STEW - FOF: An Interesting Fund Of Funds Approach

Summary

- FOF takes an approach of investing in other funds, primarily closed-end funds but also exchange-traded funds, too.

- This makes it a one-stop shop for instant and broad diversification across a diverse pool of different asset classes, sectors and industries.

- Unfortunately, at this time, it appears that the fund is continuing to carry an elevated valuation, trading at a slight premium to its NAV.

Written by Nick Ackerman, co-produced by Stanford Chemist. A version of this article was originally published to members of the CEF/ETF Income Laboratory on January 16th, 2023.

Cohen & Steers Closed-End Opportunity Fund ( FOF ) can be an attractive closed-end fund to consider. By investing in FOF, one is gaining immediate and vast diversification. That includes a healthy portion of equity and fixed-income positions, even a small amount of municipal bonds and commodities. The underlying funds carry exposure to various sectors and industries, as well as different types of debt instruments.

Unfortunately, it doesn't look like a buy today due to trading at a slight premium to its NAV. Although it was trading at an even higher premium, that came down quite swiftly recently. This will be a fund to continue to watch closely to see if we can get a discount.

One of the biggest benefits of investing in FOF is gaining exposure to discounts on discounts in the CEF space. A CEF can trade at a discount, so FOF being a CEF itself, can trade wildly between discounts and premiums. So today will be more of an update piece and taking a look at potentially new positions in the fund's top ten holdings. I'd also mention that the latest premium is almost pushing it to where investors could consider selling out of the fund for now.

Since our last coverage , the fund has performed fairly well. Some of this was due to premium expansion, but not all of it.

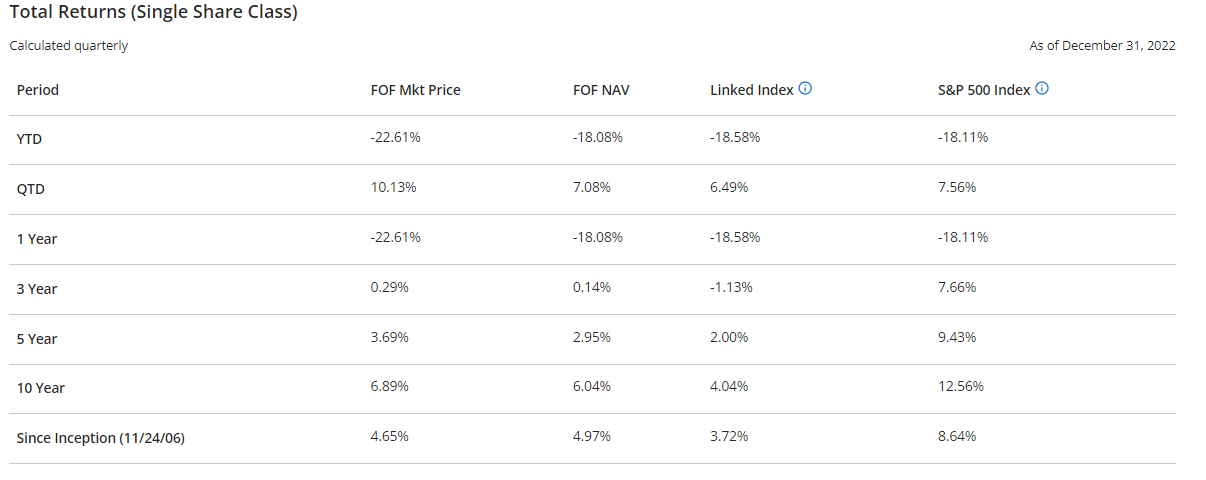

FOF Returns Since Previous Update (Seeking Alpha)

The Basics

- 1-Year Z-score: 0.38

- Premium: 0.80%

- Distribution Yield: 9.19%

- Expense Ratio: 0.95%

- Leverage: N/A

- Managed Assets: $291.21 million

- Structure: Perpetual

FOF has an investment objective of "seeking to achieve total return consisting of high current income and potential capital appreciation." It will invest "in the common stock of closed-end management investment companies that invest significantly in equity or income-producing securities." This broad-based approach sets management up for an endless amount of flexibility. Also interesting is that they don't include ETFs in that description but still hold ETFs in smaller pieces.

