SI - First Republic: When Preferred Equity Goes To Zero Part 2

2023-04-29 08:43:06 ET

Summary

- The First Republic preferred shares are down over -70% in the past week.

- Regulators are set to restructure FRC this weekend, either by taking it into receivership or creating a new bridge bank entity to be capitalized by another market player.

- In our opinion, all envisioned scenarios will result in the preferred equity for First Republic to be completely wiped out.

- A bank that only a few days ago recorded a book value of $76.97 per share for its common equity is now facing receivership.

- We have seen similar actions from the FDIC for SVB and Signature Bank, where they announced the restructurings in the weekend, prior to the market open on Monday.

Thesis

We have covered Signature Bank's preferred equity in the past, and highlighted the causes that led to the preferred stock for the entity to go to zero. In our opinion, this weekend will see yet another regional bank restructuring, with the preferred equity for First Republic Bank ( FRC ) going to zero in our humble view.

The 2023 bank runs are like no other. The market knew in the back of its mind when it sold off last year that violently higher rates will have repercussions. It just did not know where to look exactly. It turns out that the accounting concepts of held-to-maturity and available for sale is where it should have focused. The impact of higher rates in the economy was not immediate. It takes 6 to 12 months for rates to percolate through the economy, and now in 2023 we are witnessing the full impact of the Fed's actions last year. From housing and mortgage rates to commercial real estate and regional banks. It is a bit like the dreaded IRS - a light doesn't pop-on when you submit your taxes with an error on them. It takes a while for the system to process all returns and flag problems. It is the same with the economy - right now it is flagging all the issues that zero rates created.

An investor might rightfully ask themselves - how is it possible that a bank that recorded a few days ago a book value of $76.97 per share be in a position to go into receivership this weekend? Make no mistake about it - it is our firm belief that one way or another, we will have some sort of announcement by Sunday evening regarding either a sale or restructuring for FRC.

Why we do not see a full recovery in preferred shares pricing

The Series I shares ( FRC.PI ) from FRC are telling us that the market sees a full attachment here by trading them at $1.96/share. The downfall has been very swift and furious.

Technically, if a suitor just buys the bank via an outright common equity purchase the preferred equity should be back to $25/share. So, if Bank A offers $1 for FRC, and the FDIC pushes the sale through, then the preferred shares in effect will have the same credit profile as the ones issued by Bank A. The problem is that nobody wants FRC. There are a couple of reasons nobody desires FRC presently:

1. Too Big

The bank is just too big, with assets in excess of $150 billion. These are large figures by any measure, making the suitor pool extremely small. There are not a lot of players who can digest such an entity, let alone step-in into a workout situation. We argued in a separate piece that PACW was small enough to be able to work through its problems or find an appropriate suitor. Think about it this way - if you own a beaten-up $2,000 car and you are trying to sell it, you will get a lot of people who will have some sort of interest in it (even if they bid lower than your price). Conversely, if you are trying to sell your 'gently used' Bugatti Chiron , the pool of potential buyers will be very small.

2. Other banks have their own issues

The problems that are plaguing FRC are not singular. Many banks are experiencing the same issues, compounded with fears around credit losses from a potential recession. These are not ideal times for banks to contemplate acquisitions, but rather focus on minimizing credit losses and cleaning up portfolios.

So if FRC will not be acquired outright, then we will probably see a restructuring where the assets and deposits are stripped into a new entity, while the common, preferred equity and bonds will remain in the old one. This is what was done with Signature Bank ( SBNY ):

A bridge bank is an institution that has been authorized by a national regulator or central bank to operate an insolvent bank until a buyer can be found.

A bridge bank is charged with holding the assets and liabilities of the failed bank until the bank becomes solvent again-either through acquisition by another entity or through liquidation.

