FE - FirstEnergy: Continuing To Deliver On The Thesis

2023-11-07 01:06:24 ET

Summary

- FirstEnergy reported mixed Q3 2023 earnings, beating earnings expectations but missing revenue expectations.

- The company's stock price dropped after the earnings release but has seen a 9.55% increase over the past month.

- FirstEnergy delivered growth in revenue, operating income, and net income, reaffirming its long-term guidance for earnings per share growth.

- The company continues to rely much more heavily on debt than its peers, which has not been a problem yet but could be one long term.

- FE stock may have gotten ahead of itself, as it currently looks expensive relative to its peers.

On Thursday, October 26, 2023, regulated electric utility FirstEnergy Corp. ( FE ) announced its third quarter 2023 earnings results. At first glance, these results appeared to be mixed as FirstEnergy missed analysts' revenue expectations but still managed to beat them in terms of earnings. As most investors consider earnings to be somewhat more important than revenue, this is a positive sign.

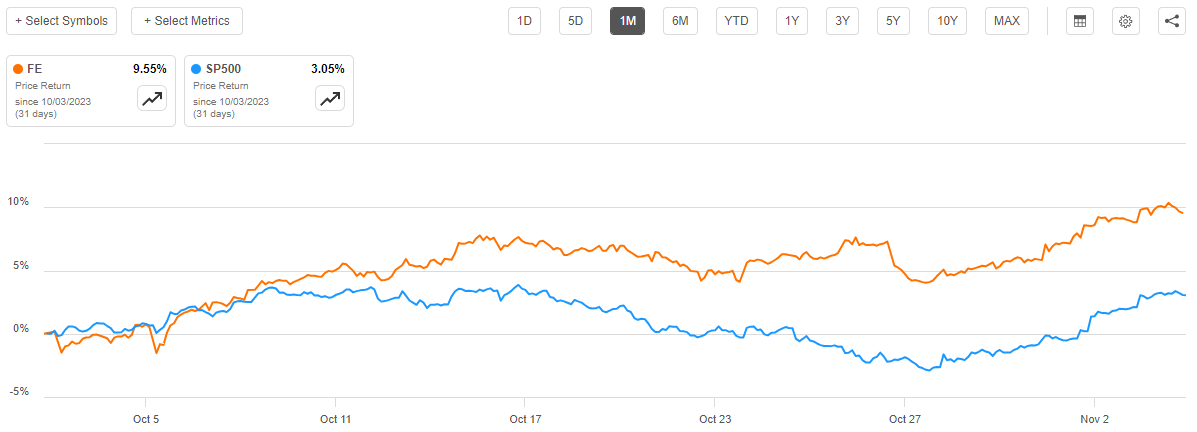

The market certainly seemed to be somewhat mixed with FirstEnergy's results over the past month. The company's stock price did drop in the trading session that immediately followed the release of these results. However, the stock is up 9.55% over the past month. That substantially beat the S&P 500 Index ( SP500 ) over the period:

{kind=link}

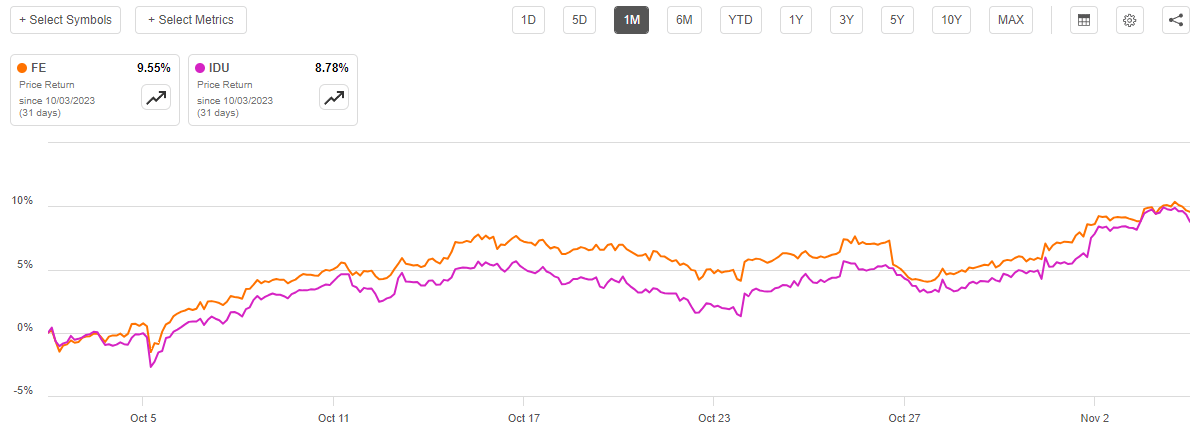

This was generally a very good performance from FirstEnergy, particularly considering that the utility sector in general has been struggling over the past several months due to it acting somewhat as a bond proxy. The sector did do okay in October though, but it still underperformed FirstEnergy's stock price performance. Here is the past thirty days' chart showing FirstEnergy's stock price against the iShares U.S. Utilities Index ( IDU ):

{kind=link}

When we consider that FirstEnergy has been somewhat more troubled than many other utilities over the past several years, that is certainly an impressive performance.

Let us take a look at FirstEnergy's third quarter results and see if purchasing the stock makes sense today.

Earnings Results Analysis

As regular readers are no doubt well aware, it is my usual practice to share the highlights from a company's earnings report before delving into an analysis of its results. This is because these highlights provide a background for the remainder of the article as well as serve as a framework for the resultant analysis:

- FirstEnergy reported total revenues of $3.4870 billion during the third quarter of 2023. This represents a 0.35% increase over the $3.4750 billion that the company reported in the prior year quarter.

- The company reported an operating income of $715.0 million in the most recent quarter. This represents a 17.21% increase over the $610.0 million that the company reported in the year-ago quarter.

- FirstEnergy reported that weather-adjusted deliveries to its customers increased by 1.2% year-over-year. This was primarily driven by increases in commercial and residential consumption, as industrial consumption remained unchanged.

- The company reaffirmed its long-term guidance of delivering 6% to 8% earnings per share growth annually.

- FirstEnergy reported a net income of $400.0 million during the third quarter of 2023. This represents a 19.76% increase over the $334.0 million net income that the company reported during the third quarter of 2022.

It seems essentially certain that the first thing that anyone reviewing these results will notice is that FirstEnergy generally delivered across-the-board performance increases in revenue, operating income, and net income. This is in line with the company's typical pattern of delivering relatively slow year-over-year growth. This chart shows the company's revenues from the last ten full-year periods as well as the trailing twelve-month period:

{kind=link}

As we can clearly see, FirstEnergy has generally been delivering growth over the past few years, although the pandemic did slow it down a bit. The general trend still points to year-over-year revenue growth, however.

We can see that the pandemic itself did not cause a huge decline in the company's revenues. This is also to be expected, as electric utilities like FirstEnergy tend to be reasonably well insulated from disruptions in the general economy. I explained why this is the case in my previous article on FirstEnergy:

The reason for this general stability over time is that FirstEnergy provides a product that is generally considered to be a necessity for our modern way of life. After all, who among us does not have electric utility service to our homes and businesses? Indeed, how many of us know someone who does not have this service? As such, most people will prioritize paying their utility bills ahead of any discretionary expenses during times when money gets tight.

This is a characteristic that can certainly be appreciated right now. One of the reasons why the market went up over the past week is because various participants in the market are expecting that the United States will enter a recession that forces the Federal Reserve to cut interest rates. One of the characteristics of a recession is that many people have less capacity to engage in discretionary spending and thus cut back. However, they are still likely to pay their electric bill straight through the recession. Thus, FirstEnergy should be better positioned to handle economic weakness than many other companies that trade in the public markets.