At first blush, the fund's expense ratio doesn't seem too high for a CEF. CEFs usually has an expense ratio of 1% or greater. However, that doesn't factor in the underlying expense ratios of the fund either. Therefore, when investing in this fund, you get expenses on expenses. Some of the top holdings have expense ratios of anywhere from 0.03% for the ETFs to 2.64% for the leveraged CEFs. I think that's one of the reasons why it can be even more important to wait for a discount before considering this fund.

The fund is also fairly small, which can mean a lack of liquidity. For smaller investors, it likely isn't an issue, but for larger retail investors, it could be as the doorway to buy and sell can be restricted.

The fund isn't leveraged itself, but the underlying positions are. Some of them are highly leveraged, which comes with all the usual negatives with rising rates. Particularly, that means some of the underlying holdings are paying much higher yields on their borrowings. On the other hand, several of these funds are hedged in various ways. It's one more way that FOF's diversification can help negate some of the negative impacts.

Performance - Premium Reaching Near Peak

As a hybrid fund that is actively invested and can change dynamically to the environment, it can be harder to come up with a benchmark. Most benchmarks are fixed to certain indexes. Therefore, they present their annualized performance against the S&P 500 Index but also have a "Linked Index" that they include.

{kind=link}

Naturally, this linked Index is a better representation; on that basis, results have been fairly promising. The linked index is the S-Network All Taxable ex-Foreign plus Capped Muni CEF Index.

We may also compare FOF to another CEF-focused fund of funds, except in the ETF structure. That would be the Saba Closed-End Funds ETF ( CEFS ), which is actively managed. We also have the Invesco CEF Income Composite ETF ( PCEF ), which is passively managed based on the S-Network Composite Closed-End Fund Index.

On that basis, we see some interesting results. CEFs have been a much better performer on a total NAV return basis. However, it has been much closer in the last ten years on a total share price basis. One of the reasons for this is that FOF has expanded from a discount to a premium which extended its performance to be relatively much higher than on an NAV basis.

YCharts

Thus, more evidence that the fund's current premium could potentially eat into future results. Buying the fund at a discount can be much more competitive than it would be at a premium.

The fund has been flirting with a premium. In fact, recently, the fund was at an all-time high premium for the fund, excluding shortly after the fund launched. It has come down since, but a premium takes away one of the main benefits of investing in FOF.

Overall, CEFs look much more attractive than they had been. They are trading towards the bottom range of their historical discounts. So, investing in CEFS or PCEF could be a valid option while sitting on the sidelines, waiting for FOF to come back to a better valuation. In that way, you aren't paying up for FOF but could also be gaining exposure to these interesting discounted securities at this time.

{kind=link}

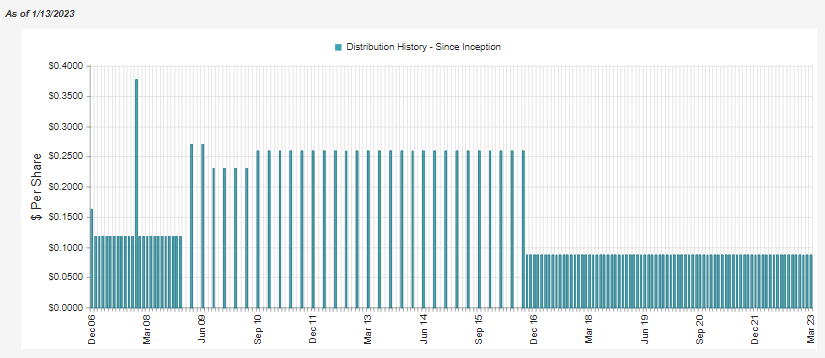

Distribution - Attractive And Steady

Besides the GFC period, FOF has been able to deliver a consistent distribution month after month to shareholders for years. While they went quarterly for several years after the GFC, when they went back to monthly, it was the same amount as the quarterly. So we only see a couple of cuts around 2008/09.

