SCGLF - FLC: High-Risk High-Reward Yield Play With This Preferred Stock CEF

2023-09-27 05:34:23 ET

Summary

- The Flaherty & Crumrine Total Return Fund is a fixed-income fund that primarily invests in preferred stock.

- The fund has experienced disappointing performance due to rising interest rates, but its high current yield is attractive.

- FLC's leverage and distribution cuts may be concerning, but its current discount on net asset value makes it a reasonable investment option.

- The biggest risk here is interest rates, but it is likely that rates have peaked in the absence of commodity-driven stagflation.

- The fund may be worth owning for those who are comfortable with the risks, although the only significant return for a while will be the distributions.

The Flaherty & Crumrine Total Return Fund ( FLC ) is a closed-end fund that can be used by investors who are looking to generate a high level of income from the assets in this portfolio. This fund is a bit unusual as its name does not really reflect its portfolio or strategy. This is actually a fixed-income fund that invests primarily in preferred stock, just like most of Flaherty & Crumrine's other closed-end funds. The name suggests that it invests in common equities, but these securities only comprise a very tiny proportion of the fund's portfolio. The fund's credentials as a source of income are quite attractive though, as its 7.38% current yield is higher than most things in the market and it is one of the few assets with a higher yield than money market funds or short-term U.S. Treasuries today.

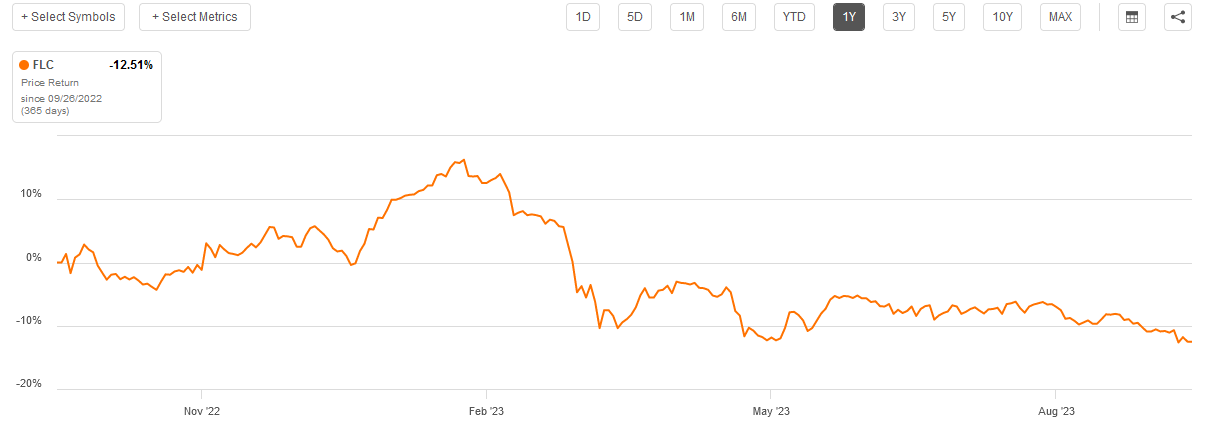

As has been the case with most fixed-income funds, the Flaherty & Crumrine Total Return Fund has delivered a rather disappointing performance over the past year, as rising interest rates have pushed down fixed-income prices. Over the past twelve months, the fund's shares have declined by 12.51%:

{kind=link}

This is a significantly larger decline than most fixed-income indices have delivered, but the higher yield of this fund relative to the indices offsets this poor price performance somewhat. The fund does still have a negative total return over the period though, so it has still handed losses to its investors. This could make the fund unattractive today, particularly for risk-averse investors or those who are otherwise concerned with the preservation of principal. This is understandable, but it is important to keep in mind that the losses that the fund handed investors over the past year will not affect anyone buying the fund today. The most important thing is where the fund is going in the future, so we will want to investigate that over the course of this article.

