FBP - First BanCorp: Worthy Of Consideration

2023-09-24 04:34:49 ET

Summary

- First BanCorp has recovered most of its losses from earlier this year and is currently down only 7.6%.

- The company is a financial holding company based in Puerto Rico with branches in the US Virgin Islands, British Virgin Islands, and Florida.

- First BanCorp has seen growth in net interest income and non-interest income, as well as an increase in deposits, but a decrease in net income due to a reduction in net interest income.

- Overall, shares are worth considering given how cheap they are.

Earlier this year, when the bottom fell out for the banking sector in response to the crisis that enveloped the space, practically every player in that market took a beating from a share price perspective. The vast majority of the companies that were hurt during that time have yet to stage a full or even sizable partial recovery. But one exception to this is First BanCorp. ( FBP ). At one point, shares were down as much as 29.8% compared to where they closed February of this year out at. But as of this writing, they have recovered most of that loss and are down only 7.6%. Digging into the bank, I see both positive and negative attributes that investors should be aware of. Truly, I would argue that this is far from being the best prospect on the market. At the same time, however, I do think that it makes for a logical opportunity for some investors, particularly because of the large inflow of deposits the institution recently received and how cheap shares are relative to earnings.

A play on Puerto Rico

First BanCorp operates as a financial holding company that is based out of Puerto Rico. In addition to having its main office located there, it also boasts 59 branches throughout the territory. But that's not the only place that it has a physical presence. According to management, the company also has 8 banking branches in the US Virgin Islands and in the British Virgin Islands. This is in addition to 9 branches that are located stateside in Florida. Through these locations, the institution provides a number of traditional banking services. Examples here include both commercial and corporate banking activities such as the issuance of real estate and construction loans, commercial loans, and other related types of loans. It also provides these customers with cash management and business management services.

Outside of this, the institution also provides mortgage banking that includes the origination, sale, and servicing of residential mortgage products. Retail banking activities like accepting deposits, issuing credit card loans, issuing personal loans, and providing lines of credit, are also in its wheelhouse. The company even has a treasury and investments arm that lends funds to the other aspects of the company.