{kind=link}

However, that doesn't tell us if the fund is still earning its distribution. In this case, the 9.19% distribution rate on the share price is quite attractive. Unfortunately, this is where the premiums can also impact CEFs. The fund has actually to earn 9.26% to maintain the same distribution. Due to only a shallow discount at this time, it isn't a dramatic difference. It is even certainly possible for managers to accomplish this, but for equity funds, it becomes harder and harder in a bear market.

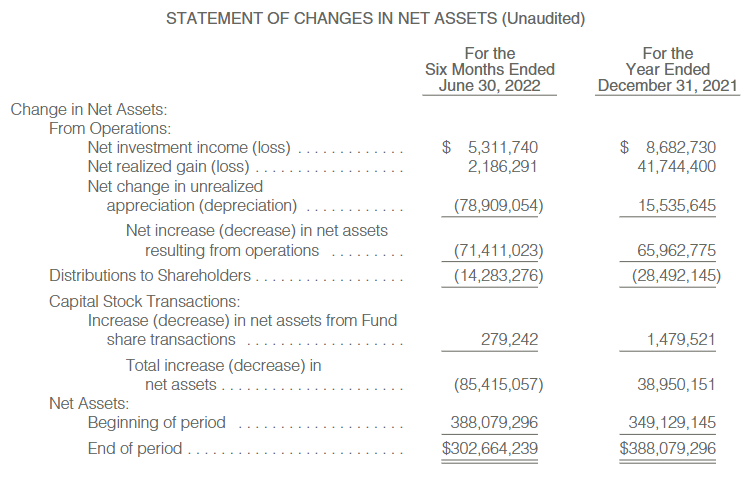

Their last semi-annual report shows that they were able to increase net investment income from the prior fiscal year. Being that it is a six-month period, if we annualize out the $5.312, we would see it come to $10.624 if it carried on through the latter half of the year. That works out to a 22.35% increase, something that's quite positive for the fund when gains become more difficult to find.

{kind=link}

Looking at it another way, it untimely works out to an NII distribution coverage of 37% from 30.5%. Whatever they can do to increase NII seems like a smart move through 2022.

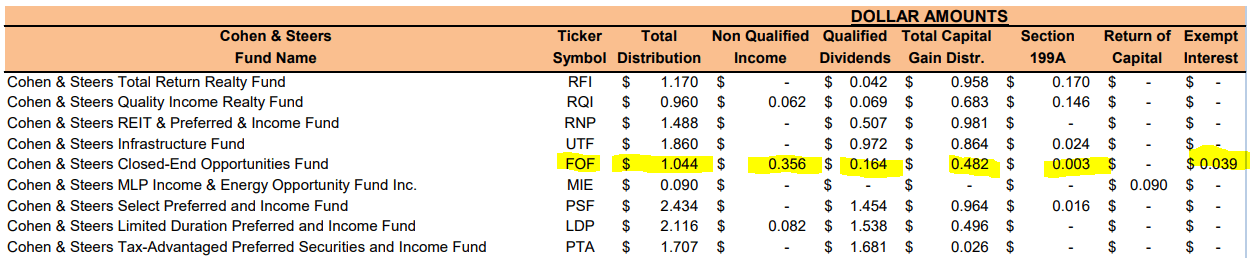

We should be getting the next tax classifications for 2022 before too long. However, we can see that for 2021, there was a mixture of distributions characterized in a plethora of different ways. Par for the course considering the fund's diversified approach.