About The Fund

According to the fund's website , the primary objective of the Flaherty & Crumrine Total Return Fund is to provide its investors with a high level of current income. Specifically, the website states:

The Fund's primary investment objective is to provide its shareholders with high current income. The Fund's secondary investment objective is capital appreciation.

In seeking its investment objectives, the Fund will normally invest at least 80% of its total assets in a diversified portfolio of preferred securities and other income-producing securities, consisting of various debt securities. The portions of the Fund's assets invested in various types of preferred, debt or common stock may vary from time to time depending on market conditions, although the Fund will normally invest at least 50% of its total assets in preferred securities.

This description makes it quite clear that the Flaherty & Crumrine Total Return Fund is primarily a preferred stock fund, despite its name. As such, we might expect that the majority of the fund's assets will be invested in preferred stock. This is indeed the case, as we can clearly see here:

CEF Connect

The fund's strategy description states that at least 50% of its assets will be invested in preferred stock in most cases, and we can certainly see that reflected above. The fund's allocation to fixed-income securities is much higher though, as the preferred stock plus bond allocation is 91.93%. The fund also has a 3.20% allocation to convertible securities, but these do not trade exactly like other fixed-income securities because of the conversion component. Convertible securities are still somewhat interest-rate sensitive just like preferred stock and bonds, but the price of the linked stock can also play a role in pricing these securities. Regardless, we can still see that the overwhelming majority of this fund's portfolio consists of fixed-income securities despite the name of the fund implying that it will invest in common stocks, bonds, and preferred securities in order to achieve the maximum possible total return.

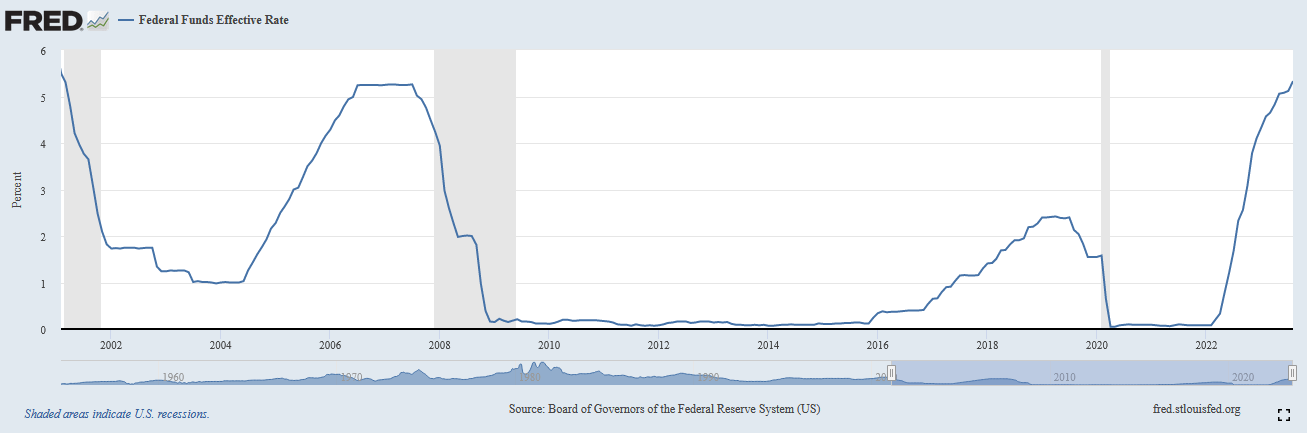

As everyone reading this is no doubt well aware, fixed-income securities prices have an inverse relationship to interest rates. The Federal Reserve has been aggressively raising interest rates in the United States since March 2022 as part of an effort to combat the incredibly high inflation rate that is plaguing the American economy. As of the time of writing, the effective federal funds rate stands at 5.33%, which is the highest level that we have seen since February 2001:

{kind=link}

This is the biggest factor that has been pushing down the price of the Flaherty & Crumrine Total Return Fund over the past year. After all, preferred stock tends to trade like bonds that have no maturity date, so the overwhelming majority of the fund's assets have prices that inversely correlate to the market interest rate.