{kind=link}

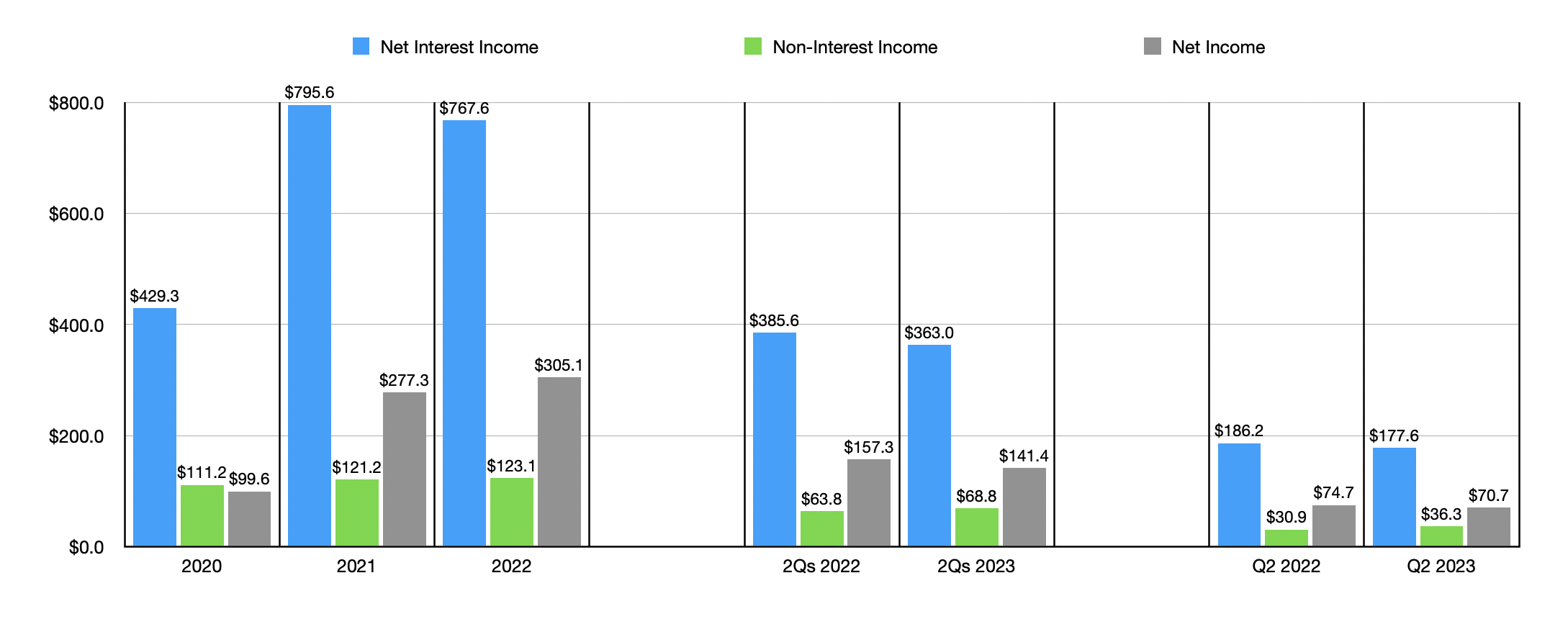

Over the past few years, First BanCorp has seen some interesting results. Net interest income, for instance, expanded from $429.3 million in 2020 to $767.6 million last year. For the current fiscal year, financial performance on the top line has been a bit disappointing. Net interest income during the first half of 2023 totaled $363 million. That's actually down from the $385.6 million reported one year earlier. It is important to note, however, that before factoring in provisions for losses, net interest income would have been higher year over year. The reason for the drop stems from a large swing associated with a provision for credit losses involving loans and finance leases. This, management said, with a swing of $41 million and was driven by a deterioration in forecasted commercial real estate prices, a slightly less favorable economic outlook, and an increase in historical charge off levels associated with consumer loans and finance leases.

Over this same window of time, non-interest income for the company increased consistently year after year, climbing from $111.2 million in 2020 to $123.1 million last year. For the first six months of this year, it totaled $68.8 million. That is slightly higher than the $63.8 million reported the same time last year. Meanwhile, net income has largely grown as well, climbing from $99.6 million to $305.1 million over the past three years. But because of the reduction in net interest income this year, it has fallen from $157.3 million to $141.4 million.

