UPWK - Fiverr International: Too Many Question Marks

2024-01-08 11:54:04 ET

Summary

- Fiverr is in a crucial crossroad, looking to re-accelerate its growth following a stagnant 2023 and a looming AI disruption.

- Fiverr's KPIs are the main propellers of its growth and they show signs of weakness, leading bears to believe Fiverr's glory days are behind it.

- Analysis of the sales and marketing expenses provides an alarming sign regarding its effectiveness. The new CMO has a lot of work to do.

- Management team claims that they haven't seen a negative impact from AI, but there are contrary indications that creativity-related gigs have been negatively affected.

- From a valuation perspective, the jury is still out on the stock, giving it industry's average multiples and waiting to see what happens next.

Fiverr International Ltd. ( FVRR ), the online marketplace for freelance services, has found itself under a lot of pressures in the last 24 months. The Software-as-a-Product company, who turned as one of Covid-19's biggest beneficiaries, is struggling to find new growth catalysts, with one technological development that seems to threaten it more than anything else - the AI revolution.

In this article we will delve into Fiverr's KPIs and try to learn from them what the future holds for Fiverr. We will also closely examine Fiverr's sales and marketing efforts in recent quarters and analyze how effective these efforts have been. And of course, we will explore whether the "AI threat" is valid or not, and stress Fiverr's valuation to get a better understanding whether the stock is "cheap", like some of the bulls may think. The answers, as you can guess, are more complicated than first thought.

But before we delve into these burning questions, let's provide a short summary of Fiverr's business model and a quick recap of its public life.

