FOCS - Focus Financial Partners: Likely To Be Acquired By CD&R

Summary

- Non-binding merger arb opportunity offering a potentially high IRR.

- Private equity giant Clayton Dubilier & Rice, LLC has made a non-binding acquisition proposal to acquire Focus Financial Partners Inc. at $53/share.

- CD&R has entered into an exclusive due diligence.

- The transaction seems highly likely to proceed to definitive stage and close successfully after that.

This is a non-binding stage merger arb play currently offering a high-probability 6% return. The target’s management seems willing to sell the company, and the transaction is thus highly likely to proceed to the definitive stage. The buyer is unlikely to walk away given its reputation and acquisition rationale. Added confidence comes from the fact that a large shareholder is willing to roll-over its stake. The IRR is likely to be substantial if the transaction closes in short order - potentially within 4-6 months.

Late last year, private equity ("PE") giant Clayton Dubilier & Rice, LLC (CD&R) made a non-binding acquisition bid to acquire the registered investment advisor ((RIA)) roll-up Focus Financial Partners Inc. (NASDAQ: FOCS ). Subsequently, this month both parties entered into an exclusivity agreement for a limited time period. Proposed consideration is $53/share - a 6% spread to the current share price. FOCS’ largest shareholder Stone Point Capital (owns 21%) has hinted that all of its-affiliated entities might roll-over their stakes, including one of the funds managed by Stone Point ( Trident FFP , 11% stake). CD&R has noted that its offer is “best and final,” suggesting any price bump is unlikely. Nonetheless, FOCS’ management is seemingly willing to sell the company. The buyout interest follows the strategic review launched back in Nov’22 to evaluate a non-binding acquisition offer from CD&R. The review was also intended to explore potential alternative transactions and included meetings with other prospective bidders. Worth noting that during the strategic review FOCS’ special committee informed CD&R that it would enter into an exclusivity agreement if the PE firm submitted an offer at $53/share.

Aside from due diligence, the transaction would require approval from the majority of FOCS’ disinterested shareholders. In my view, these equity holders are likely to support the potential transaction. The bid comes at a 36% premium to FOCS’ 60-day WVAP. Premium to December 28 (the date when the special committee authorized its advisors to contact other potential bidders) is 48%. Moreover, the transaction would value the target fairly. CD&R’s bid implies 11.1x TTM adjusted EBITDA valuation and 10.1x on estimated 2023 EBITDA. While this is admittedly a tad below the historical multiples of 12.1x-14.8x FOCS fetched in 2018-2021, the offer seems to value FOCS decently on a relative basis. While there are no directly comparable peers, another Canada- and US-focused RIA aggregator CI Financial ( CIX:CA ) trades at 6.3x/6.6x TTM/2023 adjusted EBITDA multiples. Other RIAs LPL Financial Holdings ( LPLA ) and Avantax ( AVTA ) trade at 9.1x and 8.6x on a forward-EBITDA (2023E) basis. FOCS’ shareholder base includes 5 passive institutional investors, including Vanguard, Wasatch Advisors, Capital World Investors, Blackrock and JP Morgan (combined 35% stake). Given the deal’s large premium to unaffected share price and seemingly fair valuation, these equity holders might be likely to support the transaction.

The chances of CD&R going ahead with a definitive proposal seem quite high. While the acquisition of FOCS would be the PE firm’s first venture into the wealth management space, CD&R is a highly reputable buyer. The PE firm is among the largest globally, with over $50bn in assets under management ("AUM"). The sample size of CD&R’s recent history with non-binding merger proposals is rather limited, however, the PE firm has proceeded rather swiftly to definitive agreements in both recent non-binding merger situations, including CNR (non-binding proposal in Feb’22 and definitive agreement in Mar’22) and CVET (both non-binding proposal and definitive agreement in May’22).