The majority of it was tax-friendlier qualified dividends and long-term capital gains. However, a sizeable portion was also attributed to non-qualified or ordinary income. That will get taxed at the highest rates, meaning that if you have room in a tax-sheltered account, FOF could be appropriate there. On the other hand, it also shouldn't be completely ignored if you must put it in a taxable account.

FOF Tax Classification 2021 (Cohen & Steers (highlights from author))

{kind=link}

FOF's Portfolio

With a sizeable portion of my portfolio in CEFs, it's always interesting to see what the professionals are investing in the CEF space.

Overall, they are tilted heaviest in equity funds by a fairly meaningful degree. Since our last update, this was bumped up slightly from the 51% listed.

FOF Sector Allocation (Cohen & Steers)

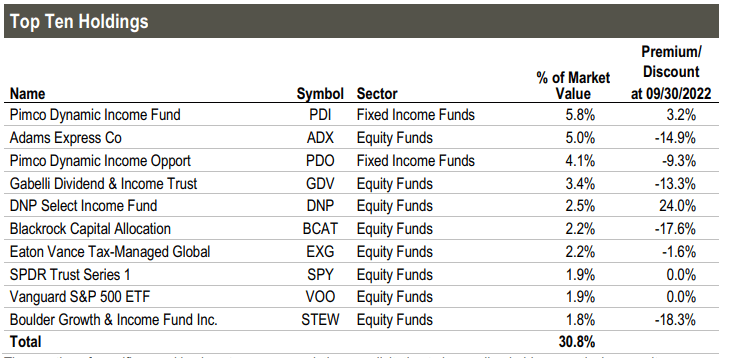

Turnover in this portfolio can be fairly aggressive, with the latest semi-annual report showing 25%. That being said, their top ten holdings haven't changed drastically from our last update, mirroring what we see above in the overall sector diversification of the fund.