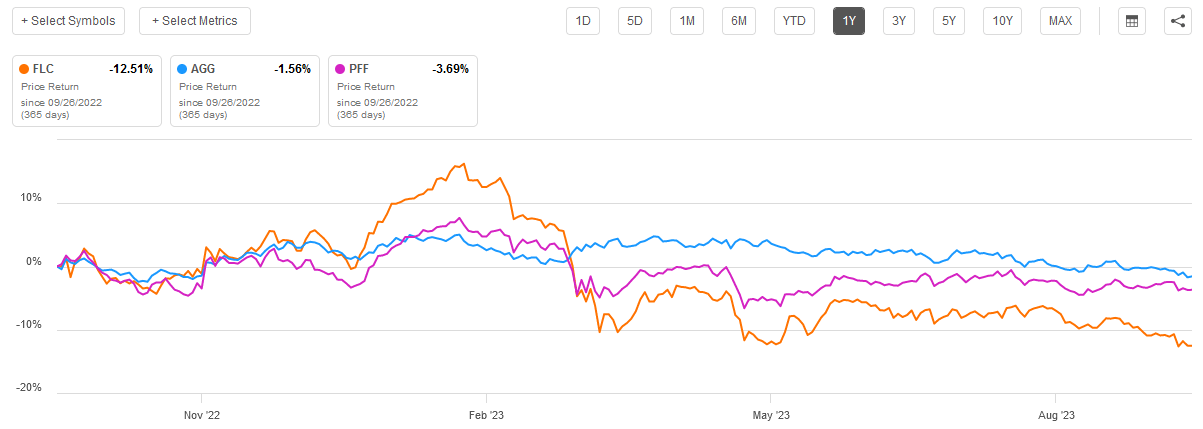

Unfortunately, despite a bit of strength earlier this year, the fund's performance has since fallen off a cliff. Over the past year, the fund has underperformed both the Bloomberg U.S. Aggregate Bond Index ( AGG ) and the ICE Exchange-Traded Preferred & Hybrid Securities Index ( PFF ):

{kind=link}

This is disappointing, particularly given the magnitude of the underperformance. One of the reasons for this is that the Flaherty & Crumrine Total Return Fund employs leverage as a means to boost its returns, but it also boosts the fund's losses. We will discuss this later in this article. Another factor may be the fact that the fund cut its distribution in February, May, and August. As we can see above, the fund suffered fairly large declines right around that time. This is partly because the market will sometimes price closed-end funds at a level that gives the fund a certain yield. We see this with things like the AllianceBernstein Global High Income Fund ( AWF ), which has actually gone up over the past year despite being unable to cover its distribution out of investment profits (see my recent article on this fund for more information).

Thus, we likely have a combination of factors that adversely impacted the share price of the Flaherty & Crumrine Total Return Fund over the past year. However, as I stated in the introduction, anyone buying the fund today will be unaffected by these losses. They will only be affected by the fund's performance going forward. As the fund's portfolio is heavily weighted to interest-rate sensitive securities, this forward outlook depends heavily on what policy the Federal Reserve takes going forward. I discussed the potential outlook for interest rates in a very recent article and see no real need to repeat the full discussion here. After all, that other article is fully available to be read and reviewed. In short, though, the outlook largely boils down to the direction of crude oil prices and inflation. There are two possible scenarios:

- If the global economy remains reasonably strong and demand for crude oil remains high over the next few quarters, then rising crude oil prices could push the United States into a stagflationary period resembling the 1970s. The Federal Reserve may be forced to push interest rates higher.

- In the absence of such a scenario, rates decline slightly in 2024 and continue a slow decline before settling into a long-term neutral range of around 3% in 2027 or later.

