PFF - FLC: This Fund May Not Be Able To Sustain Its Recent Gains (Rating Downgrade)

2024-01-10 13:10:33 ET

Summary

- Flaherty & Crumrine Total Return Fund has suffered from multiple distribution cuts, resulting in a low forward yield of 6.81%.

- The FLC closed-end fund's share price has increased by 9.53% since the last article, outperforming the preferred stock index and bond index.

- The fund's exposure to the banking sector has increased, and its leverage remains high, posing risks for investors.

- The fund may not be able to hold onto its recent gains, as the economy is too strong and inflation is too high to justify recessionary rate cuts.

- The fund is trading at a lower-than-average discount, providing an opportunity to realize some gains and reduce risk.

The Flaherty & Crumrine Total Return Fund ( FLC ) is a closed-end fund, or CEF, that has long been a fairly popular one among income-focused seekers due to its relatively high yield. Unfortunately, this fund has suffered from a few of the problems that have plagued other closed-end funds from this particular fund house over the past two years. In short, a series of distribution cuts has devastated the distribution to the point that the fund only has a 6.81% forward yield. That is pretty low for a closed-end fund, as even equity funds manage to beat this yield. It is terrible for a fixed-income fund like this one, as most of the other funds that we have discussed in this column yield above 9% right now.

For example, consider the John Hancock Preferred Income Fund III ( HPS ), which we discussed yesterday. That fund has a 9.01% forward yield, which obviously beats the Flaherty & Crumrine Total Return Fund by a few hundred basis points, which adds up to a lot of money over time due to the effects of compounding. As such, income-focused investors may be best off looking elsewhere right now unless there is some reason to believe that things will improve for this fund. Unfortunately, it does not appear that a turnaround is imminent as we will discuss in the course of this article.

As regular readers will likely remember, we last discussed the Flaherty & Crumrine Total Return Fund in late September. It was a very different market environment at that time. In late September, the market was still suffering from a secular bear as the euphoria from earlier in the year was rapidly wearing off and investors began to expect that the Federal Reserve would not be reducing interest rates anytime soon. This mood changed a few weeks following the publication of the previous article, and the market began to drive up the price of just about everything in the market in anticipation of a massive loosening of monetary policy in 2024.

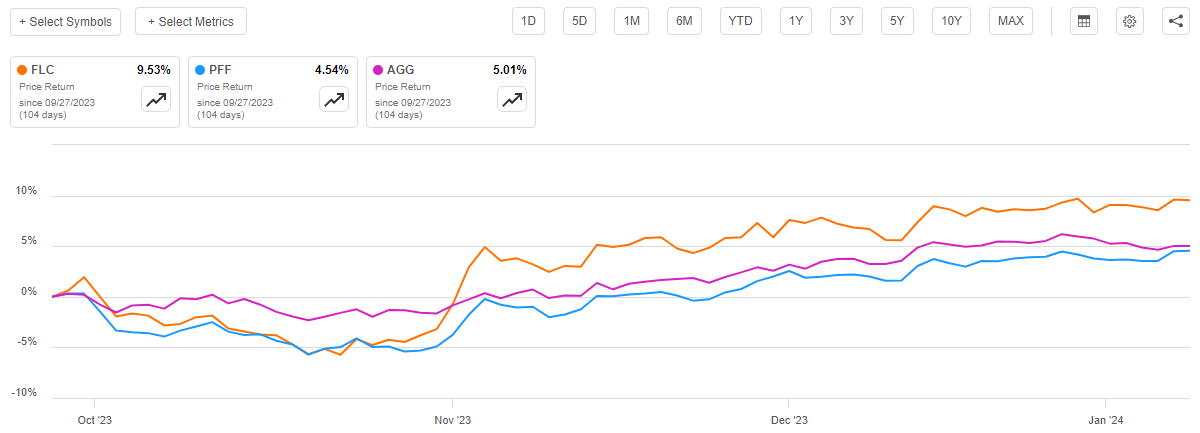

This fund’s share price certainly benefited from that end-of-year euphoria, as the share price has increased by 9.53% since the date that the previous article was published. This is quite a bit better than the 4.54% gain in the ICE Exchange-Listed Preferred & Hybrid Securities Index ( PFF ) and the 5.01% gain in the Bloomberg U.S. Aggregate Bond Index ( AGG ):

{kind=link}

This strong performance is one reason for the low yield, as rising share prices will naturally decrease the yield from that security. There could be some reasons to believe that the fund will not be able to sustain these gains, though. The most notable of these is that the market has priced in a level of interest rate cuts that would require a severe recession to justify and recent economic data is too strong to suggest that a recession is on the recession. In fact, the current data shows that the economy has been improving since October and as such any rate cuts risk reigniting inflation. As such, the share price may have gotten ahead of itself, which we will discuss in more detail later in this article. If this is the case, then it could be positioned for a near-term decline, which suggests that investors who have benefited from this gain may want to sell some of their positions now in order to lock in some of the gains that they have already received.

