FG - Fidelity National Financial: A Sleeping Beauty Ready To Wake Up

2023-11-29 01:30:21 ET

Summary

- Fidelity National Financial's core business is title insurance and related services, which is suffering due to high mortgage rates and low real estate activity.

- Title insurance business appears at the bottom of its cycle and even a slight reduction in mortgage rates is expected to jumpstart it.

- FNF's subsidiary, F&G Annuities & Life, primarily offers fixed annuities and is likely to be spun off tax-free to FNF shareholders in 2025. It enjoys strong growth.

- In the long term, the Company has beaten the index and is positioned to repeat its performance.

My recent update on F&G Annuities & Life ( FG ) was a call to review its parent Fidelity National Financial ( FNF ).

FNF consists of 3 segments - Title, F&G, and Corporate. The latter one is insignificant and includes some small real estate-related businesses, changes in the tax valuation allowance, investments close to $1B, interest expense, and certain unallocated overhead. The two other segments deserve a detailed description.

Title insurance and related services

This is FNF's core business. It provides title insurance and escrow and other related services including trust activities and home warranty products. Title insurance is required for almost any property sale or refinancing. It is a form of indemnity insurance that protects against financial loss from defects in title to real property and from the invalidity or unenforceability of mortgage loans. Every mortgage lender requires it but it can also protect property owners.

Residents of the US and Canada take title insurance for granted as an item of real estate closing or refinancing. I was recently involved in a property sale in a country where title insurance is not common (it's available there but is exotic, untested, and expensive) and for the first time, I fully recognized the importance of the product. Many issues that popped up during the sale process would be of no significance in the US.

Due to its nature, title insurance sales are synced with real estate cycles. Today this business is suffering as high mortgage rates almost kill refinancings and suppress sale activities at least for residential properties. To preserve margins, FNF has to scale down its activities by closing offices and reducing its workforce. Once interest rates start going down, the reverse process will take place.

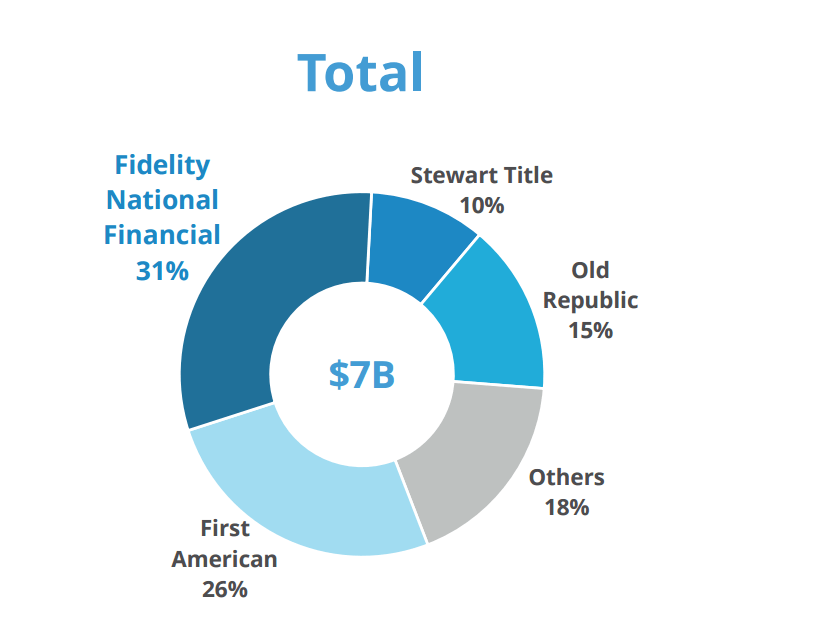

FNF is well positioned to navigate real estate cycles as it is the biggest and most profitable title insurer in the US as seen on the slides below.

{kind=link}

{kind=link}

It operates under multiple brands in all states and territories and is #1 or #2 in 39 of them. Around 15% of title insurance sales represent commercial revenues which are less cyclical than residential. Title insurance is sold either directly or through independent agents such as attorneys or real estate professionals. Agents improve coverage but direct sales are more profitable.

