FWRG - First Watch: Another Strong Quarter Amid Tough Macro Backdrop

2023-12-11 12:25:44 ET

Summary

- First Watch reported impressive Q3 results despite the tough macro backdrop, with record revenue, positive dining room traffic, and 15% system-wide sales growth.

- Meanwhile, commodity deflation and menu pricing helped to offset higher labor costs, with First Watch reporting continued growth in restaurant level margins and significant earnings growth.

- In this update, we'll look at First Watch's Q3 results, recent industry-wide trends and whether it's worth paying up for the stock after a strong reaction following Q3 results.

The Q3 earnings season for the restaurant industry is finally over and we saw mixed results. Evidence of this came from weak reports from Dine Brands ( DIN ) and Cracker Barrel ( CBRL ) offset by a solid performance from several quick-service names. That said, First Watch Restaurant Group ( FWRG ) was clearly an exception in the casual dining space, maintaining positive dining room traffic, reporting high double-digit revenue growth, and enjoying a 140 basis point improvement in margins. In this update, we'll look at First Watch's Q3 results, recent industry-wide trends, and whether this growth stock is worth chasing after a strong reaction following Q3 results.

{kind=link}

First Watch Menu Offerings - Company Website

Q3 Results

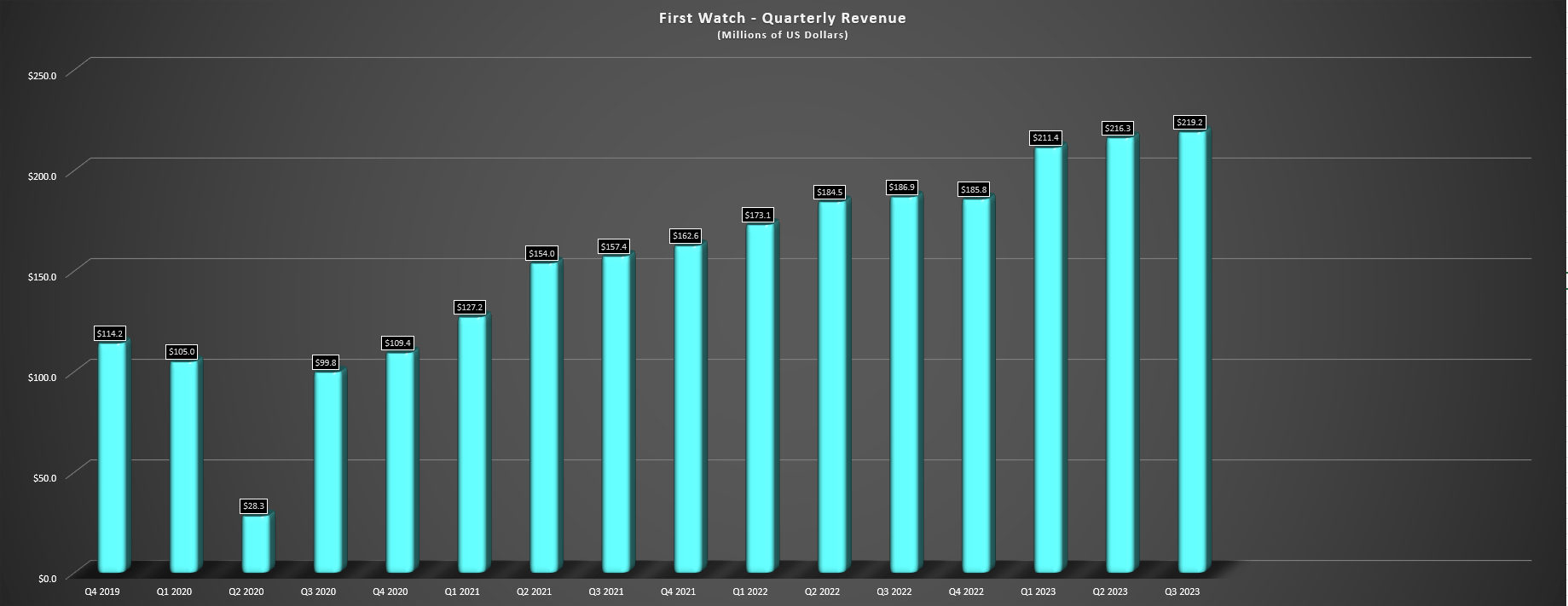

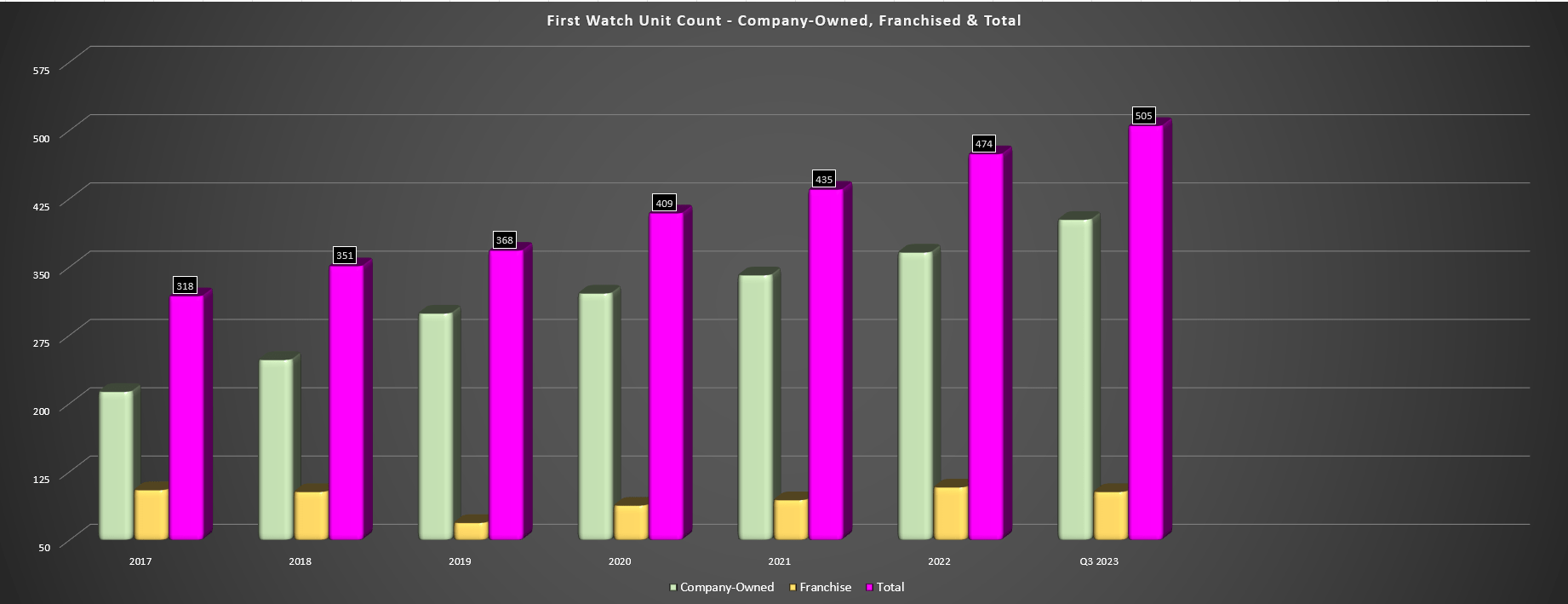