If we assume that the United States will avoid the stagflation scenario, then we can assume that the worst is behind us as far as the fund's losses are concerned. While it is unlikely that the fund will deliver rapid or substantial gains in the near term, it should be able to remain at least relatively stable or slowly appreciate while providing a high yield that can be used to purchase other assets (or reinvested into the fund) or spent to support your lifestyle. If the stagflation scenario actually occurs, then pretty much everything except crude oil, gold, and other commodities is going to get pulverized. Obviously, the fund's shares would continue to decline in such a scenario.

One of the defining characteristics of most preferred stock funds is that they usually have a fairly high weighting to the banking sector. The Flaherty & Crumrine Total Return Fund is no exception to this, as currently 55.9% of the fund's assets are invested in the banking sector:

Flaherty & Crumrine

This may be concerning for some investors considering that the United States saw three major bank failures this year. Credit Suisse ( CS ), one of the two largest banks in Switzerland, also failed but Credit Suisse had been having problems for quite a while and the problems in the American banking system may have just been a catalyst for its failure. In response to the failures, the Federal Reserve unveiled an emergency bank lending program that allows banks to borrow against the face value of depreciated assets, such as U.S. Treasury securities that have gone down in price as interest rates have risen, in order to meet depositor demands. It appears that this has stabilized the system, even though there is currently $108 billion in outstanding loans to regional banks under the program. This was not a situation like what occurred in 2008 as the nation has not yet seen a wave of defaults on formerly high-rated debt securities or loans. Thus, there is probably no real need to worry about the risk of bank failures reducing the value of the preferred stocks in the portfolio. There is also probably no real reason to worry about banks defaulting on their preferred stock dividend payments. The real risk to this fund's portfolio is the trajectory of interest rates, and that risk is pretty reasonable in the absence of a worst-case stagflation scenario.

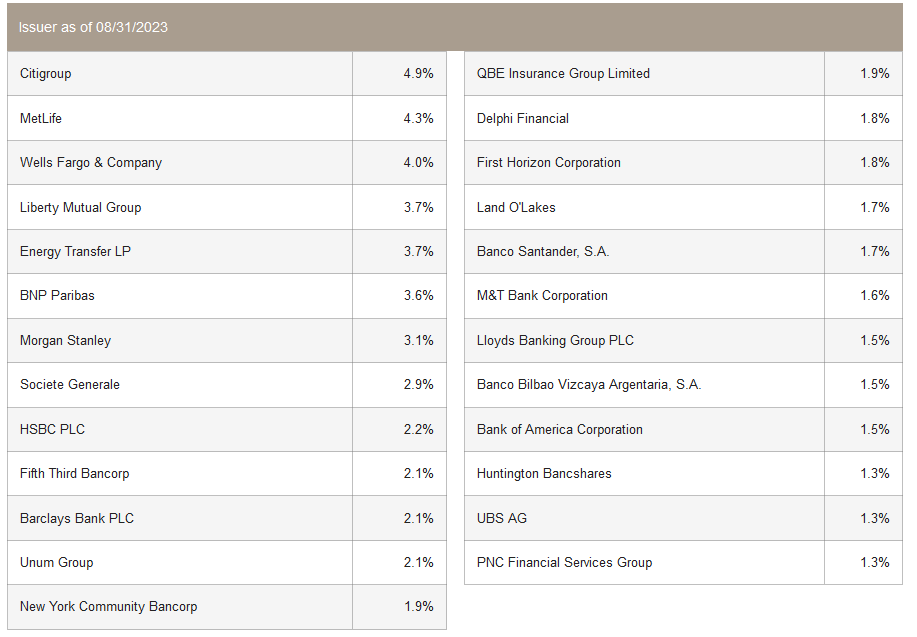

It is important to note that not all of the securities that are held by the fund are from American issuers. We can see this by looking at the largest positions in the fund. Here they are:

{kind=link}

We see BNP Paribas ( BNPQF ), Societe Generale ( SCGLF ), HSBC (HSBC), Barclays ( BCS ), and several other issuers on this list that are not American companies. In fact, only 70.6% of the fund's assets are invested in securities from American issuers:

Flaherty & Crumrine

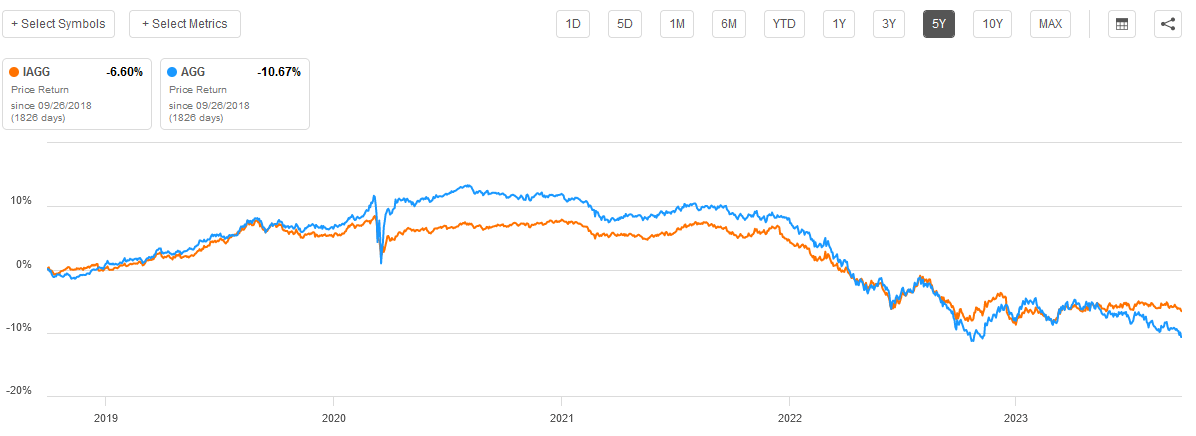

This does change the interest rate risk somewhat. Foreign securities are much more affected by the interest rate and monetary policies of their home countries than by anything the Federal Reserve does. This is why the Bloomberg Global Aggregate ex-USD 10% Issuer Capped Index ( IAGG ) does not have the same yield or trade in lockstep with the Bloomberg U.S. Aggregate Bond Index:

{kind=link}

We can see that the two indices have had some similarities, but that is because most developed countries have had similar interest rate policies over the past several years. Overall, though, we can still see that the fact that 29.40% of the assets of the Flaherty & Crumrine Total Return Fund are invested in securities from non-American issuers means that we cannot depend solely on the monetary policies of the Federal Reserve to determine its trajectory. However, the policies of the U.S. central bank still dominate the majority of the portfolio, so it is by far the most important institution to watch for those who are investing in this fund.

Leverage

As mentioned earlier in this article, the Flaherty & Crumrine Total Return Fund employs leverage as a method to artificially boost the effective yield and total return of its portfolio. This is a strategy that is used by most closed-end funds. I explained how it works in numerous previous articles. To paraphrase myself:

Basically, the fund borrows money and then uses that borrowed money to purchase preferred stock, debt securities, and other income-producing assets. As long as the purchased securities have a higher yield than the interest rate that the fund has to pay on the borrowed money, the strategy works pretty well to boost the effective yield of the portfolio. As this fund is capable of borrowing money at institutional rates, which are considerably lower than retail rates, that will ordinarily be the case. However, it is important to note that leverage is less effective at boosting yields today with rates at 6% than it was two years ago when rates were 0%. This is because the difference between the yield that the fund can receive and the rate at which it can borrow is much narrower than it once was.

Unfortunately, the use of debt in this fashion is a double-edged sword. This is because leverage boosts both gains and losses. As such, we want to ensure that the fund is not employing too much leverage because that would expose us to an excessive amount of risk. I do not like to see a fund's leverage exceed a third as a percentage of its assets for this reason.