Title insurance is rather unique in many ways. Save for retroactive reinsurance, it is probably the only insurance line that protects against past events which makes in-house data extraordinarily important. Like many real estate actors, title insurers rely on personal connections, earned trust, and brand recognition. Insurance premiums are usually capped and often fixed. These factors in combination with capital requirements and the scale required make the industry unattractive for newcomers/disruptors and the competition is likely to stay as it has been = primarily between the top four players.

FNF has been the industry's largest player with a stable market share of ~30-31%. Operating margins are strong and stable at 15-20% as FNF reserves only 4.5% of title revenues which is sufficient to cover claims and claim adjustment expenses.

The industry meanwhile is growing quickly. Since title insurance premium is proportional to the size of the sale or refi, it has two underlying sources of growth: an increase in the number of properties in the US and the appreciation of home prices. The industry has grown from $15.6B in 2017 to $27.6B in 2021 which corresponds to ~15% CAGR.

Insiders are well-aligned with investors. Since 1984, FNF has been led by William Foley who is currently its chairman. He owns 3.4% of the company worth ~$450M. Overall insiders own 5.4% of shares.

Mr. Foley used to be an attorney in charge of his law firm when in 1984 he led a leverage buyout of a small title insurance company Fidelity National in Phoenix, AZ. He dropped his legal practice and committed himself to running the acquired business. 20 years and 80 acquisitions later, FNF became the biggest player in the industry with a 30% market share. The company went public in 1987. Quite shortly after the LBO, Fidelity moved to curb the company's dependence on independent agents and focus on direct selling through its employees. It allowed Fidelity to control its costs and maintain margins through different stages of real estate cycles. The company has never lost money on an annual basis.

All of the above makes FNF's title business fundamentally attractive provided investors can handle cyclicality.

F&G Annuities & Life

Please check my " F&G Annuities & Life : Likely Acquisition Target With Projected 30%+ Annual Return" for a company detailed description. I will outline only the key details below.

FNF acquired F&G on June 1, 2020 for $2.7B. After June 1, 2025, FNF can spin off F&G tax-free to its shareholders as long as it has owned at least 80% of F&G shares. The spin-off is likely to occur shortly after this date. FNF has done similar transactions several times in the past, it is in the best interest of wealthy FNF insiders as well as other investors, and the probable spin-off is being publicly discussed on FNF earnings calls.

In December 2022, FNF spun off 15% of F&G, and it is now publicly traded.

Even though the company is called F&G Life And Annuities and technically belongs to the life insurance industry, there is very little Life in it but plenty of Annuities. Fixed annuities (mostly fixed indexed annuities) are by far the main product. Additional products include other types of annuities - immediate annuities, group annuities (aka pension risk transfers - PRT), and funding agreements (while not annuities, they are almost identical in structure). The only life product today is the so-called Indexed Universal Life comprising only 5% of GAAP net reserves.

Issuing fixed annuities is a straightforward spread-based business in theory. The company receives funds from customers and invests them, aiming to generate interest that exceeds the rate credited to customers' accounts. For the last several years, F&G has retained Blackstone ( BX ) to manage investments with excellent after-fee results.

Fixed annuities are in high demand today due to two reasons. First, high interest rates make fixed products attractive. Secondly, the number of (future) retirees is growing quickly. The most successful company in the subindustry is Apollo's ( APO ) Athene with about $250B of invested assets and an ROE of ~16-17%. F&G was built according to Athene's recipes but is five times smaller with ROE close to 10% in recent quarters.

F&G's growth is steep as seen on the slide:

{kind=link}

The figure on the slide - 13% YoY in AUM - underestimates growth. F&G is currently reinsuring its flow for certain annuities in return for ceding fees. AUM including reinsured flow is ~$53B vs $47B on the slide.