First Watch Restaurant Group ("First Watch") released its Q3 results last month, reporting record revenue of $219.2 million (+17% year-over-year), net income of $5.4 million (Q3 2022: ~$0.05 million), and hit the 500 restaurant milestone in the quarter. Meanwhile, system-wide sales ticked up to $270.3 million (+15% year-over-year) on the back of franchise acquisitions and the company landed on Newsweek's Top 100 List for a second year in a row for Most Loved Workplace, a competitive advantage from a retention standpoint in an industry with historically high turnover. The impressive sales performance was attributed to same-restaurant sales growth of 4.8% offset by negative 1.9% traffic growth, translating to a minor deceleration in two-year same-restaurant sales (16.8% vs. 21.2% in Q2 2023) and traffic sequentially (traffic fell 70 basis points from 1.2% to 1.9%).

{kind=link}

First Watch Quarterly Revenue - Company Filings, Author's Chart

Although the negative traffic may concern some investors, it's important to note that First Watch is trouncing its peers with 400 basis point outperformance according to Black Box Intelligence, highlight traffic share growth. It's also worth noting that dining room traffic remains positive, but the drag on First Watch's traffic is coming from off-premise (increased from ~5% of sales to ~18% of sales as of Q2 2023). The company noted previously that this is expected and the results are not surprising given that it's the highest-ticket occasion and simultaneously offers the least experience. Still, it is extremely impressive that First Watch is remaining at positive on-premise as this is a clear divergence from its peers in the casual dining space and even at many quick-service concepts.

