FELE - Flowserve Corporation: Not A Great Purchase Right Now

Summary

- Flowserve Corporation has had a great run in recent months, even as some of its fundamental data has been disappointing.

- I clearly underestimated the company previously, but this doesn't mean it still offers a good opportunity for investors.

- The picture could change, but for now it looks like there are better prospects that can be considered.

No investment ideology is perfect. This is true even of value investing, which has got to be the most successful investment approach developed so far. But even value investing can result in undesirable outcomes. One type of undesirable outcome is underestimating just how much upside a company has from a share price perspective. When this is misjudged, you don't lose money on the company in question unless you were short the stock. But you do miss out on some attractive upside. One really good example of this can be seen by looking at Flowserve ( FLS ), an enterprise that operates as a manufacturer and aftermarket service provider of comprehensive flow control systems. Examples include pumps, valves, seals, automation and aftermarket services, and more. Previously, I rated the company a ‘hold’ to reflect my view that shares should not generate upside or downside that would materially deviate from the broader market for the foreseeable future. But with the idea in mind that many of the issues the company faced should be temporary in nature and with sales rising in the latest quarter for which data is available, the stock has moved up materially. In retrospect, I clearly underestimated the company. But now, given how shares are priced, I do think it is worthy of the ‘hold’ rating I assigned it previously.

Going against the flow

Back in late September of last year, I revisited Flowserve after the company had experienced a great deal of weakness on both its top and bottom lines. At that time, the deterioration in its fundamental performance made shares look pricey. It is true that the company had some positive things going for it, such as bookings and backlog data that could be considered bullish. But because of how shares were priced and the direction the fundamentals were moving, I ended up keeping it at the ‘hold’ rating I assigned it previously. Since then, things have not gone exactly as planned. While the S&P 500 is up 10.6%, shares of Flowserve have seen upside of 35.7%. It is worth noting that, while this particular call has been off by a great margin, the stock is down 5.4% from the time I initially rated it a ‘hold’ back in April of last year. By comparison, the S&P 500 over that time is down 10.1%.