After the full spin-off, F&G will become the only independent fixed annuity provider. All peers have been acquired by alternative asset managers and/or bigger life companies. The last one - American Equity ( AEL ) is in the process of being acquired by Brookfield with the closing expected in early 2024. The AEL acquisition price was close to its book value ("BV") ex-AOCI.

Upon the spin-off, F&G is expected to become an acquisition target as well trading close to its BV ex-AOCI.

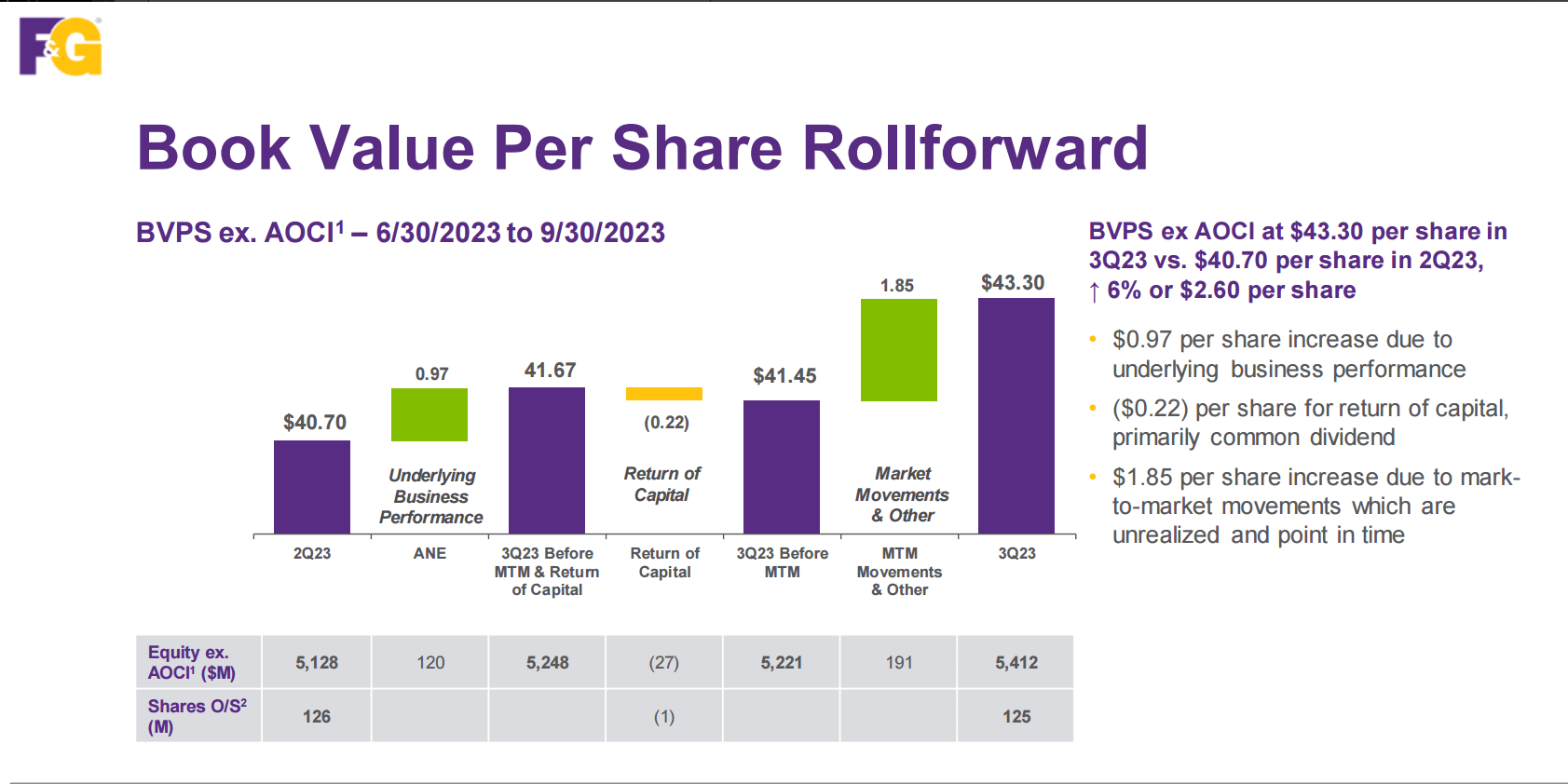

{kind=link}

The slide above shows the progress in the BV growth with the current value of $43.30 per share or $5,142M in total. The FG stock is currently trading at $42.40.

