RSP - FOF: Attractive 9.50% Yield But Don't Buy It At The Current Premium

2023-08-04 15:33:48 ET

Summary

- The rapidly rising cost of living in the U.S. due to inflation is putting financial pressure on many Americans.

- Investors can earn income by purchasing shares of closed-end funds specializing in income generation.

- The Cohen & Steers Closed-End Opportunity Fund currently yields an attractive 9.50% and invests in a combination of common stocks and fixed-income assets.

- The fund underperforms a comparable index fund and has a significantly lower yield.

- It makes no sense to purchase this fund at the current premium, but an argument for it can be made if the price drops to a discount.

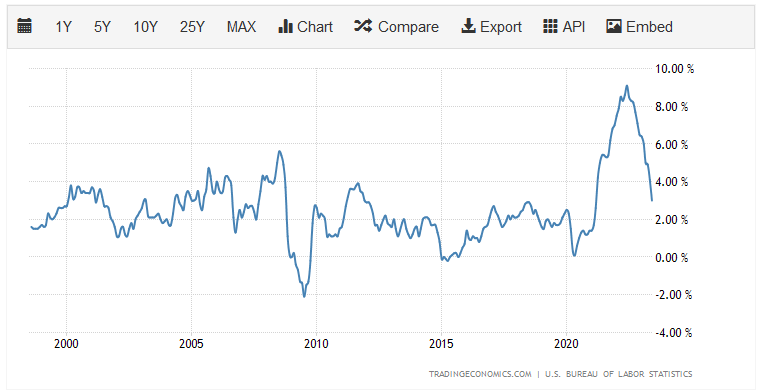

There can be little doubt that one of the biggest problems facing the average American today is the rapidly rising cost of living. Ever since the COVID-19 pandemic, inflation has been at the highest levels that the United States has experienced in decades, which has rapidly driven up the cost of food, energy, shelter, and just about everything else that we use in our daily lives. This is clearly shown by the consumer price index, which claims to measure the price of a basket of goods that is regularly purchased by the average American consumer:

{kind=link}

That chart shows the year-over-year change in the consumer price index every month over the past 25 years. As we can clearly see, this figure has been much higher than average over the past two or three years. This has put a great deal of financial pressure on many Americans and even forced some to resort to desperate measures simply to feed themselves and maintain some measure of comfort in their everyday lives. Indeed, I have speculated that these desperate measures have been one of the reasons why the jobs market continues to look strong, as large numbers of people are taking on second jobs simply to earn the money that they need to make ends meet.

As investors, we are certainly not immune to this situation. After all, we all require food for sustenance and need to heat our homes. We might also want to enjoy some of the comforts available in life. All of these things cost more money than they did a year or two ago. Fortunately, we do not have to resort to desperate measures to obtain the extra money that is needed to maintain our lifestyles. After all, we have the ability to put our money to work for us to earn an income. One of the best ways to accomplish this is to purchase shares of a closed-end fund, or CEF, that specializes in the generation of income.

These funds are unfortunately not particularly well followed in the financial media and are unfamiliar to many investment advisors. As such, it is not as easy to obtain the information that we would really like to have in order to make an informed investment decision. That is a shame because many of these funds offer certain advantages over familiar open-ended and exchange-traded funds. In particular, a closed-end fund is capable of employing certain strategies that allow them to boast higher yields than any of its underlying assets or indeed just about anything else in the market.

In this article, we will discuss the Cohen & Steers Closed-End Opportunity Fund ( FOF ), which currently yields an attractive 9.50%. That is certainly enough to appeal to any investor that is seeking a high level of income to sustain their lifestyle. As some readers might recall, I have discussed this fund before, but several months have passed since that time so obviously a great many things have changed. This article will therefore focus specifically on those changes and provide an updated analysis of the fund's finances. Let us investigate and see if this fund could be a good addition to your portfolio today.

About The Fund

According to the fund's webpage , the Cohen & Steers Closed-End Opportunity Fund has the objective of providing its investors with a high level of total return. This is not especially surprising considering that the fund is invested in a combination of both common stocks and fixed-income assets:

CEF Connect

The reason that this is not surprising is that common stock is by its very nature a total return vehicle. After all, investors purchase common stock for two purposes:

- To receive an income from the dividends that the company pays out.

- To benefit from capital gains as the issuing company grows and prospers.

This is the very definition of total return, which the fund itself confirms on its webpage:

The investment objective of the fund is to achieve total return consisting of high current income and potential capital appreciation through investments in the common stock of closed-end management investment companies that invest significantly in equity or income-producing securities.