About The Fund

According to the fund’s website , the Flaherty & Crumrine Total Return Fund has the primary objective of providing its investors with a very high level of current income. This is somewhat surprising considering the name of this fund, but it does make sense considering the fund’s strategy. As the website explains,

The Fund’s primary investment objective is to provide its investors with a high level of current income.

…

In seeking its investment objectives, the Fund normally will invest at least 80% of its total assets in a diversified portfolio of preferred securities and other income-producing securities, consisting of various debt securities. The portions of the Fund’s assets invested in various types of preferred, debt or common stock may vary from time to time depending on market conditions, although the Fund will normally invest at least 50% of its total assets in preferred securities.

The Fund will invest, under normal market conditions, at least 25% of its total assets in the financials sector, which for this purpose is comprised of the bank, thrifts & mortgage finance, diversified financial services, finance, consumer finance, capital management, asset management & custody, investment banking & brokerage, insurance, insurance brokerage and real estate investment trust industries. From time to time, the Fund could have more than 25% of its total assets in insurance companies, while at other times it could have that portion in banks. At all times, though, the Fund would have at least 25% of its total assets invested in the financials sector. In addition, the Fund also may focus its investments in other sectors or industries, such as (but not limited to) energy, industrials, utilities, communications, and pipelines. The Adviser retains broad discretion to allocate the Fund’s investments as it deems appropriate considering current market and credit conditions.

This description strongly suggests that investors should generally expect that the fund will normally be invested in the banking and financial services sector. This is certainly the case right now, as 57% of the fund’s assets are invested in securities issued by banks. The fund also has 3.5% invested in “Finance” companies but does not specify exactly what these companies might be involved in. Presumably, these are non-bank companies that still make loans to consumers or businesses.

Flaherty & Crumrine

We can also see a 20.7% allocation to insurance companies, which means that this fund is somewhat more allocated to the financial services sector than the broader preferred stock index. This is what BlackRock lists for the sector holdings of the iShares Preferred and Income Securities ETF, which we are using as a proxy for the preferred stock index:

{kind=link}

The index fund has 73.90% of its assets invested in “Financial Institutions,” but it does not specify exactly what qualifies as a financial institution. If we assume that it is banks, insurance companies, and non-bank financial companies then the Flaherty & Crumrine Total Return Fund has 81.2% of its assets invested in such companies, which is considerably more than the index. As such, investors in the fund should be very comfortable investing in this sector and should design their portfolios appropriately to ensure that they are properly diversified. After all, the financial services sector accounts for 13.04% of the S&P 500 Index (SP500) so having an S&P 500 Index fund combined with this one will give you a fairly large exposure to the sector that will need to be diversified away.

The fund’s exposure to banks has increased a bit since the last time that we discussed it. As noted in the previous article, at that time the fund had 55.9% exposure to the banking sector. It did have 22.3% of its assets invested in securities issued by the insurance sector though, so it appears that the fund may have moved some of its assets from insurance into banks. This fund only has a 7.00% annual turnover though so a large move of its assets like that would be unusual. It is possible that the fund’s assets in the banking sector outperformed the insurance company’s securities, which increased its weighting to the banking sector but that would be unusual. After all, preferred securities typically move based on interest rates and not so much on the performance of the issuing company. Regardless of the reason, we can still see that the fund increased its exposure to banks at the expense of insurance companies during the fourth quarter.

The banking sector is currently sitting on $600-$700 billion of unrealized losses. This is mostly due to fixed-rate U.S. Treasuries, mortgage loans, and other instruments that declined in value in a rising interest rate environment. The scale of these losses is sufficient that it may worry some investors, but this is a very different problem than the banking sector experienced back in 2007. There has not been a spike in defaults that is forcing banks to realize losses. As long as there are no more bank runs, the unrealized losses should eventually be erased as the securities mature, or interest rates decline and cause capital appreciation in the currently depreciated securities. The Federal Reserve implemented a program back in the Spring of 2023 that has generally been effective at preventing banks from needing to sell their depreciated assets to meet the withdrawal demands of depositors, so we probably do not have to worry about this problem.