The next slide shows the evolution in F&G's ROE:

{kind=link}

Assuming an ROE of 10%, on June 1, 2025, BV will be about $50 per share including dividends, or $6,250 in total.

BV can climb higher if F&G improves its ROE to mid-teens in line with Athene's. This is precisely what the company intends to do based on the recent Investor Day. Below are the main levers identified in the company's presentations:

- Continued strong growth of AUM. This is almost guaranteed because of the current interest rate environment. Scaling up will allow to reduce overhead and reach operating leverage.

- Increasing net investment spread by leveraging Blackstone capabilities.

- Producing non-spread margins by investing in distribution channels and reinsuring a fraction of annuities flow. Non-spread business needs less capital and is supposed to foster ROE growth.

A couple of weeks ago, F&G announced an additional investment of $250M by FNF. It will occur in late 2023 or early 2024 but no further details were communicated. While it can happen in the form of preferred or common equity, the latter seems more likely as it better fits the interests of FNF, F&G, and their shareholders.

FNF will invest funds at 10% or more in line with F&G's ROE. F&G will grow its capital to better capitalize on the current favorable environment. As we know, scaling up benefits ROE.

Currently, only 15% of F&G is trading publicly. The trading is thin with noticeable bid-ask spreads. Unfortunately, FNF can distribute only a limited number of additional F&G shares as it has to maintain its ownership above 80%. Increasing its stake in F&G will allow FNF to spin off more of F&G shares without violating the 80% threshold to facilitate trading.

Finally, since all F&G shares will eventually end up in the hands of FNF shareholders, $250M represents an additional tax-free future dividend.

Valuations

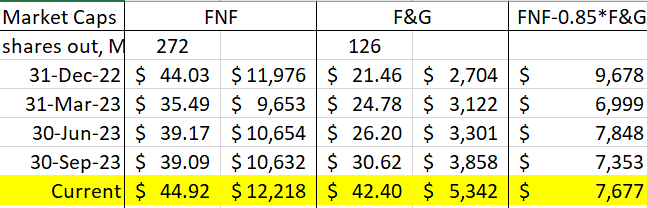

We will start with determining the current value of FNF ex-F&G by deducting 85% of F&G market cap from FNF market cap:

{kind=link}

So the current value of the Title and Corporate segments is about $7.7B or ~$28 per share. Excluding the COVID panic, the stock has not been that low since early 2017 but a more detailed review is needed for comparison purposes.

We should be cautious here. Before F&G, FNF several times invested in businesses (mostly financial) and spun them off several years later. Shareholders benefited from these transactions. For example, Fidelity National Information Services ( FIS ) was spun off in 2006 and has a current market cap of $33B and Black Knight Financial (recently acquired by Intercontinental Exchange ( ICE ) for $12B) was spun off in 2017. The coming spin-off of F&G follows the tested blueprint.