{kind=link}

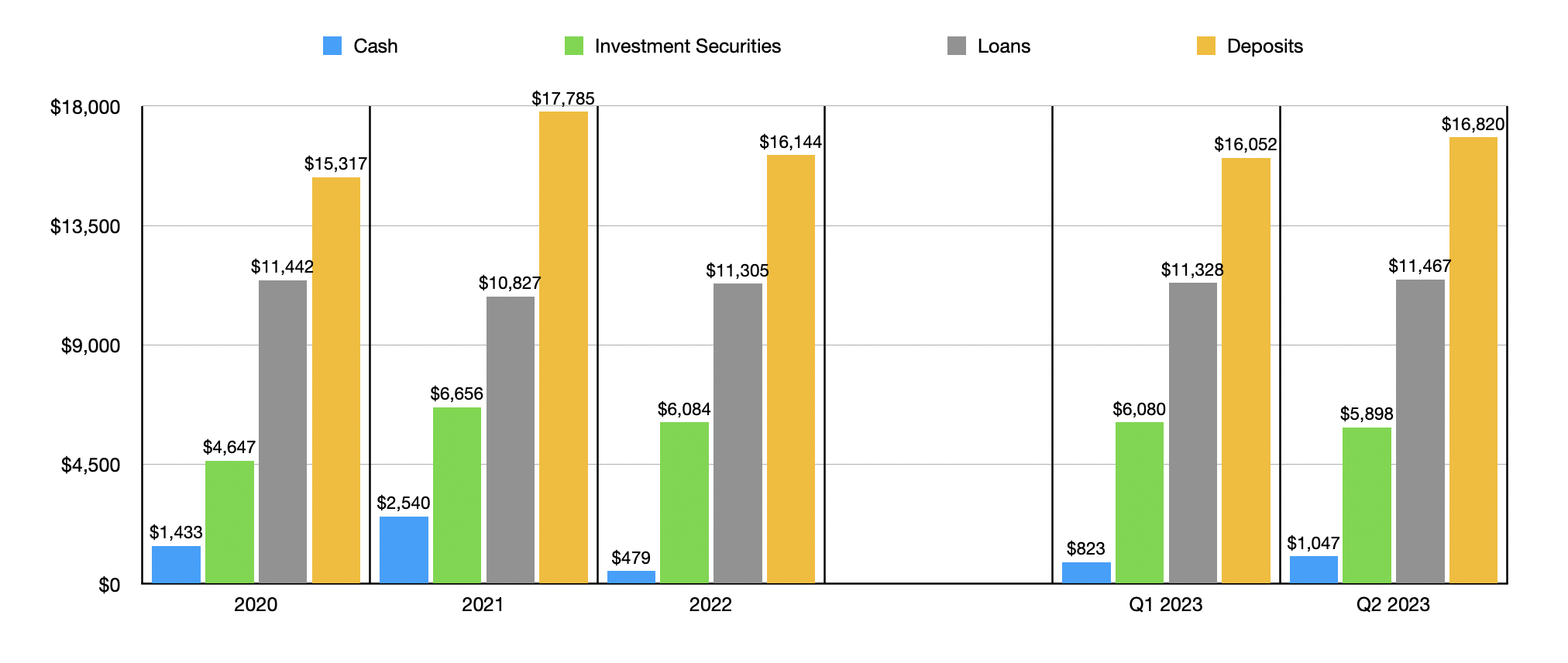

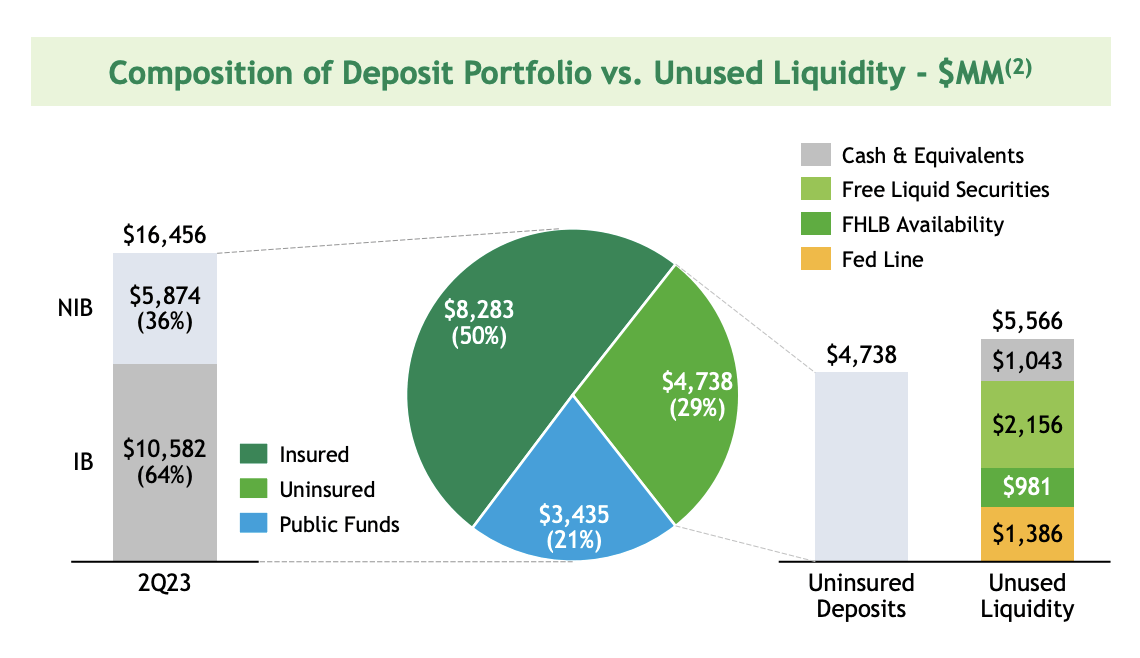

This overall growth has only been made possible by a combination of higher interest rates and, most importantly, larger deposits. Deposits back at the end of 2020 totaled $15.32 billion. By the end of last year, deposits had grown to $16.14 billion. We did see a dip to $16.05 billion in the first quarter of 2023. But that was short lived, with deposits popping up to $16.82 billion by the end of the second quarter. Another good development is that the bank has seen a slight improvement in its uninsured deposit exposure. I understand this is an area that many investors have been concerned about. Personally, I prefer an institution with less than 30% of its deposits classified as uninsured. And First BanCorp comes in right under the wire at 29%. That's a drop from 30% reported for the end of the first quarter. Unfortunately, management has not provided estimates for prior periods. But it's likely that it was higher at the end of last year than it was at the end of the first quarter.