{kind=link}

Author - SEC EDGAR Data

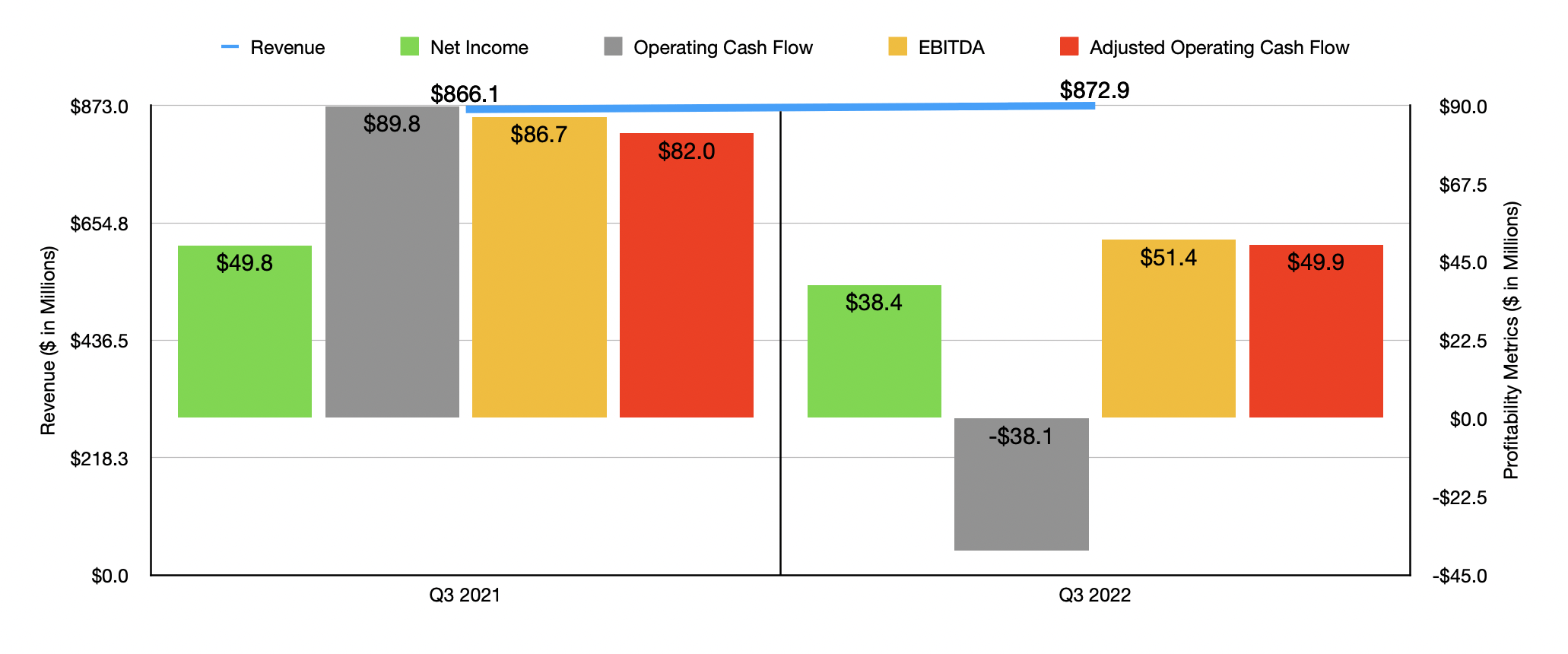

A lot of the recent enthusiasm surrounding Flowserve seems to stem from its most recent financial performance. During the third quarter of its 2022 fiscal year, for instance, sales came in at $872.9 million. That's only marginally higher than the $866.1 million reported one year earlier. This increase of only 0.8% may not look impressive. But it's important to note that sales would have been a great deal higher in the third quarter had it not been for a $55 million hit that the company took from foreign currency translation. Adjusting for this, sales would have increased by roughly 7.1% according to management, the increased sales were driven by aftermarket activities for the most part and came even as the company experienced operational interruptions related to the implementation of its enterprise resource planning system, or ERP. But that series of interruptions was estimated to have cost the company $30 million in sales for the quarter, meaning that revenue, adjusting for this also, would have been up 10.6% year over year.

Even though revenue increased during this time, the company did see profits struggle. The firm went from generating a net profit of $49.8 million in the third quarter of 2021 to generating a profit of only $38.4 million during the third quarter of 2022. Operating cash flow plunged from $89.8 million to negative $38.1 million. Though if we adjust for changes in working capital, it would have gone from $82 million to $49.9 million, while EBITDA went from $86.7 million to $51.4 million. In addition to suffering from the decline in sales, the company also reported a drop in its gross profit margin. Year-over-year the margin declined from 23.6% to 27.4%, driven by a number of factors including the absorption of $5.1 million of fixed manufacturing costs primarily from the aforementioned operational interruptions the company experience. Though this kind of margin decline may not seem like much, when applied to the sales the company did experience in the third quarter, the impact translated to $16.6 million in missed profitability on a pre-tax basis. Selling, general, and administrative costs also happened to rise year over year, climbing from 23.2% of sales to 25.3% of sales. Increased asbestos-related costs, operating lease expense changes, and other factors, all played a role in this. This stripped another $18.3 million in pre-tax profits from the company.

