BSJT - Fixed Income Perspectives - Looking Ahead At Q1 2024: A Turning Point For Policy

2024-01-10 08:42:00 ET

Summary

- The downward inflation trend has bolstered market confidence that monetary policy is sufficiently restrictive as to achieve the FOMC’s longer-run goals. Further, policymakers’ rhetoric has turned more dovish, suggesting that a critical inflection point has been reached in fixed-income markets.

- Historically, the final rate increase of a hiking cycle has been a reliable guidepost for interest rates in which duration transitions cyclically from being a headwind to a tailwind for bonds. Early indications suggest that this time will be no different.

- Risk assets should also benefit from the conclusion of the hiking cycle. Combined with greater clarity on monetary policy, 2024 is starting off in a Goldilocks period (where economic data is not too hot or too cold), fostering demand for duration as well as credit.

As central banks reach a fulcrum point in monetary policy, we see recessionary pressures mounting over the first quarter of 2024:

1. After steadily declining in 2023, inflation is likely to continue cooling over the first quarter of 2024.

2. Although the labor market is showing signs of achieving a better balance, any sustained increase in unemployment claims would likely signal a recession.

3. The consumer - resilient over 2023 - will need to continue to contend with stubbornly high (albeit moderating) inflation, higher borrowing rates and tighter lending standards.

Macro outlook

U.S.

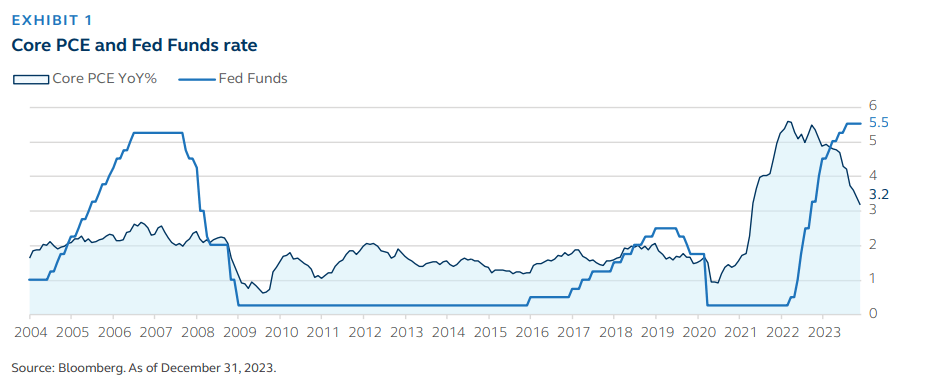

Between November 2021 and November 2022, core PCE (the Federal Open Market Committee’s ((FOMC)) preferred measure of inflation) remained within an uncomfortably elevated range of 5.0-5.5%. Over the course of 2023, however, we’ve witnessed a steady decline in core PCE, with the latest reading (3.2% as of 11/30/2023) matching the Fed’s year-end guidance provided in their December Summary Economic Projections (3.2%). The downward trend in core PCE is likely to persist in 2024 as the U.S. economy slows and shelter inflation (which tends to lag changes in the Fed policy rate by 18 to 24 months) continues to cool.

{kind=link}

The downward trend in inflation has bolstered market confidence that monetary policy is now sufficiently restrictive as to achieve the FOMC’s longer-run goals. One indicator of this was the October CPI print, which marked the first time this cycle that market pricing discounted no additional rate hikes. Further, policymakers’ rhetoric has turned more dovish to close 2023, suggesting that a critical inflection point has been reached in fixed income markets.

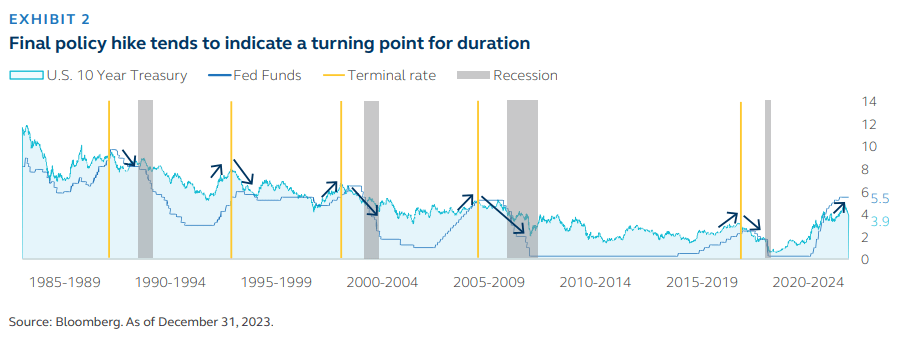

Historically, the final rate increase of a hiking cycle has been a reliable guidepost for interest rates in which duration transitions cyclically from being a headwind to a tailwind for bonds. Early indications suggest that this time will be no different, as an appetite for duration has seemingly returned and investors that had been awaiting further clarity on the path of Fed policy are now returning to the market, leading to a pronounced rally in interest rates to end the year.

{kind=link}

Risk assets should also benefit from the conclusion of the hiking cycle. Spreads in most sectors have compressed and levels now appear consistent with a soft-landing scenario. Combined with greater clarity on monetary policy, 2024 is starting off in a Goldilocks period (where economic data is not too hot or too cold), fostering demand for duration as well as credit. If soft landing expectations are challenged by a weakening economy in the months ahead, rates will further benefit, while credit spreads may decouple and widen as is typically the case when recession fears escalate.

