PCK - Finding Pockets Of Value In This Bull Market

2023-08-21 11:58:03 ET

Summary

- The article evaluates the state of the equity market and suggests areas to invest in that offer relative value.

- Valuations are getting stretched as stocks rise, driven by P/E expansion rather than earnings growth.

- The article recommends investing in the Energy sector, British large-caps, and fixed-income plays, such as investment-grade corporate bonds and munis.

Main Thesis & Background

The purpose of this article is to evaluate the state of the broader equity market and to come up with a few places to put cash to work without grossly overpaying for the shares. I see this as a very relevant discussion to have as we push deeper into Q3 because as 2023 has gone on the market has been doing extremely well. The gains have not been evenly spread out by any means, but we are still seeing healthy returns from each major index within the US (and a similar pattern would emerge if we looked at other developed markets as well):

{kind=link}

With these types of gains, it could be real simple just to ride the wave and hope the momentum carries the indices higher. There is merit to that strategy and I certainly won't be selling off my positions en masse to trigger tax gains when more could be on the way.

But on the other hand, the rapid rise in both the S&P 500 and the NASDAQ have me generally unwilling to deploy a lot of new cash to the funds I own that track them. Rather, I think the time is ripe to get a bit more active with my portfolio and add to sectors/funds/stocks that offer some relative value. That is the purpose of this review - to try to find some value in an increasingly rising market. After some research, I have found three spots that I think will serve me well in the months ahead.

Valuations Getting Stretched As Stocks Rise

The first topic I want to get in to is valuation. As the prior paragraph mentioned - stocks are up big this year for the most part domestically. That is good news for current investors, but what does it say about the future outlook? To me, that is the more appropriate concern for the time being.

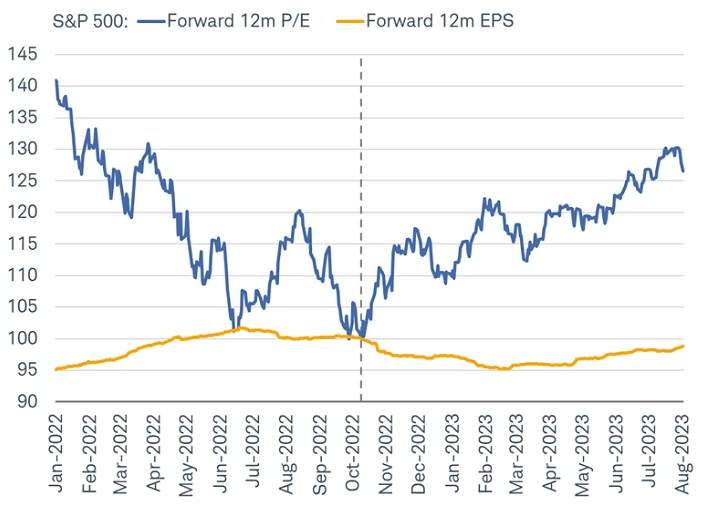

In this regard I am not overly bullish. The problem rests with why stocks have been rising so handsomely. It has been partially because of rising earnings, but the majority of the gains (at least for the S&P 500) are being driven by P/E expansion from the "price" side of the equation:

Valuation Metrics (Charles Schwab)

{kind=link}

What this is showing is that multiples are rising as investors pay up for the same amount of earnings. This pushes the P/E higher because of forward expectations. Investors are willing to pay more today for earning because they hope the future will be brighter. And I am not sure that is completely justified.

If the indices were rising due to earnings, then that is about a bullish a case as one can make. But a market rising on sentiment along rings the contrarian alarm bells. This simple notion suggests that investors should be getting a bit more creative than just index investing going forward and to look for pockets of value rather than paying up for the S&P 500. While that can be easier said than done, I do see a few areas where relative value exists and those are the areas of focus I will discuss below.

Energy Rising On Tight Crude Supply

Area number one for me right now is the Energy sector. This was a big winner in 2022 only to fall victim to a reversal at the start of this year. However, as time has gone on, investors are once again waking up to the fact that the oil market has changed dramatically and top energy producers are set to reap the benefits of rising prices globally. This has occurred largely due to shortages as producers have curtailed supply while the globe has continued to demand oil (imagine that!).

Here at some home (in the US) we see a similar picture. Crude inventories, while still higher than most of 2022, have been falling dramatically over the past few quarters. This is putting upward pressure on prices:

US Inventories (Crude Oil) (Yahoo Finance)

{kind=link}

The takeaway for me is there is value here because Energy rising are rising for the right reasons. Their outputs (what they sell) are getting more valuable. This means earnings are likely to rise over the next few cycles and that is preferable to me rather than valuation expansion like what we are seeing in the broader S&P 500.