Earlier in this article, we saw that the Flaherty & Crumrine Total Return Fund typically declined much more than either of the major preferred stock indices during periods of market weakness. This is partially due to the effects of the fund's leverage boosting the fund's losses. That is the primary reason why we do not want the fund's leverage to be excessively high. As of the time of writing, the Flaherty & Crumrine Total Return Fund has leveraged assets comprising 41.28% of its portfolio. That is substantially higher than what we normally see in other preferred stock funds, as well as being well above the one-third limit that would like to see as a maximum. This fund therefore appears to be running a fairly high-risk, high-reward strategy. This has certainly proven to be a mistake over the past eighteen months or so, although it could actually benefit the fund going forward once the central bank is able to cut rates. This is still a risk that we should not ignore, however.

Distribution Analysis

As mentioned earlier in this article, the primary objective of the Flaherty & Crumrine Total Return Fund is to provide its investors with a very high level of current income. In pursuance of this objective, the fund has assembled a portfolio consisting of preferred stock, bonds, and other assets that deliver the majority of their investment returns in the form of direct payments to their owners. As such, these assets typically have higher yields than most other things in the market. The fund collects the payments that it receives from these securities, and even applies a layer of leverage to boost them, and pays them out to its shareholders, net of investment expenses.

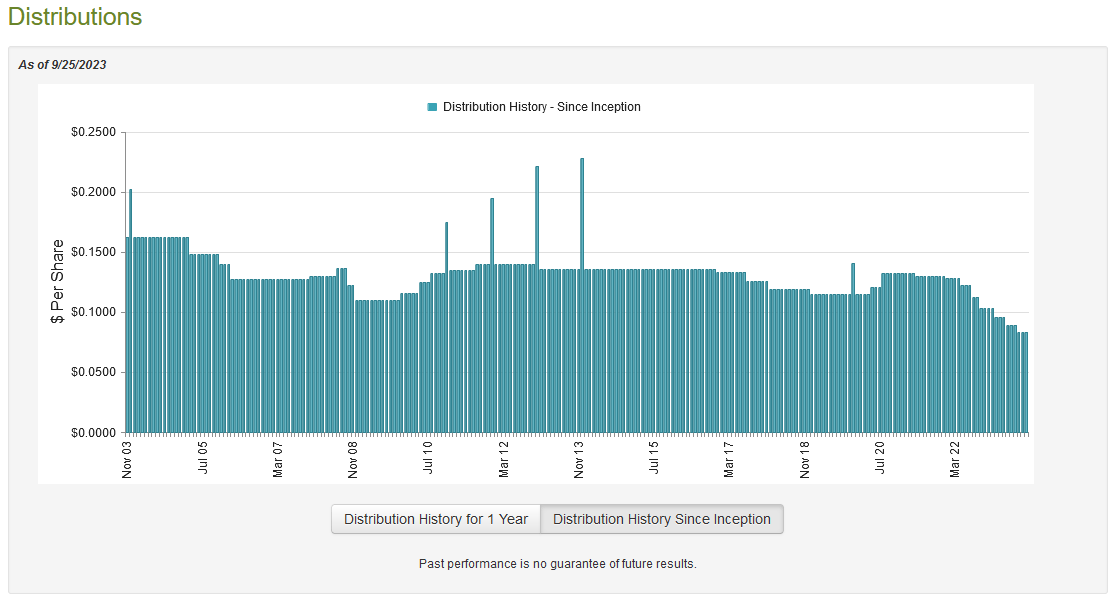

This basic business model suggests that the fund will have a very high yield. That is indeed the case, as the fund currently pays a monthly distribution of $0.0835 per share ($1.002 per share annually), which gives it a 7.38% yield at the current price. Unfortunately, the fund has not been particularly consistent with respect to its distribution, having both raised it and cut it multiple times since its inception:

{kind=link}

This is almost certainly going to be a turn-off for any investor who is seeking a safe and secure source of income to pay their bills or finance their lifestyles. The fact that this fund has cut the distribution four times in the past twelve months certainly will do nothing to boost its appeal among these investors. However, this sort of variation in the distribution over time is very typical for fixed-income funds due to the general interest rate sensitivity of their assets. After all, no fund is sufficiently large to control the market interest rate. In addition, most Flaherty & Crumrine fixed-income closed-end funds have reduced their distributions multiple times over the past year so this one is hardly alone in that respect.