We also see above that FirstEnergy has managed to deliver a certain amount of growth over the period, albeit a limited amount. This is also something that we expected to see. After all, FirstEnergy has been actively working to increase its rate base. I explained the concept of rate base in various previous articles. To paraphrase myself:

The rate base is the value of the company's assets upon which regulators allow it to earn a specified rate of return. As this rate of return is a percentage, any increase to the rate base allows the company to raise the prices that it charges its customers in order to earn that allowed rate of return. The usual way through which a company increases its rate base is by investing money into upgrading, modernizing, and possibly expanding its utility-grade infrastructure.

FirstEnergy Corporation has been investing money into expanding its rate base. The company currently is in the middle of a $12 billion capital investment plan that is devoted to this purpose, which is to be carried out over the 2023 to 2025 period. FirstEnergy was originally planning to invest $3.4 billion this year into upgrading its infrastructure, but the company increased this spending along with its results announcement. It now plans to spend $3.7 billion this year, which should speed up its near-term growth somewhat over the previously presented spending level.

The company is expecting its full-year operating (non-GAAP) earnings per share to come in at $2.49 to $2.59 per share, of which $0.55 to $0.65 per share will come in the fourth quarter. The company reported $1.95 year-to-date:

| Q1 2023 |

| Q2 2023 |

| Q3 2023 |

| Operating Earnings Per Share |

| $0.60 |

| $0.47 |

| $0.88 |

Thus, if the company reports $0.55 to $0.65 per share in the fourth quarter, it will come in somewhere in the projected range. That would also represent a slight increase over the $2.41 per share that the company reported for the full-year 2022 period. Thus, we can see that FirstEnergy's growth story generally remains intact.

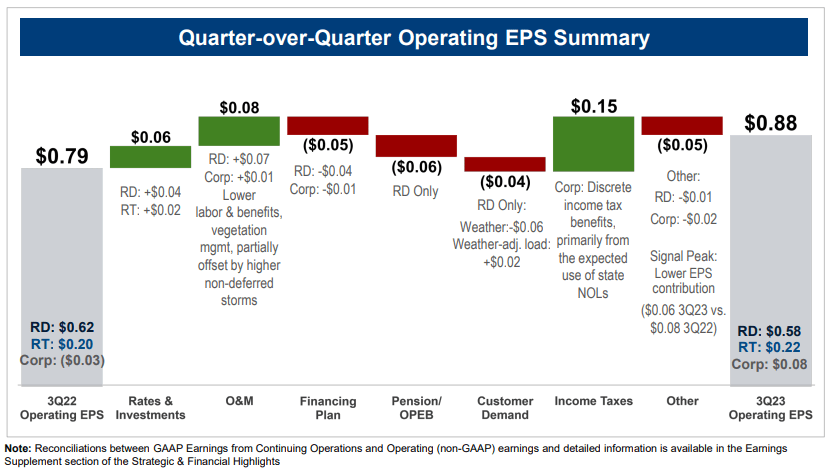

FirstEnergy delivered some earnings per share growth during the most recent quarter. The company reported operating earnings per share of $0.88 per share in the quarter, which was an 11.39% increase over the company's $0.79 operating earnings per share last year. This was partly caused by the company's investment in its rate base, which boosted earnings per share by $0.06 year-over-year:

{kind=link}

In short, the company seems to be on track so far to meet its guidance, which of course represents a year-over-year increase.

Overall, the company is continuing on with the thesis that we discussed in various previous articles, which is a positive sign.

Financial Considerations

As I pointed out in my last article on FirstEnergy:

One of FirstEnergy's largest problems is that the company is much more reliant on debt to finance its operations than its peers. We can see this by looking at the net debt-to-equity ratio, which tells us the degree to which the company is financing itself with debt as opposed to wholly-owned funds.

