TPYP - First Trust Energy Infrastructure: A Closed-End Fund's ETF Conversion

2023-12-18 05:10:23 ET

Summary

- First Trust Energy Infrastructure Fund is a pipeline-focused closed-end fund trading at a 5.97% discount to net asset value.

- FIF is set to convert to an ETF in Q2 2024, which will eliminate the discount and potentially provide a 6.38% return.

- Hedging the position can mitigate underlying volatility while accepting the pipeline beta can provide stable returns and monthly distributions.

The end of the year tends to be a great time to pick up a few closed-end funds at a discount. This year, I'd say the picking is particularly good, and the recent rally does not appear to have limited the opportunity set much. I've been looking at a lot of different funds. This one is fascinating, and I've owned it for a while now. First Trust Energy Infrastructure Fund ( FIF ) is a pipeline-focused fund that trades at a modest discount to a net asset value of 5.97%. Pipeline-focused funds are often a wasteland within the closed-end fund space. They seem to trade at significant discounts almost perenially. Here is a graph of the historical discount:

So, why am I interested here just as the discount to net asset value has basically disappeared recently?

Usually, I wouldn't be interested in a pipeline fund at a 6% discount. Not in the least. This article covers some discounts across different types of funds (equity/fixed-income) and discount averages by subtypes. Given current discount levels, I need around a 15% discount on a pipeline fund to motivate me to look a bit closer.

I'm interested here because the fund is converting into an ETF . A conversion from a closed-end fund to an ETF instantly closes the discount. This is supposed to happen during the second quarter of 2024. That means it could happen around April 16, 2024, and near the end of May in a bear case scenario. A 6% discount means as an investor you capture a return of around 6.38% on your invested capital when the discount disappears.

Capturing a ~6% return over the next ~6 months possibly sounds underwhelming to most people. I happen to think it is fantastic especially if you hedge out the underlying and are satisfied with the 6%.

I can also imagine, and I've often done this in the past myself, investors just accept the pipeline beta. Enjoy the 20% leverage, the monthly distributions and the generally stable returns while capturing the 6% bonus at the end of a short ride. It is better to get the 6% hedged, but I'll get into that in a minute.

The fund has $340 million of assets under management. Annualized its distribution is around 7.4%. About 20% of its investments are bought on leverage (this is quite relevant when trying to hedge the position). The fund charges around 3% in expenses. Nearly half of that is related to interest costs.

The reason why I like to own this position hedged is because it allows me to pick up 6% of returns with essentially no capital tied up. I can go long this closed-end fund, short out the underlying, and effectively, this nets out to zero. Meanwhile, the assets I own at a discount to net asset value will start approaching their net asset value or will trade there on conversion. Depending on how sloppy I execute the hedge, there will be minimal variability in the return of this "bet". The 6% sails in quite predictable although not necessarily in a linear fashion. I can add this bet to a portfolio almost without regard for what is already in it or the existing market risk of my portfolio (obviously don't do this).

However, if you go unhedged, the underlying volatility may dwarf the 6%. Perhaps the underlying moves 18% up or 12% down. The 6% is going to provide a strong tailwind to the scoreboard at the end of May but the risk/returns are comparatively very weak. If I add an unhedged position to my portfolio I have to pay a lot of attention to my existing exposures and how this relates and changes my portfolio.

The top 10 holdings of the fund look like this:

| Holding |

| Percent |

| Enterprise Products Partners, L.P. |

| 8.09% |

| Energy Transfer, L.P. |

| 6.60% |

| Plains GP Holdings, L.P. |

| 6.13% |

| Kinder Morgan, Inc. |

| 5.07% |

| DT Midstream, Inc. |

| 4.82% |

| Sempra |

| 4.20% |

| Williams Cos., Inc. |

| 4.17% |

| ONEOK, Inc. |

| 4.16% |

| Hess Midstream, L.P., Class A |

| 2.84% |

| Targa Resources Corp. |

| 2.82% |

The ideal way is to hedge out the underlying portfolio as precisely as possible. The latest quarterly positions are available here . Hedging the underlying out very precisely is probably only something large funds are going to do. Maybe, not even these are bothering. Note that the fund uses 20% leverage to obtain its positions.

I'm currently hedging out my exposure through a pipeline-focused ETF . There are many available like the Alerian MLP ETF ( AMLP ), the JPMorgan Alerian MLP Index ETN ( AMJ ), The First Trust North American Energy Infrastructure Fund ( EMLP ), the Global X MLP ETF ( MLPA ), the Tortoise North American Pipeline Fund ( TPYP ) and the InfaCap MLP ETF ( AMZA ). These are just the ones that have assets over $300 million.