However, the Federal Reserve program was theoretically temporary, so investors might still have concerns about the banking sector. As such, they may be inclined to avoid this fund due to its high exposure to the banking sector. However, every preferred stock fund will be heavily weighted to the banking sector because banks are by far the largest issuers of preferred securities in the market.

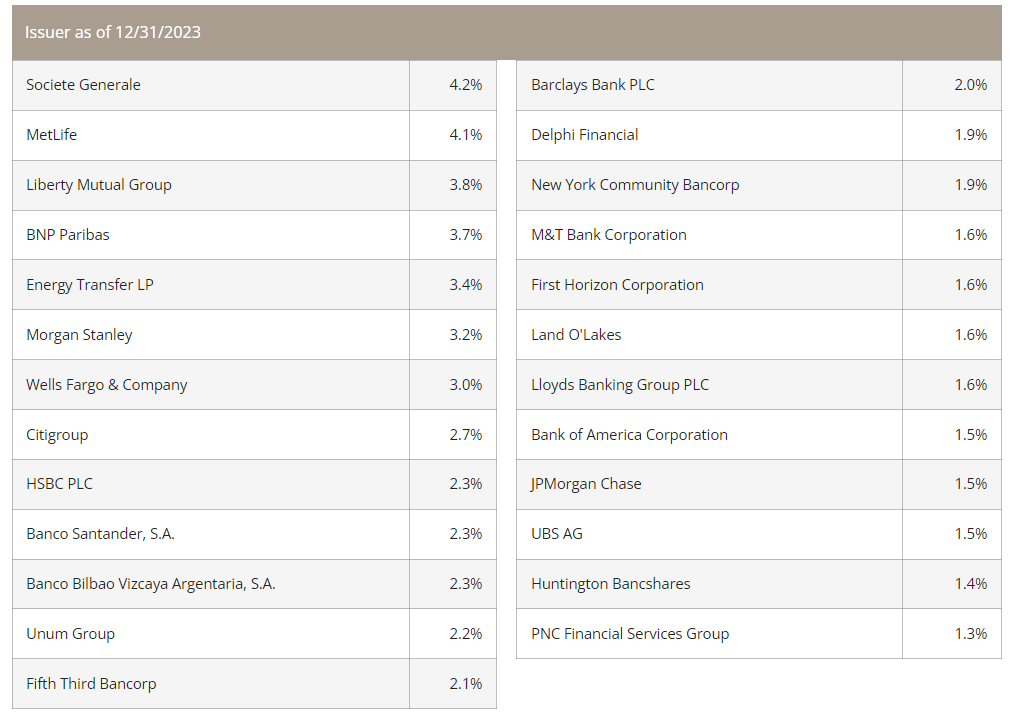

As the Flaherty & Crumrine Total Return Fund has a very low turnover, we can probably expect that many of the fund’s largest positions will be the same as the last time that we discussed it. This is certainly the case. Here are the largest positions in this fund as of the time of writing:

{kind=link}

There have been some changes here, but most of them are fairly minor changes that are simply weighting changes. For example, Citigroup ( C ) represented 4.9% of the fund’s total assets a few months ago but today it only represents 2.7% of the fund’s assets. There are numerous examples of changes like this, but the actual companies that are on the list have not really changed. That is exactly what we would expect considering this fund’s very low turnover, as weighting changes can be the result of one company outperforming another in the market.

Once again, though, we do not normally see vast performance differences between preferred stocks, so the fund is probably doing a bit of active management to change its weightings. Overall, though, we can clearly see that this fund does not change its portfolio nearly as much as some other funds do. Investors should be able to appreciate this because it helps to keep expenses down.

The Reason For The Sell Rating/Thesis

As mentioned in the introduction, investors have been bidding up the share price of the Flaherty & Crumrine Total Return Fund in anticipation of a series of interest rate cuts by the Federal Reserve in 2024. In fact, shares of the fund are up 11.69% since the start of October. This is the sort of performance that we might expect from common equities, not from fixed-income securities such as the ones that are held by this fund. However, the fund’s portfolio has not performed as well as its share price. The net asset value is only up 8.59% over the same period:

{kind=link}

This could be a sign that the market has been somewhat too exuberant with respect to this fund, however over the trailing one-year period, the fund’s share price has substantially underperformed the fund’s portfolio, so this is really just a correction for that problem. As we will discuss later in this article, the recent price appreciation has not made the fund’s shares overpriced based on the actual portfolio. The shares are still cheap compared to the fund’s underlying assets.