We have seen in various past articles that FirstEnergy has a much higher debt-to-equity ratio than its peers. This continues to be the case today. As of September 30, 2023, FirstEnergy had a net debt of $24.3360 billion compared to $10.945 billion of shareholders' equity. This gives the company a net debt-to-equity ratio of 2.22 today. That is an increase over the 2.17 ratio that the company had on June 30, 2023. This is concerning, as we want the company's debt to be going down, not up.

Here is how FirstEnergy's net debt-to-equity ratio compares to some of its peers:

| Company |

| Net Debt-to-Equity Ratio |

| FirstEnergy |

| 2.22 |

| Exelon Corporation ( EXC ) |

| 1.68 |

| Entergy Corporation ( ETR ) |

| 1.85 |

| DTE Energy ( DTE ) |

| 1.88 |

| Duke Energy ( DUK ) |

| 1.52 |

For most of the past decade, it was not really a big deal for a company to be heavily reliant on debt to finance its operations. This is because interest rates were incredibly low, which allowed companies to pay very minimal interest even if they had an enormous debt load. Things are very different today, as interest rates are currently at the highest levels that we have seen since 2001. This is causing interest expenses to rise for most companies. This is particularly noticeable across the utility sector, which I pointed out in a recent article . Thus far though, FirstEnergy has not really been impacted by this, as its interest expenses have been quite stable:

{kind=link}

We are starting to see interest expenses trending upwards though. It seems like the company's expenses will climb further as it is forced to start rolling over debt and financing its operations with higher interest-rate debt. After all, as I have pointed out in various previous articles, it seems highly unlikely that interest rates can fall meaningfully unless the Federal Reserve is willing to accept high inflation. The rising interest rates will serve as a headwind to the company's earnings.

Valuation

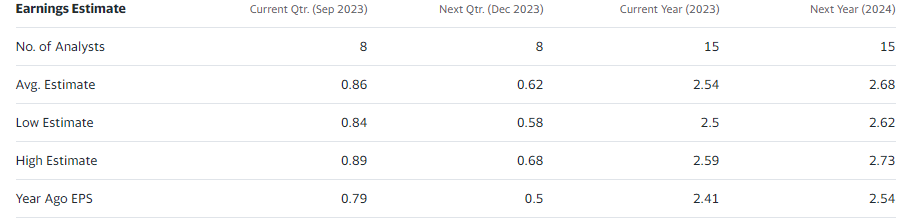

The analyst consensus right now is that FirstEnergy will grow its earnings per share by 5.51% next year:

{kind=link}

The five-year analyst consensus projections give the company a price-to-earnings growth ratio of 2.41 at the current stock price. Here is how that compares to the company's peers:

| Company |

| PEG Ratio |

| FirstEnergy |

| 2.41 |

| Exelon Corporation |

| 2.38 |

| Entergy Corporation |

| 1.60 |

| DTE Energy |

| 1.82 |

| Duke Energy |

| 2.48 |

(all figures from Yahoo! Finance)

As we can see, based on analyst consensus earnings growth, FirstEnergy is currently rather expensive when compared to its peers. This is the exact opposite of what we would normally expect to see. As I have pointed out in various previous articles, highly leveraged utilities such as this one tend to trade at a discount to their peers. This is due to the risks that accompany the company's high debt load.

The takeaway here appears to be that FirstEnergy's recent strength in the market may have caused its share price to appreciate too quickly and make the stock expensive relative to its peers. It may be a good idea to wait for the price to come down before buying into the company.

Conclusion

In conclusion, FirstEnergy's results continued to build on our basic thesis. The company exhibited the overall financial stability and generally slow growth that we have come to expect. The company does have the potential to deliver a respectable total return, however, as the 4.45% current dividend yield gives it a 10% to 12% total return if the company can manage to hit its earnings guidance going forward. As there are signs that the economy may soon enter into a recession, the stability that we see here is exactly the kind of thing that we should be able to appreciate.

For further details see:

FirstEnergy: Continuing To Deliver On The Thesis