Another noteworthy aspect here is participation of Stone Point. Stone Point is a private equity firm (over $35bn in raised capital) with a number of wealth management holdings. Stone Point has been invested in FOCS since 2017 when it acquired a majority stake in tandem with KKR (before the IPO in 2018). The equity holder currently controls 2/8 board seats. Agreement to roll its stake from the largest shareholder - which is highly familiar with the business - is a positive here.

Industry Background

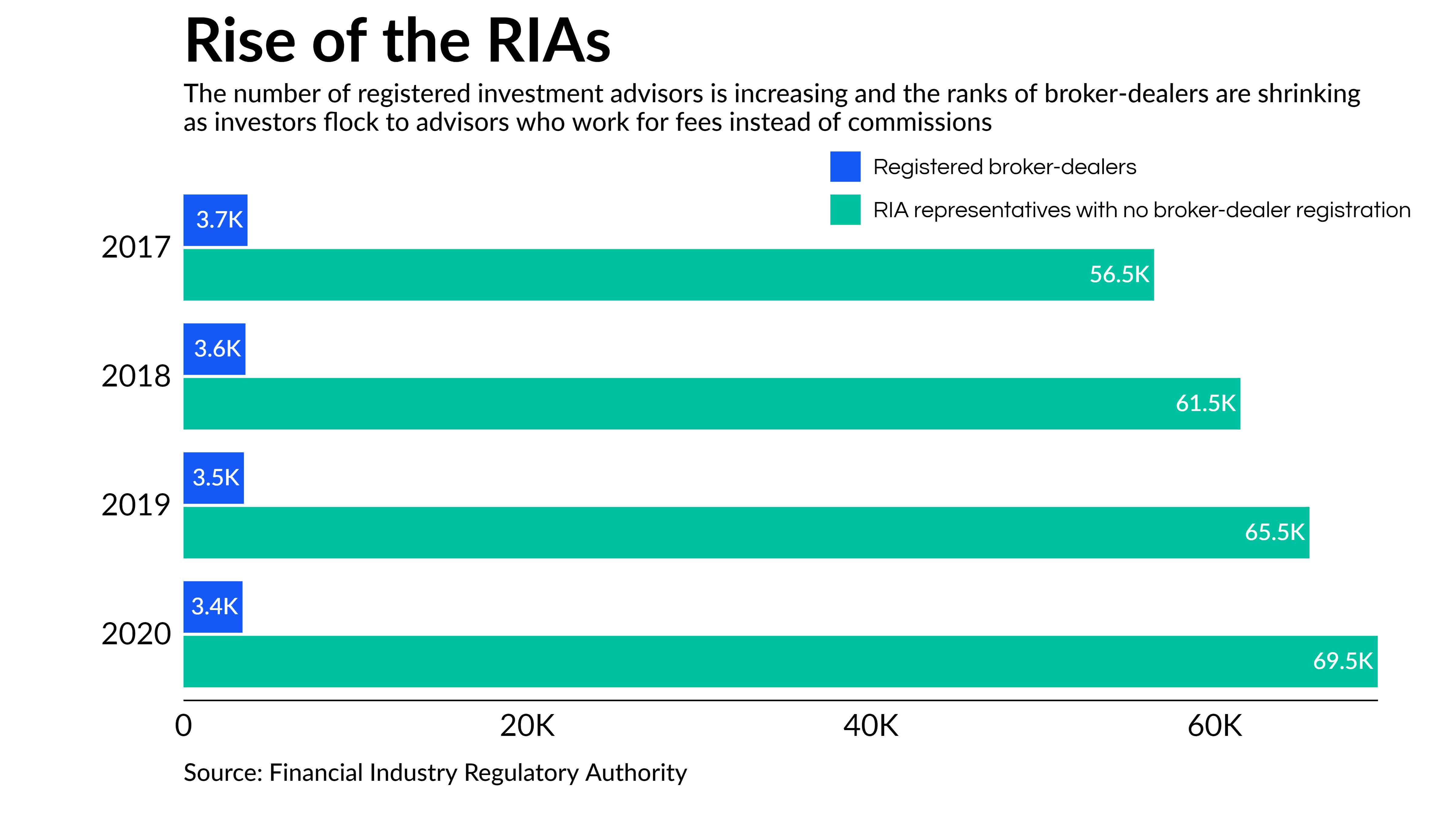

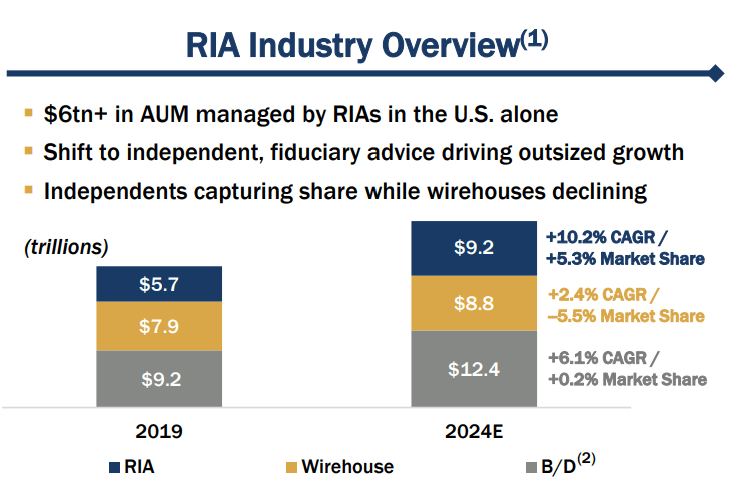

The acquisition seems to make sense for CD&R given the growth of RIAs in the financial advisory space. PE giant’s attempt to scoop up Focus comes amid investors’ gradual shift from broker-dealers and wirehouses (full-service broker-dealers) to RIAs, such as Focus. This trend has been driven by the presence of RIAs’ fiduciary duties, meaning that RIAs must operate only in the client’s best interest. This contrasts with potential conflicts of interest for broker-dealers/wirehouses as they pocket product-based commissions instead of fees received by registered investment advisors. Meanwhile, on the owner side, RIAs allow for greater autonomy, easier scaling of the business and better succession planning. Not surprisingly, market share of RIAs in the US has continued to rise and is expected to grow by 5.3% from 2019 to 2024 compared to -5.5% and 0.2% for wirehouses and broker-dealers. Deteriorating macroeconomic environment and subsequent economic recovery might further boost the market share captured by RIAs given that they have historically tended to materially outperform wirehouses and broker-dealers in post-crisis periods (per Cerulli, as noted by FOCS’ management).

American Banker, Financial Industry Regulatory Authority Focus Financial Partners Investor Presentation, September 2022

{kind=link}

{kind=link}

Increasing number of RIA’s, driven by secular tailwinds, has led to record-high M&A activity in the space (see chart below). The interesting thing here is that the industry has seen high involvement of private equity firms interested in getting a piece of the RIA market. According to Echelon , private equity firms directly participated/backed 70% of wealth management industry transactions in 2022. On top of RIAs’ high net profit margins (generally at or above 25%), PE firm have been attracted by RIA’s higher client retention rate as compared to PE firms, also allowing for recurring revenue streams. Despite the macroeconomic turmoil and rising interest rates, PE buyers have been in a good position to capitalize on RIA consolidation opportunities. The point I am trying to make here is that, given the secular tailwinds for RIAs growth and consolidation, CD&R’s interest in a large RIA roll-up is not surprising.