Going into the new year, unemployment claims will be a key metric to follow in the U.S. Hiring has slowed steadily since the Fed began its hiking campaign, and the labor market is showing many signs of achieving better balance after a period of extreme tightness post-pandemic. Aggregate weekly hours, overtime hours, and temporary hiring have all declined significantly, but layoffs and unemployment claims have remained stubbornly low. This environment indicates that companies that once faced challenges attracting employees are now reluctant to reduce headcount, especially as the consumer has remained resilient. At this stage, companies have cut work but not workers. Any sustained increase in unemployment claims would signal an escalating slowdown and an imminent recession.

Global

While peak policy rates appear to be behind us, economic tightening is far from over. At the end of the year, we witnessed the market rapidly pricing and unwinding higher-for-longer rates, aided by policymakers shifting their emphasis away from hiking rates toward pausing and assessing incoming data. Concurrently, global economic data continued to soften and inflation data improved, helping to affirm the dovish policy turn. Remarkably, this was all achieved without increasing recession expectations and many investors now believe a soft landing may be within reach.

That said, we caution that the tightening we have experienced so far is just the beginning of what will continue far beyond a Fed policy shift. Using mortgage rates to proxy consumer borrowing costs and corporate bond yields to proxy business borrowing costs, the gap between the existing cost of funding and the current cost of funding is around 200 basis points (bps) across the U.S., U.K., and EU, a level unseen since the 1980s. Due to the extraordinarily low interest rates post-Global Financial Crisis, most of the U.S. economy is still being funded by very low rates. A higher cost of funding only kicks in upon refinancing, bringing about additional tightening even as policymakers remain on hold. This is likely to continue cooling economic activity and bring about higher default rates for businesses and households in the years to come.

Europe provides a clear prologue. Due to the short-reset nature of European mortgages, outstanding mortgage rates have already risen around 250 bps, despite the European Central Bank’s delayed rate lift-off relative to the Fed’s. As a result, consumer spending in Europe failed to support the economy in 2023 despite similarly tight labor markets with a low unemployment rate, and the eurozone economy contracted in Q3 2023. In the U.S., outstanding mortgage rates have only risen 100 bps, still 400 bps below current mortgage rates. The impact of the bulk of the Fed’s interest rate hikes has yet to reach most U.S. households and businesses.

Meanwhile, Japan looks set to finally exit its negative interest rate policy that has been in place since 2016. This follows the effective exit of yield curve control policy this year that will be fully implemented by next year. As the Bank of Japan gathers conviction of sustainable inflation to exit its negative interest rate policy, further rate hikes cannot be ruled out. The impact of tightening would come at a politically sensitive time, as 2024 is a major election year for G4 with the U.S. presidential election in November, the EU parliament election in June, the U.K. general election by January 2025, and the Japan general election by October 2025. This will ensure the bread-and-butter issues of the electorate stay at the forefront of policymakers’ minds. If the shift in the trajectory of growth and jobs occurs concurrently with lagged tightening impact, watch for sharper turns from central banks than current guidance.

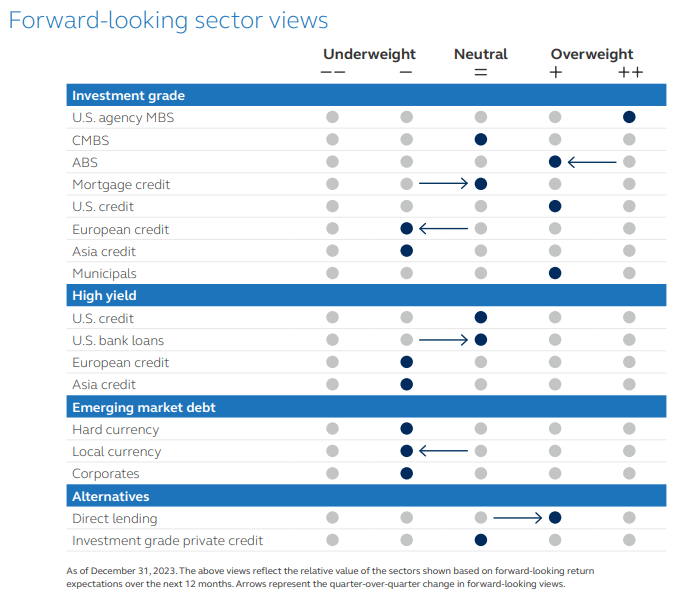

Summary of investment implications

Investment Grade Credit

With the journey to higher rates now in the rear-view mirror, investment grade ((IG)) credit offers compelling yield on an absolute and risk-adjusted basis, as the technical underpinnings of the market remain strong. We now see a favorable entry point for IG credit investors.

High Yield Credit

Despite less-robust corporate earnings forecasted in 2024 and the prospect of a more challenging fundamental environment, the strength of balance sheets and above-average yields continue to make high yield look compelling.

Securitized Debt

Shaped by competing technical and fundamental factors, asset-backed securities are likely to face a dynamic landscape in the first quarter of 2024. There are select opportunities within commercial mortgage-backed securities, but strong credit work and selectivity remain critical. Mortgage spreads have been strongly correlated with interest rates, and the turn in the rate cycle is an important inflection point for the sector.

