STKS - Fiesta Restaurant Continues To Face Strong Headwinds

2023-07-26 14:33:14 ET

Summary

- Fiesta Restaurant Group has received another Sell rating due to the challenging future for the company, with factors such as a potential economic downturn and a difficult situation in Florida.

- Despite slight improvements in revenues and EBITDA, the company's market value has not appreciated, and the stock has lost significant ground compared to other players in the industry.

- I think the company's financial position is also challenging, with an Altman Z score suggesting a high probability of bankruptcy within a few years, and the company is currently destroying value for its shareholders.

Another Sell Rating for Fiesta Restaurant Group

This analysis reiterates a Sell rating on Fiesta Restaurant Group, Inc. ( FRGI ) stock as I predict an even more challenging future for this casual restaurant business, for the reasons explained below.

On February 15, 2023, my previous analysis supported a Sell rating on shares of Fiesta Restaurant Group - a Texas-based operator of branded Pollo Tropical casual restaurants in Florida and franchised Pollo Tropical restaurants in Puerto Rico, Panama, Guyana, Bahamas, Ecuador and Florida.

The rating was given because the company's profitability was seen to continue to suffer from higher inflation affecting household consumption growth and from the prospect of a sharp downturn in the economy.

How Fiesta Restaurant Group Performs on the Stock Market

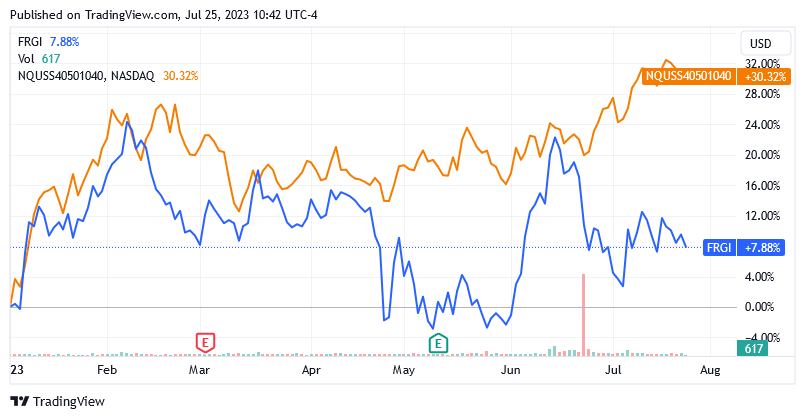

In the meantime, there has been a slight improvement in terms of revenues and EBITDA without this having led to an appreciation of the market value of Fiesta Restaurant's shares.

The stock has lost significant ground relative to many other players in the industry, as shown by the chart below where the YTD performance of US small-cap restaurant stocks is represented by the selected index.

The index is up 30.32% year-to-date compared to FRGI +7.86, and while other restaurants have been much more regular, shares of FRGI have shown a pattern that is not recommended for heart patients.

{kind=link}

This does not mean that this stock is now much cheaper than many operators in the industry, but I think that the market is still not seeing any concrete improvement in the company's profitability, despite management's initiatives.

The future remains highly uncertain as, in addition to the looming recession, of which the weakest growth in the services sector since February is a strong predictor, the picture for Fiesta Restaurant Group is exacerbated by the difficult economic situation in Florida. Indeed, it turns out that Florida's economy is under a combined attack from high inflation, high insurance costs, and a recently passed immigration law that is forcing many workers to leave the State. Florida is indeed where Fiesta Restaurant makes most of its sales.

At this point, with no reason to attract long-term investors, the stock is heavily exposed to short-term factors. The stock plummeted between March and May as a result of the US regional banking crisis and the 25-basis point rate hike on May 3. Then the stock rebounded slightly in June on the back of newfound optimism about the possibility that monetary policy had peaked with rate hikes following the US Fed's decision to take a break at its June 14 meeting. It then pulled back sharply on the prospect of one or more further increases in the cost of money by the end of the year, raising the risk of a recession.