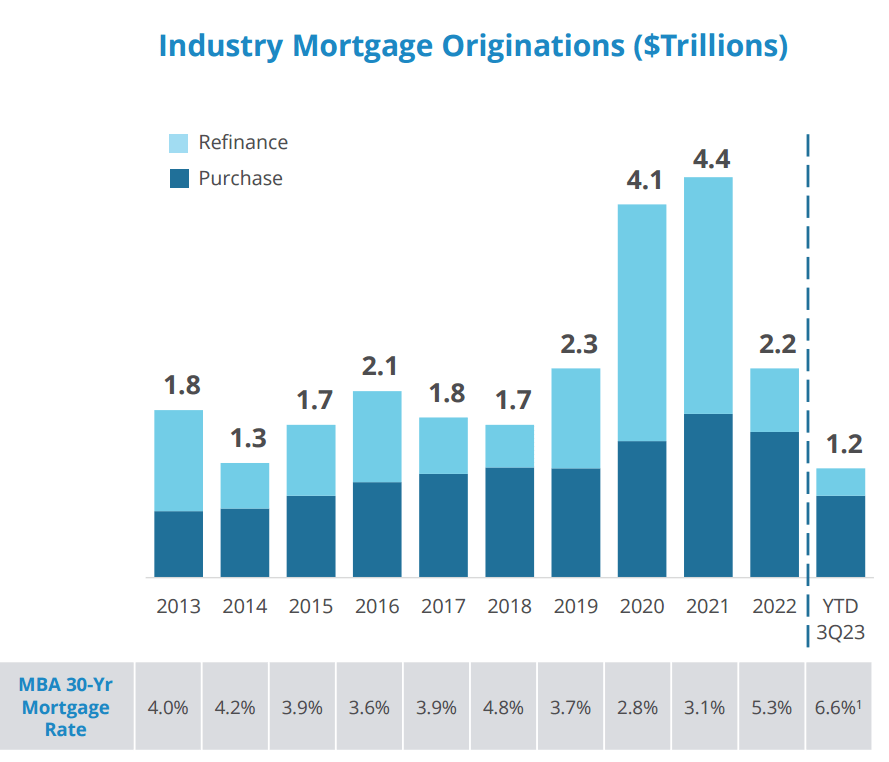

For comparison, we can use only years starting with 2017 after the last spin-off. Due to the COVID extraordinary refinance boom, 2020 and 2021 are bad comps. 2022 was affected by F&G's partial spin-off. It leaves us only with 2017, 2018, 2019 as comps. Of these, 2018 was the worst from the standpoint of both mortgage originations and interest rates as seen on the following slide:

{kind=link}

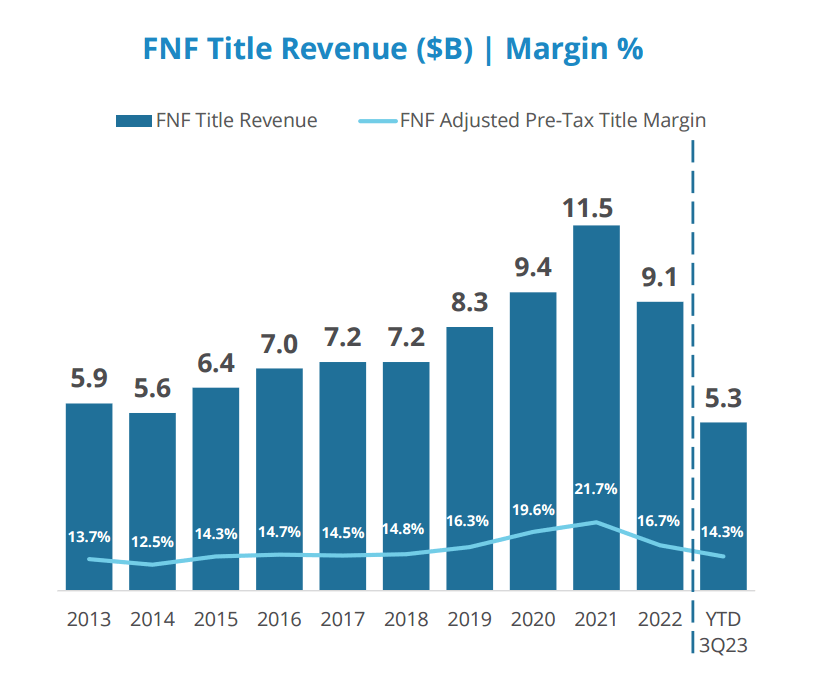

Management often compares 2023 with 2018. Q3 adjusted pretax earnings for the Title segment were $287M and $311M in 2018 and 2023 respectively. For the full 2018, adjusted pretax earnings for the Title segment were almost $1.1B. The same figure for Q3 TTM is ~$1B.