Municipals

Though credit spreads are not as wide as a year ago, we still see a relative value opportunity in 2024 with spreads compressing further based on diversification benefits and demand for high-quality, long-duration assets. With new issue supply projections flat versus 2023 levels, the supply/demand dynamic is likely to be supportive of spreads.

Emerging Market Debt

Despite investor skepticism of the asset class given ongoing geopolitical tensions, a lack of recovery in China, and the renewed socialist momentum in Latin America, our base case into 2024 remains optimistic about the emerging market sector.

Private Credit

Although headwinds to the economy are expected, several supportive trends for middle market direct lending have an opportunity to enhance risk-adjusted returns relative to historical loan vintages. Based on early indications, U.S. private market issuance will start strong in 1Q relative to prior years.

Investment grade credit

As we look into 2024, IG credit has emerged as a sleep-easy-at-night asset class, offering solid return potential. With the journey to higher rates now in the rearview mirror, IG credit offers compelling yield on an absolute and risk-adjusted basis, as the technical underpinnings of the market remain strong. As rates begin to fall - and even as they oscillate - the commanding starting point for yields creates the perfect backdrop to drive high-single digit total returns for high-grade corporate bonds. As we enter the new year, we see a favorable entry point for IG credit.

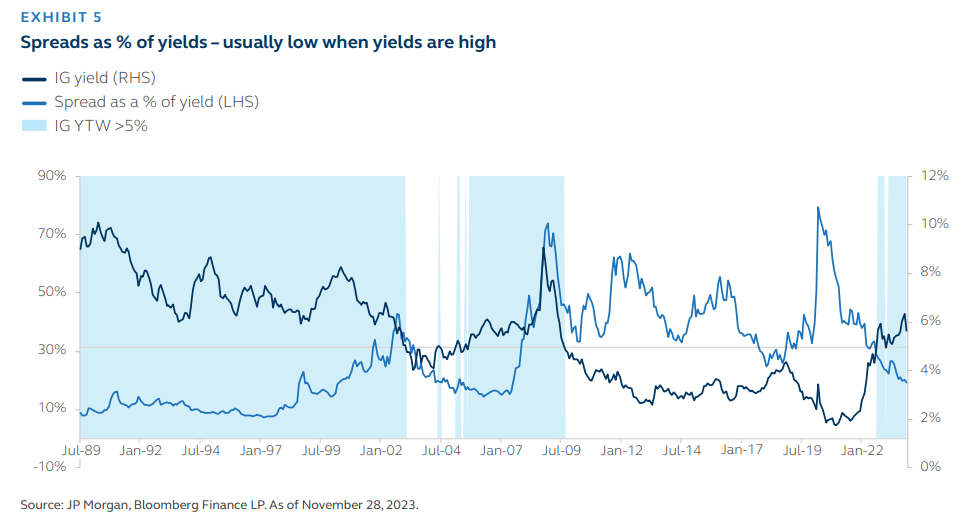

With corporate bond yields near 5.0%, duration acting as a tailwind, and rates at an elevated level (though likely to trend lower over 2024), the path to higher returns in high-grade bonds remains promising. As a bonus, higher all-in yields can cushion spread widening given their tighter relative starting point - a higher and more favorable breakeven factor. While some may claim IG spreads as a percent of yields near 20% are low, on a relative basis, this has remained the norm in past periods of high yields. With 60% of institutional IG credit buyers being yield-focused, the strong yield and total return argument remains well in place. Even with spreads at very tight levels, the institutional appetite for corporate bonds has not diminished. This technical support - along with a manageable supply outlook - paints a vibrant picture for IG credit.

{kind=link}

While a recession has eluded us to date, a confluence of headwinds could slow the spending frenzy, the main engine of economic growth. As such, we maintain a higher quality bias within investment grade credit as fundamentals have begun to turn. To that end, consumers face higher borrowing and energy costs, and companies have seen leverage and interest expense tick up. Although a buoyant consumer has so far pushed off a recession, the chance that lavish spending continues as excess savings run out remains to be seen. On top of that, banks have been tightening lending standards for over a year, as shown in the Fed’s Senior Loan Officer Survey. Moreover, any further dis-inversion of the yield curve will make investments farther out on the yield curve, such as corporate bonds, stand out on a risk-adjusted basis. Despite headwinds hovering on the horizon, IG credit fundamentals are starting from a strong base, and yields remain compelling.