The Wild Ride of the Amazon of Freelancers

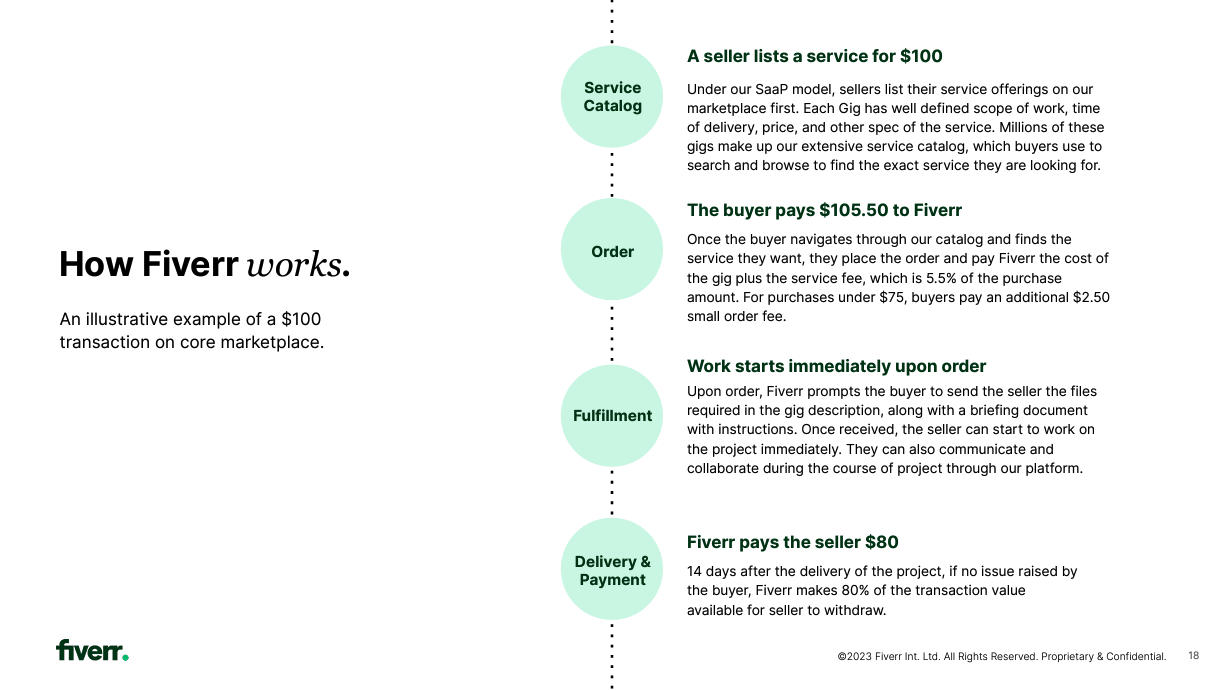

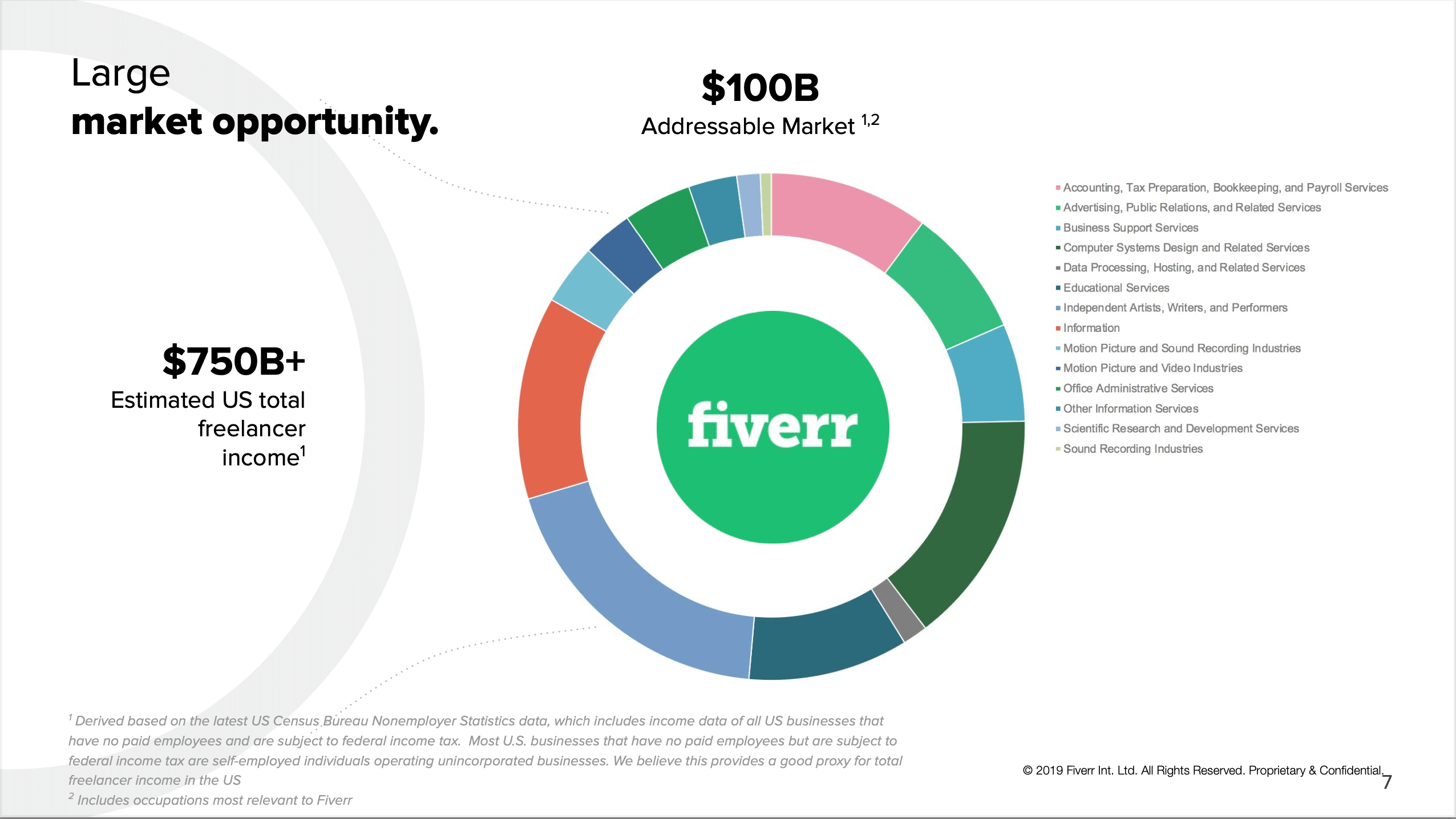

When Fiverr IPOed in 2019, it stated that it aims " to make working with freelancers as easy as buying something on Amazon ". The company is running a platform on which freelancers, known as "sellers", offer their services, or "gigs", to buyers. Such services vary from digital marketing, bookkeeping, content writing, graphic design, applications programming, translation and much more. Fiverr estimated that its total addressable market in the U.S. alone is over $100 billion per year, with the company only scratching the tip of the iceberg thus far, generating $353 million in revenues in the last 12 months.

Fiverr generates its revenues mainly through transaction-based fees. Both the buyers and the sellers (the freelancers) pay those fees, with the buyers paying a 5.5% service fee (with additional $2.50 for purchases under $75) and the sellers paying 20% fee upon successful completion of a gig. For example, a $100 gig will cost the buyer $105.5, with the seller netting only $80 ($100 x 80%). Fiverr will earn $25.5, which are 25.5% of the original gig cost.

{kind=link}

Source: Fiverr's Investor Presentation (November 2023)

Fiverr IPOed in June 2019 at $21.00 per share and at implied valuation of $800 million, yet soared 90% on its first day of trading and closed at $39.90 per share. The company didn't attract a lot of Wall Street's attention, and after two months the stock plunged back to its offering price. It was small-cap foreign company that nobody really cared about, with daily volumes sometimes below 70K shares. When I initiated my first position in this stock few months after the IPO, I remember finding it hard to buy the stock due to low liquidity and wide bid-ask spreads.

Then came Covid-19.

When the Covid outbreak started in early 2020, it triggered businesses, especially small and medium ones ("SMBs") to invest more into their online presence and individuals to spend more time online, what provided massive tailwinds for Fiverr's platform. Demand for freelancers' services on Fiverr surged, with categories related to e-commerce, content creation and digital marketing benefitting from the increasing demand. In March 2020, during the first innings of Covid and when Fiverr traded at ~$28.00, I called a bullish turn for Fiverr on my Seeking Alpha blog , stating the following:

With regards to the Coronavirus and the stay-at-home economy trend, I will not be surprised if this virus turns out as another catalyst for Fiverr, helping the company penetration across labor sectors that wouldn't reach for the freelancers market under normal circumstances.