Any improvement in the coming quarters due to seasonal effects as we are in the holiday season may have already been factored into the share price. But what really matters from now on is that the operating environment is going to be quite challenging for Fiesta Restaurant Group's margins, and I think that's going to put negative pressure on the stock price.

How Fiesta Restaurant Performs in a Challenging Context

The parent company of restaurant brand Pollo Tropical on May 10 reported earnings for the first fiscal quarter of 2023 ended April 2, 2023.

It reported non-GAAP earnings per share of $0.02 on revenue growth of 8.1% year over year to $103.4 million, beating analysts by $0.14 million.

The increase in revenues was driven primarily by menu price increases of approximately 10%.

However, the restrictions still in place in the first quarter of 2022 to prevent the spread of the Covid-19 virus may have affected the comparison, making the year-over-year revenue increase appear much more striking than it actually could be.

Furthermore, this type of interference in determining the trend may call into question the company's true ability to pass on a higher operating cost due to inflation to the end consumer.

In terms of earnings released in May , the results were mixed.

During the quarter, the company delivered adjusted EBITDA of $6.5 million for an EBITDA margin of 6.3% of total sales compared to 5.5% in the prior-year quarter, while representing a decline of 80 basis points sequentially.

Net loss from continuing operations was $2.1 million, or a net loss of $0.09 per diluted share, in the first quarter of 2023, which worsened from a net loss from continuing operations of $1.3 million, or a net loss of $0.05 per diluted share, in the first quarter of 2022.

A Profitability that Is Struggling to Gain Momentum amid a Future Fraught with Pitfalls

Of course, the company needs to increase its profitability, but achieving that goal won't be easy in a particularly difficult Florida economic environment.

The company must focus on the freshest, highest quality ingredients when preparing its tropically inspired dishes. In addition, a lot of attention must be paid to the appearance of the building, creating a tropical-smelling atmosphere, and improving the quality and speed of service.

All these important initiatives have become very expensive due to inflationary pressure on raw materials, finished goods, services provision, and the difficulty of finding skilled labour.

Fiesta Restaurant Group will face a much higher operating cost in the future for the factors just mentioned, which must necessarily be passed on to the end consumer.

If it is to succeed with its strategy and be able to increase its profit margin, Fiesta Restaurant Group must raise the price of its freshly prepared tropically inspired menu items.

However, higher pricing is not easy to implement in Florida right now, as the risk of consumers skipping the specialty on the company's menu is being fueled by reduced purchasing power affecting budgets among consumer households.

According to the latest inflation data from the Labor Department, Florida is already the hardest-hit state in the United States as it has the highest cost of living of any state, reports Yahoo Finance . Even cities like Miami and Tampa have inflation between 7% and 7.3%, while the national average in the US is 3% instead.

In addition, there is the labour issue, which is by no means of secondary importance, on the contrary: labor costs account for no less than 70% of the total operating costs of a restaurant company. Improving the quality and speed of service may require an increase in headcount or salary to retain the best skills, despite "reduced hourly and management turnover" that the company sees as a progression toward increased sales and profitability.

Among other things, lower staff turnover may simply reflect a trend that makes today's workers much more attached to their job in a climate that offers no security of finding another job, for example in the event of a layoff. And that poses a big problem for a restaurateur when he may need to find staff quickly at times when a greater influx of customers is expected, even though this type of business is familiar with seasonal factors.

In addition, hospitality businesses could be among the hardest hit in Florida by the reduction in the workforce resulting from the exodus of workers caused by an anti-illegal immigration law that Governor DeSantis signed in May. This action may have been reflected in the negative trend that FRGI's share price had in May.

Plus, one of the biggest cost hikes Fiesta Restaurant Group may face in the future could be the restaurant rent expense which is typically the third-highest cost of running a restaurant.