However, there is evidence that most of the fund’s assets are overvalued right now. As mentioned earlier in this article, the market has been bidding up the price of fixed-rate preferred stock and bonds in anticipation of a series of interest rate cuts by the Federal Reserve in 2024. The federal funds futures market currently expects that the effective federal funds rate will decline by 1.384 percentage points by the end of December 2024:

{kind=link}

This would require five or six 25-basis point cuts to the federal funds rate over the next eleven months. The Federal Open Market Committee only meets eight times in 2024, and the market is not expecting any change to the federal funds rate in January. That leaves only seven meetings, and the central bank will have to cut at nearly all of them in order to actually deliver on this expectation. There has only been one time in history (in the 1980s) when the Federal Reserve has embarked on a monetary loosening regime to that degree in the absence of an incredibly severe recession. If recent job reports are any indication, the economy is not experiencing a severe downturn. Indeed, most official economic releases from the Federal Government suggest that the economy has strengthened over the past two months.

The most recent core consumer price index also shows a 3.99% year-over-year increase:

{kind=link}

The consumer price index excluding food and energy went from 300.261 to 312.251 over the one-year period. That is a 3.99% annual increase over the period, which is double the Federal Reserve’s target inflation rate. Thus, inflation continues to come in very hot, and when we consider the strength of recent job reports, an interest rate cut in March cannot possibly be justified. That casts some cold water on the prices that the market has currently assigned to the securities in this fund’s portfolio.

If the Federal Reserve does fail to reduce interest rates to the market’s current expectations, then we will almost certainly see the shares of this fund decline sharply. As such, it might make sense for investors to take some of their recent gains off of the table as a risk-reduction strategy. After all, taking some of your profits will reduce the amount that you could potentially lose in a market correction should the above thesis prove to be correct.

Leverage

As is the case with most closed-end funds, the Flaherty & Crumrine Total Return Fund employs leverage as a method of boosting the effective return of its portfolio. I explained how this works in my previous article on this fund:

Basically, the fund borrows money and then uses that borrowed money to purchase preferred stock, debt securities, and other income-producing assets. As long as the purchased securities have a higher yield than the interest rate that the fund has to pay on the borrowed money, the strategy works pretty well to boost the effective yield of the portfolio. As this fund is capable of borrowing money at institutional rates, which are considerably lower than retail rates, that will ordinarily be the case. However, it is important to note that leverage is less effective at boosting yields today with rates at 6% than it was two years ago when rates were 0%. This is because the difference between the yield that the fund can receive and the rate at which it can borrow is much narrower than it once was.

Unfortunately, the use of debt in this fashion is a double-edged sword. This is because leverage boosts both gains and losses. As such, we want to ensure that the fund is not employing too much leverage because that would expose us to an excessive amount of risk. I do not like to see a fund’s leverage exceed a third as a percentage of its assets for this reason.

As of the time of writing, the Flaherty & Crumrine Total Return Fund has leveraged assets comprising 39.91% of its portfolio. This is quite a bit less than the 41.28% leverage that the fund had the last time that we discussed it, which makes a certain amount of sense. After all, the fund’s net asset value has increased since our last discussion, so its leverage now represents a lower percentage of a larger portfolio.

Despite the reduction in leverage over the past three months though, the fund is still using an uncomfortably high level of leverage. After all, its leverage is still quite a bit higher than many of the other preferred stock closed-end funds that currently trade in the market. That actually could be one of the reasons for the fund’s distribution cuts over the past two months. After all, leverage amplified the losses that the fund took as rising interest rates reduced the value of the assets in its portfolio and because this fund is more heavily leveraged than its peers, it took higher losses as a percentage of the portfolio.

This is exactly the same problem that the energy infrastructure funds suffered back in 2020 when the pandemic collapsed the oil and gas industry. Most of those funds have never been able to regain their previous net asset values or distributions, and this one might have the same problem even once interest rates decline, as they eventually will.