As I pointed out earlier, anyone buying today does not have to worry about the distribution cuts that the fund imposed in the past. This is because anybody buying the fund today will receive the current distribution at the current yield and will be completely unaffected by past events. Thus, the most important thing is how well the fund can sustain its distribution going forward, so let us investigate this.

Fortunately, we have a fairly recent document that we can consult for the purpose of our analysis. As of the time of writing, the fund's most recent financial report corresponds to the six-month period that ended on May 31, 2023. The market for fixed-income securities was surprisingly strong during the first half of 2023, due mostly to investor expectations that the Federal Reserve would quickly cut rates. As we have seen, this assumption proved to be false but that did not prevent the market from handing opportunities for the fund to earn some capital gains by selling assets into this strength. This report should give us a good idea of how well it managed to accomplish that task.

During the six-month period, the Flaherty & Crumrine Total Return Fund received $3,606,204 in dividends along with $6,385,440 in interest from the assets in its portfolio. When we combine this with a small amount of income from other sources, we get a total investment income of $10,019,210 for the fund during the six-month period. The fund paid its expenses out of this amount, which left it with $5,530,248 available for shareholders. As might be expected, this was not enough to cover the $6,091,098 that the fund actually paid out during the period, but it did get pretty close. However, we usually like a fixed-income fund to completely cover its distributions out of net investment income so this situation is concerning.

With that said, the fund does have other methods through which it can obtain the money needed to cover its distributions. For example, it could have been able to generate capital gains by taking advantage of the aforementioned market strength during this period. Unfortunately, the fund failed miserably at this task. It reported net realized losses of $4,968,271 and incurred another $8,952,899 in net unrealized losses. Overall, the fund's net assets declined by $14,482,020 during the period after accounting for all inflows and outflows. Obviously, this fund failed to cover its distributions, which certainly explains the wave of distribution cuts. It seems quite possible that the fund is trying to bring its distribution into line with its net investment income. That would certainly be nice if it manages to do so, but we will need to wait until the fund releases its full-year financial report to know for certain. That document probably will not be released until early next year. However, the fund probably is getting pretty close to fully covering its distribution out of net investment income so we should not have to worry too much about it.

Valuation

As of September 25, 2023 (the most recent date for which data is currently available), the Flaherty & Crumrine Total Return Fund has a net asset value of $16.12 per share but the shares currently trade for $13.46 each. This gives the fund's shares a whopping 16.50% discount on net asset value at the current price. This is one of the largest discounts available in the market for any closed-end fund, and it is obviously much better than the 12.52% discount that the shares have averaged over the past month. As such, the current price certainly looks quite reasonable.

Conclusion

In conclusion, the Flaherty & Crumrine Total Return Fund is a preferred equity closed-end fund, despite the name implying that it is something else. As such, the fund's forward performance depends heavily on interest rates, and these are uncertain. While the Federal Reserve currently expects that rates have peaked and will very slowly decline, there is a risk of stagflation caused by rising commodity prices that could force them up further. The fund's distribution is probably secure right now, although the multiple cuts over the past year are certainly not doing the fund any favors among those investors who are seeking a safe source of income. The fund's leverage is also a bit high, but this could work in its favor as rates start to decline. Overall, the fund could be a reasonable investment right now if you are comfortable with the interest rate risk.

For further details see:

FLC: High-Risk, High-Reward Yield Play With This Preferred Stock CEF