Looking at the results from a margin standpoint, First Watch delivered here as well. This was evidenced by 18.7% restaurant level margins, with the company benefiting from lower avocado and pork prices plus menu pricing that provided 220 basis points of leverage on food & beverage costs, in addition to lower to-go supply costs and lower insurance costs which allowed for leverage in its other expenses category. The 270 basis points in gains here were partially offset by a 60 basis point loss hit on labor (33.3% vs. 33.9%), with the culprit being more managers per restaurant (up from 2.8 to 3.1) and wage increases. However, with manager and employee turnover improving and clear market share growth, the company appears to be doing lots right as these investments are paying off both from a staffing and sales standpoint.

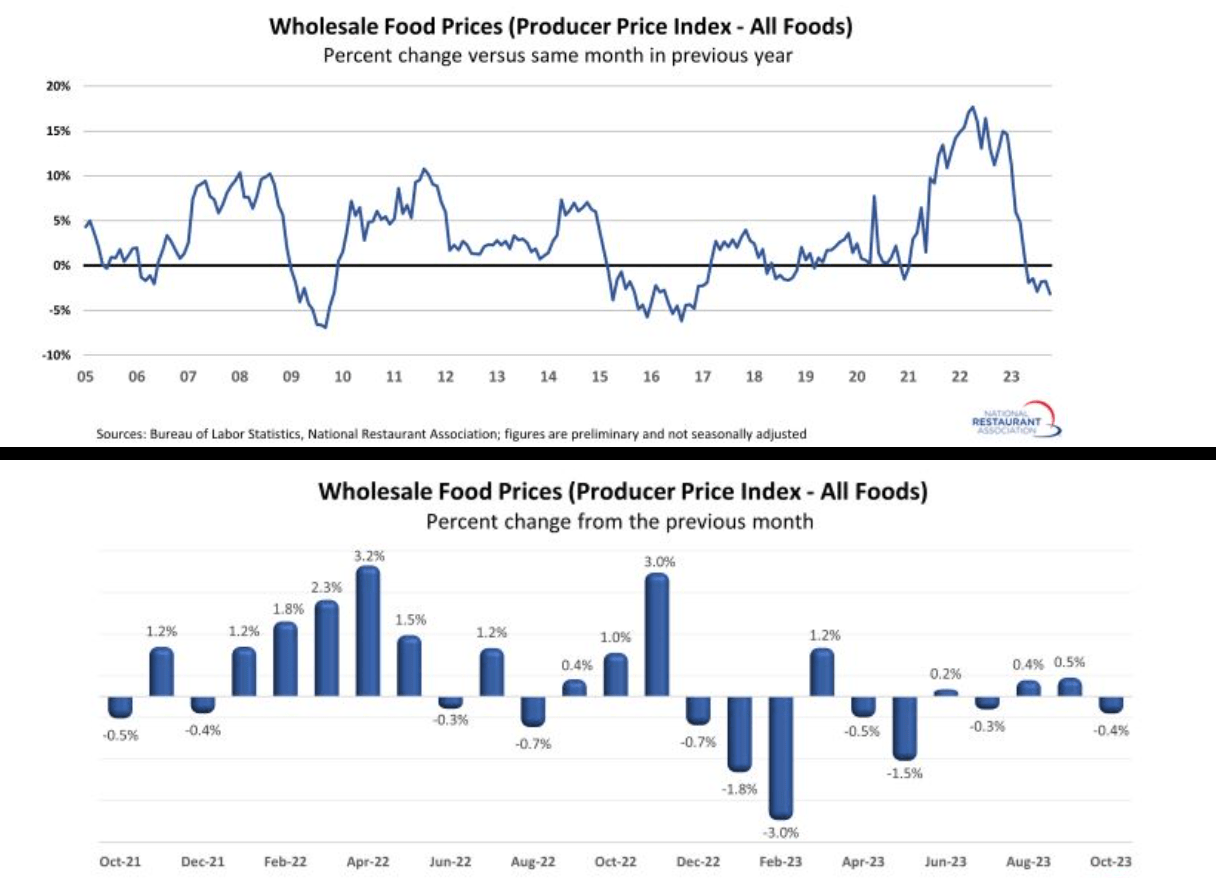

As the chart below highlights, wholesale food prices have continued to decline, with First Watch benefiting from this trend, unlike its higher beef incidence peers that continued to get hit with significant beef inflation (27% year-over-year in October).