Source: Seeking Alpha

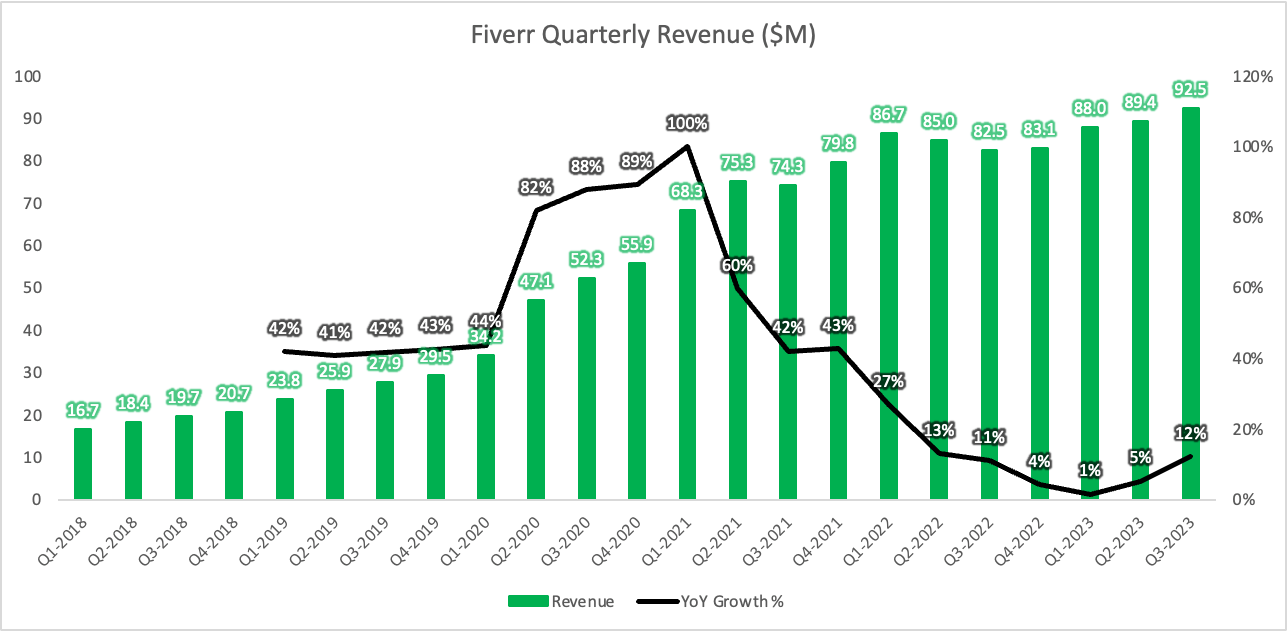

In the months that followed, the company fired on all cylinders, with quarterly revenue growing at a 80-100% rate , fueled by soaring number of Active Buyers, Spend Per Buyer and an increasing Take Rate, a result of a commission rate increase and new ancillary services such as Fiverr Learn (e-learning platform) and Fiverr Workspace (back-office tools). At its peak, on February 12th, 2021, Fiverr's stock price reached $323.10, implying a $11.65 billion valuation for a company that generated only $189.5 million in revenue in 2020 (i.e. TTM P/S multiple of 61.5x). Wall Street found its new darling.

However, Q2 of 2021 marked the beginning of an increase in vaccination rates around the world and the relaxation of Covid-related restrictions. People started to go out again, and got some off-screen time. Fiverr was immediately affected, with growth cooling to pre-Covid levels. But the big sucker punch came in 2022, when challenging macro economic environment , articulated in rising energy prices, inflation and rising interest rates, on top of Apple's ( AAPL ) change in private policy, led SMBs to cut heavily on spending, resulting in less demand for freelancers. Fiverr's revenue growth decreased to single digits by the end of 2022, and a $27.6 million intangible assets write-down in Q2-2022 led to the biggest quarterly loss in the company's public history. The "growth at all costs" slogan has been replaced with "focus on profitability", and the management team set an ambitious target of 25% adjusted EBITDA margin to prove Wall Street it has more than just growth.

{kind=link}

Source: Author's Process of Fiverr's Shareholders Letters

KPIs Will Make You, KPIs Will Break You

Many growth companies, and especially SaaS ones, use key performance indicators, known as "KPIs", to help their management teams and investors gauge their performance. In Fiverr's case, and because its business model is pretty straight forward, we can learn a lot from the related KPIs. Fiverr uses three key KPIs that basically builds up its top line.

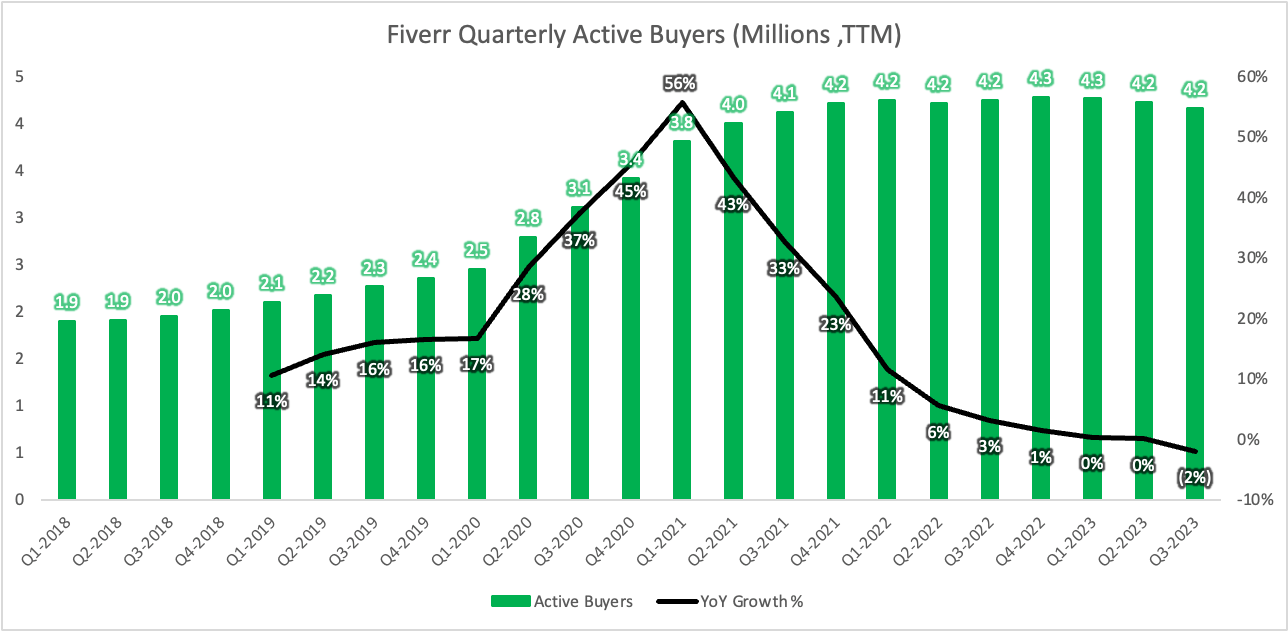

The first is the Active Buyers , which are defined as users who have ordered a work on the platform within the last 12-month period. As you can see in the graph below, Fiverr experienced a surging Active Buyers growth during the Covid period in 2020 and the beginning of 2021, reaching more than 4 million Active Buyers. Although that growth has slowed since then, and is basically stagnant these days, Fiverr can be encouraged by the fact that it didn't experience a massive churn, as one would have expected. In other words, Covid contributed to the significant growth of the Active Buyers base, but Fiverr managed to maintain that base and make it "sticky" to its platform. The 2% decline in Q3-2023 is a bit alarming, so it will be worth to closely monitor that KPI in future quarters.