{kind=link}

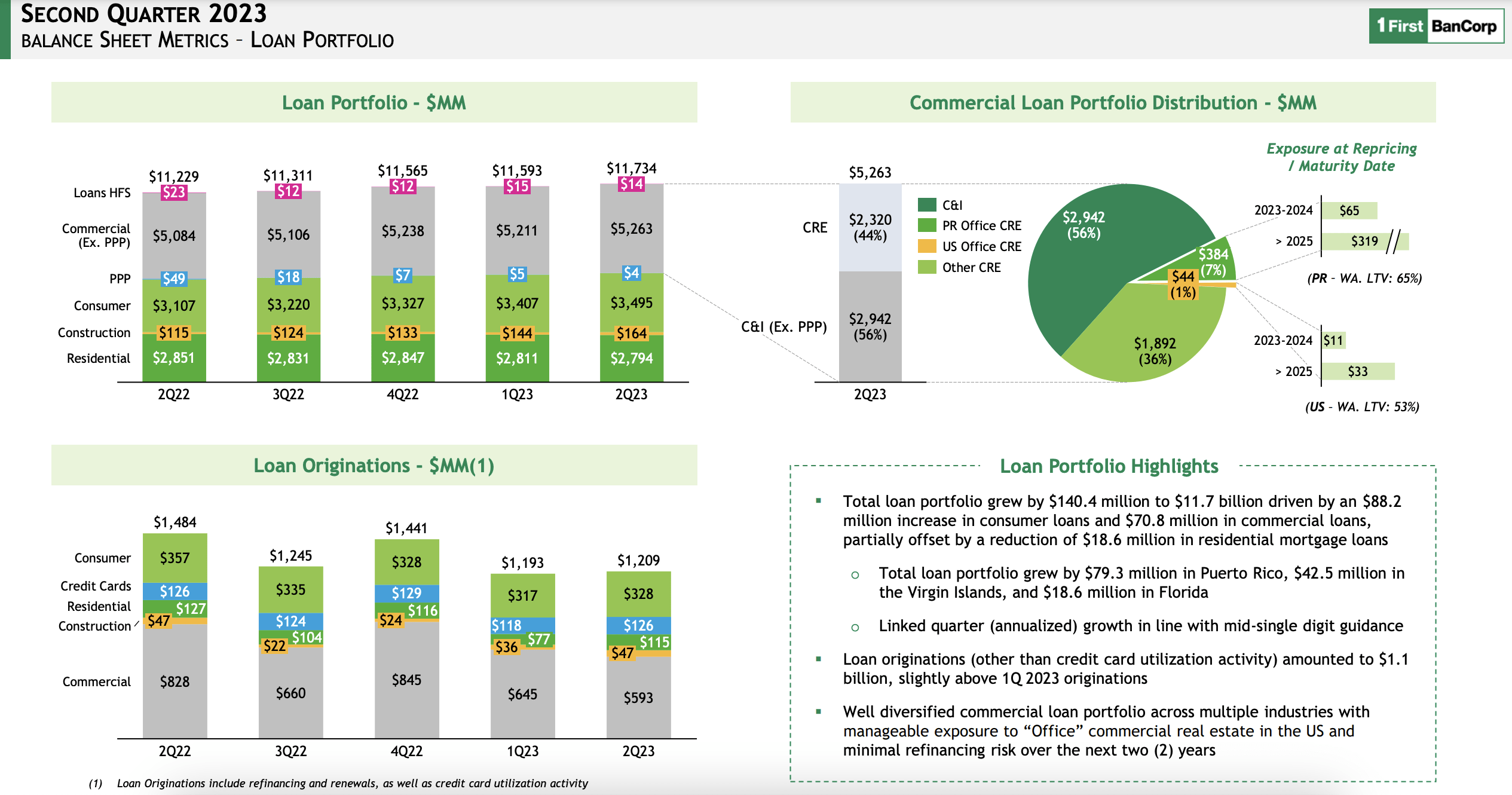

A growth in deposits has allowed the company to increase its other activities. Loan values actually dipped from $11.44 billion to $11.30 billion over the past three years. But we have seen a slight improvement to $11.47 billion by the end of the second quarter. One area of exposure that many investors seemed concerned about involves office properties. And as I have written about in prior articles, there is good reason to be worried. The good news for shareholders here is that only about 3.7% of the company's total loan portfolio, or about 8.1% of its commercial loan portfolio, is in the form of office assets.

{kind=link}

If the growth in activities is not coming from loans, the only place it could be coming from would be investments and cash. Sure enough, that's what we see when we dig deeper. In particular, investment securities went from $4.65 billion in 2020 to $6.08 billion in 2022. They have fallen slightly to $5.90 billion as of the end of the most recent quarter. For context, the largest chunk of these securities, about $2.76 billion in all, is in the form of residential mortgage-backed securities. This is followed very closely by the $2.52 billion associated with US government and agencies obligations. Since the end of 2022, the value of cash on the company's books has also grown, climbing from $478.5 million to $1.05 billion. At the same time, debt has actually dipped from $858.8 million to $661.7 million.