ECHELON Partners 2022 RIA M&A Deal Report Executive Brief

Focus Financial Partners

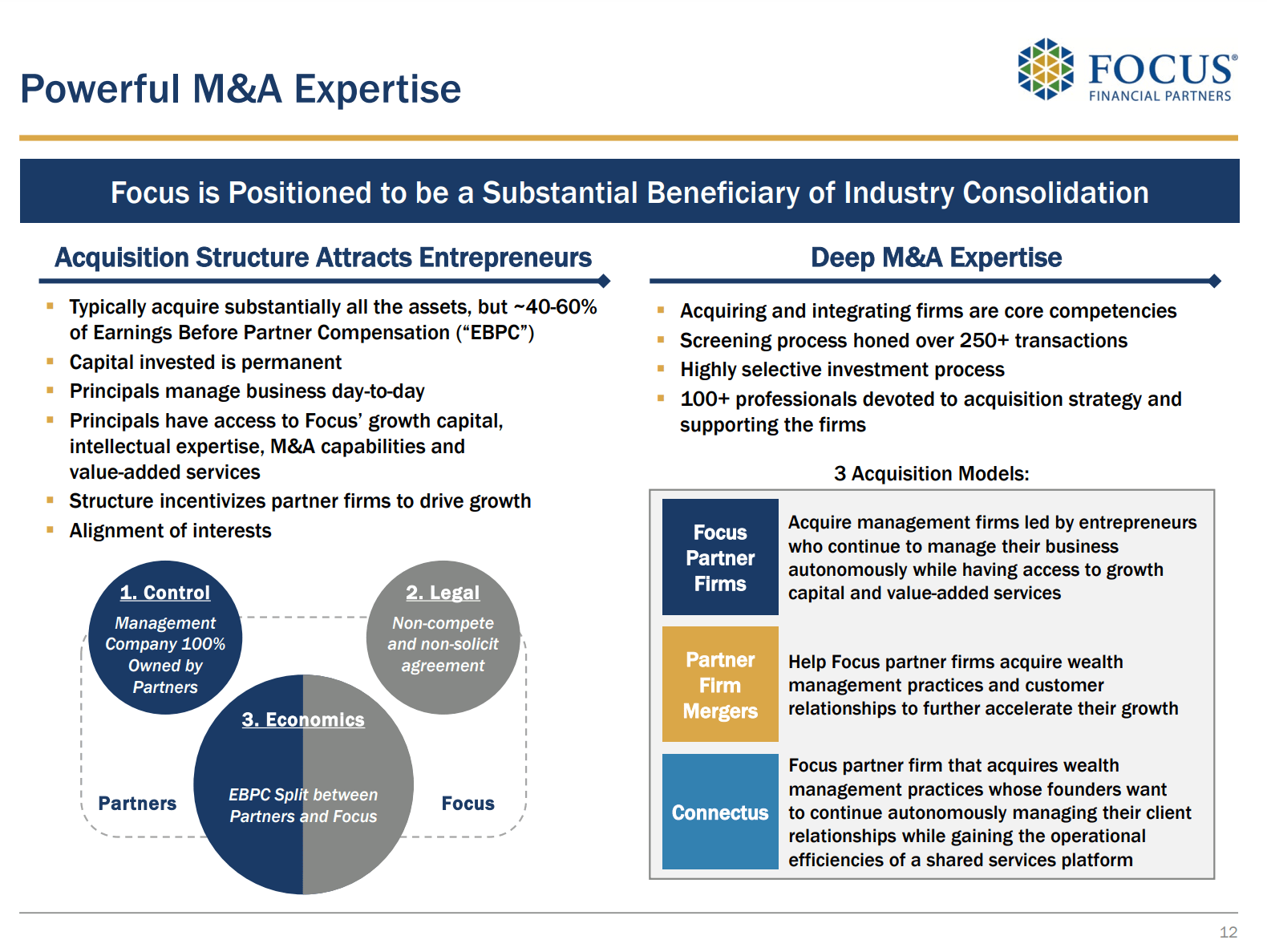

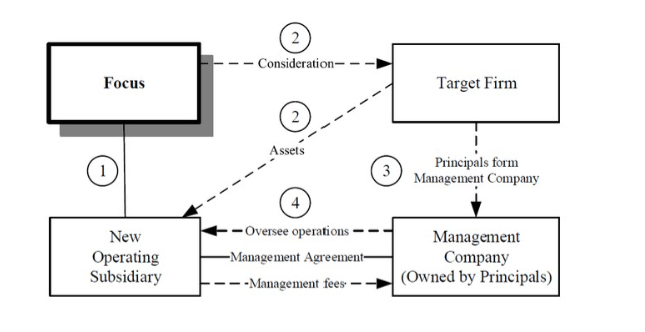

Focus Financial Partners is a partnership of independent wealth management firms. The company has acquired over 80 partner firms. FOCS’ partner firms provide a number of services to high and ultra-high net worth individuals, including investment advice, financial and tax planning, consulting, tax return preparation and other. Partner firm acquisitions are structured in a way where FOCS acquires the partner’s assets and becomes entitled to a portion of the partner’s earnings (generally 40-60% of earnings before partner compensation or EBPC) for a certain level of base target earnings. The remaining portion of EBPC is paid as a management fee to the partners’ principals who in turn own/run the newly established management subsidiary (see charts below). 95% of FOCS’ revenues are fee-based/recurring.

Focus Financial Partners Investor Presentation, September 2022

{kind=link}

{kind=link}

FOCS has a number of competitive advantages which allow it to attract partner firms. Firstly, FOCS provides a range of value-added services to partners, such as marketing, business development, legal and compliance support, among others. Another aspect is that acquired partner firms retain nearly full autonomy in their operations. Other benefits to partner firms include easier access to bank capital and FOCS’ negotiating power with third-party vendors.

The company’s strategy has revolved around pursuing acquisitions. The company has expanded its revenues from $0.9bn in 2018 to $2.1bn in 2022. The management has been bullish about further growth through M&A given secular tailwinds, including the need for both succession planning (driven by the aging of founders) and scale. Expansion is also expected to come from increasing international presence. Currently, 94% of the company’s revenues come from the U.S. The management has set out a revenue target of $5bn for 2025.

Risks