{kind=link}

Source: Author's Process of Fiverr's Shareholders Letters

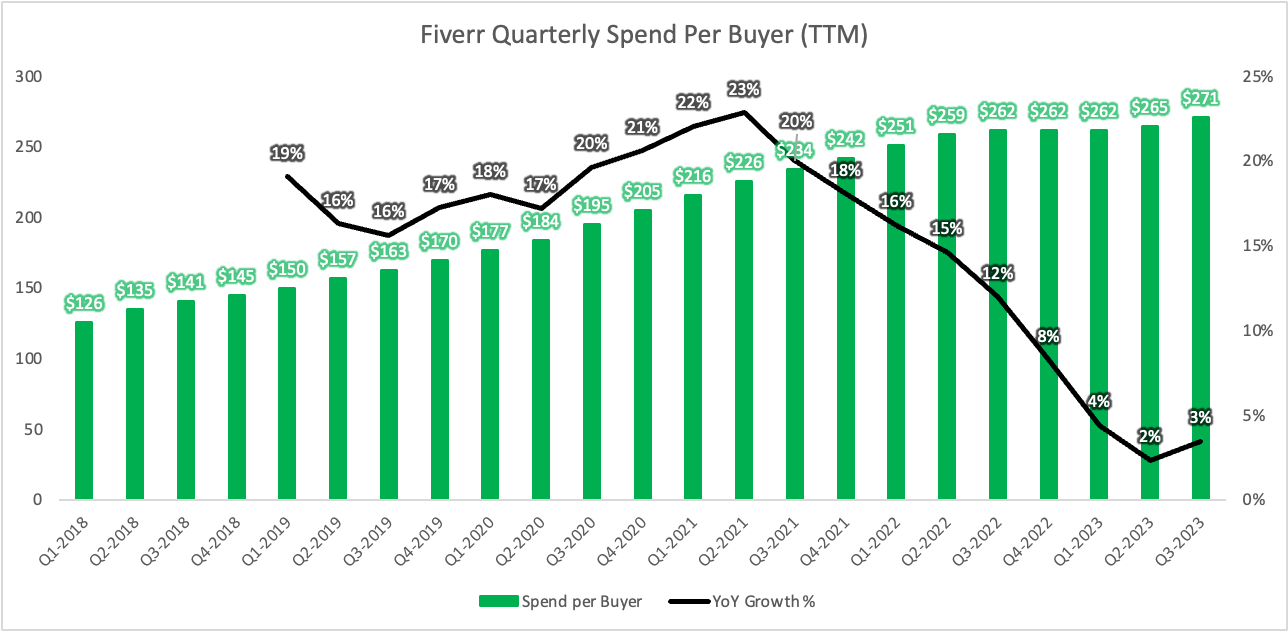

The second KPI is called Spend Per Buyer (or "SPB"), and is calculated by dividing Fiverr’s Gross Merchandise Value (the total value of transactions processed through Fiverr's platform) within the last 12-month period by the number of Active Buyers as of such date. This KPI also experienced an impressive growth during Covid which has been followed by a lower single-digit growth in recent quarters, now stagnating around ~$270. As it's becoming harder to make buyer spend more on their gigs, Fiverr must innovate, and in the summer of 2023 it announced a new product called "Fiverr Certified" , as part of its "Fiverr Business Solution" package. "Fiverr Certified" connects between SMBs and special freelancers that have been certified by SaaS vendors such as ClickUp, Monday.Com or Stripe, to help the SMBs integrate the products of those SaaS companies into their businesses. The interesting upside with "Fiverr Certified", according to Fiverr and although it's too early to fully assess its contribution, is that the a verage project size ranges between $700 to $800, significantly higher than the marketplace average.

{kind=link}

Source: Author's Process of Fiverr's Shareholders Letters

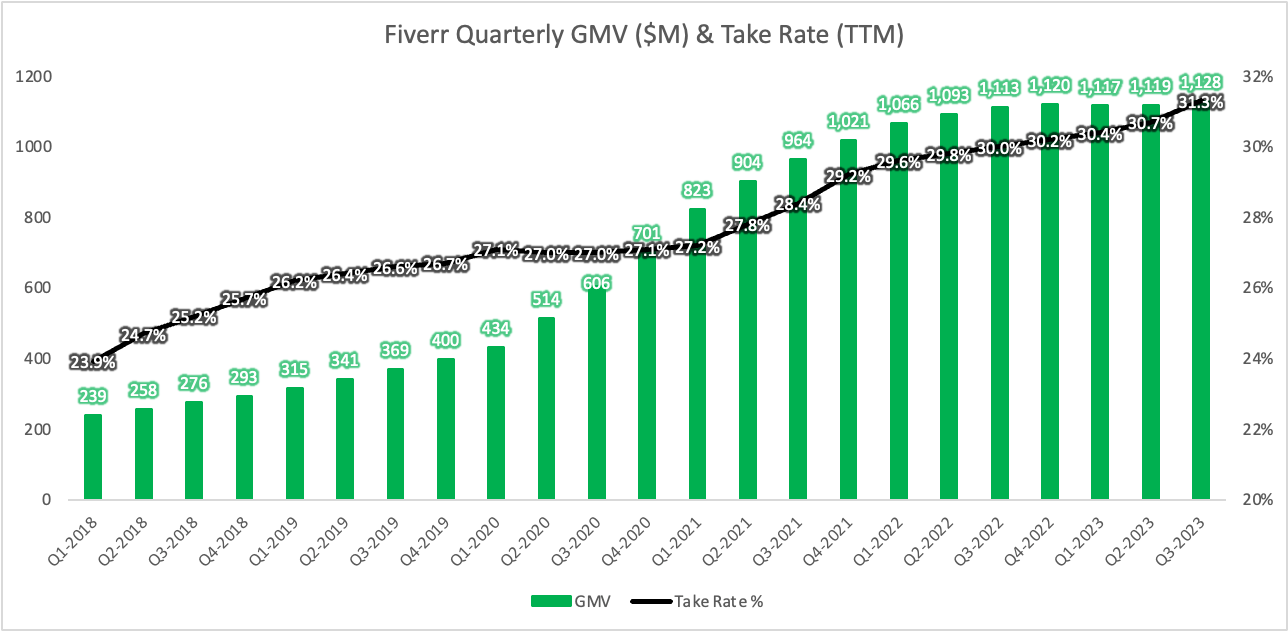

The third and final KPI is the Take Rate, which is essentially how much Fiverr charges on average from each transaction on its platform. If you remember the example I gave at the beginning of the article, Fiverr basically charges an "organic" 25.5% from each transaction. However, Fiverr launched in recent years many ancillary services, such as back-office software subscriptions, e-learning courses and promoted advertising solutions. Fiverr doesn't disclose the proportions of these ancillary services from its top line, yet we can assume with very high probability, based on Fiverr's total Take Rate of ~30%, that they comprise only a small fraction of it.

