ADX - FOF: This Attractive CEF Has Nice Features But Is Substantially Overpriced

2023-04-19 11:23:20 ET

Summary

- Today's incredibly high rate of inflation has made investors hungry for income.

- Cohen & Steers Closed-End Opportunity Fund invests in a portfolio of high-yielding closed-end funds to provide its investors with a high level of income.

- The FOF closed-end fund's strategy appears solid as it is reasonably well diversified and consistently beats its benchmark indices.

- The fund has overdistributed over the past two years, which puts pressure on its ability to maintain its distribution.

- The FOF fund is trading at a premium, so the price is clearly too high here.

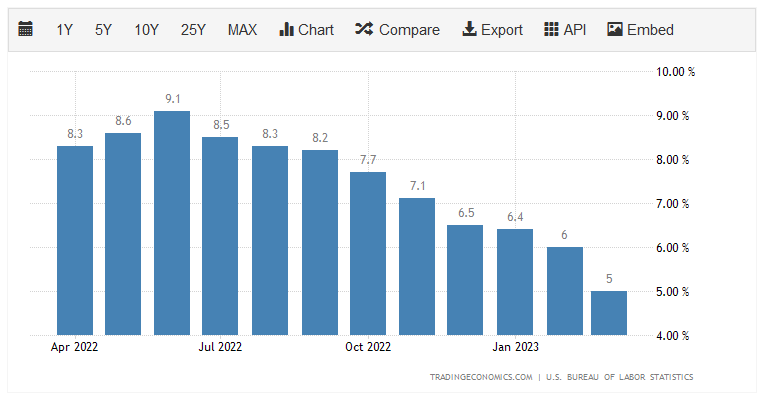

Without a doubt, one of the biggest problems facing Americans today is the incredibly high level of inflation that has been dominating the economy. Over the past twelve months, there has only been one month in which the consumer price index showed less than a 6% increase year-over-year:

{kind=link}

As I discussed in a recent blog post , this has had a devastating effect on consumers, particularly those of limited financial means. This is especially problematic since food, energy, and other necessities are some of the items that have seen the greatest price appreciation. This has caused many people to take on second jobs or enter into the gig economy in an effort to obtain the extra money that they need to buy food and keep themselves and their families fed.

Fortunately, as investors, we have other means that we can employ to obtain the extra income that we need to maintain our lifestyles. After all, we have the ability to put our money to work for us in this capacity. As I have discussed in various previous articles, one of the better ways to do this is to purchase shares of a closed-end fund, or CEF, that specializes in the generation of income. However, there are a substantial number of these funds so it can be complicated and confusing to put together a portfolio of them. One solution then is to purchase a fund that invests in other funds. This gives you the advantage of professional management for your closed-end fund portfolio as well as possibly getting a higher yield than the underlying funds. This is because the closed-end fund of funds is able to employ certain strategies that have the effect of boosting its overall portfolio yield.

In this article, we will discuss the Cohen & Steers Closed-End Opportunity Fund ( FOF ), which is one of the more well-known funds available in this category. As of the time of writing, this fund yields 9.48%, so it does manage to boost a higher yield than many other closed-end funds, but it is admittedly not the highest in the sector. I have discussed this fund before, but that was close to two years ago, so obviously numerous things have changed. This article will therefore focus specifically on those changes as well as provide an updated analysis of the fund’s finances. Let us investigate and see if this fund could be a good addition to your portfolio today.