Distribution Analysis

As mentioned earlier in this article, the Flaherty & Crumrine Total Return Fund has the primary objective of providing its investors with a very high level of current income. In order to achieve this objective, the fund invests in a portfolio that primarily consists of preferred stocks and bonds, both of which deliver a significant portion of their overall investment returns in the form of direct payments to their owners. In this case, it would be the fund that receives these payments, and the yields of these securities should result in this fund receiving a higher level of income from its portfolio than it would if it had the same amount of money invested in common equities.

This fund takes things a step further, though, as it borrows money to purchase more preferred stock and bonds than it could control solely by using its equity capital. That should give the fund’s portfolio a higher effective yield in most cases because it will be collecting payments from more securities. The fund pools the payments that it receives from all of the securities in its portfolio and combines them with any profits that it manages to generate from trading the assets in its portfolio, although it does not engage in too much of this given the very low turnover. The fund then pays all of this money out to its shareholders, net of its expenses. As preferred stocks and bonds tend to have reasonably high yields in the current environment, we might expect that this business model will result in the fund’s shares having a very high current yield.

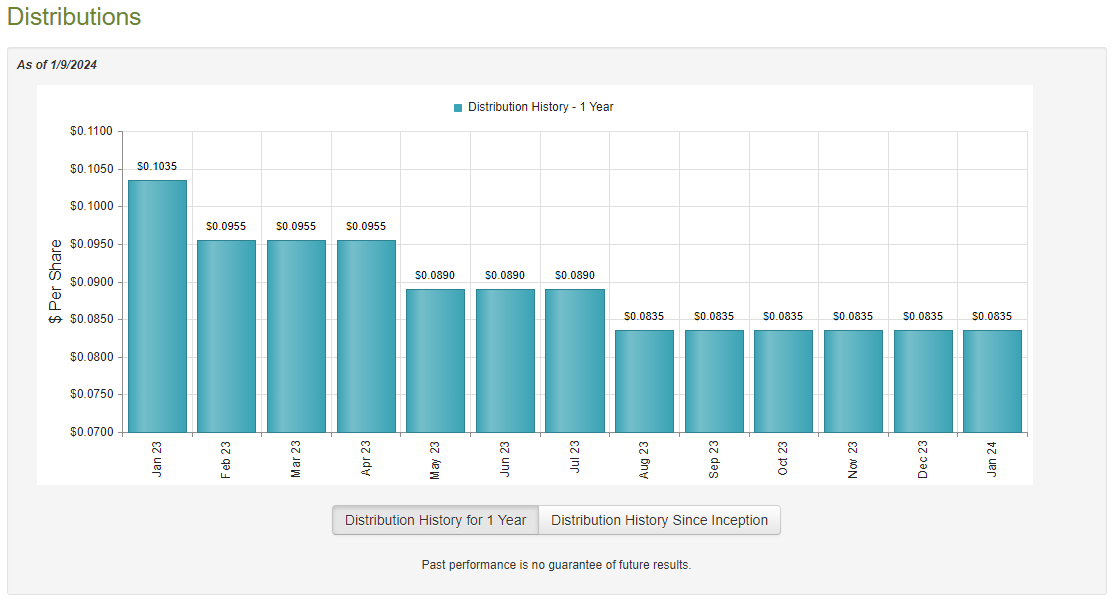

That is indeed the case, as the Flaherty & Crumrine Total Return Fund pays a monthly distribution of $0.0835 per share ($1.002 per share annually), which gives it a 6.81% yield at the current price. That is quite a bit lower than many of the other preferred stock and fixed-income funds on the market, which is very disappointing. The fund has also not been especially consistent with respect to its distribution over the years. As we can see here, it has both increased and decreased the payout numerous times:

{kind=link}

The fact that the fund’s distribution has been variable over the years could be somewhat of a turn-off for those investors who are seeking to receive a safe and consistent income from the assets that they have accumulated over their lifetimes. The fact that the fund has reduced its distribution three times over the past twelve months will only add to this aversion:

{kind=link}

It is not exactly surprising that the fund would need to repeatedly cut its distribution in the current market environment. After all, the steep rise in interest rates over the past two years resulted in the fund suffering from significant losses as the value of the assets in its fixed-income portfolio declined. This fund took greater losses than some of its peers due to its relatively high level of leverage. The fact that the fund’s repeated distribution cuts is easily explainable is unlikely to be comforting to any new investors, however.

As I have pointed out in numerous previous articles, the fund’s distribution history is not necessarily the most important thing for new investors. This is because anyone who purchases the fund today will receive the current distribution at the current yield and will not be affected by any events that occurred in the fund’s past. The important thing for a new investor is the fund’s ability to sustain its current distribution at the current level. Let us investigate this.