The key take here is that Fiverr manages to charge in total more than 30% from each transaction value. This figure is sometimes more than double than what competitors such as Upwork ( UPWK ) or Freelancer ( FLNCF ) charge, which is approximately 15-20%. A key argument of Fiverr's bears is that Fiverr’s Take Rate is not sustainable, and freelancers will eventually push back, increasing the risk of moving to other freelancer platforms or just completely “off-shoring” transactions (connecting directly with the buyer).

{kind=link}

Source: Author's Process of Fiverr's Shareholders Letters

If I had to pick the most important KPI, I would go with the Active Buyers one. The buyers on Fiverr's platform are what eventually drives its growth and basically create the desired marketplace. Freelancers will come and go, some are probably offering their shops on other freelance platforms, but what will differentiate Fiverr is the value proposition it gives to its buyers versus those of other platforms such as Upwork, Freelancer or Toptal. In order to underpin this value proposition and attract new buyers, Fiverr has to spend on marketing. And when I say "to spend", I mean a lot! This leads me to the next part of this article, in which we will discuss the main expenses on Fiverr's P&L - sales and marketing.

Marketing Efforts Are Not Working

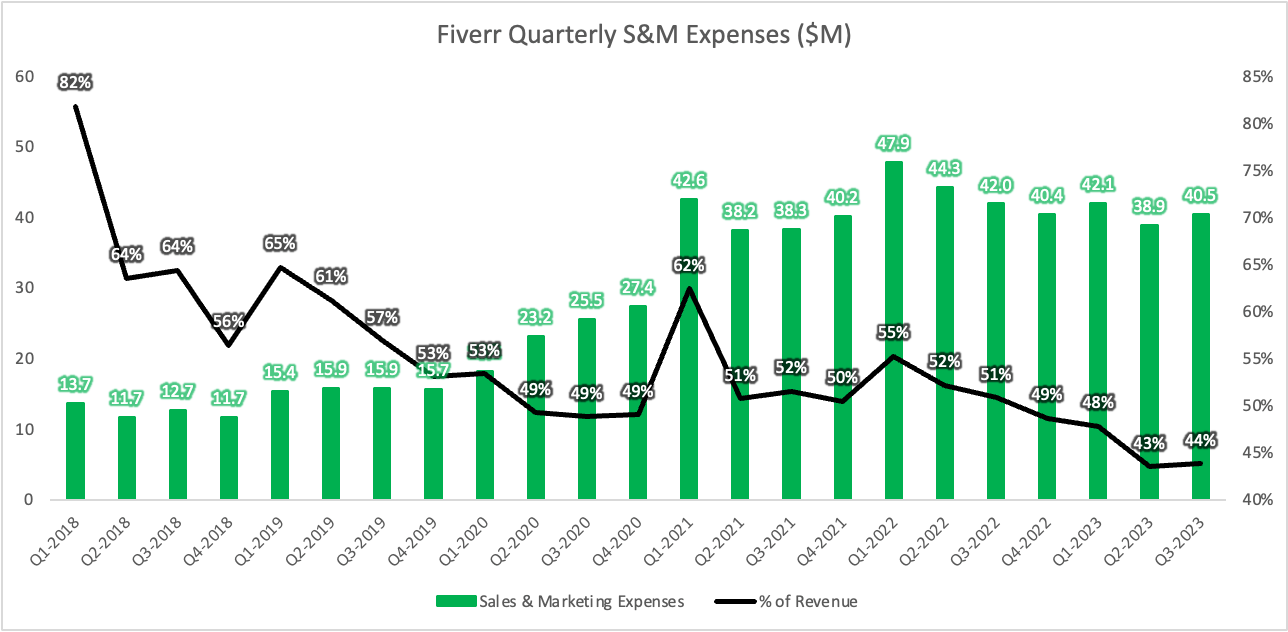

Since Q1-2018, the sales and marketing (S&M) expenses of Fiverr accounted for the lion’s share of the P&L expenses , with an average of 55%. Following the uptick in S&M expenses during Covid (well-articulated through the $8 million, 30-seconds Super Bowl commercial in February 2021), Fiverr tried to be much more cost-disciplined in recent quarters , and S&M expenses have been pretty much stagnant around $40 million a quarter, accounting for ~ 45% out of total revenues. However, Fiverr still spent approximately $161.9 million in S&M in the last 12 months, yet Active Buyers growth rates have been on a secular decline (stuck at ~4.2 million), so has been the Spend Per Buyer growth rates (stagnant at ~$270) and inevitably Fiverr's revenues. All that leads to the burning question - are Fiverr's S&M expenses justify themselves? Did the $161.9 million in S&M that Fiverr spent in the last 12 months were deemed accretive or not?