High yield credit

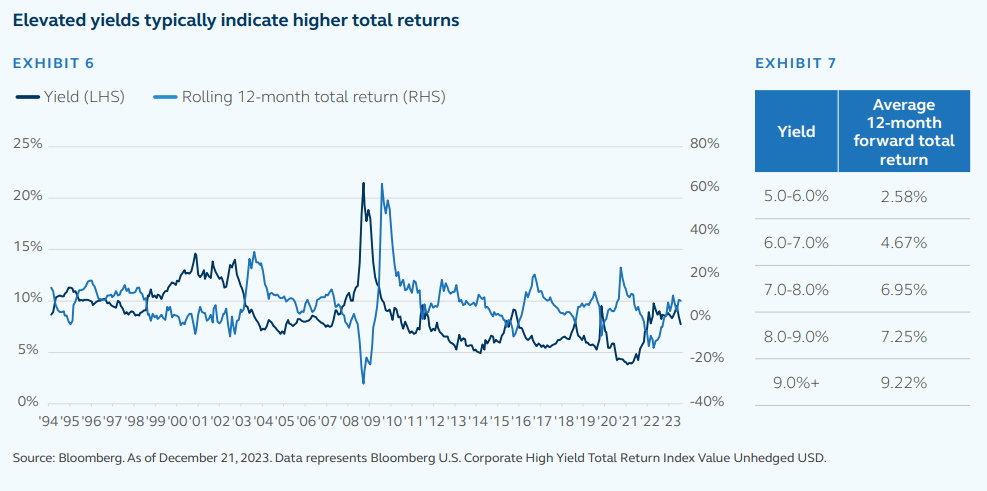

In navigating the current landscape, high-yield ((HY)) investors have much to consider, including the future direction of the economy, the trajectory of interest rates, and mounting geopolitical tensions. Against this backdrop and despite these risks, we continue to believe that the HY market is in a fundamentally attractive place. The quality of the market is at historically high levels, while issuer fundamentals - including leverage ratios and interest coverage - are at very strong points, and there are very few bonds maturing in 2024. Candidly, a little bit of the performance potential for 1Q 2024 has been offset by the strong performance of the asset class in late 2023. However, with starting yields in the 7.6% area, the asset class still provides a substantial income buffer that allows it to weather adverse economic or geopolitical events and has historically produced attractive returns at these rates (Exhibits 6, 7).

We understand we are in a higher interest rate regime, which will cause corporate earnings to not be as robust as previous years. Because of this, we believe spreads will widen slightly from current levels. However, a slowdown and expected spread widening should not scare investors away from high yield, as starting yields are still well above the 10-year average. Yes, spreads are below average but yields are not. At the same time, the FOMC has indicated that they’ve reached their peak federal funds rate for this hiking cycle. Historical data suggests that following a peak in the fed funds rate, the HY market realizes a 12.3% average return over the following 12-month period. This historical perspective fuels further optimism about the HY market’s performance post-interest rate hikes.

Despite less-robust corporate earnings forecasted in 2024 and the prospect of a more challenging fundamental environment, the strength of balance sheets and above-average yields continue to make HY compelling. We believe defaults are unlikely to increase dramatically, instead we believe they’ll remain closer to the historical average level of 4%. The asset class should be positioned to potentially provide equity-like returns with bond-like volatility over the next year. This unique combination of characteristics makes the HY market an attractive proposition for investors.

{kind=link}

Securitized debt

Mortgage-backed securities (MBS) Fundamentals remain constructive, as cash flows are stable with minimal refinancing risk even if rates rally further in the first quarter. Implied interest rate volatility is elevated when compared to historical averages, potentially benefiting investors if volatility normalizes. Valuations have also been attractive, as mortgages are trading with spreads well above historical averages, more in line with prior periods of severe stress. Mortgages appear cheap relative to Treasurys and IG credit. However, technicals were a challenge in 2023, as banks reduced exposure to MBS due to balance sheet pressure and lackluster deposit growth. It appears that many investors have been on the sidelines awaiting greater clarity on the Fed hiking cycle. As inflation continues to improve, Fed officials are not only signaling the end of the hiking cycle but beginning to talk openly about the prospects for rate cuts in 2024. Market pricing reflects this pivot. Mortgage spreads have been strongly correlated with interest rates, and the turn in the rate cycle is an important inflection point for the sector.

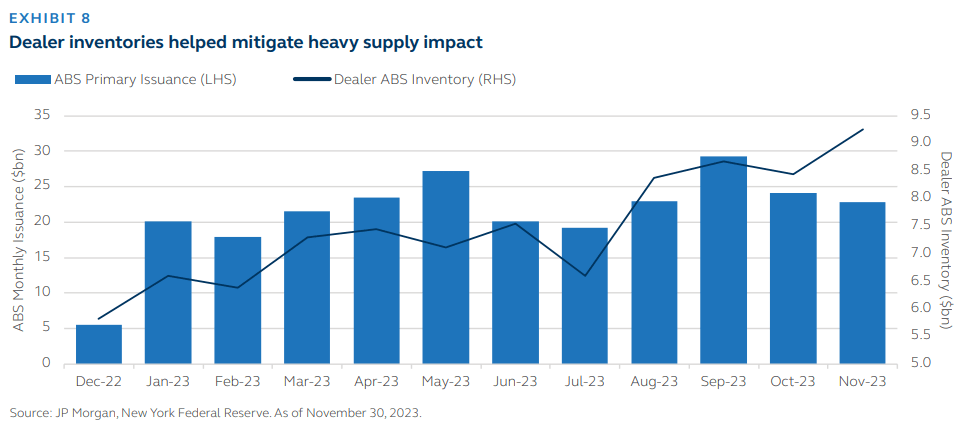

Asset-backed securities ((ABS)) Shaped by competing technical and fundamental factors, ABS is likely to face a dynamic landscape in the first quarter of 2024. A surge in auto-related ABS issuance during the second half of 2023 led to underperformance versus other spread products. Deals were well-received by investors, with most transactions seeing healthy subscription levels at issuance, and dealers have added inventory. However, the sheer volume of new issue supply ultimately weighed on relative performance, a trend that should continue into 2024 as banks and credit unions remain active issuers.

