ECAT - FOF Is Richly Priced CEFS Could Be An Alternative

2023-11-30 13:50:51 ET

Summary

- Cohen & Steers Closed-End Opportunity Fund takes a fund of closed-end funds approach, offering significant diversification.

- FOF is currently trading at a fairly elevated premium, which is unusual in looking at its history and indicates it is overvalued.

- Saba Closed-End Funds ETF could be a potential alternative for investors, as shares can be picked up at NAV while waiting for a better entry level for FOF.

- Alternatively, CEFS just looks like a solid fund that investors could hold for the long term as well.

Written by Nick Ackerman, co-produced by Stanford Chemist.

Cohen & Steers Closed-End Opportunity Fund ( FOF ) takes a fund of closed-end funds approach, which allows for significant diversification by investing in one position alone. That can be one of the more appealing aspects of this approach. It can also often lead to discounts on discounts if FOF is trading at a discount.

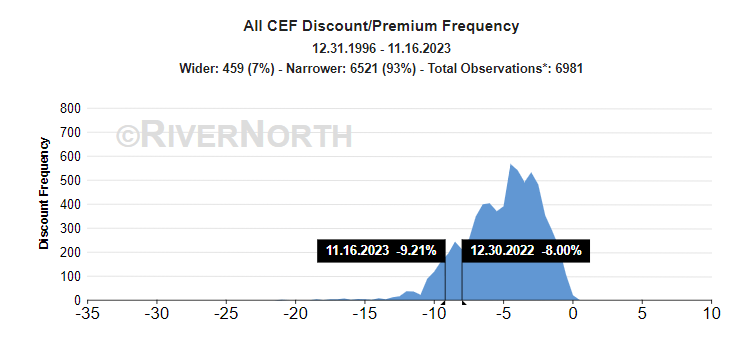

This is another appealing aspect of the fund, especially when CEFs are trading at historically wide discounts. While we are off the discount lows that we touched more recently, we are still trading at a place where CEF discounts are trading at tempting levels.

CEF Discount/Premium Historical Levels (RiverNorth)

{kind=link}

However, for FOF especially, it has been bucking this trend. Instead, in the last several years, it has been flirting with a premium instead. Though there have been periodic times when the fund could be had at a discount, currently, the fund is trading at a fairly elevated premium that is toward the highest level we've seen it reach historically. The premium has risen materially since our last update earlier this year.

Since the fund's inception, it has generally traded at a discount, so we are seeing a trading level that is well above that average at this time.

Ycharts

Considering we aren't getting the benefit of a discount on discount, choosing something like Saba Closed-End Funds ETF ( CEFS ) could be a potential alternative for investors to consider at this time while waiting for FOF to slip to a discount. As an ETF, the fund won't generally have to deal with drastic discounts/premiums.

FOF Basics

- 1-Year Z-score: 2.58

- Premium: 6.47%

- Distribution Yield: 9.47%

- Expense Ratio: 0.95%

- Leverage: N/A

- Managed Assets: $284.332 million

- Structure: Perpetual

FOF has an investment objective of "seeking to achieve total return consisting of high current income and potential capital appreciation." It will invest "in the common stock of closed-end management investment companies that invest significantly in equity or income-producing securities." This broad-based approach sets management up for an endless amount of flexibility.

CEFS Basics

- Dividend Frequency: Monthly

- Dividend Yield: 9.19%

- Expense Ratio: 2.42% (inclusive of acquired fund fees)

- Leverage: 14.2%

- Managed Assets: $143.5 million

- Structure: Active ETF

CEFS's investment objective and investment strategy are to "generate high income by investing in closed-end funds trading at a discount to net asset value, and heading the portfolio's exposure to rising interest rates."

The Opportunity

FOF doesn't utilize leverage at the fund level, and I view that as a positive at this time. CEFS, on the other hand, does incorporate leverage into its strategy. Additionally, the majority of CEFs are leveraged, and that means leverage on leverage. In some cases, it is highly leveraged, which is often the case for funds such as the PIMCO CEFs.

Another consideration is the expenses of the fund. By taking a fund-of-fund approach, you also get fees on fees. An important distinction here is that ETFs are required to also include the "acquired fund fees and other expenses."

In this case, the CEFS management fee is 1.10% , and the acquired fund fees and other expenses come to 1.32%. That pushes their total annual expenses to 2.42%.

CEFS Expense Ratio (Saba)

Due to being leveraged, CEFS will also have an interest expense, which came to 1.65% in their last semi-annual report .

On the surface, that makes the 0.95% expense ratio that FOF has look pretty good in comparison. However, closed-end funds are not required to include the underlying fund expenses. Therefore, the 0.95% reflects the management fee and operating expenses of the fund. It does not include the underlying fund expenses, which would presumably push it up to a similar level to that of CEFS management and acquired fund fees combined. Having no leverage, they won't have to worry about the interest expense at the fund level.