{kind=link}

Wholesale Food Prices - National Restaurant Association, BLS

Finally, as for the financial results and guidance, First Watch saw net income soar to $5.4 million ($22.7 million year-to-date), and has revised its guidance to $91.0 to $92.0 million in adjusted EBITDA, up from $76.0 to $81.0 million previously. This is despite continued development delays reported industry-wide and called out by First Watch, offset by franchise acquisitions during the year, which included an additional six franchises acquired in Florida after quarter-end. Last, same-store sales guidance has been increased to 7-8% (but with flat traffic) vs. 6.8% with positive traffic initially. I don't see the revision to the traffic guidance as that meaningful given that it has been a brutal year with traffic outperforming expectations for many casual dining restaurants.

Industry-Wide Trends & Recent Developments

Moving over to industry-wide trends, traffic has remained negative based on seated diners' growth from OpenTable, and this is despite the persistent decline in gas prices that often provides a tailwind for industry-wide traffic (more disposable income with less pressure on wallets). This may mean that consumers are more tapped out than they were last year when the pullback in gas prices led to improving traffic, and this somewhat jives with First Watch's slightly less upbeat comments with it stating:

"While we have observed and in fact benefited from the strength and resilience of the consumer throughout the year, there's reason to believe that the weight of the environment is beginning to have an impact, but as we have experienced in prior downturns, consumers are less willing to gamble with their discretionary dollars and would rather seek out more familiar and enjoyable experiences that are consistent and deliver value like First Watch."

- First Watch, Q3 2023 Conference Call

{kind=link}

In addition, when asked about the industry seeing some softness and whether it could balance its own results against this through October, First Watch stated:

"Well, we've consistently talked about our traffic particularly where the off-premise traffic is concerned that we've seen that kind of seeking a new home. I don't know exactly where it's going to land at some point, but that traffic has descended throughout the year, while our dining rooms have remained positive. They're probably less positive in the third quarter than they were earlier in the year. So there is a -- there is that -- there is some downward pressure, and I think that's what First Watch is seeing and that's what the industry is seeing."

- First Watch, Q3 2023 Conference Call

This commentary suggests Q4 may be a little below plans, and this would correlate with Black Box data, which suggested that Florida was the worst-performing region in October (~25% of FWRG's system is in Florida), which could have something to do with lower traffic due to record heat. That being said, First Watch has continued to reaffirm that it is seeing no indications of check management, and the only indicator of check management is declining off-premise incidences which suggests that consumers are pulling back on the most expensive way of dining. In addition, its mix remains positive according to the company, with it benefiting from continuous menu innovation and trade-ups into LTOs that are seeing strong guest reception. Therefore, any potential softness in Q4 is likely a short-term blip, but not indicative of any market share losses.

In summary, the results were overwhelmingly positive, and certainly far better than the commentary we're getting out of many other casual dining brands in Q2/Q3.