{kind=link}

Author - SEC EDGAR Data

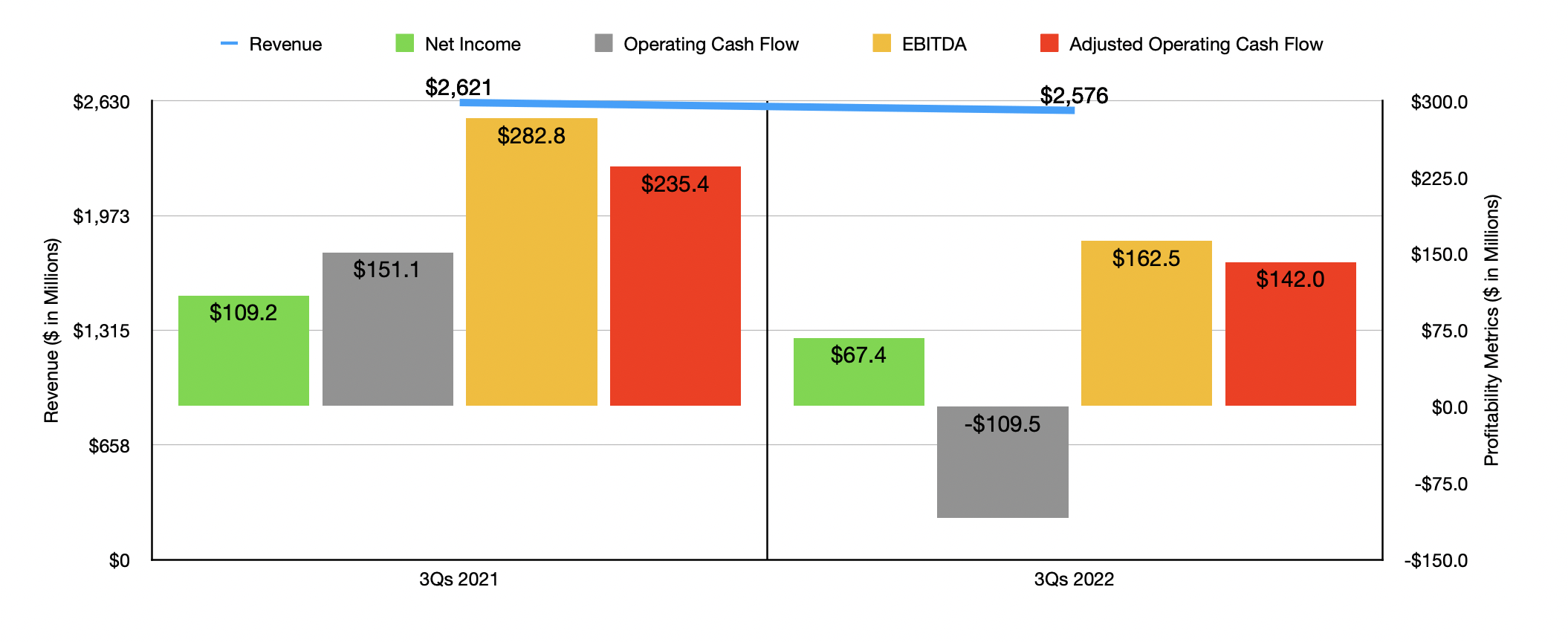

With the exception of sales, the third quarter of 2022 looked very similar to the first nine months of the year as a whole. Sales dropped from $2.62 billion to $2.58 billion. But again, the company suffered tremendously here from not only the aforementioned ERP implementation, but also from $116 million associated with foreign currency translation. Profits followed sales lower. Net income plunged from $109.2 million to $67.4 million. The company saw its operating cash flow decline from $151.1 million to negative $109.5 million. But if we adjust for changes in working capital, the picture was not quite as bad, with the metric falling from $235.4 million to $142 million. And finally, EBITDA for the company shrank from $282.8 million to $162.5 million.

When it comes to the final quarter of 2022, management did say that revenue should be up between 8% and 10% year over year. They also said that adjusted earnings per share should be at least $0.40. However, it's important to note that adjusted earnings tend to be very similar to GAAP earnings for the company over time. By my own estimate, net income for the company for 2022 will likely have been $77.7 million. The adjusted operating cash flow for the company should be around $205.9 million, while the EBITDA for the firm should total about $228.9 million.