The above asset allocation chart needs some clarification in light of this description. The fund is not investing in fixed-income securities such as bonds and preferred stock directly. Rather, what it is doing is purchasing closed-end funds that invest in these securities. Technically, all of the assets of the fund consist of common stock of other closed-end funds. The fact that the fund is splitting its assets between the various types of funds is nice to see as it provides it with exposure to each of these asset classes, which could help reduce the fund's overall volatility.

This comes from the fact that, historically, stocks and bonds move opposite to each other. In the past, stocks rose during a strong economy due to rising corporate profitability and the central bank would raise rates to keep inflation in check. This caused stocks to go up and bonds to decline during such a situation. The reverse happened during a recession, as falling corporate profits weighed on stocks and the central bank would cut rates in an attempt to stimulate spending and capital investment. That caused stocks to decline but bond prices to rise.

Unfortunately, the zero-interest-rate policy that prevailed in the United States and abroad over most of the past fifteen years has severed this link and now both asset classes tend to move in sync with one another. As such, the fund's strategy does not provide the inherent protection against volatility that it once did.

As regular readers are no doubt well aware, I have devoted a considerable amount of time and effort over the past several years to discussing closed-end funds here at Seeking Alpha. As such, many of the largest positions in the fund will probably be familiar. Here they are:

CEF Connect

I have discussed many of these funds in the past, so most of them should be somewhat familiar. As expected, we do see a variety of different types of funds here. The Adams Diversified Equity Fund ( ADX ) and Invesco S&P 500 Equal Weight ETF ( RSP ) are both equity funds that primarily invest in the largest companies in the United States. The Sprott Physical Gold and Silver Trust ( CEF ) is an interesting fund that simply holds gold and silver bullion in a vault in Canada and then sells shares against it. It differs a bit from most gold and silver funds in that the shares can actually be exchanged for physical bullion. The remainder of the funds on this list invest in either fixed-income securities or in both fixed-income securities and common equity.

There have been very few changes to the largest positions in the fund over the past few months. In fact, the only significant change is that the SPDR Gold Shares ( GLD ) exchange-traded fund was removed and replaced with the PIMCO Access Income Fund ( PAXS ). There were also a few weighting changes, but this could be explained by one fund outperforming another in the market. It is not necessarily indicative of the fund actively trading in the market in order to change its weightings.

The reason that this is important is that it costs money to trade closed-end funds or other assets, and these costs are billed directly to the fund's shareholders. This creates a drag on the overall performance of the fund and makes management's job more difficult. After all, the fund's management needs to deliver sufficient returns to cover the fund's expenses and still have enough left over to satisfy the shareholders. This is a task that very few management teams manage to accomplish on a consistent basis, and it is one reason why actively-managed funds usually underperform their benchmark indices.

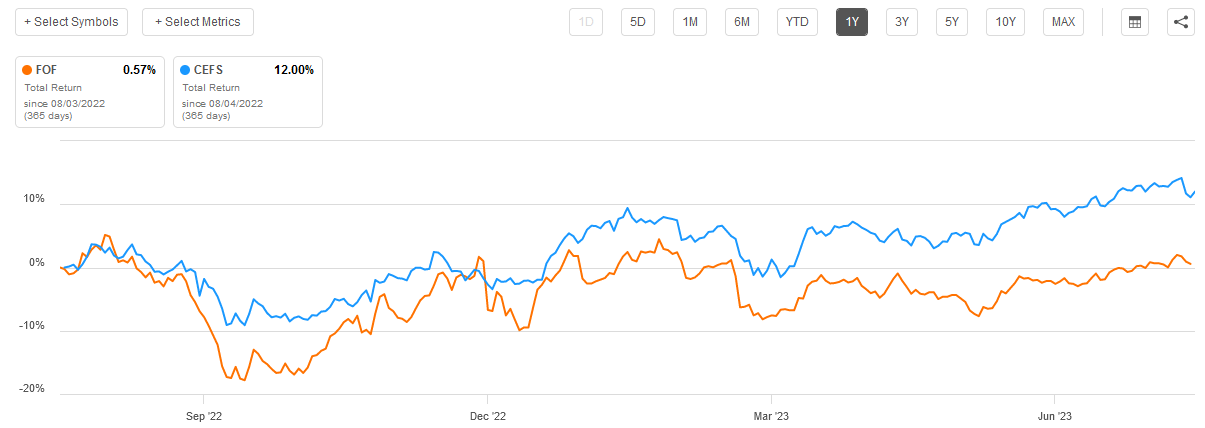

The Cohen & Steers Closed-End Opportunity Fund has not proven to be an exception to this rule over the past year. As we can see here, the fund's shares have fallen by 8.19% over the trailing twelve-month period:

{kind=link}

This is quite a bit worse than the Saba Closed-End Funds ETF ( CEFS ) delivered over the period. The index fund was almost flat, delivering a 0.20% gain over the period in question. Unfortunately, the high yield of the Cohen & Steers Closed-End Opportunities Fund does nothing to close the performance gap here as the index fund has a similarly high yield. As we can clearly see here, the index fund totally outperformed the closed-end fund in terms of total return:

{kind=link}

This certainly reflects quite poorly on the fund's management, as the closed-end fund underperforms a benchmark closed-end fund index on every possible measure. In fact, the index fund has a higher yield than the closed-end fund. This makes it difficult to make a good case for buying the Cohen & Steers Closed-End Opportunity Fund, especially as the fund's share price has actually outperformed the portfolio itself over most trailing periods:

Cohen & Steers

This is something that occasionally happens with closed-end funds, and it could unfortunately be a sign that the fund has gotten ahead of itself and is currently trading for well above its intrinsic value. We will discuss this later in this article.

Leverage

In the introduction to this article, I mentioned that closed-end funds have the ability to employ certain strategies that allow them to boost their effective yields well beyond that of any of the underlying assets. This is one reason why closed-end funds tend to boast higher yields than almost anything else in the market. One of the strategies used by these funds to accomplish this goal is the use of leverage. In short, a fund borrows money and then uses that borrowed money to purchase stocks, bonds, or other assets. As long as the yield that the fund gets from the purchased assets is higher than the interest rate that it has to pay on the borrowed funds, the strategy works pretty well to boost the effective yield of the portfolio. As closed-end funds are capable of borrowing money at institutional rates, which are considerably lower than retail rates, this will usually be the case.

Unfortunately, this strategy is not as effective today with interest rates at 6% as it was eighteen months ago as the difference between the yields of the purchased asset and the interest rate that the fund has to pay on the borrowed money will be much narrower than it used to be.

However, the use of debt in this fashion is a double-edged sword. This is because leverage boosts both gains and losses. This is not a particularly big deal with the Cohen & Steers Closed-End Opportunity Fund because it is not currently employing any leverage itself. However, most of the funds that are included in the portfolio do use leverage and so their share prices will almost certainly prove to be more volatile than market indices. That will naturally have an impact on the performance of this fund so it is something that we should keep in mind. With that said though, the goal of most closed-end funds is to maintain a relatively stable portfolio in terms of size and pay out all of the returns that they generate.

Distribution Analysis

As mentioned earlier in this article, the primary objective of the Cohen & Steers Closed-End Opportunity Fund is to provide its investors with a high level of total return. In order to achieve this objective, it invests in a portfolio of closed-end funds that usually have remarkably high yields. After all, the funds held by this fund are employing leverage to boost their returns relative to the market and pay out all of their investment profits.

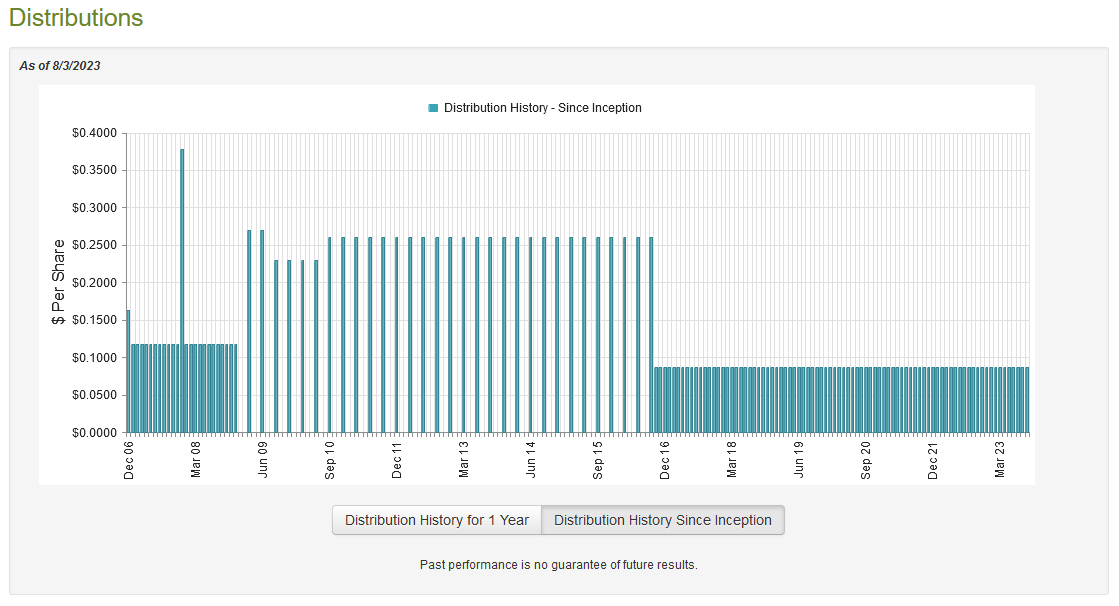

The Cohen & Steers Closed-End Opportunity Fund collects these distributions and pays them out to its own investors. As such, we can assume that it will probably have a very high yield itself. This is certainly the case as the fund pays a monthly distribution of $0.0870 per share ($1.044 per share annually), which gives it a 9.50% yield at the current price. This fund has generally been pretty consistent with its distribution over the years, although it has varied it once or twice over the past seventeen years:

{kind=link}

The general stability here is likely to appeal to any investor that is seeking a reasonably consistent and secure source of income to use to pay their bills or finance their lifestyles. It is difficult to explain how the fund has managed to be so consistent though, as many of the assets in its portfolio have changed their own distributions over the years. This is particularly the case with fixed-income funds that account for about half of the assets in this fund's portfolio. As such, we want to have a look at the fund's finances in order to determine how secure and sustainable its distribution is.

Unfortunately, we do not have an especially recent document that we can consult for the purposes of our analysis. As of the time of writing, the fund's most recent financial report corresponds to the full-year period that ended on December 31, 2023. As such, this report will not include any information about the fund's performance so far this year. That is a bit of a shame as the market so far in 2023 has been considerably stronger than last year's. However, sometimes seeing how well a fund handles a challenging market is much more insightful than seeing how well it handles a strong one.

During the full-year period, the Cohen & Steers Closed-End Opportunity Fund received $16,292,796 in dividends and surprisingly nothing in interest. Thus, the fund's total investment income was $16,292,796. The fund paid its expenses out of this amount, which left it with $13,223,196 available for shareholders. That was, unfortunately, nowhere close to enough to cover the $28,580,365 in distributions that the fund paid out over the period. This is something that is almost certain to be concerning at first glance as the fund does not have enough net investment income to cover its distributions.

Fortunately, the fund does have other methods through which it can obtain the money that it needs to pay its distributions. For example, closed-end funds frequently pay out return of capital distributions and the Cohen & Steers Closed-End Opportunities Fund will receive such distributions. These distributions are not included in investment income for the fund though, but they still represent money that can be paid out. The fund might also have capital gains that can be paid out. Unfortunately, it did not have much success at that during the full-year period. The fund reported net realized losses of $2,959,313 alongside $79,435,461 net unrealized losses over the period. In total, the fund's net assets declined by $96,869,870 during the period after accounting for all inflows and outflows. Thus, it did not come anywhere close to covering the distributions that it paid out.

This is a big problem for the sustainability of the distribution if the fund does not manage to correct this problem in the near future. Hopefully, it was able to earn sufficient gains during the first half of this year to both cover the distributions and rebuild the asset level of its portfolio, but we will have to wait until the fund releases its semi-annual report to know for certain how successful it was at this.

Valuation

It is always critical that we do not overpay for any asset in our portfolios. This is because overpaying for any asset is a surefire way to earn a suboptimal return on that asset. In the case of a closed-end fund like the Cohen & Steers Closed-End Opportunities Fund, the usual way to value it is by looking at the fund's net asset value. The net asset value of a fund is the total current market value of all the fund's assets minus any outstanding debt. It is therefore the amount that the shareholders would receive if the fund were immediately shut down and liquidated.

Ideally, we want to purchase assets of a fund when we can obtain them at a price that is less than net asset value. This is because such a scenario implies that we are acquiring the fund's assets for less than they are actually worth. This is, unfortunately, not the case with this fund today. As of August 3, 2023 (the most recent date for which data is available as of the time of writing), the Cohen & Steers Closed-End Opportunities Fund had a net asset value of $10.82 per share but the shares currently trade for $11.06 each. That gives the shares a 2.22% premium to the net asset value at the current price. That is worse than the 1.41% premium that the shares have averaged over the past month, and it is obviously above the intrinsic value of the shares.

Honestly, I cannot see any reason to purchase the shares of this fund at a premium, especially when a comparable index fund outperforms it and offers a higher yield. There could be a case to be made to buy this fund if it ever starts trading at a discount, though.

Conclusion

In conclusion, closed-end funds are generally an excellent way for an income investor to obtain a very high yield while still maintaining some diversification. The Cohen & Steers Closed-End Opportunity Fund offers one way to get a portfolio of these funds, allowing for a very high degree of diversification. The fund's almost even split between common equity and fixed-income funds is a pretty good way to reduce volatility historically, but unfortunately, this strategy has not worked very well for most of the past two decades.

When we consider that Cohen & Steers Closed-End Opportunity Fund underperformed a comparable index fund over the past year and has a lower yield, it makes absolutely no sense to purchase it at the current premium. Potential investors should wait until the shares are available at a price that is less than the net asset value.

For further details see:

FOF: Attractive 9.50% Yield, But Don't Buy It At The Current Premium