{kind=link}

Source: Author's Process of Fiverr's Shareholders Letters

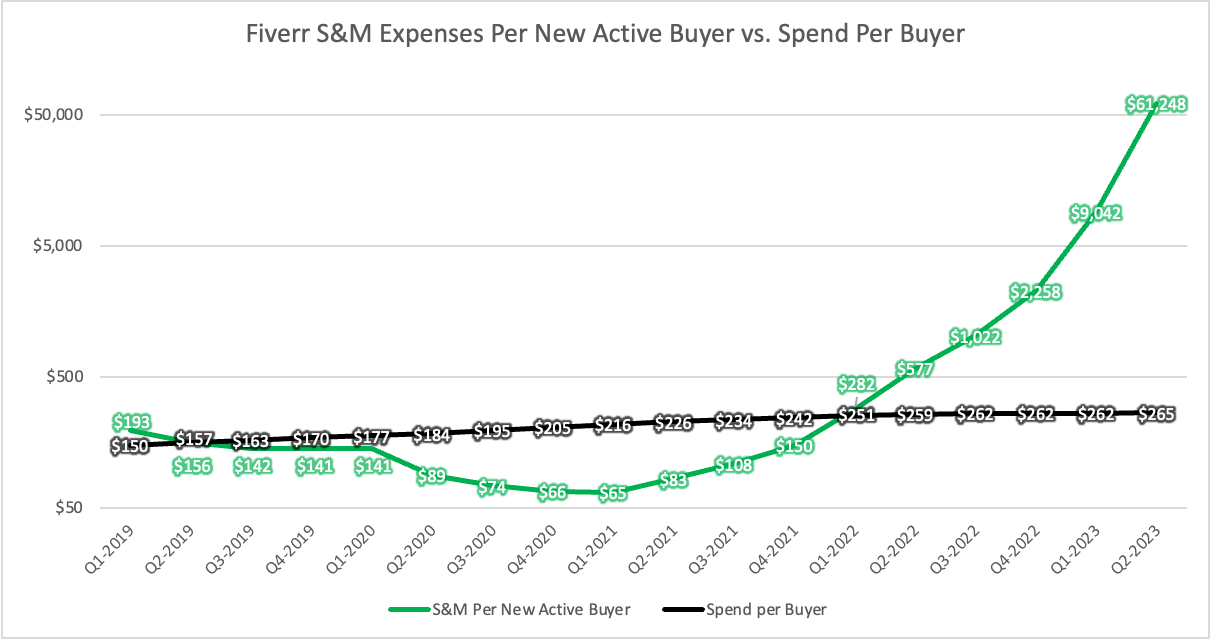

To answer that question, I will try to figure out how much Fiverr spends to acquire a new buyer on its platform. Because the Active Buyers figure is on a TTM basis, I will use only TTM numbers. For example, in Q1-2019 Fiverr had 2.1 million Active Buyers versus only 1.9 million in Q1-2018, i.e. a net increase of 200 thousand new buyers. During that period, Fiverr spent $51.4 million on sales and marketing. Now let's assume that 75% of those S&M expenses were attributed to acquiring new buyers, while the other 25% were attributed to maintaining existing ones. Based on that assumption, Fiverr spent $38.5 million on acquiring new buyers, i.e. $193 per new buyer. On the other hand, during that period the Spend Per Buyer was only $150, hence the "marginal contribution per new buyer" (S&M expenses per new buyer minus the Spend Per Buyer) was negative $43. We can continue this exercise until Q2-2023 and compare the results to the respective Spend Per Buyer:

{kind=link}

Source: Author's Process of Fiverr's Shareholders Letters

** In Q3-2023 there was the first-ever decline in Active Buyers on a TTM basis, hence the S&M expenses per new active buyer are negative

As can be seen, the " marginal contribution per new buyer" was positive in 2019 and got even better during Covid (the "belly" in 2020-2021). However, s ince Q1-2022 Fiverr's sales and marketing expenses don't yield the desired outcomes, with a "record" set in Q2-2023, when the $163.3 million in S&M expenses (on a TTM basis) added only 2,000 net new buyers. Assuming the 75% distribution I'm using, that is $122.5 million in S&M expenses for acquiring those 2,000 net new buyers, or $61K per each one, and all that versus only $265 in Spend Per Buyer. Even if we assume a different distribution, say 50-50% between new buyers and existing ones, Fiverr's marketing is still performing really bad since early 2022. Things got even worse in Q3-2023, when Fiverr reported its first ever Active Buyers decline of 2% (on a TTM basis), versus S&M expenses of $161.9 million during that period. In other words, Fiverr spends ton of money on sales and marketing, but buyers just don't come as they did few years back.

In early November 2023, Fiverr announced the appointment of a new Chief Marketing Officer. One would assume that this is correlated to the marketing difficulties we have just mentioned. There is no doubt that Fiverr will need to recalibrate its sales and marketing approach in order to re-accelerate its growth again. The hyperbolic surge in S&M spending per new buyer is very alarming and something that Fiverr must address immediately. We should closely monitor that trend in future quarters.

The AI Revolution – Friend or Foe?

One of the strongest bearish thesis on Wall Street regarding Fiverr is that artificial intelligence, or "AI", is going to disrupt its business model in a very negative way. Why? Well, Fiverr is known as the go-to place for those searching for talent from creativity-related industries, such as content writing, video-editing, advertising, digital marketing etc. The problem with these types of services, or "gigs", according to the bears, is that AI applications such as ChatGPT, Dall-E, Stable Diffusion, Midjourney and others are going to replace the need for freelancers doing these gigs. Why, for example, would someone hire a freelancer on Fiverr to write him a resume when ChatGPT can do that for free and in five seconds?