A bridge bank is usually established by a publicly backed deposit insurance organization, such as the Federal Deposit Insurance Corporation (FDIC), or a financial regulator. In the United States, the FDIC was given authority to charter these temporary banks by the Competitive Equality Banking Act ((CEBA)) of 1987.1

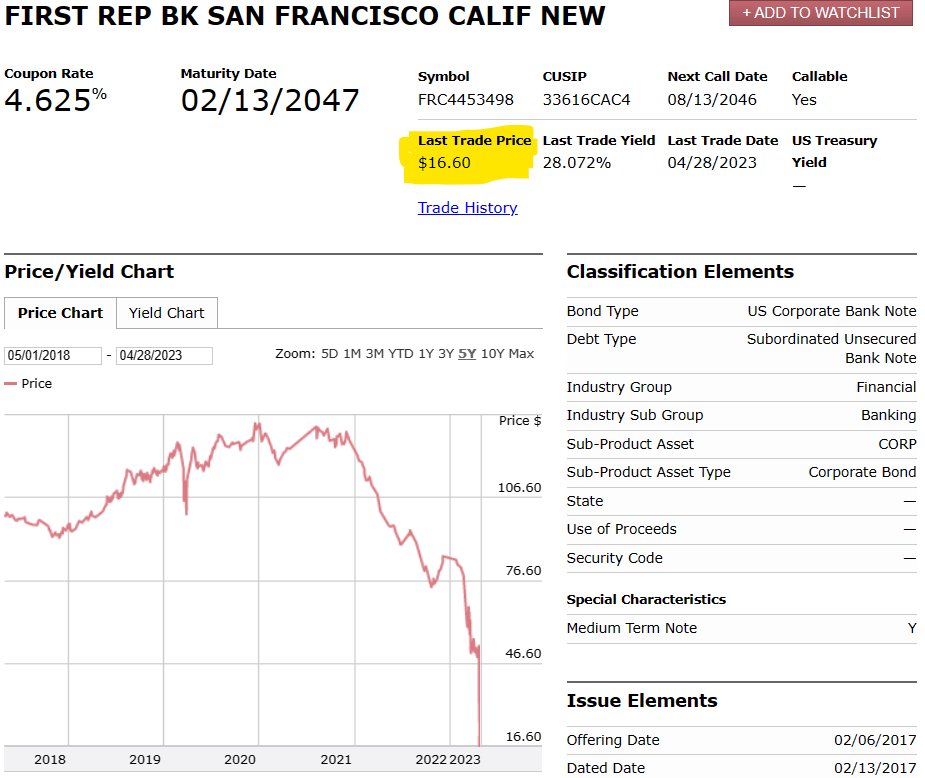

What is the bond market telling us?

The bond market is telling us a similar story:

{kind=link}

We can see above the 2047 Senior Unsecured notes trading at 16 c/$, pretty much being a speculative play right now. If the FRC restructuring takes the format of a bridge entity, expect the senior notes to also move closer to zero.

At the end of the day the FDIC wants to avoid another full receivership , and is not concerned with the preferred equity or debt recovery. As investors in FRC, all forms of capital will suffer impairment. What the FDIC wants to avoid is another hit to its deposit insurance fund, which is down already $22.5 billion on the back of the failed regional banks. That is why we are seeing discussions around pooling equity from several banks to capitalize some sort of bankruptcy remote vehicle where the FRC assets can be dumped.

Conclusion

First Republic is a U.S. regional bank. The entity has come under distress in the past months, and its common equity and preferred shares have been decimated in the past week. We expect some sort of resolution this weekend to the FRC saga, with bids due from several large banks. In a usual take-over proceeding the common equity can get wiped out, but the rest of the capital structure usually survives. Unfortunately there is nothing commonplace about FRC. This is a highly distressed entity which nobody seems to desire. The FDIC has aggressively tried to push for some sort of restructuring, fearing more hits to its insurance fund via a full receivership.

In our opinion, the restructuring here will take the format of a bridge entity, where all the loans and deposits will be placed, while the common stock and preferred equity will be left in the current shell entity. That translates into a zero recovery for the preferred equity, similar to what we have seen for Signature Bank ( SBNY ), Silvergate Bank ( SI ) and Silicon Valley Bank ( SIVBQ ). The capital markets seem to agree, with all forms of FRC investor capital collapsing in price in the past week. Preferred equity used to be a safe way to clip a high yield in the investment grade banking space. Investors should now realize there is actually no subordination for this asset class in a bank run.

For further details see:

First Republic: When Preferred Equity Goes To Zero, Part 2