{kind=link}

Short-duration ABS remains an attractive investment, boasting higher yields compared to similarly rated alternatives. These short securities leverage an appealing point on the yield curve and should continue to attract yield-focused investors seeking to capitalize on the current rate environment. While overall consumer health remains resilient, a cautious approach is warranted. Signs of stress are surfacing among lower-tier borrowers, necessitating vigilance in monitoring potential ripple effects. Navigating the asset class demands a balanced strategy that capitalizes on favorable short-term dynamics while staying attuned to emerging market risks.

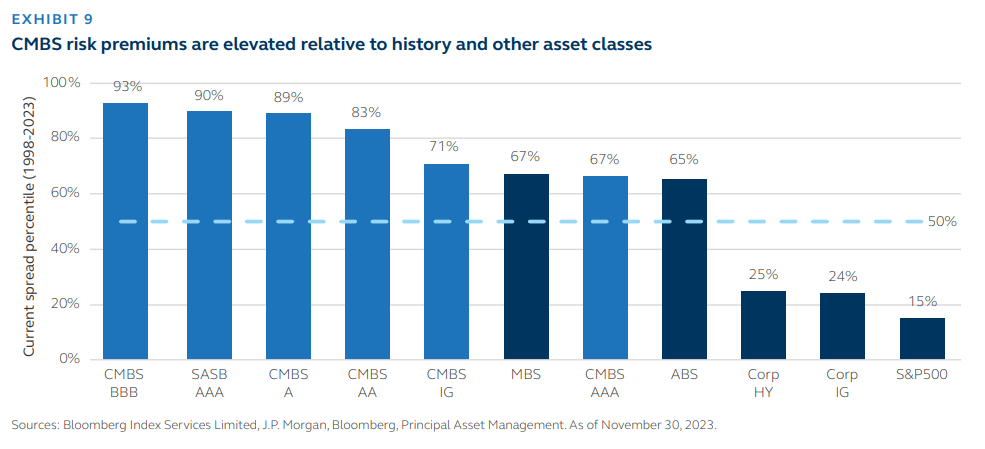

Commercial mortgage-backed securities ((CMBS)) CMBS continues to demand additional yield for potential recession risk, as evidenced by spreads trading in the 90-95th percentiles going back 20 years relative to comparable fixed income asset classes trading tighter than historical averages. If economic data continues to soften and the market firmly believes the Fed is done hiking, we expect transaction activity to pick up and bring transparency to property valuations. In this scenario, cap rates stabilize, the Treasury curve flattens, and credit spreads tighten. We believe this would support selectively layering in duration and credit exposure.

However, headwinds in the office segment are finally manifesting into loan delinquencies. While other property segments have seen stability, office delinquencies both in conduit and single-asset single-borrower loans increased in 2023, a trend we expect to continue in 2024 as borrowers, especially those with floating-rate liabilities and softer net operating income growth, struggle to secure refinancing in a higher-rate environment. Ultimately, there are opportunities within the CMBS market, but strong credit work and selectivity remain critical.

{kind=link}

Municipals

U.S. financial assets experienced a sudden and favorable rebound in prices during the final two months of 2023. Much of this rebound can be attributable to money returning to fixed income after inconsistent demand for most of the year. To those clients looking to increase allocations to IG credit, we view taxable U.S. municipal bonds as an attractive complement to those credit-centric mandates.

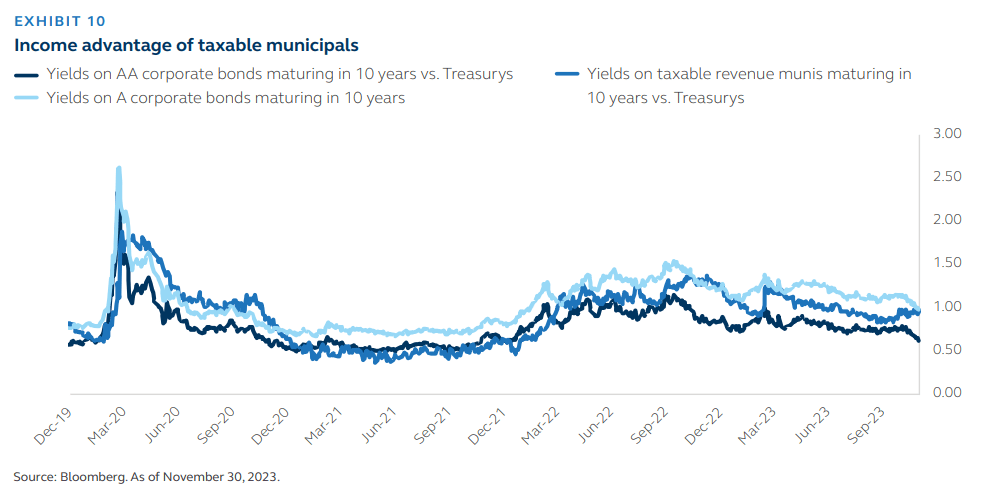

Though index-based total returns have been similar over 2023 (+8.84% in taxable municipals and +8.52% for IG corporate), taxable municipal spreads still provide an income advantage when compared to similar-maturity corporates. Ten-year taxable municipal spreads are wider than AA-rated corporate spreads while yielding about the same as A-rated corporate spreads (Exhibit 10).