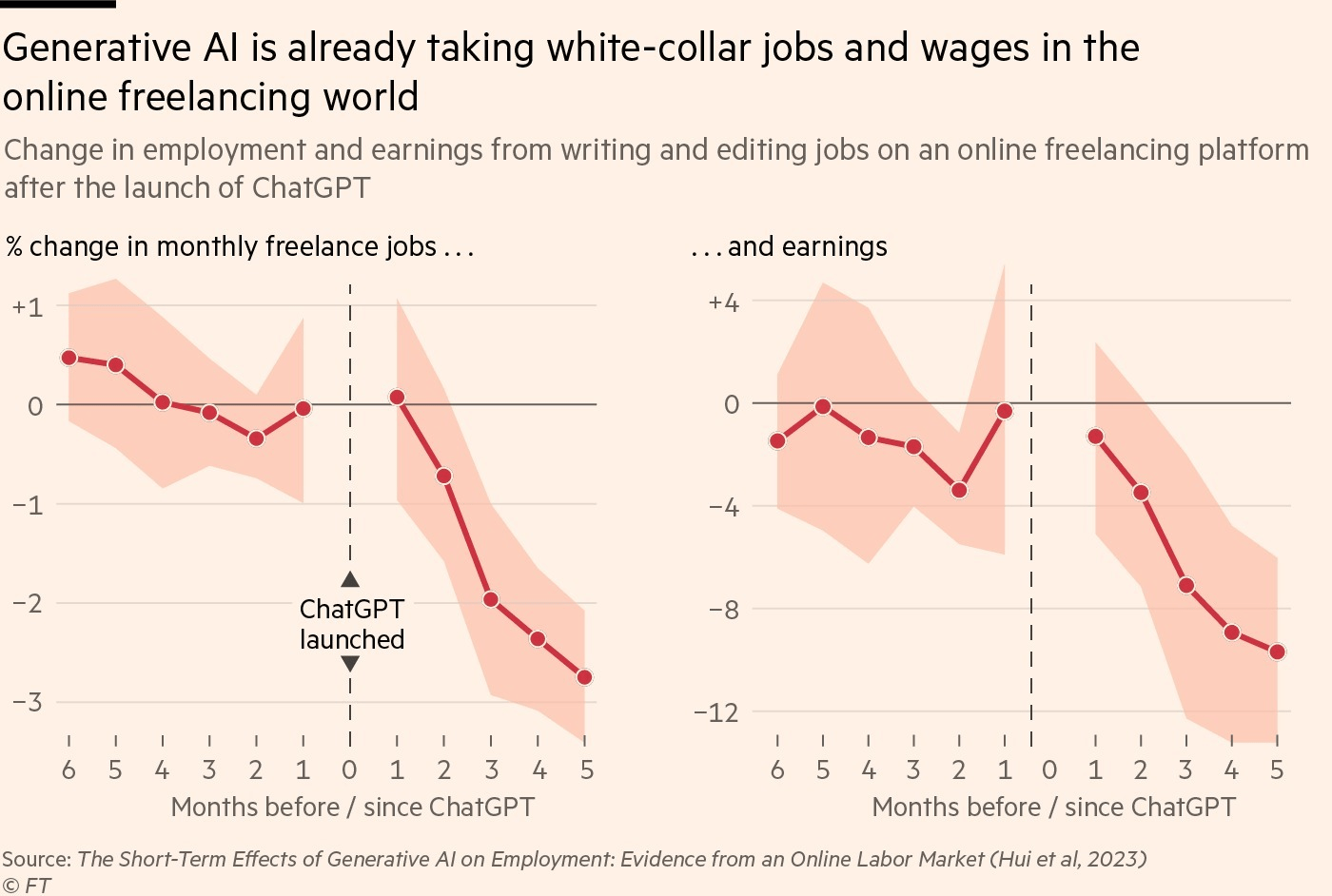

Although Fiverr did add new AI categories to its marketplace and said that it experienced a strong demand for such services, the bears would argue that it will not be enough to offset the cannibalization of the creativity-related gigs. A paper published in August 2023 by researchers from Washington University and New York University (later quoted by the Financial Times) examined how the November 2022 rollout ChatGPT impacted the earnings of Upwork's freelancers. The findings were quite disturbing: freelancers that specialized in "writing and editing" jobs earned ~8% less in April 2023 than they did before ChatGPT's release, and the demand for such works decrease by close to 3%.

{kind=link}

Source: Financial Times

Recently I came across an interesting interview with an Australia-based freelancer who offers writing services on Fiverr , which provided another evidence on the phenomena. The freelancer said that ChatGPT have led to less demand for his work, adding that he's seen some freelancers' earnings fall from $2,500-$3,000 per month to approximately $1,000 today. The idea that ChatGPT, for example, can actually be the freelancer itself, may put many human freelancers jobs at risk, according to the bears.

But if we really want to assess the risk for Fiverr, we need to understand how many gigs on its platform are exposed to AI disruptions, if any. Fiverr doesn’t provide any breakdown of its categories contribution to its revenue line, but did state in its Q3-2023 letter to shareholders that no single category accounted for more than 10% of total revenue on the core marketplace. However, Fiverr did provide on its investors' presentation from July 2019 the company's addressable market with breakdown to categories (see the pie chart below). Although that breakdown may have changed since then, it immediately stands out how many categories are likely be disrupted by AI technology:

{kind=link}

Source: Fiverr's Investor Presentation (July 2019)

Among the categories stands out the “Independent Artists, Writers and Performers” which represents the single biggest category that may also be highly susceptible to AI disruption. Other "highly-exposed" categories are "Advertising, Public Relations and Related Services" and "Motion Picture and Sound Recording Industries".

Fiverr's management team understands the threat, and was quite quick to respond, whether through the “Power of Humanity” campaign in September 2023 or in an open letter in The New York Times penned by CEO Micha Kaufman under the title "An Open Letter to AI".

Source: Digital Synopsis

Kaufman and his team insisted in recent earning calls that they have not seen AI negatively impact their business and that they are seeing AI more as a friend than a foe . On top of that, they added that they don't anticipate AI development to displace the need for human talent, and that AI won't replace the freelancers, but that freelancers using AI will eventually outcompete those who don’t. Kaufman said that interest and demand for the new AI categories on Fiverr's platform are "booming", the result of an " increasing need for human skills to deploy and implement AI technologies ". Bulls will embrace those comments from Fiverr and argue that AI technology will disrupt lower-skilled freelancers, while the skilled ones, if correctly use the technology, will be able to capitalize on it and improve their offerings on Fiverr.

My take here is that we are actually in the midst of an ongoing shift in the freelancers landscape, and perhaps in the entire labor market. Therefore, it may be just too soon to fully determine what AI will do to Fiverr's platform. I do believe that freelancers in the creative industry will have to acquire AI skills in order to stay relevant, but also that new AI-related categories will emerge on Fiverr's platform and add completely new offerings.

SMBs Sentiment is Still Very Low

An important element investors of Fiverr should also monitor is the small and medium businesses (SMBs) sentiment, due to the fact that Fiverr’s buyers' community is comprised mainly from SMBs. The stay-at-home economy during the Covid “heydays” have forced small and medium businesses to build and expand their online presence , investing in digital services and particularly in website development, SEO/SEM, content marketing, social media marketing, creative and design services. This trend was the main tailwind for Fiverr in 2020 and 2021, leading to surging demand for freelancers services. However, following the challenging macro economic conditions starting in 2022 , SMBs reduced spending , leading to less demand for freelancers services.

Another event, maybe less intuitive by its linkage, occurred in 2021 when Apple changed its privacy policy. The change aimed to prevent advertisers from tracking iPhone and iPad users without their consent, what made it harder to target new customers online. It was a curveball for SMBs , who relies heavily on online ads to attract new customers. The full impact was felt in 2022, when inflation joined the fray, leading SMBs to cut back on marketing spending and investments, which hurt demand for freelancers doing those marketing works.

