PSLV - FOF: Narrowing Premium Helps But Distribution Could Be Under Pressure

2023-10-13 14:17:49 ET

Summary

- Cohen & Steers Closed-End Opportunity Fund allows investors to easily assemble a portfolio consisting of other closed-end funds.

- The FOF closed-end fund has underperformed a similar exchange-traded fund recently, which could partly be due to a narrowing price premium.

- The FOF fund offers a high yield of 10.31% but may face challenges in covering its distribution if unrealized gains have been eroded.

- The fund's price has been improving, as investors become less willing to overpay for assets in the rising rate environment.

The Cohen & Steers Closed-End Opportunity Fund ( FOF ) is a closed-end fund aka CEF with a rather interesting premise. Rather than requiring investors to go through all the work of finding their own funds to invest in and configure their portfolio around it, the fund itself will assemble a portfolio consisting of other funds and then allow investors to simply purchase its shares. In this way, it is similar to the Saba Closed-End Funds ETF ( CEFS ), except that it is not structured as an exchange-traded fund.

As is the case with most closed-end funds, the Cohen & Steers Closed-End Opportunity Fund provides its investors with a very attractive 10.31% yield, which is high enough to attract many income-focused investors. When we consider the diversity that this fund would have simply by virtue of the fact that its assets are other funds, this could very easily be a very appealing choice for any income-focused investor.

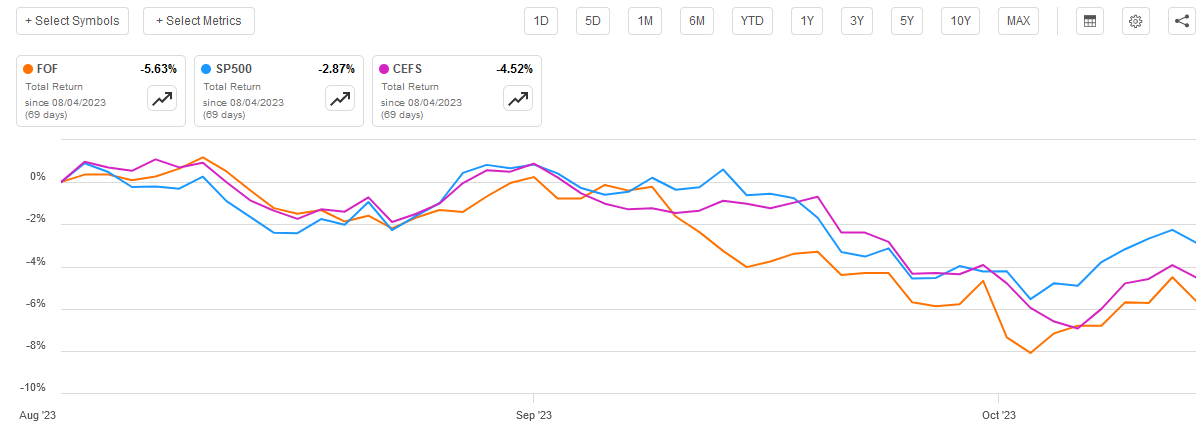

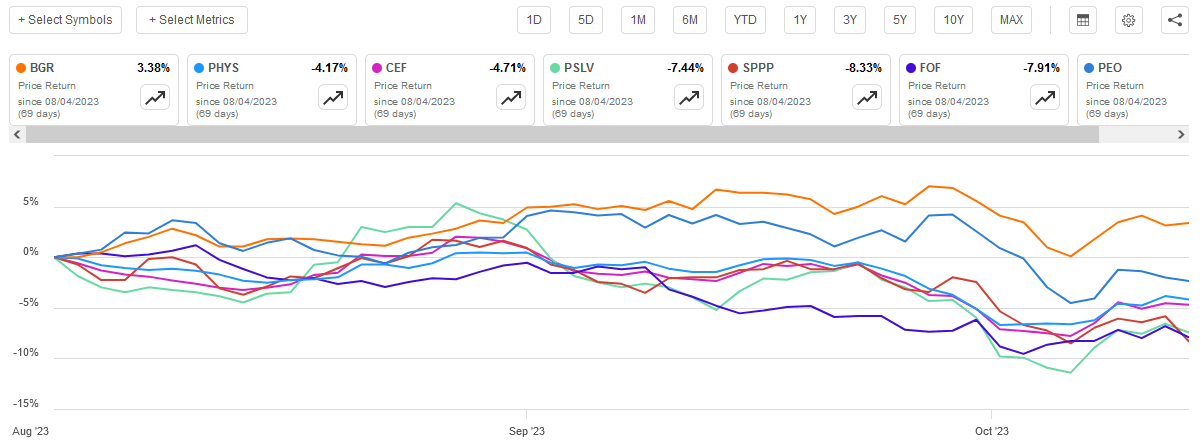

As regular readers may recall, we last discussed this fund in early August. Unfortunately, its performance since that time has left something to be desired. The fund has handed its investors a 5.63% loss over the period when we consider the fact that its interim distributions offset some of the share price declines. This is worse than either the S&P 500 Index ( SP500 ) or the Saba Closed-End Funds ETF:

{kind=link}

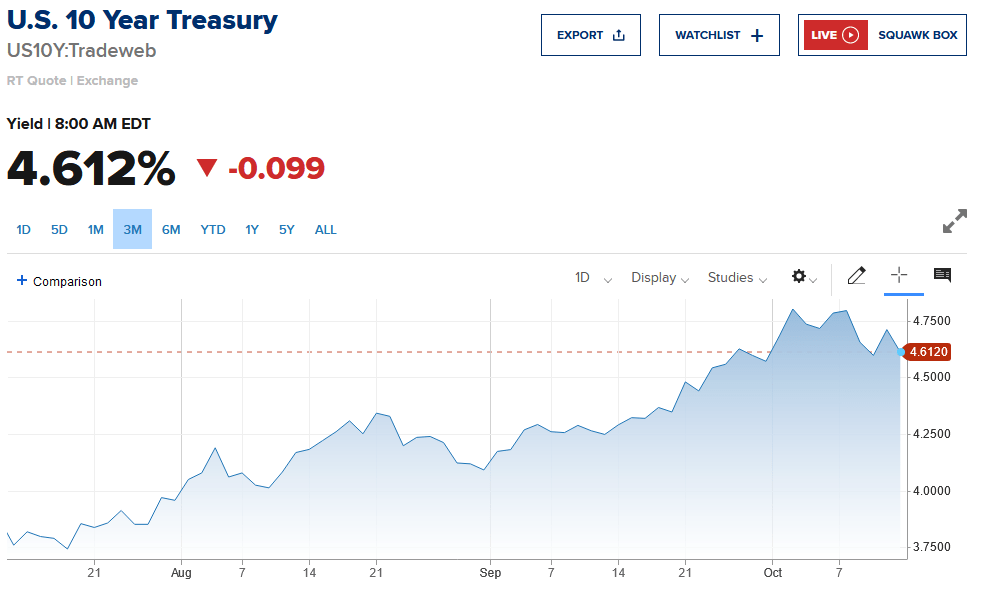

One of the reasons for this is the rising interest rate environment that dominated the market over the period. As everyone reading this is well aware, the market has finally abandoned its optimism about a near-term pivot by the Federal Reserve and has started to allow interest rates to rise. This is especially true with respect to long-term rates, as the interest rate on the ten-year Treasury has gone from 3.759% three months ago to 4.612% today:

{kind=link}

As many closed-end funds invest in fixed-income securities, this had a negative effect on their portfolios and share prices. In addition, some closed-end funds are purchased primarily for the yields, and pretty much everything that this situation applies to would decline in price so that it delivers an appropriate premium to the ten-year U.S. Treasury.

However, these statements also apply to the Saba Closed-End Funds ETF, which invests in very similar assets. As such, the fact that it outperformed the Cohen & Steers Closed-End Opportunity Fund is something that does not speak particularly well about this fund. We should investigate further to determine the potential causes of this.

