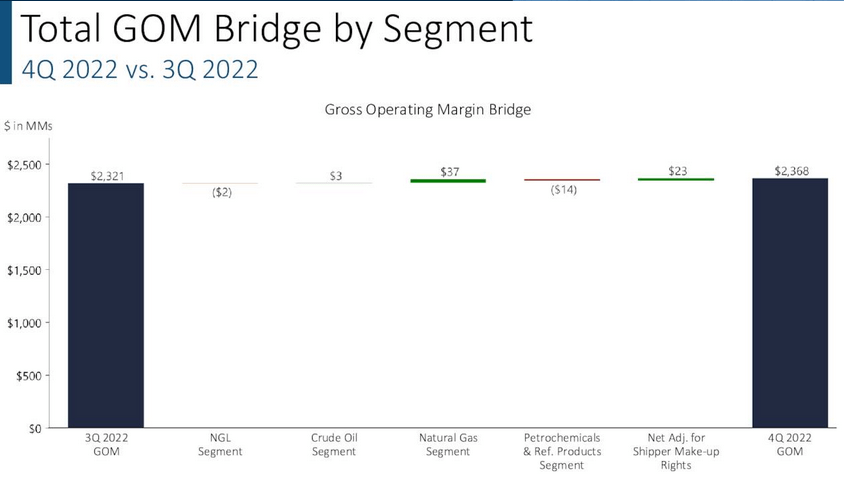

The #1 holding is midstream giant Enterprise Products Partners L.P. ( EPD ) with a near 10% weight. EPD's is organized into 4 operating segments, which in Q4 had the following gross operating margin, or GOM, in parentheses.

- NGL Segment ($1.29 billion)

- Crude Oil Segment ($418 million)

- Natural Gas Segment ($315 million)

- Petrochemicals & Refined Products Segment ($339 million)

As can be seen, the NGL Segment is as large as the other three segments combined. The graphic below is a sequential GOM bridge from Q3 to Q4 and demonstrates the relative stability of the business model in the current operating environment and one that is largely built on the foundation of long-term contracts based on volumes and/or cost-of-service ("COS") as opposed to the price of the actual commodity being transported:

{kind=link}

EPD is +3.6% over the past year and currently yields 7.72%.

Magellan Midstream Partners ( MMP ) is the # 2 holding with an 8.3% weight. MMP is +12.9% over the past year and currently yields nearly 8%. In Q4, MMP missed on the bottom line , but Q4 free cash flow of $324 million was +15.1% yoy while distributable cash flow ("DCF") was $345 million (+16.2% yoy).

The #4 holding in the FEN ETF is Cheniere Energy Partners ( CQP ), a growing and leading global LNG exporter. Cheniere swung to a profit in Q4 , as revenue of $9 billion increased 38% yoy, and GAAP profits of $15.78/share came in far above the consensus estimate ($6.02/share) and compared to a year-earlier loss of $1.32 billion ($5.22/share). The units are up 20.9% over the past year and currently yield less than 1%. The relatively low yield is because Cheniere is still in a significant growth mode as the partnership recently initiated the permitting process for a major expansion of LNG export capacity at its Sabine Pass terminal in Louisiana.

The Williams Companies ( WMB ) is the #5 holding with a 4.8% weight. In Q4, WMB delivered a $0.09/unit top-line non-GAAP beat while revenue of $10.97 billion (+3.2% yoy) was light by $110 million. WMB units are down 6% over the past year, which is just about what its yield is. That being the case, investors in WMB have been "kissing their sister" over the past year (i.e., not getting anywhere).

The top-10 list is rounded out by Kinder Morgan ( KMI ) with a 3.1% weight. On the first day of March, Bernstein upgraded KMI to over-weight after its previous (and rather humorous ...) take on the MLP as a 'leaky bucket' or 'death by a thousand cuts' , referring to what it estimates as an annual "roll off of ~$250 million of EBITDA, mostly in, but not limited to, gas pipelines." Indeed, units are down 3.3% over the past year and currently yield 6.6%.

KMI is one of the largest energy infrastructure companies in the U.S. and operates through four segments: Natural Gas Pipelines, Products Pipelines, Terminals, and CO2. CO2 may become a growth lever if the partnership can tap into CO2 sequestration tax credits available in the Biden Administration's Clean-Energy Act (also known as "IRA"). It may have to partner with a larger partner to scale up to some of the bigger CCS projects.

As for the portfolio as a whole, has allocated capital across the portfolio as follows:

First Trust

Going forward, in the mid to long term, I would not be surprised to see the Electric Power Transmission sub-sector (17.7% allocation) grow faster than the other sectors listed.

Performance

The graphic below shows the FEN ETF's 5-year total returns as compared to some of its peers: the USCF Midstream Energy Income Fund ETF ( UMI ), the Global X MLP ETF ( MLPA ), the Global X MLP & Energy Infrastructure ETF ( MLPX ), and the Alerian MLP ETF ( AMLP ):

As you can see, the FEN ETF is the laggard of the pack - and by a significant margin (more than 50% below its nearest peer). Much of that is because quarterly distributions have been stuck at $0.30/unit since 2019 , when it was cut nearly in half from the previous $0.58/unit. Not a good track record for an ETF that advertises itself as an "Income and Growth" fund.

Risks

As I have been writing on Seeking Alpha for the last year or so (pushing back against the more popular and false narratives out there ...) we currently live in an " Age of Energy Abundance ". Now, the midstream companies in the FEN ETF are generally supposed to be insulated from the actual price of the commodity they transport. However, when prices fall (due to either over-production and/or a lack of demand), that means price differentials fall, and that typically hurts midstream companies that process, transport, and charge terminal fees for the commodity.

Meantime, supply/demand fundamentals still matter in the commodity space, so any significant economic slowdown in the global economy could certainly negatively impact global petroleum supply/demand. Since the U.S. is now the #1 producer of petroleum and LNG exporter on the planet, that could therefore certainly reflect negatively back into the U.S. midstream space as well.

Summary & Conclusion

I started off this piece thinking it would likely be a positive review. However, FEN not only hasn't kept pace with its direct peers with respect to total returns, its distribution growth is practically non-existent. Given the massive growth in the NGLs, natural gas, and LNG export volumes over the past year (not to mention crude oil exports recently), if this ETF couldn't grow during that time frame, when would it?

I've noticed there are many investors on Seeking Alpha that over-emphasize dividend income as opposed to total returns. That is exactly the mistake opportunity that owning FEN could lead to. That being the case, I would certainly not buy the FEN ETF.

If I were an investor looking for income from MLPs (I am not ...) and if I already owned FEN, I would sell it and put the proceeds into MLPA instead. However, over the long-term, I would advise investors looking for exposure to income from the energy sector to simply build their own portfolio with four core highly rated companies: Chevron ( CVX ), Exxon ( XOM ), ConocoPhillips ( COP ), and Phillips 66 ( PSX ) - which recently took over midstream giant DCP Midstream. While your yield may not be as good (in the short term), your after-tax... total returns will likely be far superior to those of an ETF like FEN.

That opinion is easily supported by the following 3-year total returns comparison:

For further details see:

FEN: 9% Yield From Energy Midstream MLPs Not Worth It