An interesting survey, that Fiverr itself referred to, is The National Federation of Independent Business (“NFIB”) SMB sentiment. That sentiment hit a 10-year low in April 2023 (89.0) as businesses were bracing for a looming recession . Although SMBs sentiment has improved a little since then, it is far even from Covid and pre-Covid levels. The conclusion is that any future recovery in Fiverr's business will probably have to follow an improving SMBs sentiment.

Source: The National Federation of Independent Business

Valuation and Short Interest

Bulls would argue that Fiverr stock has bottomed, or close to bottom, with growth stagnation fully baked into the stock price, which can be reflected in the stock's 2023 performance (down 5% on an annual basis). To stress this assumption, let's look at Fiverr's sales multiples, which are generally used for growth SaaS companies, since those companies are usually not profitable and invest a lot in their growth. We will also look at the price-to-cash flow multiple (P/CF), to stress the possibility that Fiverr is somehow a value play rather than a growth one.

The first peer group we will use is the Staffing & Employment Services industry (excluding companies with market cap of less than $100 million):

| Staffing & Employment Services |

| P/S |

| EV/S |

| P/CF |

| RevGrowth (*) |

| Industry Median |

| 1.0x |

| 1.0x |

| 12.0x |

| 7.6% |

| Fiverr |

| 2.8x |

| 2.1x |

| 15.3x |

| 29.3% |

| Upwork |

| 2.8x |

| 2.6x |

| 46.6x |

| 24.2% |

(*) Defined as the 3-year revenue CAGR

Fiverr trades at significant premium to the industry's multiples, which can be attributed to Fiverr's superior growth. Moreover, when comparing Fiverr with its biggest competitor Upwork, both trade at similar sales multiples, yet Fiverr trades at major discount when looking at the P/CF multiple (15.3x versus Upwork's 46.6x).

However, the Staffing & Employment Services industry is comprised from many "old-school", slow to moderate-growth players such as Automatic Data Processing ( ADP ), Manpower ( MAN ) and Paychex ( PAYX ), while Fiverr's business model of online services marketplace has similarities to the Internet Content & Information industry. Therefore we should also take a look at this industry (again excluding companies with market cap of less than $100 million):

| Internet Content & Information |

| P/S |

| EV/S |

| P/CF |

| RevGrowth (*) |

| Industry Median |

| 2.8x |

| 2.2x |

| 18.1x |

| 17.1x |

| Fiverr |

| 2.8x |

| 2.1x |

| 15.3x |

| 29.3% |

(*) Defined as the 3-year revenue CAGR

Here we can see that Fiverr trades at similar revenue multiples to those of the industry, with a slight discount of the cash flow multiple.

The Internet Content & Information peer group, which I find more relevant in terms of the technology tilt and the growth profile, implies that there are no major pricing anomalies with Fiverr, reflecting a neutral stance of investors.

On the other hand, bears would argue that the elevated short interest (~10.7%) versus both industries indicates that many investors still see a potential downside risk for the stock, although a potential for a massive short squeeze seems modest as the Days to Cover Ratio is less than 5 days.

| Industry |

| Median Short Interest |

| Staffing & Employment Services |

| 3.2% |

| Internet Content & Information |

| 4.1% |

The Verdict

Fiverr has been through one hell of a ride since its IPO in 2019. The company, which experienced high growth rates that only skyrocketed during Covid, is now finding it hard to maintain past growth rates. Bears would argue that Fiverr's glory days are behind it, that the stock peaked in 2021 and will never reach those highs again. The weakening KPIs, the disturbing economics of the marketing efforts and the AI threat that may change the entire freelance economy support the bears' thesis.

However, There is a possibility that we will see KPIs re-accelerating again, the result of new innovations from Fiverr such as the "Fiverr Certified" (certified freelancers offering tech vendors services), "Fiverr Neo" (AI-based matching tool), "Fiverr Pro" (premium marketplace offering) and other ancillary services. Moreover, the new CMO may be able to turn the "marketing ship" and improve the efficiency of the marketing campaigns, and the AI revolution may turn as an AI resolution , with new AI-related categories taking the places or complementing "old" ones, leading to a "soft AI landing" for Fiverr's platform.

From valuation perspective, it seems like the jury is still out on the stock, giving it industry's average multiples following a stagnant 2023 stock performance.

The bottom line is that Fiverr is in a crucial crossroad, maybe the most significant one in its life as a public company. Fiverr may be able to reinvent itself, re-accelerate its business and start growing again like it did before Covid (because Covid's growth rates will probably not happen again). The other option is that Fiverr will gradually fade, with its stock continuing to move sideways before ultimately decline below the IPO offering price.

I would closely monitor Fiverr and look for the following signs to turn bullish on the stock and rate it as a "Buy" in the future:

- Active Buyers base stops declining, and starts to grow at low-teens rate.

- Spend Per Buyer starts to grow at low-teens rate.

- Take Rate doesn't fall below 30%.

- "S&M expenses per new Active Buyer" decline dramatically so the " marginal contribution per new buyer" turns positive again.

- SMBs sentiment shows signs of continuing improvement.

On the other hand, I would turn bearish on the stock and rate it as a "Sell" if the followings happen:

- Active Buyers base continues to decline in Q4-2023 and Q1-2024

- Spend Per Buyer stays stagnant or declines (which is something that never happened thus far)

- Take Rate falls below 28%.

- "S&M expenses per new Active Buyer" stay the same or slightly decline so the " marginal contribution per new buyer" stays negative.

- SMBs sentiment significantly deteriorates.

There is no doubt that the next few quarters will be super interesting for Fiverr's followers. The scenarios I laid out will take few quarters to fully unfold to either direction, hence investors wishing to take position in this stock should probably be patient. For now, Fiverr is in a "Show Me" mode. Therefore, I currently rate it with a "Hold" . Even if the company successfully re-accelerates and the stock shoots up, there will be plenty of time to jump on the bandwagon.

Fiverr's "Power of Humanity" Campaign

Thanks for reading!

If you liked this article and do not want to miss any of these in the future, please scroll up and click "Follow" next to my name.

For further details see:

Fiverr International: Too Many Question Marks