Unfortunately, we do not have an especially recent document to consult for the purpose of our analysis. As of the time of writing, the most recent financial report for the Flaherty & Crumrine Total Return Fund corresponds to the six-month period that ended on May 31, 2023. As such, it will not provide insight into the fund’s performance over the past seven months. That is very disappointing because there are quite a few things that have transpired over the intervening period that could have an impact on the fund’s financial performance. In particular, the market downturn over the summer that was driven by investor pessimism about the potential for near-term reductions in interest rates almost certainly caused the fund to take some losses.

That could have been the reason for the distribution cut in August. The market generally returned to its usual euphoric mood in mid-October though and since that time it has been driving up the price of preferred stock and bonds, which undoubtedly has benefited this fund and provided it with the opportunity to earn some profits. The most recent financial report will not provide any information about these two disparate events, so unfortunately, we will have to wait another month or so for the fund to release its annual report to have any better information about how well it performed. For now, though, we will proceed with the information that we have available to us.

During the six-month period, the Flaherty & Crumrine Total Return Fund received $3,606,204 in dividends along with $6,385,440 in interest from the assets in its portfolio. When we combine this with a small amount of income that came from other sources, we see that the fund had a total investment income of $10,019,210 over the six-month period. The fund paid its expenses out of this amount, which left it with $5,530,248 available to the shareholders.

As might be expected, that was not enough money to cover the distributions that were made over the period, but the fund did manage to get pretty close. Over the six-month period, the fund paid $6,091,098 to its shareholders in distributions. We would ordinarily prefer a fixed-income fund to fully cover its distributions out of net investment income and this one obviously failed to accomplish that goal. This is something that might be concerning to risk-averse investors.

However, there are other methods through which the fund can obtain the money that it needs to cover its distributions. For example, it might be able to earn some capital gains by exploiting price fluctuations that accompany changes in interest rates. Realized capital gains are not investment income for tax or accounting purposes, but they obviously do represent money coming into the fund that can be paid out to the investors.

Unfortunately, the fund failed miserably at achieving necessary profits via alternative methods. For the six-month period, it reported net realized losses of $4,968,271 and had another $8,952,899 net unrealized losses. Overall, the fund’s net assets declined by $14,482,020 after accounting for all inflows and outflows during the period. This comes on the heels of a $50,583,517 decline in net assets over the preceding full-year period. This certainly explains why the fund’s management implemented so many distribution cuts over the past two years, as this fund has been consistently bleeding assets. That is not something that we like to see as investors.

Fortunately, there are some signs that the fund has managed to correct this problem since the most recent reporting period ended. This chart shows the fund’s net asset value since June 1, 2023:

{kind=link}

As we can clearly see, the Flaherty & Crumrine Total Return Fund has managed to increase its net asset value by 7.30% since the closing date of its most recent financial report. This strongly suggests that the fund has managed to cover all of the distributions that it paid out since the closing date of its most recent financial report with a significant amount of money left over. This is a good sign if the fund manages to hold onto the recent gains that it has experienced from its portfolio. However, there is no guarantee that this will be the case.

Valuation

As of January 9, 2024 (the most recent date for which data is available as of the time of writing), the Flaherty & Crumrine Total Return Fund has a net asset value of $17.06 per share but the shares only trade for $14.83 each. This gives the fund’s shares a whopping 13.07% discount on net asset value at the current price. This is not as attractive as the 14.36% discount that the fund’s shares have had on average over the past month, but a double-digit discount generally represents a decent price to enter into any fund.

However, as mentioned throughout this article, it probably makes more sense to sell some of your position and realize some gains considering the risk. The shares are currently a bit more expensive than they have been averaging, so right now could be a reasonable time to conduct the sale.

Conclusion

In conclusion, the Flaherty & Crumrine Total Return Fund has earned a great deal of ire from income-focused investors over the past few years due to its fairly frequent and large distribution cuts. These cuts continued into this year, despite the federal funds rate likely peaking in July. The fund has delivered fairly large gains over the past two months though, but there is a great deal of risk that the fund may not be able to sustain these gains. After all, the recent gains are dependent on recession-level interest rate cuts and current economic data does not support this outcome. As such, it may be prudent for investors to take some of their gains off the table in order to protect what they already have and reduce their risks going forward.

For further details see:

FLC: This Fund May Not Be Able To Sustain Its Recent Gains (Rating Downgrade)