{kind=link}

Similar income and spread advantages can also be realized in longer maturities. For liability-driven portfolios, longer-dated taxable municipals can be a particularly attractive option to match future liabilities. Coupled with the higher credit ratings of the asset class, the added income and duration are particularly favorable when risk-based capital charges are considered. The average credit rating of the Bloomberg Taxable Municipal Index is Aa2/Aa3 versus an average rating of A3/Baa1 for the Bloomberg U.S. Corporate Investment Grade Bond Index.

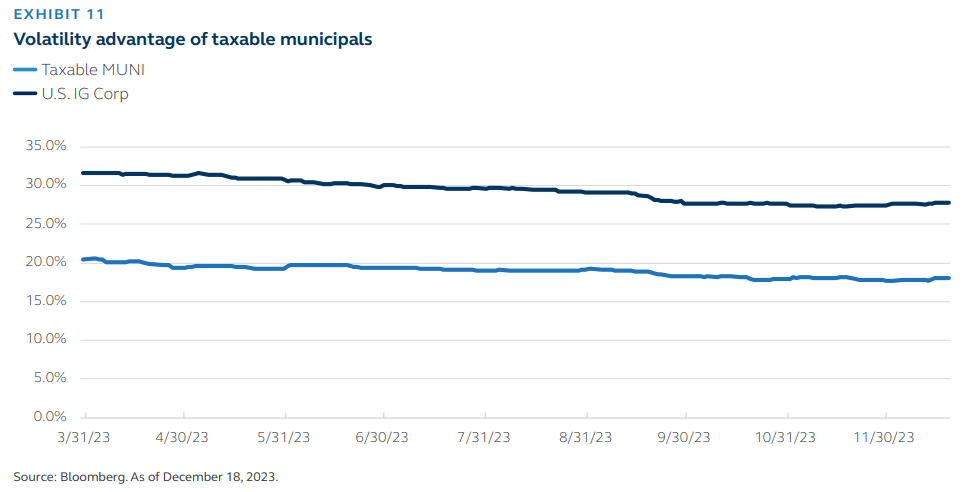

In addition to attractive spreads, taxable municipals offer correlation benefits and lower volatility - key attributes in risk management. Over the last year, taxable U.S. municipals have been less correlated to higher-beta asset classes - such as high yield debt and stocks - than corporate bonds, while exhibiting less spread volatility. The 360-day volatility of the spread of the Bloomberg Taxable Municipal Index is 18.1%, considerably lower than the 27.8% of the Bloomberg U.S. Corporate Investment Grade Bond Index.

{kind=link}

Admittedly, credit spreads are not as wide as a year ago, but we still see a relative value opportunity in 2024 with spreads compressing further based on diversification benefits and demand for high-quality, long-duration assets. With new issue supply projections flat versus 2023 levels, the demand/supply dynamic is likely to be supportive of spreads as well. Should lower hedging costs continue their recent trend, we anticipate increased interest from foreign accounts - especially Europe - further supporting this technical imbalance.

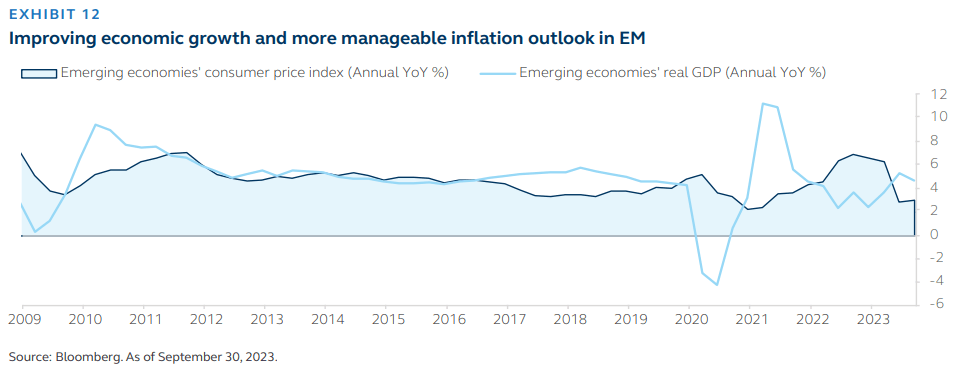

Emerging market debt ((EMD))

On the back of slowing developed markets ((DM)) growth and stabilizing emerging markets ((EM)) growth after a resilient performance in 2023 led by Brazil, Mexico, and India and the reopening of the economy in China, EM is set to increase its growth outperformance versus DM in 2024. Despite investor skepticism of the asset class given the ongoing geopolitical tensions, a lack of recovery in China, and the renewed socialist momentum in Latin America, one of the key factors of EM performance was orthodox policy in many EM nations, managing their inflation dynamics with credible monetary policies. This factor, coupled with the Fed undertaking a shift in policy, sets the stage for a relative bounce in EM debt with many EM countries already experiencing moderating inflation and monetary policy easing. For instance, recent policy easing measures in China to address declining growth momentum and the upswing in the technology cycle - led by investments in AI - offer notable support to key EM economies. That said, pockets of EM are continuing to show stress in the post-pandemic environment or for legacy reasons; however, on balance these risks are already suitably priced in the markets.