{kind=link}

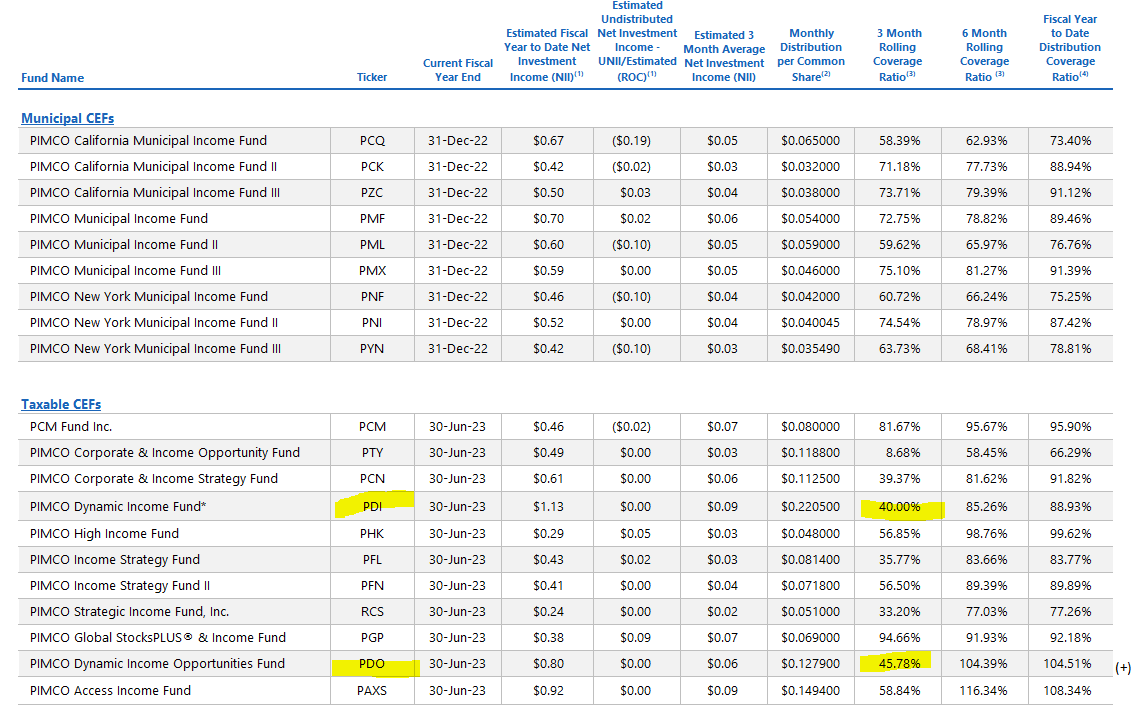

PIMCO Dynamic Income Fund ( PDI ) is the largest holding and was previously too. Their weighting only declined a bit from 6%. However, the fund's premium has also come down from the 5.8% it was at previously. Today, PDI's premium is standing at just over 10%, making it less attractive.

They also hold PIMCO Dynamic Income Opportunities Fund ( PDO ). This was one of my favorites through 2022 because of the abnormally large discount relative to other PIMCO names. PDO's discount has only narrowed slightly from our last update to what we see above. However, as of today, the fund has jumped to touch a premium, making it much less attractive.

The fund's distribution coverage had also been incredibly strong. That being said, the latest UNII report from PIMCO shows that coverage has collapsed on a 3-month rolling basis. The 6-month period can be a better gauge as it smooths the data, which can be more irregular for a 3-month period. While it's better, it also isn't looking too hot at this point either. So this will certainly be something to keep an eye on as we go forward.

{kind=link}

We also have some of the more boring CEFs that most investors don't like holding due to lower distributions. That includes Adams Express ( ADX ), Gabelli Dividend & Income Trust ( GDV ) and SRH Total Return Fund ( STEW ) (formerly the Boulder Growth & Income Fund (BIF). In holding them in FOF, you get a more regular monthly distribution that ADX and STEW don't pay. You also get a higher upfront distribution yield.

Of course, that doesn't mean that it is covered, as we showed above. As equity funds, these are more susceptible to declines overall. ADX's distribution yield history also is distorted due to its strategy. They pay out a low quarterly, then top off their minimum 6% managed distribution plan with a large year-end.

YCharts

There were three funds that dropped off the fund's top ten holding list. That included two commodity funds, Sprott Physical Gold and Silver Trust ( CEF ) and SPDR Gold Trust ( GLD ). The other name that fell off the top list was DoubleLine Income Solutions ( DSL ). At the same time, the fund's commodity fund exposure only declined from 7% to the 6% listed. So it wasn't an overall dramatic shift, and the allocations could have just fallen a bit, resulting in their removal from the top ten.

One name, in particular, that replaced those that fell off was the BlackRock Capital Allocation ( BCAT ). BCAT is one fund that is attractively valued and brings a lot of diversification to the table by itself. It is a multi-asset, multi-sector fund that can invest in just about anything Rick Rieder decides.

For that reason of being so diversified, some investors are probably disappointed. It has underperformed the S&P 500 significantly since it launched. However, that really isn't the fund's main goal. Reflecting the hybrid approach, the fund has significantly outperformed bonds. The fund's discount widening significantly is what resulted in most of the drop for this fund too. Which is one of the primary reasons it has appeal at this time.

YCharts

Conclusion

FOF invests in a basket of CEFs and ETFs. It is spread across 114 holdings, but each of these can also potentially hold hundreds or thousands of other positions. With that being the case, you could be exposed to 10,000+ stocks and bonds. Of course, a lot of these underlying positions will carry significant overlap. As a point, the fund holds both the SPDR S&P 500 ETF ( SPY ) and the Vanguard S&P 500 ETF ( VOO ).

However, the unfortunate point of this fund right now is that it is pushing near an all-time high premium. While the underlying CEFs might be attractively discounted, FOF could be the wrong way to benefit from that. Investing in your own CEFs directly or choosing an ETF fund of funds could be a better option for the time being.

For further details see:

FOF: An Interesting Fund Of Funds Approach