{kind=link}

Author - SEC EDGAR Data

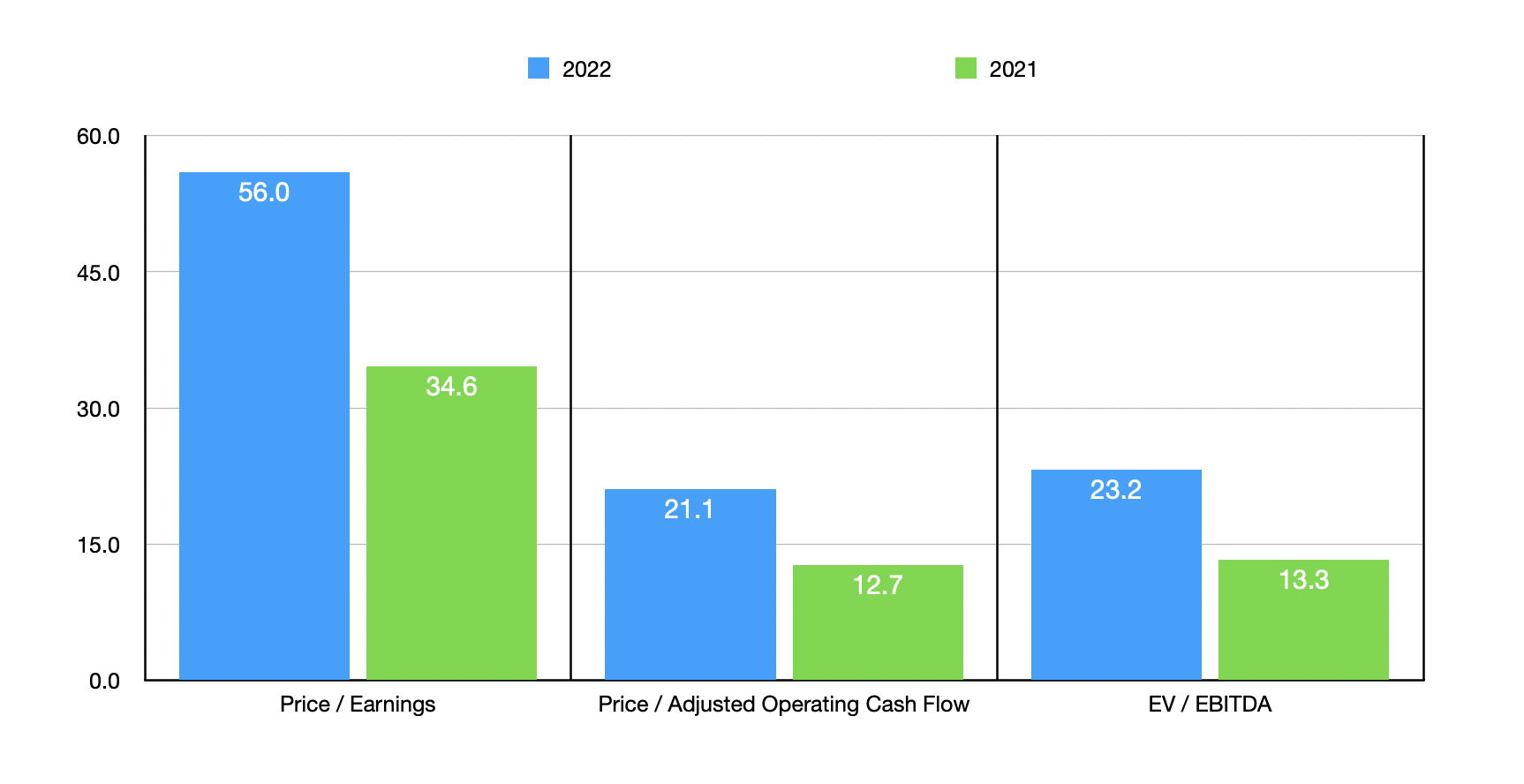

Based on these numbers, the company is trading at a price-to-earnings multiple of 56. The price to adjusted operating cash flow multiple should be considerably lower at 21.1, while the EV to EBITDA multiple should come in at around 23.2. By comparison, if we assume that the company should eventually revert back to the levels of profitability experienced in 2021, these multiples would be 34.6, 12.7, and 13.3, respectively. I also, as part of my analysis, compared the company to five similar firms. On a price-to-earnings basis, these companies ranged from a low of 5.8 to a high of 27.9. When it comes to the EV to EBITDA approach, the range was from 3.6 to 18.5. In both cases, Flowserve was the most expensive of the group. And finally, when it comes to the price to operating cash flow approach, the range should be from 5.7 to 95.7. In this scenario, three of the five firms were cheaper than our target.

| Company |

| Price / Earnings |

| Price / Operating Cash Flow |

| EV / EBITDA |

| Flowserve |

| 56.0 |

| 21.1 |

| 23.2 |

| Mueller Industries ( MLI ) |

| 5.8 |

| 5.7 |

| 3.6 |

| Gates Industrial Corp. ( GTES ) |

| 19.0 |

| 20.0 |

| 10.8 |

| Franklin Electric Co. ( FELE ) |

| 22.0 |

| 95.7 |

| 14.3 |

| John Bean Technologies ( JBT ) |

| 27.9 |

| 25.5 |

| 18.5 |

| Hillenbrand ( HI ) |

| 15.8 |

| 17.3 |

| 8.4 |

Takeaway

Looking back to when I wrote my most recent article on Flowserve, I have come to believe that I was overly bearish about the firm and its prospects. Shares were not exactly in deep value territory when I wrote about it then. But they were cheap enough to warrant some upside potential. Fast forward to today, and mix in the uncertainty of the broader market, and I do think that the firm warrants a ‘hold’ rating. This is true even though backlog for the company of $2.6 billion is 32.1% higher than it was the same time last year. However, if we do start to see some improvement in its bottom line, that backlog, combined with said improved profitability, could eventually change my mind.

For further details see:

Flowserve Corporation: Not A Great Purchase Right Now