About The Fund

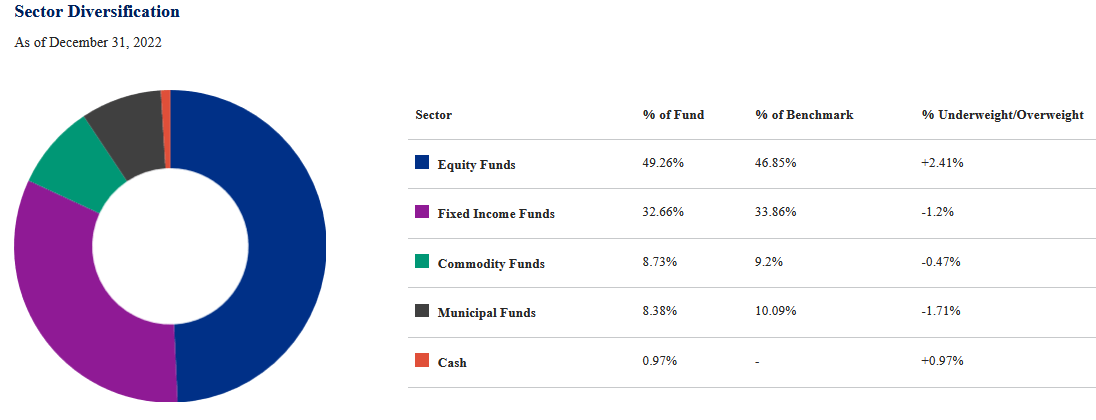

According to the fund’s webpage , the Cohen & Steers Closed-End Opportunity Fund has the stated objective of providing its investors with a high level of total return. That is not particularly surprising for a fund like this one. This is because closed-end funds themselves typically aim to deliver either current income or total return, depending on their type. A fixed-income fund will normally target current income as an objective while an equity fund will target total return. This fund, for its part, is split between the two types but it does have a higher allocation to equity funds:

{kind=link}

Total return is the most logical objective of this fund since that is what the equity funds and commodity funds in its portfolio are aiming to maximize. Those two types of funds account for 57.99% of the portfolio, which is the majority. This does not mean that the Cohen & Steers Closed-End Opportunity Fund is sacrificing its potential for income, however. This is because closed-end funds operate a bit differently than exchange-traded funds. A closed-end fund will generally try to keep its share price fairly flat and pay all of its capital gains and income after expenses to the shareholders via its distribution. This should result in a significant amount of money flowing into the Cohen & Steers fund that it can pay out to its own investors. Indeed, the fund’s own website implies that it is doing precisely that:

“The investment objective of the Fund is to achieve total return consisting of high current income and potential capital appreciation through investments in the common stock of closed-end management investment companies that invest significantly in equity or income-producing securities.”

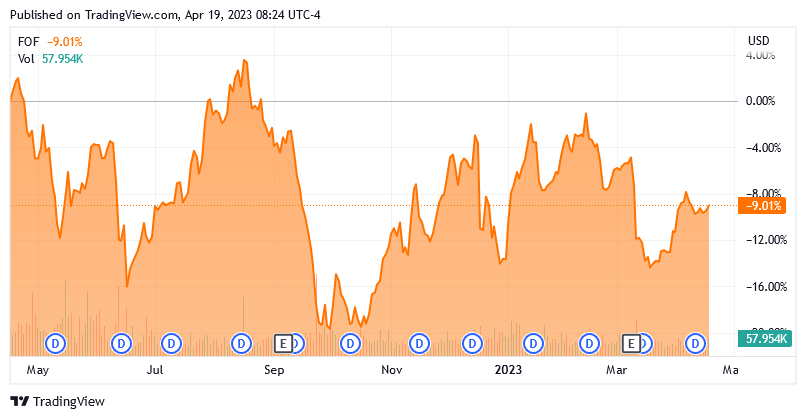

This fund has not done a great job keeping its share price level over time, though. As we can see here, the Cohen & Steers Closed-End Opportunity Fund has lost 9.01% over the past year:

{kind=link}

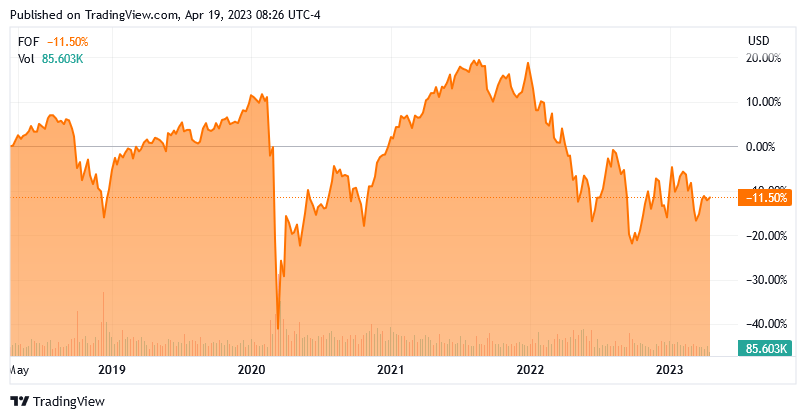

The fund’s long-term performance is even worse, as it is down 11.50% over the past five years:

{kind=link}

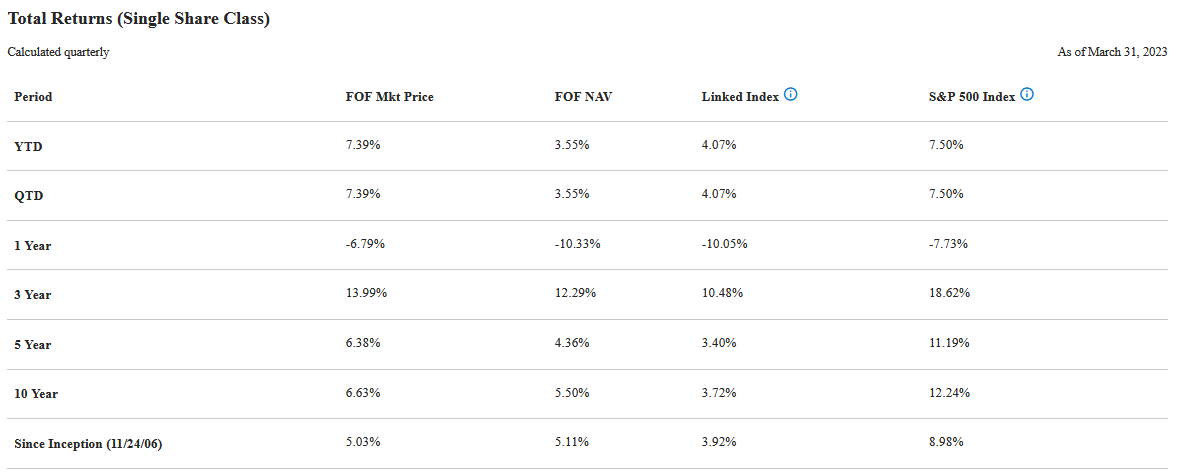

However, this is somewhat misleading for two reasons. The first is that it does not consider the effect of the fund’s distributions on the return actually realized by investors. The fund’s yield is actually higher than the amount that it lost over the past year, and it did manage to beat the S&P 500 Index (SP500) in 2022. The second reason that just looking at the fund’s chart is misleading is that closed-end fund shares can sometimes deliver very different performances in the market than the fund’s portfolio itself actually delivers. That can result in situations in which an investor can purchase shares of a fund for less than the market value of the assets that are represented by each share. That is different from both open-end mutual funds and exchange-traded funds which are both priced in line with the performance of the underlying portfolio.

This chart shows the actual performance of the fund that would be realized by an investor that reinvested the distributions that were received into the fund’s own shares:

{kind=link}

The performance at net asset value is the most important, as that shows us what the fund’s underlying portfolio actually delivered. This is much better than the share price performance over the same period. We do see, though, that the fund generally underperformed the S&P 500 Index though, which is quite disappointing. It is also not exactly surprising though because this fund has a significant allocation to fixed-income funds that are invested in bonds or preferred stocks. Bonds and preferred stocks are considered to be less risky than the common stocks that comprise the S&P 500 Index, so they should generally deliver a lower return. The fund’s benchmark index is the Morningstar US All Taxable Ex-Foreign plus Capped Muni CEF Index, which it managed to beat handily over any given period. That is certainly an admirable performance that is better than most funds are able to deliver.

As regular readers are no doubt well aware, I have devoted a considerable amount of time and effort over the past few years to the discussion of closed-end funds here at Seeking Alpha. As such, many of the largest positions in the fund will likely be familiar to most readers. Here they are:

CEF Connect

Admittedly, we do see quite a few funds here that I have never specifically discussed, but there are a few that I have, such as the Adams Diversified Equity Fund ( ADX ), both of the PIMCO funds, the Gabelli Dividend & Income Trust ( GDV ), and the Sprott Physical Gold and Silver Trust ( CEF ). Overall, this list largely conforms to the fund’s structure that we saw earlier as we see a combination of equity, fixed-income, and commodity funds listed here.