Both funds are also actively managed, with Saba being an activist that specifically targets opportunities to potentially exploit funds in the CEF space. FOF is typically more passive in that they aren't investing in funds to push them into tender offers, liquidating, or any other activist actions.

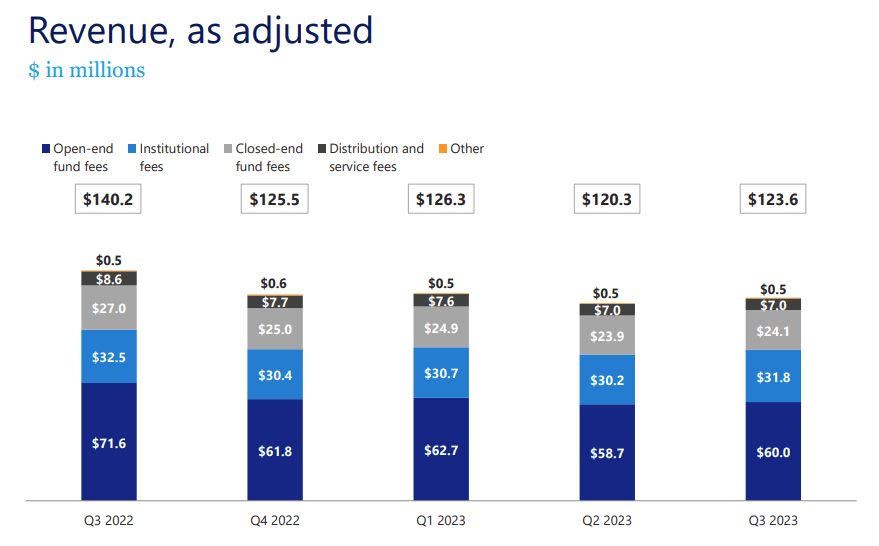

After all, they offer a lineup of closed-end funds that offer a fairly meaningful contribution to the company's revenues and profits. Things could get a little awkward if they were pushing peers to liquidate funds.

CNS Revenue Per Segment (Cohen & Steers)

{kind=link}

Considering the richer premium of FOF at this time, CEFS offering a chance to buy shares near parity with its NAV is something that is more attractive currently. This also means that while you aren't getting a discount on discounts, you're not paying a premium for discounts, which would somewhat offset the historically wide discounts that are available for CEFs right now.

At the same time, CEFS's historical performance has been able to top FOF, so that's something equally to be aware of. You at least aren't getting into a fund with a poor historical track record, though that, of course, doesn't guarantee you're getting a fund that will perform better going forward as well.

Ycharts

The divergence between these funds seemed to really come around the beginning of 2022. Prior to that, FOF was able to perform a bit more similarly to CEFS on a total return basis. The funds have performed closer on a total share price return basis due to FOF's rising premium. Going forward, one would have to anticipate that the premium likely continues to rise to outperform materially. In my opinion, history would suggest that isn't likely to happen.

A Look At The Portfolios

On the surface, the divergence in performance isn't really explained by how the funds are positioned more broadly. They both take an approach to investing across asset classes.

Here's a look at FOF's latest asset class breakdown:

FOF Asset Breakdown (Cohen & Steers)

Here is CEFS asset class breakdown:

CEFS Asset Breakdown (Saba)

The equity exposure for FOF was higher, but that wasn't necessarily something that would have seen the fund perform worse on the surface. Fixed-income funds were slammed while interest rates were rising rapidly.

One area that helped CEFS over FOF is that they were short Treasury Futures, which led to gains for the fund as rates rose higher. As yields rise, the price of Treasuries falls; thus, being short Treasury futures was the way they hedged against interest rates - as their investment strategy mentioned. The Saba pressures on the funds they did go into activist mode on could have also led to better outcomes.

Otherwise, the diverging performance simply came down to CEFS making better individual selections. Even with being leveraged, CEFS was able to hold up better and then rebound harder. In which case, that's a positive to be leveraged.

As of the end of October 2023 , CEFS listed 129 positions with an average weighted discount of -14.7% for the underlying holdings. At the end of September 2023 , FOF listed the average discount of the funds held came to -8.62% across 97 holdings.

Unfortunately, those are two quite different periods, and we don't have a direct comparison. While a month often wouldn't result in significant changes, the month of October just so happened to be particularly volatile in the overall market, and that did push around CEF discounts quite a bit. At least, in general, it can give us some context of what the discounts of the underlying funds were for each.