Geopolitically, we expect 2024 to be an intense year of elections across the emerging market countries. Following Taiwan, national elections are scheduled for 40 countries, including Indonesia, India, Mexico, Russia, and Ukraine. The outcome of the 2024 U.S. election could have deep implications for global geopolitics - the direction of the Russia/Ukraine and the Middle East conflicts, U.S./China strategic competition, and the broader relationship between the global south and the West and between Western allies themselves.

Away from the primary EM markets, we see the potential for select distressed stories to find new life and possibly return to normal trading markets. These include new leadership and a possible new policy direction in Argentina and sanction relief for Venezuela with the potential for some form of resolution of outstanding defaulted debt. The conflict in Ukraine seems likely to find a resolution, as funding and fatigue from both sides are growing; however, the context of how that might occur remains unclear. Additionally, Russian sanctions are unlikely to be dropped in 2024, even with a cessation of fighting. Investors will also be watching the Israeli/Hamas conflict. With limited market spillover to the greater Middle East, we remain bullish on the region into next year. The speed of developed market rate cuts and the broader opening of capital markets will also be key determining factors for the ability of frontier market players to address their near-term debt maturities and avoid renewed debt distress. Our base case into 2024 remains optimistic about the EM sector.

{kind=link}

Private credit

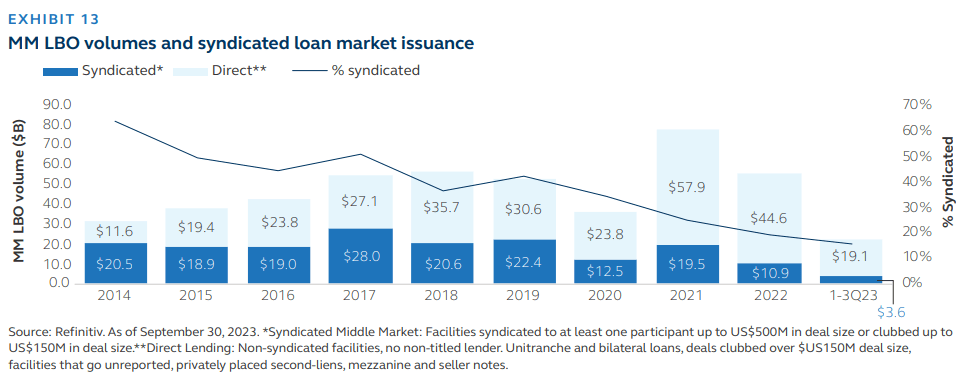

Direct Lending In 2023, tightening credit conditions, an uncertain economic environment, and declining enterprise value multiples slowed M&A and leveraged buyout ((LBO)) activity in the direct lending space. With fewer loan prepayments and refinancing activity and less natural deal flow from new LBOs, capital deployment for many lenders slowed significantly. Despite the slowing, middle market direct lending continued to fill the void left by commercial banks and the continued decline in syndicated loan market issuance (Exhibit 13).

{kind=link}

While these trends are likely to play out further in 2024, investors have now had over a year to embrace higher interest rates. With less fear of “rate whiplash” and having had time to digest the denominator effect (the value of fixed rate instruments and equity falling in a correlated manner with rising rates), investor flows are likely to pick up considerably for middle market direct lending.

Although headwinds to the economy are expected, several supportive trends for middle market direct lending have an opportunity to enhance risk-adjusted returns relative to historical loan vintages.

- Increased focus on economically resilient business models: Focus will remain on the more cyclically resilient industries and borrowers that can generate steady financial performance through a cyclical downturn.

- More conservative leverage profile: Leverage expectations are considerably lower than levels targeted just a couple of years ago in a much lower-rate environment.

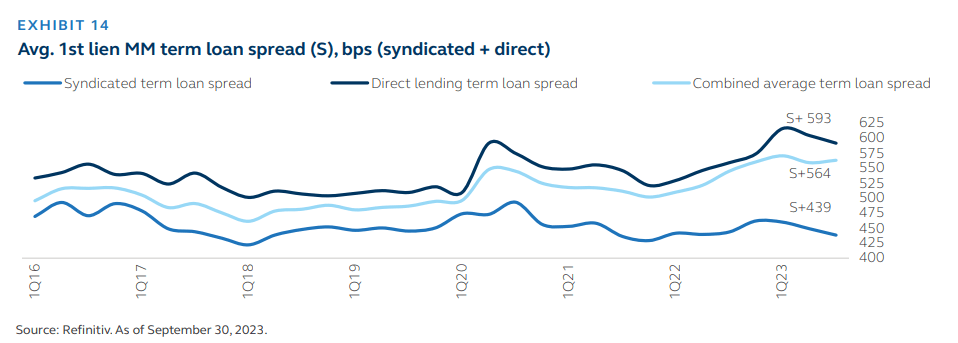

- Valuations remain attractive: With not only the base secured overnight financing rate (SOFR) remaining at a relatively high level, the spread premium to public high yield loans is and will likely remain near the upper end of the range for much of the coming year.