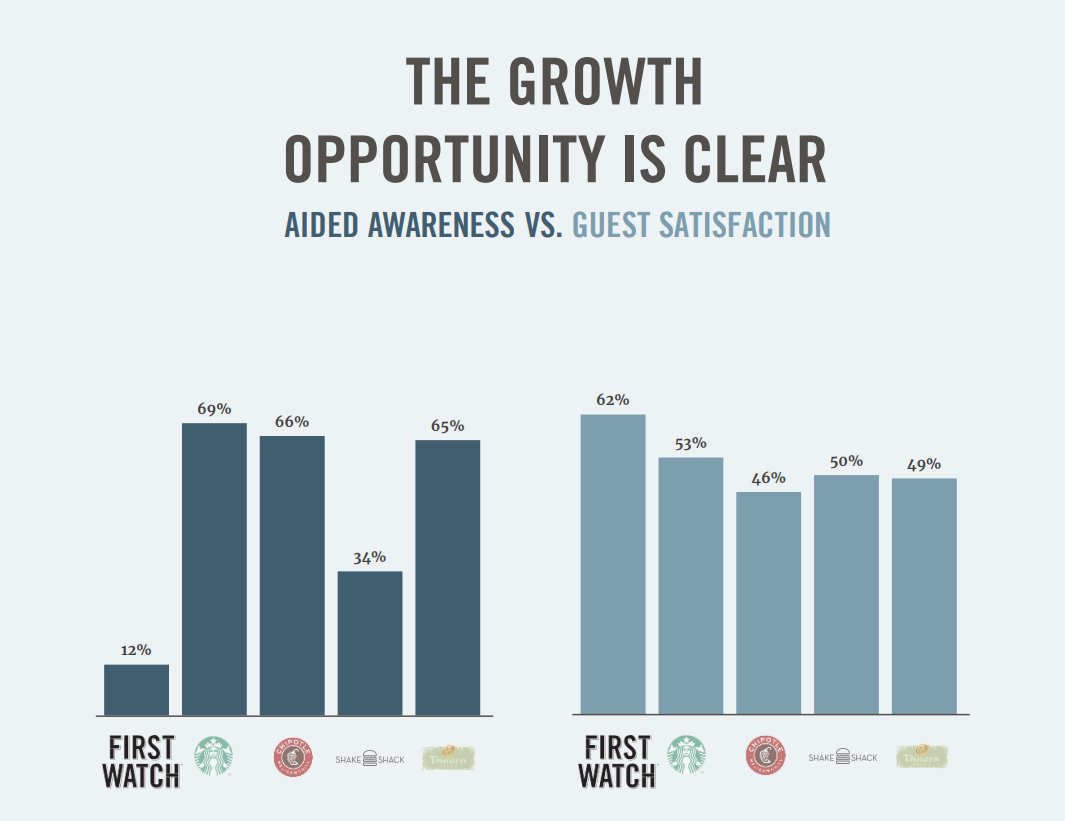

Finally, looking at First Watch's long-term growth, the below chart shows First Watch as a clear leader vs. several iconic brands in guest satisfaction despite low aided awareness, an impressive feat. This statistic certainly supports the company's ability to grow traffic share and its overall units long-term even with other brands like Denny's promoting more heavily ($5.99 Grand Slam), and with less than one-fourth of its ultimate 2,200 restaurant goal currently, First Watch could make for a solid long-term outperformer vs. other casual dining names for patient investors if purchased at the right price . Let's look at the valuation below and see whether FWRG is offering an adequate margin of safety.

Aided Awareness & Guest Satisfaction vs. Other Iconic Brands - Company Presentation, Technomic 2022