In addition, Energy shares remain cheaply valued compared to other corners of the market (and also in isolation). Looking at the sector as a whole, I see a current P/E just over 6!

Current Valuation (Energy Sector Benchmark) (Vanguard) Current Valuation (Energy Sector Benchmark) (Vanguard)

The conclusion I draw is that Energy has a very strong chance of performing well and it has the valuation to draw in new buyers who may have been on the sidelines. This is a win-win for the current environment and is clear to me that "buy" is the right rating here.

*I own the Vanguard Energy ETF ( VDE ) and the iShares Global Energy ETF ( IXC ) and would recommend both as long-term holds.

British Large-Caps Historically Under-Priced

My next stop is across the pond over the United Kingdom ((UK)). This comes at a time when Britain is facing some major challenges. Primary above them are rising interest rates, above-average inflation (compared to other developed countries), and continued uncertainty post-Brexit. While this clouds in the investment climate, a lot of these concerns are clearly baked in to currently share prices. I say this because British stocks are about as cheap as they have been - compared to global stocks - in over a decade:

UK Vs. Developed Markets (FactSet) UK Vs. Developed Markets (FactSet)

Of course, just being "cheap" doesn't make an outright investment case. Stocks can be cheap for good reasons and can always go cheaper. We have to acknowledge that. And as I mentioned above, there surely are plenty of headwinds facing the UK at the moment.

However, there are some bright spots too that tell me the risk-reward proposition is very reasonable going forward. One of them is that wage growth continues to remain high - driven by a tighter labor market in the UK as a whole. This is driven in part by many EU-origin workers leaving over the uncertainty of Brexit. While that has debatable benefits, one of the repercussions is the remaining British workforce has more negotiating power.

Of course, this has been a driver of inflation as well as consumers/households can cope with higher input costs and prices. But a welcomed trend that we are seeing in the market is that rents (called "lets" in Britain) are starting to decline while net earnings are continuing their upside:

Earnings vs. Rents (Britain) (Zoopla) Earnings vs. Rents (Britain) (Zoopla)

I view this as central to continuing to support a strong consumer backdrop. In order for British indices to move higher there needs to be gains in both Consumer Discretionary and Energy sectors because those areas make up a good chunk of the FTSE 100. With earnings growth resilient and rents finally starting to cool, that is good news. And Energy, as discussed in the prior paragraph, has a positive forward outlook as well.

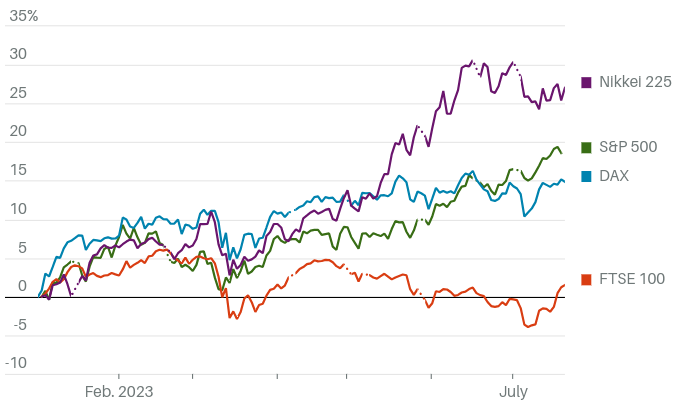

I do want to moderate expectations here a bit. I see the valuation and resilience of the British consumer as tailwinds so I am standing with the "buy" call. But this is not without risk. We have to remember that the FTSE 100 has been a big laggard this year compared to other developed markets and there is no guarantee this won't continue:

Relative YTD Performance (World Bank)

{kind=link}

The point is that simply being "cheap" isn't enough to automatically drive gains. Britain has been cheap for a while and continues to under-perform. Another case in point is Japan. While it is rising handsomely this year and it had been cheap for a very long time without moving the needle. So investors need to be aware of these historical precedents and be patient. But patience has an opportunity cost if the theme continues to under-deliver. So weigh this risk carefully.

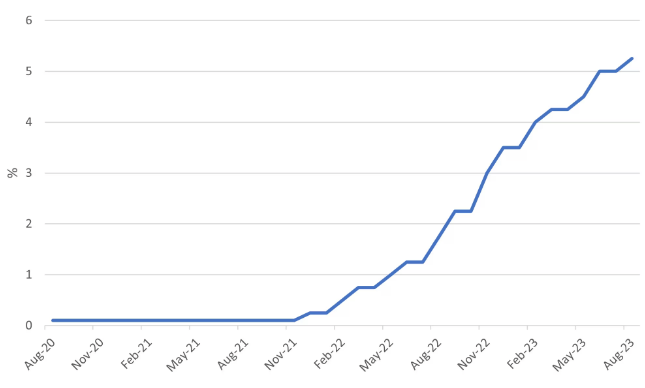

Another reality is that interest rates remain high in the UK just like other developed countries. This is going to limit business investment and will pressure consumers. While I believe the central bank will be proactive if cracks start to emerge, this still remains a very real headwind to consider:

UK's Base Interest Rate (Bank of England)

{kind=link}

The thought process here is to not be a cheerleader. I see some inherent value in British stocks and I think the time may be ripe. But the time has been "ripe" for a while and major structural challenges continue to plague the British Isles. For this reason, while I am bullish on this idea, I want to emphasize that readers need to be well-informed on the downsides risk here as well before allocating their cash to this thesis.