To improve the hedge a lot, it is possible to do correlation calculations on the pipeline ETFs that are out there and go with the highest scoring ones. Also, keep in mind borrowing costs, though. They can be steep.

{kind=link}

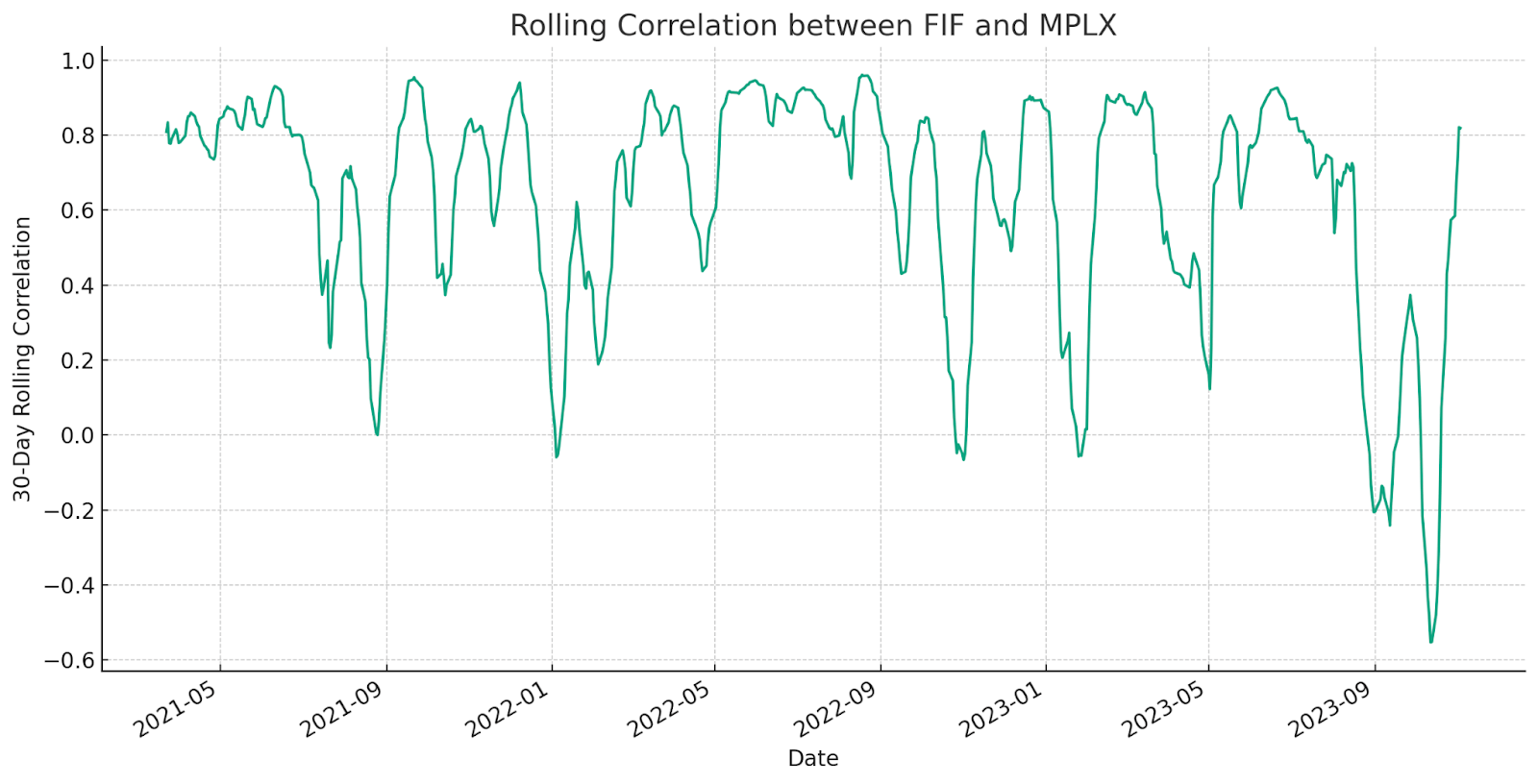

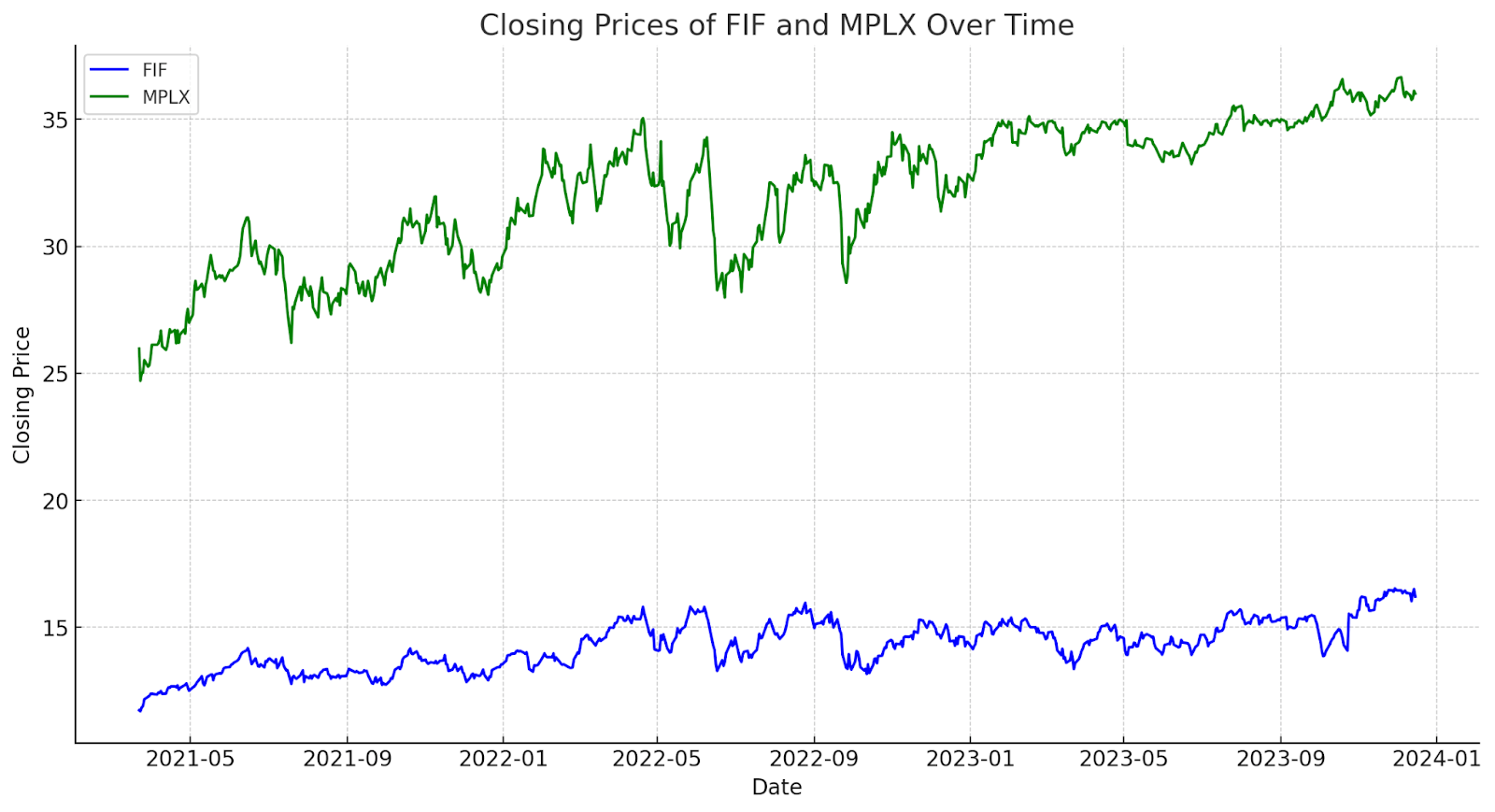

The correlation with MPLX has been decent recently. You may also want to check how it looks in price graphs:

{kind=link}

A mix between ideal and practical could be to hedge out the top-10 positions by hand and hedge out the balance through an ETF.

When I initially wrote up this idea it traded at a 7.4% discount to net asset value. I'm surprised the discount has not come in further yet. This remains a rare opportunity to pick up uncorrelated returns as this fund transitions from a CEF to an ETF. Hedged, this looks like an approximate 6% return as the fund's discount to net asset value disappears. While usually pipeline funds deserve much larger discounts, FIF's imminent conversion makes the 6% discount hard to ignore. I prefer to hedge the position. For investors more comfortable with market/industry volatility, accepting the pipeline beta and enjoying the monthly distributions can be fine.

For further details see:

First Trust Energy Infrastructure: A Closed-End Fund's ETF Conversion