The downside to pre-announcement levels is 8%. However, the downside might potentially be larger if there is no definitive agreement given that the stock has gone up 44% since the formation of the special committee (on November 1) and 40% since the special committee authorized its financial advisors to contact other potential bidders (on December 28). There are a couple of risks worth noting:

- One of the uncertainties here is related to FOCS’ potential difficulties in continuing its growth through acquisitions. RIA roll-ups, such as FOCS, have seen increasing competition coming from private equity firms as well as other RIAs starting to pursue the roll-up strategy. This has materially driven up acquisition multiples from 6x-9x EBITDA historically to as much as 20x. FOCS’ CEO explicitly called this out during Q2’22 earnings call . Another aspect here is that FOCS’ acquisition strategy has relied heavily on debt financing (equity issuance has been limited). As a result of expensive acquisitions, FOCS’ net leverage ratio (net debt divided by EBITDA) has risen from 3.5x in Q3’21 to 4.2x as of Q4’22 - close to the target ratio upper range of 4.5x. Current debt burden, coupled with toughening financing environment and elevated RIA valuation multiples, might potentially hinder the company’s ability to pursue further acquisitions. Having said that, a positive here is that FOCS’ management has noted that the valuation multiples have already started to normalize.

- FOCS’ management has a very low ownership stake (0.1% of voting power) and is compensated rather generously - for reference, the CEO received a total compensation of $12m in 2021.

Conclusion

Focus Financial Partners Inc. currently presents an interesting high-IRR merger arb opportunity. The acquisition would allow the potential buyer, which is highly credible, to acquire one of the leading RIA roll-ups. Importantly, Focus Financial Partners Inc.'s largest equity holder is willing to roll its stake. Meanwhile, the target’s management has been exploring an acquisition for a while, indicating the leadership’s willingness to sell the company. Finally, approval from Focus Financial Partners Inc.'s majority of disinterested shareholders seems likely given a decent premium and fair valuation.

For further details see:

Focus Financial Partners: Likely To Be Acquired By CD&R