About The Fund

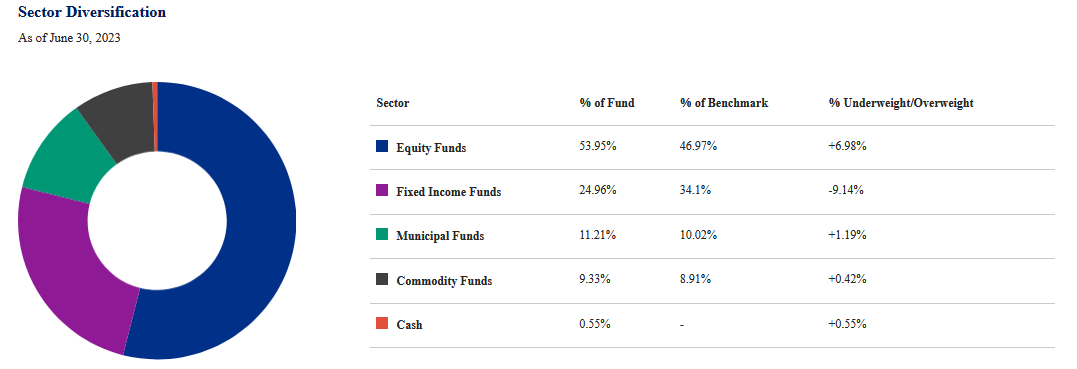

According to the fund's webpage , the Cohen & Steers Closed-End Opportunity Fund has the primary objective of providing its investors with a high level of total return. This is not particularly surprising considering that the fund invests in a combination of equity and fixed-income closed-end funds. As of the time of writing, 53.95% of the fund's assets are invested in equity closed-end funds. The remainder is invested in a combination of fixed-income, municipal bond, and even commodity exchange-traded funds:

{kind=link}

As I have explained in many previous articles, common equities are by their very nature total return instruments. After all, with the exception of a handful of real estate investment trusts and energy companies, nobody is going to purchase common equities as a source of income because their yields are far too low. As of right now, the S&P 500 Index ( SPY ) yields 1.50% and even the traditionally high-yielding utility sector ( IDU ) only yields 3.00% at the current level. These are both significantly less than a money market fund can be expected to pay out right now. The only sectors where equities can be consistently found with a yield above a money market fund are real estate and traditional fossil fuel energy. As such, most equity closed-end funds will have total return as their primary objective since they are after both income and capital gains. That would naturally apply to this fund as well, to a certain degree. After all, it is hoping to generate income from the distributions paid out by the closed-end funds in its portfolio as well as profit from share price appreciation.

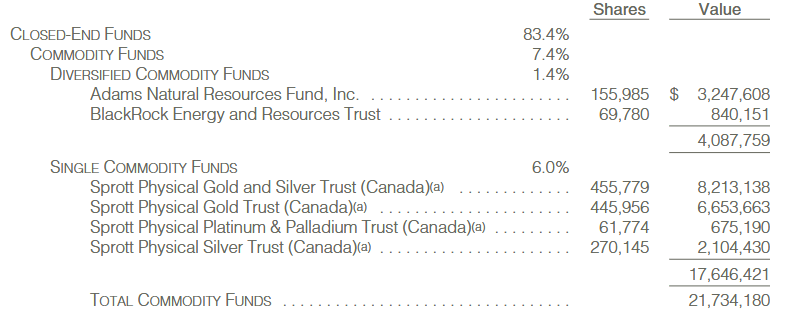

The one possibly surprising thing that we see above is that the Cohen & Steers Closed-End Opportunity Fund maintains an allocation to commodity funds. These are not the funds that many people think of when they picture a commodity fund. A common method for investors who wish to profit from price gains in a commodity is to purchase a sector fund that invests in companies producing that commodity. For example, an investor might purchase a fund like the GAMCO Global Gold, Natural Resources & Income Trust ( GGN ) if they want to profit from price gains in gold. This fund does do that to a certain extent, but primarily it is investing in funds that actually hold the physical commodity such as the Sprott funds. Here are the fund's commodity fund holdings from the semi-annual report :

{kind=link}

It is somewhat surprising that the fund would call something like the Adams Natural Resources Fund ( PEO ) or the BlackRock Energy and Resources Trust ( BGR ) a commodity fund since those are both technically equity funds that invest in commodity producers. The Sprott Funds are quite different since those actually represent shares of the physical gold, silver, or platinum bullion stored in a vault in Canada. Nevertheless, we can see that this fund does have some exposure to commodity price appreciation, which should help it protect itself somewhat against the ravages of inflation. As long-time readers also know, I am long-term bullish on both crude oil and precious metals, so I rather like seeing that this fund seemingly is as well.

In the introduction to this article, I pointed out that the Cohen & Steers Closed-End Opportunity Fund underperformed the Saba Closed-End Funds ETF since the start of August. One area in which they differ is that the Saba Fund does not specifically state any commodity exposure. Rather, the fact sheet describes its holdings as a 55% equity/45% fixed-income split. Thus, it is possible that the presence of the commodity funds created a drag on this fund's performance relative to the exchange-traded fund. That seems somewhat unlikely though, as crude oil prices are actually up since that article was published. In fact, all of the commodity funds outperformed the Cohen & Steers Closed-End Opportunity Fund since that article was written, except for the Sprott Physical Platinum and Palladium Trust ( SPPP ):