At the end of 2018, FNF's market cap was ~$9.6B. It means that upon a slight improvement in interest rates, FNF ex-F&G should be worth at least the same $9.6B.

If we assume that 2025 will be similar to 2018, FNF stock should be worth $9.6B plus 85% of $6,250M in F&G equal to ~$15B or ~$55 per share vs ~$45 currently. It translates into ~11% in annualized capital appreciation. Since FNF is currently yielding 4.3%, the total annualized return for our base case will be above 15%.

The slight improvement in interest rates may happen as early as 2024. Returns will be higher under this scenario.

Please notice that with 6.6% in mortgage in 2023, the Title results are close to 2018 with 4.8% rates. This illustrates FNF growth comprised of three components:

- The median home price was ~$323K in 2018 and is ~431K now and the same property sale/refi activity should cause mortgage originations and title insurance premiums to be ~30% higher.

- The US population grows at ~0.5% per year and the number of properties should grow at a similar rate. Under similar economic circumstances, more sale/refi transactions are likely to occur.

- FNF grows its business through tuck-in acquisitions that happen almost every year.

It means that when mortgage rates become attractive, FNF results will exceed its previous peak of 2019 (excluding COVID-related years). At the end of 2019, FNF's market cap was $13B, or 35% higher than in 2018. This illustrates the stock's potential.

All of the above is true as long as interest rates start normalizing in 2024 and 2025. It might not happen. In this case, investors will be left collecting dividends until the normalization occurs. Dividends have grown at 11% per year on average since 2015 and the last bump in weak 2023 was 7%.

Risks and conclusions

I have a long list of risks that I check every stock against. FNF surprised me: I did not discover any systematic risks the company is exposed to except for interest rates (this applies only to the core Title business; F&G has plenty of risks): the product is indispensable, new entrants/disruptors are unlikely, leverage is reasonable, management is tested and investor-friendly, no foreign risks, no noticeable legal risks, private equity is not involved, and on, and on.

Typically, even good stocks have 3-4 systematic risks. After some thinking, I figured out that William Foley is 79. Since his input has been outstanding, I guess it is a risk. Other risks may be still lurking but they do not appear easily identifiable.

There is an argument against buying FNF. We can expect strong returns only when interest rates start going down. But once it happens, other stocks may appreciate quickly and, perhaps, quicker than FNF.

We can generalize the last argument by asking how FNF has fared against the index long-term. The answer is straightforward thanks to the return calculator on the FNF site.

I picked the date of August 8, 2008. On that day, I bought American Express ( AXP ) which has delivered ~15% IRR including dividends. The S&P 500 has returned about 11% including dividends since.

{kind=link}

The slide above shows the cumulative FNF return of ~491% which translates into ~12% IRR from capital appreciation alone. The footprint indicates that return calculations do not include reinvested stock dividends. Adding, say, 3-4% yield, increases IRR to 15-16%. But this still does not count spin-offs!

That got me hooked. I tried several other dates for which I knew S&P performance (I write down and track S&P 500 values on days when I initiate new stock positions) with the same result: according to the calculator, FNF has beaten the index convincingly in the long run.

Summing up this piece, I consider FNF a buy but with a caveat. The stock can easily go lower. We already know that Q4 is challenging - just check the last earnings call (though October's mortgage originations were stronger than expected). And Q1 can be no better. We do not know when the tide will turn. I also think that F&G has climbed too fast and can temporarily retreat which should affect FNF negatively. Perhaps, the best strategy is to open a meaningful but not full position and keep adding on weaknesses.

For further details see:

Fidelity National Financial: A Sleeping Beauty Ready To Wake Up