*I own the iShares MSCI United Kingdom ETF ( EWU ) and am considering adding to my position in the near term.

Fixed-Income Plays Piquing Interest

My third area for exposure going forward is fixed-income. I personally prefer exposure to investment-grade corners of this realm, but I see merit to owning some higher yielding munis and select corporate issues as well. The reason being I think we are finally nearing "peak" rates here at home as inflation has finally begun to exhibit meaningful drops:

CPI (US) (US Buruea of Labor Statistics) CPI (USA) (US Bureau of Labor Statistics)

What this signals is that real yields in fixed-income securities will improve as inflation is going to eat away at less of the total return. It also means the Fed is likely to consider holding in its "pause" phase for the remainder of 2023 in my opinion. The sharp decline in inflation means it will be hard to justify continued hikes.

For me personally I like the idea of IG-rated corporate bonds and munis, especially over the expense of US treasuries. As US government spending remains out of control (in my view), I expect a flood of new treasuries to hit the market which makes the returns there subject to plenty of volatility:

Spending on Interest Payments (US Government) (US Bureau of Economic Analysis)

{kind=link}

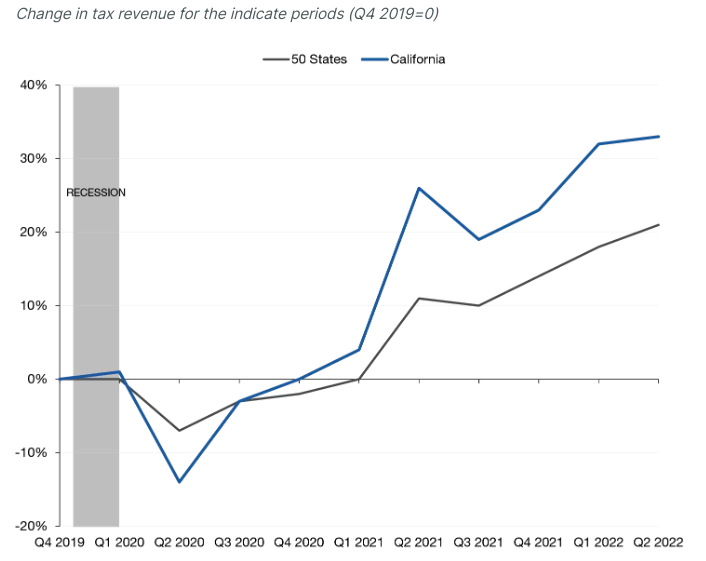

By contrast, state and local governments remain in better shape due to the limits of the amount of borrowing they are able to take advantage of in relative terms. In particular, I like the idea of California munis right now as negative headlines have - in my opinion - overstated the challenges facing the state. In truth, California has seen a greater increase in tax revenue over the past two years than the average US state:

Change in Tax Revenue (Cali vs. US state-average) (Pew Charitable Trusts)

{kind=link}

With tax revenues climbing and these securities having strong credit ratings to begin with, I see value here. While I was cautious on fixed-income positions in 2022 and in 2023, that tide has begun to turn. I still advocate approaching leverage carefully. Many muni funds use heavy amounts of borrowing and the inverted yield curve continues to weigh on that strategy. But individual issues and non-leveraged ETFs have plenty of merit at these levels.

*I own some individual muni issues from North Carolina and am considering buying PIMCO California Municipal Income Fund II ( PCK ). I also believe the unleveraged iShares iBoxx $ Investment Grade Corporate Bond ETF ( LQD ) is a good option for IG corporate bonds and debt.

Bottom-line

The consecutive rises in the major indices have me thinking it is time to get tactical. There is a case to be made for moving some in to cash given the APYs being offered for savings accounts and certificates of deposit. But long-term cash has limited usefulness - we need to earn more to beat inflation. In this light I have highlighted a few areas that I think could drive gains and provide diversification in the latter stages of 2023. While the broader bull market could certainly continue for the S&P 500 and other major indices, I want to protect some gains and not chase returns here. I hope this discussion provides some clarity and food for thought as readers allocate positions for the remainder of the calendar year.

For further details see:

Finding Pockets Of Value In This Bull Market