In the first quarter of 2023, restaurant rental costs accounted for nearly 6% of total operating expenses at Fiesta Restaurant Group, and the item was up 1% year over year.

Not only due to hurricanes and other extreme weather events in Florida, but also the high incidence of fraud and other financial crimes in the real estate insurance market is causing insurance premiums to rise exponentially. The effects may well affect the commercial real estate markets too and given many "years of legal challenges ahead, premiums could go even higher before they start to drift down", says this article from Yahoo Finance.

In addition to the total cost of using the premises, the rent includes various taxes and insurance for the building and contents of the restaurant.

Finally, Dirk Montgomery, who is Fiesta Restaurant Group's president and CEO, states that they have "generated continued traction on G&A efficiency initiatives toward the targeted G&A expense run rate of 8.5% to 9.0% of restaurant sales."

G&A as a share of total revenue was 12.75% in Q1 2023 compared to 15.42% in Q4 2022, but almost unchanged compared to 12.91% in Q1 2022. However, the company is still far from its 8.5% to 9% target, and the sequential improvement could be impacted by the sharp decline in inflation, which fell sharply to an average of 5.8% in Q1 2023 from an average of 7.1% in Q4 2022 thanks to a cut in energy costs.

The context of Fiesta Restaurant is challenging and so is its financial position, which can be summed up by an Altman Z score of 1.60 (scroll down this web page to the "Risk" section) suggesting distress zones and a high probability of bankruptcy within a few years.

The Altman Z-Score measures the likelihood that a company will face bankruptcy problems. If the value is less than or equal to 1.8, the balance sheet is in distress zones, which means a high probability of bankruptcy within a few years. When the ratio is between 1.8 and 3, the balance sheet is in a gray area, which still implies a risk of bankruptcy, albeit moderate. While a score of 3 or higher means that the risk of financial insolvency is extremely low or non-existent.

I believe Fiesta Restaurant Group is not currently creating value for its shareholders, it is destroying it. This negative dynamics can be seen as the company's weighted average cost of capital is 6.56%, while the return on invested capital is -3.74%, according to analysts at GuruFocus.com

The Stock Valuation

Shares of Fiesta Restaurant Group, Inc. ((FRGI)) traded at $7.82 as of this writing giving it a market cap of $210.08 million and a 52-week range of $5.89 to $9.28.

{kind=link}

The company doesn't pay dividends.

The 14-day Relative Strength Indicator at 44.90 shows that the shares still have plenty of room for downside if they want to hit lower levels. In this sense, as seen above, there will be no lack of headwinds for the stock price.

{kind=link}

Compared to its peers based on the fundamental indicator of 12-month EV-to-EBITDA, Fiesta Restaurant Group, Inc. appears expensive at current share price levels.

Fiesta Restaurant Group has a 12-month EV-to-EBITDA ratio of 25.38x.

Red Robin Gourmet Burgers, Inc. ( RRGB ) has a 12-month EV-to-EBITDA ratio of 14.64x.

The ONE Group Hospitality, Inc. ( STKS ) has a 12-month EV-to-EBITDA ratio of 12.12x.

NDLS Noodles & Company ( NDLS ) has a 12-month EV-to-EBITDA ratio of 13.02x.

Potbelly Corporation ( PBPB ) has a 12-month EV-to-EBITDA ratio of 22.88x.

TAST Carrols Restaurant Group, Inc. ( TAST ) has a 12-month EV-to-EBITDA ratio of 19.58x.

Conclusion

This analysis has reiterated a Sell recommendation rating on shares of Fiesta Restaurant Group.

The company needs to work very hard on its key operational initiatives to increase margins if it wants to be liked by the market, but the future is very challenging.

Not only does a looming recession threaten the Fiesta Restaurant Group's business like any other restaurant, but the difficult situation in Florida does not provide a favorable climate either.

I think investors should loosen their position and use the money to bet on other names.

For further details see:

Fiesta Restaurant Continues To Face Strong Headwinds