{kind=link}

First Watch - Total Restaurants - Company Filings, Author's Chart

{kind=link}

Valuation

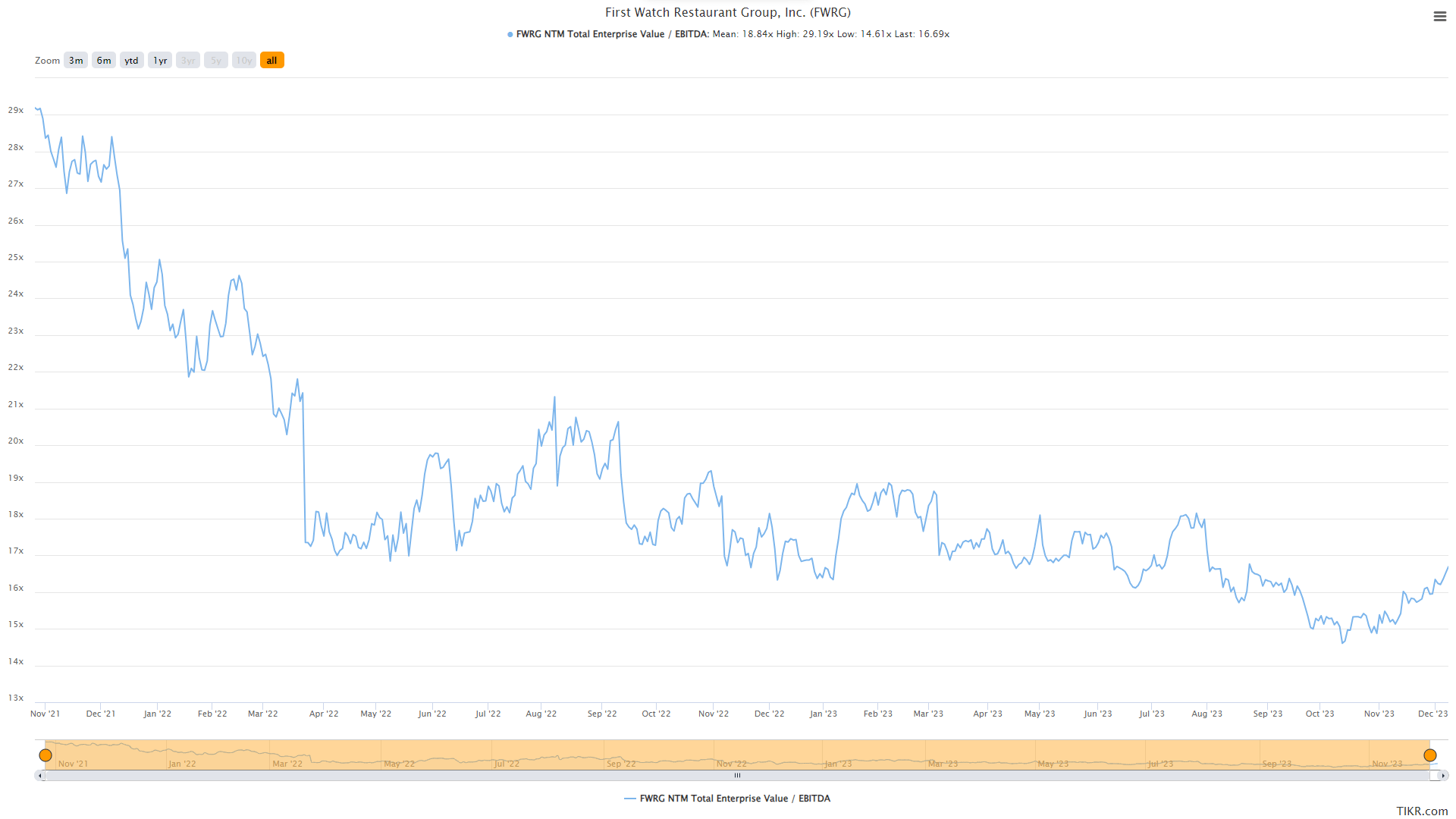

Based on ~59.8 million shares and a share price of $19.30, First Watch trades at a market cap of ~$1.15 billion and an enterprise value of ~$1.67 billion, and it remains the only restaurant IPO recently to hold on to most of its first day IPO gains vs. names that have suffered significant drawdowns like Dutch Bros ( BROS ), Portillo's ( PTLO ), Sweetgreen ( SG ), and CAVA Group ( CAVA ). Meanwhile, the stock trades at a reasonable valuation given its impressive execution (consistently over-delivering on promises), sitting at just ~16.0x EV/EBITDA estimates vs. names like Dutch Bros at over 35.0x EV/EBITDA with far worse execution. And as we can see below, FWRG trades at the lower end of its EV/EBITDA multiple since going public, with an average multiple of ~18.8x.