{kind=link}

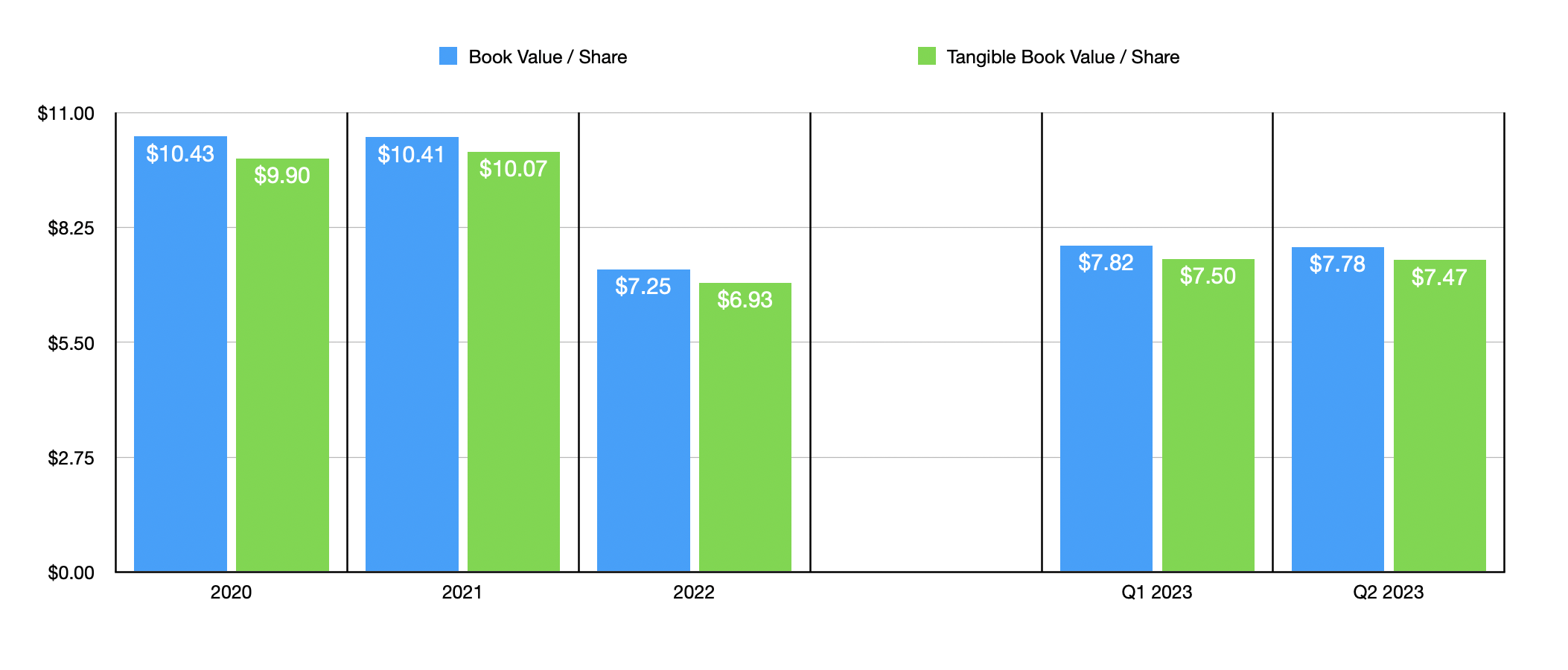

All things considered, First BanCorp looks to be a fairly solid business. Having said that, valuing it is a bit tricky. Interestingly, shares are actually trading at a 72% premium to their book value and at a 79% premium to their tangible book value. Normally, this would indicate a very risky prospect because of how expensive it is. However, it's also important to note that management has bought back a tremendous amount of stock and has not retired those shares. This creates a nifty accounting entry known as a treasury security that reduces the value of book value of equity. In the first half of this year alone, management repurchased $50 million worth of shares. Given this trend, I would say that comparing it to its book value would probably not be the best path to take. Rather, we should compare it to earnings. Using data from 2022, the institution is trading at 7.8 times last year's earnings. That's quite cheap and is lower than the 10.4 reading that the industry is currently going for on average.

Takeaway

When all is said and done, First BanCorp strikes me as an interesting prospect. This doesn't necessarily mean, however, that it is the kind of bank that I would buy. Its overall track record is decent and it's nice to see deposits grow in the most recent quarter. Uninsured deposit exposure is below the threshold I typically look for, which is great. Though the lower this is, the better. Even though the stock has rebounded significantly from its lows, shares do still appear to be trading on the cheap. So because of all of this, I've decided to rate the company a soft ‘buy’ at this time.

For further details see:

First BanCorp: Worthy Of Consideration