{kind=link}

In table form:

| Fund |

| Price Performance Since August 4, 2023 |

| Cohen & Steers Closed-End Opportunity Fund |

| -7.91% |

| BlackRock Energy & Resources Trust |

| +3.38% |

| Adams Natural Resources Fund ((PEO)) |

| -2.35% |

| Sprott Physical Gold and Silver Trust ( CEF ) |

| -4.71% |

| Sprott Physical Gold Trust ( PHYS ) |

| -4.17% |

| Sprott Physical Silver Trust ( PSLV ) |

| -7.44% |

| Sprott Physical Platinum and Palladium Trust |

| -8.33% |

In fact, all of these except for the Sprott Physical Platinum and Palladium Trust outperformed the Saba Closed-End Funds ETF as well. Thus, it was definitely not the presence of the commodity funds that dragged down this fund's performance. In fact, they almost certainly helped it and the fund would have done worse without their presence.

One thing that we do see though is that the fund's price premium has been narrowing:

CEF Connect

The last time that we discussed this fund, it was fairly expensive with its shares trading 2.22% above the actual value of the fund's assets. This difference appears to be narrowing, so any real discussion of the difference between the assets of the two funds may be immaterial when determining the reason for the performance difference. After all, exchange-traded funds are designed so that the share price in the market is always in line with the performance of the fund's assets. However, that is not the case with closed-end funds, which can sometimes have the fund's share price deliver a wildly different performance than that of the actual assets in its portfolio. This could very well be what we are seeing here with respect to this fund's performance versus an exchange-traded fund that employs a similar strategy.

Distribution Analysis

As mentioned earlier in this article, the primary objective of the Cohen & Steers Closed-End Opportunity Fund is to provide its investors with a very high level of total return. However, in order to accomplish this objective, the fund invests in a portfolio consisting of shares of other closed-end funds. As I have pointed out in various previous articles, one of the defining characteristics of closed-end funds is that they try to keep their assets under management relatively stable while paying out all of their investment returns to the shareholders. As they are paying out both received income and capital gains net of expenses, they tend to have very high yields. This alone would give the Cohen & Steers Closed-End Opportunity Fund a relatively high yield from its own portfolio. However, this fund itself may be able to generate some capital gains when the shares of the funds that comprise its portfolio appreciate in value. The fund combines its income with any capital gains that it manages to achieve and pays that amount, net of the fund's expenses, out to its own shareholders. This might be expected to give this fund a fairly high yield itself.

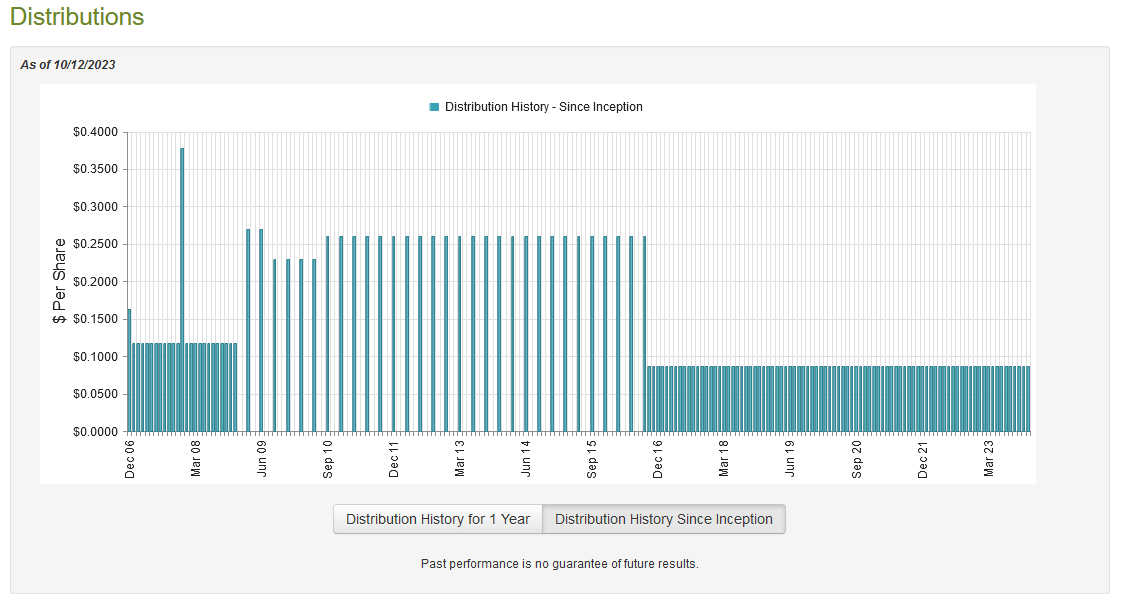

This is certainly the case, as the Cohen & Steers Closed-End Opportunity Fund pays a monthly distribution of $0.0875 per share ($1.05 per share annually), which gives it a respectable 10.31% yield at the current price. The fund has been remarkably consistent with respect to its distribution over the years:

{kind=link}

This distribution history will undoubtedly be attractive to anyone who is seeking to earn a safe and consistent source of monthly income that they can use to pay their bills or other lifestyle expenses. Unfortunately, the fact that it is flat rather than growing does mean that it has been losing purchasing power in the face of the highest inflation rate that we have seen in decades, but this problem can be offset by using part of the distribution to buy new shares on a regular basis.

As is always the case, it is important that we investigate the fund's ability to cover its distribution. After all, we do not want to be the victims of a distribution cut since that would both reduce our incomes and most likely cause the fund's share price to decline.

Fortunately, we do have a relatively recent document that we can consult for the purpose of our analysis. As of the time of writing, the fund's most recent financial report corresponds to the six-month period that ended on June 30, 2023. This document was linked to earlier in this article. This is a more recent document than the one that we had available to us the last time that we discussed this fund, which is quite nice. After all, the first half of 2023 was a much stronger market than the one that we experienced in 2022 so that could have given the fund the potential to earn some capital gains by selling appreciated assets into the market strength. While the market has since started to correct, that will not be reflected in this report as the correction started after June 30, 2023.

During the six-month period, the Cohen & Steers Closed-End Opportunity Fund received $7,048,918 in dividends from the assets in its portfolio. It received no income from interest or any other source, which is somewhat surprising. As such, the fund's total investment income was only $7,048,918 during the period. The fund paid its expenses out of this amount, which left it with $5,654,010 available for shareholders. That alone was nowhere close to enough to cover the $14,327,202 that the fund actually paid out in the form of distributions. At first glance, this may be concerning as the fund clearly failed to fully cover its distribution out of net investment income.

However, the fund does have other methods through which it can obtain the money that it needs to cover its distribution. For example, it might have been able to realize some capital gains that could be distributed to the investors. Unfortunately, the fund had mixed results in this task during the period. The fund reported net realized losses of $4,795,473 during the period but these were offset by $17,734,162 net unrealized gains. Overall, the fund's net assets increased by $4,801,998 after accounting for all inflows and outflows during the period. Thus, technically the fund did manage to cover its distribution, which represents a substantial improvement in its performance in the full-year 2022 period. We discussed that disappointing performance in the prior article on this fund.

It is important to note though that the fund relied on unrealized gains to cover the distribution. This is not necessarily a problem if it managed to realize those gains shortly after the end of the period. However, the market began to correct in mid-July and has basically continued on this downward trend for the past two months. This is particularly true in the fixed-income space, and as we saw earlier fixed-income assets account for a considerable proportion of the fund's portfolio.

As such, there is a chance that this fund saw much of its unrealized capital gains erased since the time that this report was released. If this is the case, then the distribution could be in more jeopardy than it appears since the fund may be looking at eighteen months to two years of losses. After all, I will admit that I doubt that we will enter a sustained bull market over the next two months.

Valuation

As of October 12, 2023 (the most recent date for which data is available as of the time of writing), the Cohen & Steers Closed-End Opportunity Fund has a net asset value of $10.01 per share. However, the shares currently trade at $10.17 each. This gives the fund's shares a 1.60% premium on net asset value at the current price. This is better than the 2.20% premium that the fund's shares had the last time that we discussed it, which confirms that some of the fund's price decline was simply caused by its premium narrowing. However, the current price is still higher than the 1.18% premium that the shares have had on average over the past month. In addition, it is generally not a great idea to buy any fund at a premium. Thus, it may be best to wait for the price to decline before purchasing shares of this fund.

Conclusion

In conclusion, the Cohen & Steers Closed-End Opportunity Fund has not been delivering a particularly strong performance in the market over the past two months. This is partly due to the fact that its share price premium has been narrowing in the current market environment. This is not entirely surprising, as rising rates have reduced the appetite and willingness of investors to overpay for assets.

However, the fund still does have a premium, so it might not be the best idea to purchase shares right now. This is especially true considering that the distribution may be under some pressure unless the fund managed to lock in its unrealized gains back in July.

For further details see:

FOF: Narrowing Premium Helps, But Distribution Could Be Under Pressure