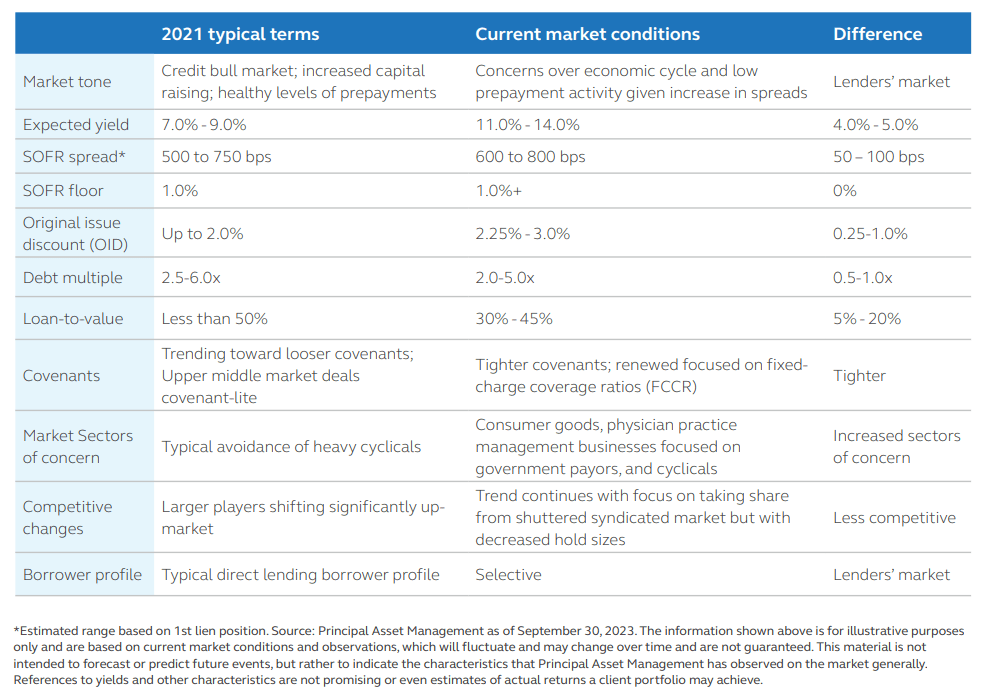

- More lender-friendly transaction terms: The structure of transactions should remain sound, with higher original issue discount, improved call protection, tighter financial covenants, and more conservative EBITDA adjustments.

- Manageable default rates: Despite annual default rates potentially moving higher and approaching 3-4% for the private middle market, credit losses should remain in the 75-150 bps range.

{kind=link}

{kind=link}

Intentional industry exposure, coupled with a disciplined credit structure and a highly selective process to identify companies that exhibit steady performance through a down cycle, should result in more favorable risk-adjusted returns.

Investment grade private credit Based on early indications, U.S. private placement market issuance will start strong in 1Q relative to prior years due to the timing of the annual industry conference being pushed back into February. Whether overall volumes in 1Q will be up relative to prior years is less clear, but we do expect more deal opportunities in the market in the weeks prior to the conference than is typical. Some high-quality financial-related issuers - CRE and alt asset/funds - are guiding to modestly higher leverage for market-related reasons after operating at the lower end of their leverage ranges. As such, we expect a nominal uptick in high-quality financial sector deal flow in the first half of 2024. Most of the ODCE Core REIT issuers are operating well within covenants where leverage limits can be as high as 60%, and many are operating in the mid-20% to mid-30% range. Conversely, some ODCE Core Plus REITs are showing initial signs of weakness related to the more interest rate-sensitive covenants, and the market may see an uptick of amendment discussions with those issuers in early 2024. Other active sectors should include private debt capital needs for infrastructure projects - energy transition, renewable power, and LNG liquefaction - which are expected to lead to strong issuance in 2024 beginning in 1Q. Data center and fiber ABS issuance will also continue into 2024, which may be seen in the IG private credit market. However, as rate increases end or potential rate cuts gain momentum, some issuers may wait to approach the market until the second half of 2024.

{kind=link}

Conclusion

With the economy ending the year on a relatively strong footing and peak rates likely behind us, the first quarter of 2024 appears to be the start of a new regime for global central banks. With key inflation measures trending in the right direction, the employment picture proving resilient and economic data softening, many anticipate policymakers to shift away from a period of aggressive policy action toward a period of measured observation - a pause. In turn, this will likely lead to an environment where bond yields remain elevated (and attractive), while the appeal of cash/cash equivalents diminishes. In our view, the shift in posture by policymakers will ultimately afford time for a slowdown in underlying growth to be further realized. This will put pressure on growth assets as well as test policymakers as they attempt to sidestep a recession and eventually lead to a policy pivot later in 2024.

So, what does this mean for fixed income investors? In the near term, with a pause to start the year, high-quality fixed income that allows for an extension in duration should deliver attractive results on a risk-adjusted basis. For those with a longer-term investment horizon, adding risk now will likely be rewarded as policymakers shift from a hawkish stance towards a dovish stance in the year ahead. Overall, most fixed-income asset classes should fare well, supported by attractive yields and resilient fundamentals.

Editor's Note: The summary bullets for this article were chosen by Seeking Alpha editors.

For further details see:

Fixed Income Perspectives - Looking Ahead At Q1 2024: A Turning Point For Policy