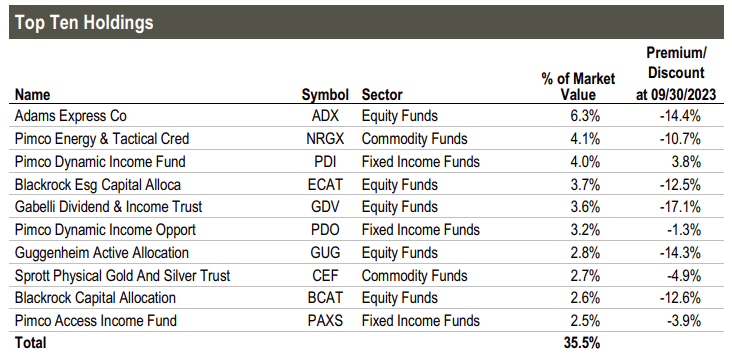

While FOF might not take an active approach to being an activist, we can see from their top ten holdings that several are targets of Saba.

FOF Top Ten Holdings (Cohen & Steers)

{kind=link}

One of those targets, in particular, is BlackRock ESG Capital Allocation Term Trust ( ECAT ), which is the largest position in CEFS. That was as of August 31, 2023, when the last update of their full holdings was available. That accounted for around 15.5% of the fund's total managed assets.

The Distributions

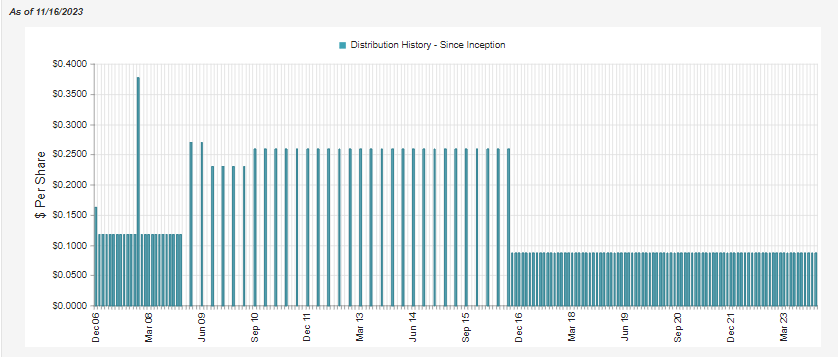

Both funds also sport high distribution rates for investors. FOF is currently at a rate of 9.47%, but due to its premium, the fund has to earn around 10.09% currently to cover it. The fund cut its distribution twice during the GFC, but it otherwise had been quite steady. When they switched back from a quarterly distribution schedule to a monthly, it was the same equivalent payout. Meaning that they've held the payout steady since 2010.

FOF Distribution History (CEFConnect)

{kind=link}

CEFS also takes the approach of offering a managed distribution that allows for a level and predictable payout from the fund. This is a bit more unusual for ETFs, but given the underlying holdings, it makes sense, as CEFs frequently have level payout policies.

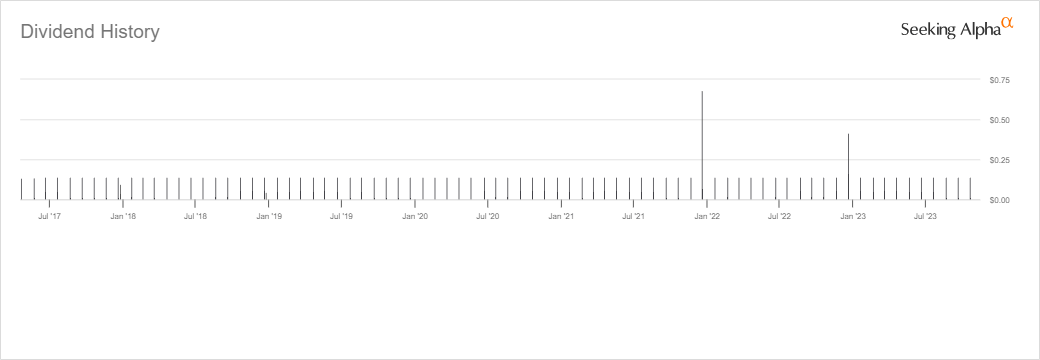

It hasn't been around as long as FOF, but during this time, the fund has held the monthly $0.14 steady the entire time. They even were able to pay out a couple of year-end specials along the way. Based on this amount, the current distribution yield comes to 9.19%.

CEFS Distribution History (Seeking Alpha)

{kind=link}

Conclusion

FOF takes an interesting fund of closed-end funds approach to investing that means instant massive diversification. If FOF drops to a sizeable discount, it would look much more appealing. That said, due to the premium that the fund is trading at, CEFS could be a potentially better alternative for the time being as a place to hide out for a better opportunity.

For further details see:

FOF Is Richly Priced, CEFS Could Be An Alternative