The largest positions list is vastly different from the last time that we looked at the fund though. In fact, the only funds that are still on the list compared to August 2021 are the Gabelli Dividend & Income Trust and the PIMCO Dynamic Income Opportunities Fund ( PDO ). Everything else was added over the past year and a half. This might indicate that the Cohen & Steers Closed-End Opportunity Fund has a fairly high turnover. This is not entirely true as the fund had a 52.00% annual turnover in 2022, which is higher than many funds, but it is far from the 90% or higher that we sometimes see. In fact, a 52.00% annual turnover is pretty close to the median for closed-end funds. The reason that this is important is that it costs money to trade stocks or other assets, which is billed directly to the fund’s shareholders. This creates a drag on the portfolio’s performance and makes management’s job more difficult. After all, the fund’s management will need to earn sufficient returns to both cover these added expenses and provide a return that is sufficient to satisfy the shareholders. That is something that very few management teams are able to do consistently, which tends to result in most actively managed funds failing to beat their benchmark indices. As we just saw though, this one has managed to pretty consistently outperform, although it still failed to beat the S&P 500. That overall speaks pretty well for the management of this fund.

Distribution Analysis

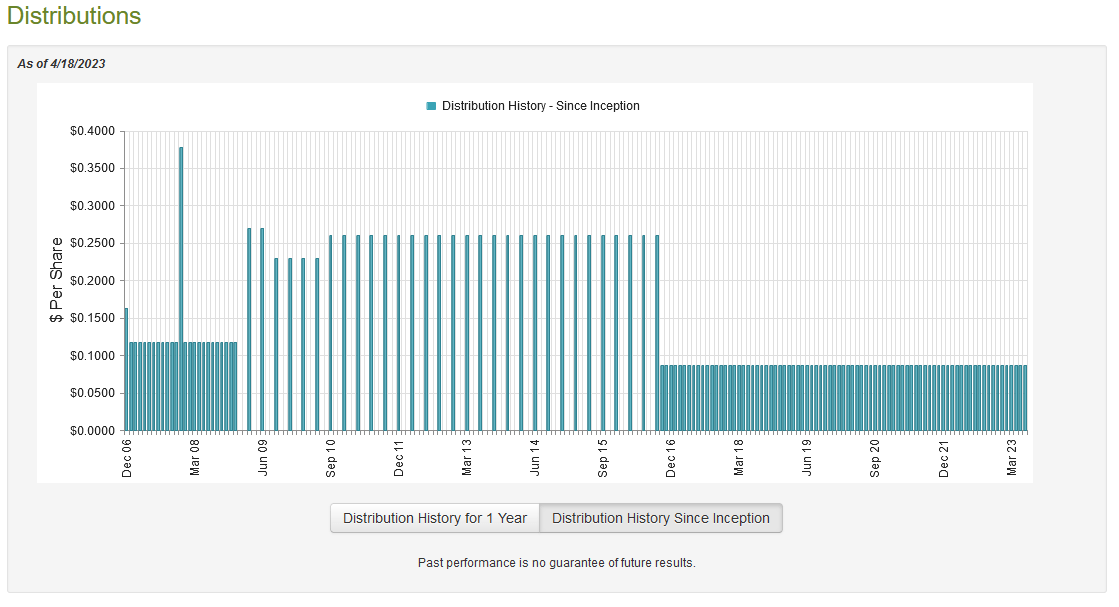

As stated in the introduction, one of the advantages of closed-end funds is that they tend to boast higher yields than just about anything else in the market. This is due to their practice of paying out essentially all of their capital gains and income after expenses, combined with the fact that many funds employ leverage in order to boost their returns (although the Cohen & Steers Closed-End Opportunity Fund does not). As this fund invests in a portfolio of these high-yielding assets and follows the same strategy of attempting to maintain a stable share price while paying out all income and capital gains, we can assume that it will also have a very high yield. That is certainly the case as the Cohen & Steers Closed-End Opportunity Fund pays out a monthly distribution of $0.0870 per share ($1.044 per share annually), which gives it an impressive 9.48% yield at the current price. The fund has been surprisingly consistent about its distribution over the years:

{kind=link}

There might be some readers that point out that the fund’s distribution seemingly dropped considerably in the middle of 2016. However, that was actually a switch from a quarterly to a monthly distribution. The fund’s distribution went from $0.26 per share quarterly to $0.870 per share monthly. That is actually a very slight increase when viewed on an annual basis ($0.004 per share). Thus, the fund’s annual distribution has been almost completely stable since 2007 with only a small decrease around the time of the 2009 recession. This is a very impressive track record that is likely to endear this fund to any investor that is seeking a stable and secure source of income to use to pay their bills or finance their lifestyles. As is always the case though, it is important for us to investigate the company’s ability to maintain this distribution. After all, we do not want to be the victims of a distribution cut in the future that reduces our incomes and almost certainly causes the fund’s share price to decline.

Fortunately, we do have a remarkably current document that we can consult for our analysis. The fund’s most recent financial report corresponds to the full-year period that ended on December 31, 2022. This is therefore a more recent report than some other funds have provided to their investors and it should give us a pretty good indication of how well this fund handled the somewhat volatile markets that dominated in 2022. During the full-year period, the Cohen & Steers Closed-End Opportunity Fund received a total of $16,292,796 in dividends and surprisingly no interest. Thus, that $16,292,796 comprised its entire income for the period. The fund paid its expenses out of this amount, which left it with $13,223,196 available for the shareholders. This was, unfortunately, not nearly enough to cover the $28,580,365 that the fund actually paid out in distributions over the course of the year. This is something that may be concerning at first glance as it clearly indicates that the fund did not have sufficient net investment income to cover its distributions.

However, the fund does have other methods through which it can obtain the money that is needed to cover the distribution. For example, some of the distributions that it received from the funds in its portfolio may have been considered a return of capital or capital gains. Those things are not included in net investment income. The fund might also generate capital gains through its own trading activity. As might be expected considering the weakness in the market over the course of the year though, the fund reported net realized losses of $2,959,313 and had another $79,435,461 net unrealized losses. It did not specifically state how much it received as a return of capital distributions, but overall, the fund’s assets declined by $96,869,870 after accounting for all inflows and outflows during the year.

That is certainly concerning, as it is a clear sign that the fund distributed too much money over the course of the year. The fund’s assets did increase during 2021, but they are still down over the two-year period. If the fund cannot reverse its losses in the near future, it may, unfortunately, be forced to cut the payout.

Valuation

It is always critical that we do not overpay for any asset in our portfolios. This is because overpaying for any asset is a surefire way to earn a suboptimal return on that asset. In the case of a closed-end fund like the Cohen & Steers Closed-End Opportunity Fund, the usual way to value it is by looking at the fund’s net asset value. The net asset value of a fund is the total current market value of all the fund’s assets minus any outstanding debt. It is therefore the amount that the shareholders would receive if the fund were immediately shut down and liquidated.

Ideally, we want to purchase shares of a fund when we can acquire them at a price that is less than the net asset value. This is because such a scenario implies that we are purchasing the fund’s assets for less than they are actually worth. That is, unfortunately, not the case with this fund today. As of April 18, 2023 (the most recent date for which data is currently available), the Cohen & Steers Closed-End Opportunity Fund has a net asset value of $10.75 per share but the shares currently trade for $11.05 each. This gives the fund’s shares a 2.79% premium to net asset value at the current price. Generally speaking, it is not a good idea to pay a premium to buy any fund, even though this one has traded for a 2.05% premium on average over the past month. It is probably best to wait a bit here and see if it would be possible to obtain this fund at a better price in the future.

Conclusion

In conclusion, there are certainly a few things to like about the Cohen & Steers Closed-End Opportunity Fund. In particular, the fund has a habit of beating its benchmark index and appears to be very well-diversified across both equity and debt funds. We even see things like precious metals funds in the portfolio to round it off. Unfortunately, there could be some questions about the Cohen & Steers Closed-End Opportunity Fund’s ability to sustain its very attractive distribution and it trades for a very expensive price. Overall, it might be best to sit on the sidelines here unless the Cohen & Steers Closed-End Opportunity Fund declines to a discount price.

For further details see:

FOF: This Attractive CEF Has Nice Features, But Is Substantially Overpriced