{kind=link}

First Watch Historical EV/EBITDA Multiple - TIKR.com

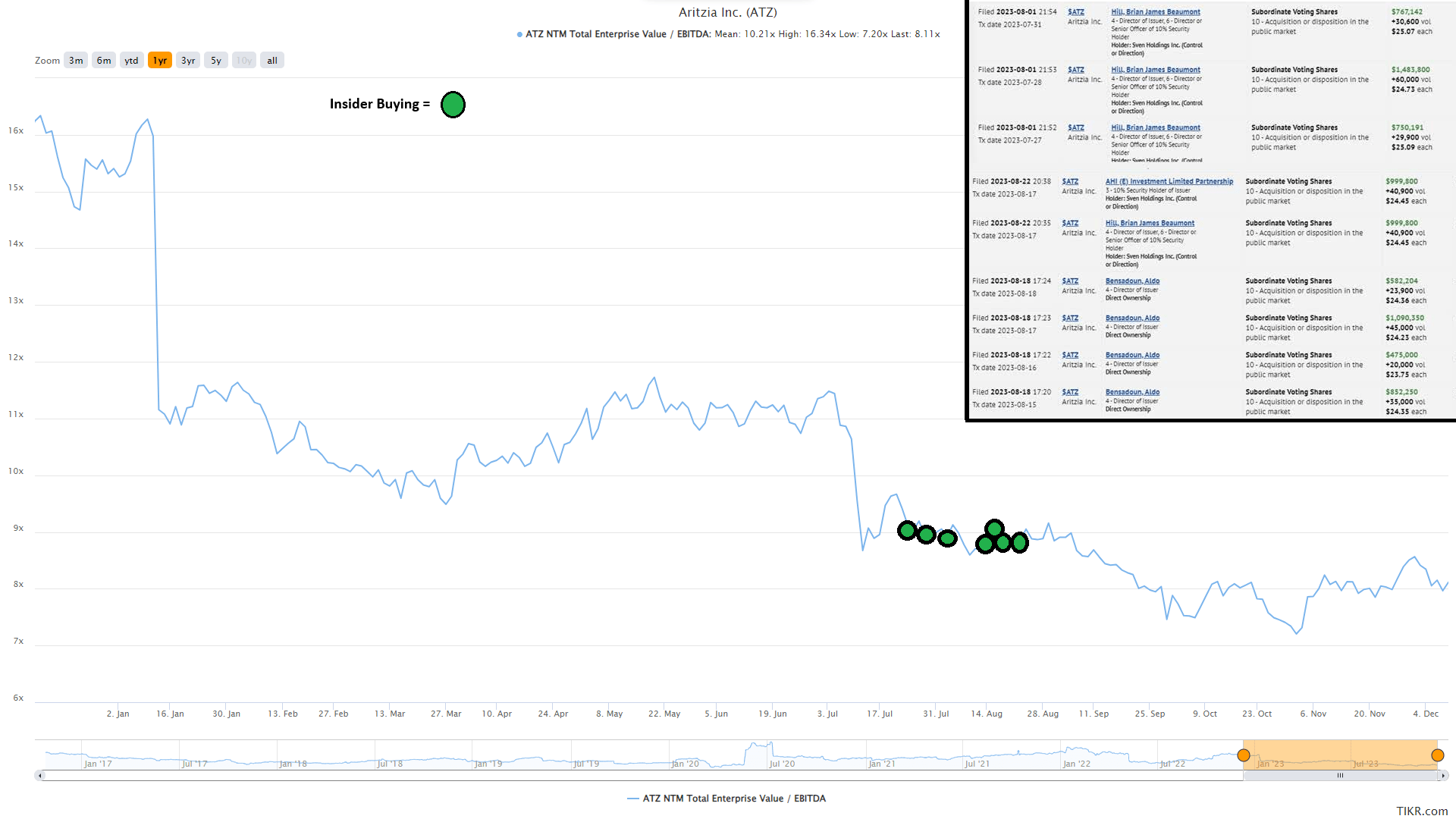

However, while this is a discount to its average multiple, I believe to be a more conservative multiple of 16.5x EV/EBITDA and FY2024 estimates of $105 million, translating to a fair value for First Watch of $20.30. In addition, I am looking for a minimum 30% discount to fair value to ensure an adequate margin of safety when starting new positions in small-cap growth stocks, implying a low-risk buy zone of $14.20 or lower after applying this discount. So, while First Watch remains one of the more reasonably valued growth stories in the sector relative to names like CAVA Group and Dutch Bros, I still don't see enough of a margin of safety just yet. Plus, with high-growth names like Aritzia ( ATZ:CA ) trading at half the multiple on CY2024 estimates with significant insider buying, I continue to see more attractive bets elsewhere from a valuation standpoint.

{kind=link}

Aritzia Valuation & Insider Buying - SEDI Insider Filings, TIKR.com

Summary

First Watch reported another impressive quarter in Q3, has continued its industry-leading growth with the help of franchise acquisitions, and continues to grow market share with incredible AUVs considering its one 7.5 hour shift. Meanwhile, guest satisfaction sits at industry-leading levels, likely because of under-pricing relative to peers (value proposition), and the company is still in the early innings of its growth story relative to its long-term potential. That said, the stock is trading at ~16.0x forward EV/EBITDA which I would consider close to fair value, and some of this growth is now starting to look priced into the stock. Hence, while I see it as one of the best run names in the full-service space, I would view any rallies above $21.00 before February as an opportunity to book some profits.

For further details see:

First Watch: Another Strong Quarter Amid Tough Macro Backdrop