BPYPO - Forget Brookfield L.P. Units. Buy The Preferreds For A 56% Yield To Maturity Opportunity

2023-03-12 08:33:53 ET

Summary

- BPY preferred shares present an enticing investment opportunity, boasting a lucrative quarterly dividend yield.

- BPY's financial position and profitability trends are worrisome to common equity holders but not enough to cause alarm over debt repayment and preferred dividend distribution.

- Certain provisions in BPYPO give incentive for BAM/BPY to redeem the $25 par shares next year, opening a 56% yield-to-maturity opportunity.

Brookfield Property Partners ( BPY ) is a real estate investment company that owns, manages, and develops high-quality commercial properties. It is a subsidy of Brookfield Asset Management ( BAM ), the Canadian alternative asset manager who has been investing in real estate for 100 years. BPY's long-term approach to investing and its focus on sustainable, environmentally responsible development practices have helped it build a reputation as a leader in the real estate industry, with over $100 billion in assets that include some of the world's most iconic offices, retail, multi-family, industrial and hospitality properties in North America, Europe, Australia, and Brazil.

From 2013 to 2021, BPY was publicly listed on NASDAQ, while BAM held onto a dominant economic and voting stake in the real estate giant. By taking BPY public, BAM was able to separate its property investments from other business ventures and offer investors a chance to invest solely in real estate assets. Additionally, the decision permitted BPY to acquire external funds without impacting BAM's capital structure while providing BAM with additional revenue as BPY's external manager.

Investor's caution over BPY's complex corporate structure suppressed its share price, and for good reasons. BAM ended up buying BPY at a discount, and since it was the majority owner, minority shareholders didn't have an opportunity to reject the merger.

Note: I use the terms "shareholders" and "Unit Holders" interchangeably in this article, but technically, the correct term is Unit Holders since BPY is registered as a partnership.

There was a Real Estate Investment Trust "REIT" version of BPY called Brookfield Property REIT ( BPYU ). BPYU was created in 2018 due to the merger between Brookfield Property Partners and GGP Inc., a publicly traded real estate company. BPYU and BPY had claims over the same assets. It was also delisted and privatized along with BPY in 2021.

| Ticker |

| Exchange |

| Current Yield |

| ( BPYPP ) |

| NASDAQ |

| 9.70% |

| ( BPYPO ) |

| NASDAQ |

| 9.90% |

| ( BPYPN ) |

| NASDAQ |

| 9.60% |

| ( BPYPM ) |

| TSX |

| 8.99% |

BPY's preferred shares still trade on the NASDAQ and TSX, offering a significant yield opportunity to income-oriented shareholders, with fixed quarterly dividends at attractive rates, priority distribution over Limited Partnership Units held by BAM, and potential for capital appreciation, especially for BPYPO, which matures (at the option of BAM) in March next year, with incentives for BAM to retire the ticker at par of 25% per unit, translating to a potential 56% yield to maturity opportunity in one year.

Can you rely on BAM to pay BPY's debt obligations?

In general, BPY's financial position and profitability trends are worrisome but not enough to cause alarm over debt repayment and preferred dividend distribution. We will examine BPY's financials in a separate section. However, because of investors' interest in the connection between BPY and BAM, specifically, how much BPY creditors (including preferred investors) can depend on the parent company to take on BPY's responsibilities if needed, we will discuss the relationship between BPY and BAM.

First, it is important to note that BPY operates as a separate legal entity from BAM. This means that BAM is not responsible for the debt and liabilities of BPY, including BPY. As a subsidy of BAM, the bankruptcy of BPY would likely have an impact on its parent company, but the extent of this impact would depend on a variety of factors.

However, as the sole owner of BPY and the parent company, BAM would still be affected by the bankruptcy of BPY. Interest payments and preferred dividends have seniority over Partnership Units' dividend distribution to BAM. Thus, a default would practically mean the loss of a valuable source of income, currently standing at $400 million annually. Another potential impact is the loss of its investment in BPY, which will likely have a significant impact on the overall value of BAM shares. BAM is the sole owner of BPY and a significant investor in its preferred. A default could lead to a disruption of BAM's operations, which could have a ripple effect not only on BAM via a complicated organizational structure.

The reputational damage of the bankruptcy of BPY on BAM would likely depend on the circumstances surrounding the bankruptcy and how the public and investors perceive it. If the bankruptcy is seen as a result of mismanagement or poor decision-making by BAM, it could lead to a significant loss of trust and confidence in the company. This could negatively impact the company's ability to attract and retain investors, partners, and employees.

On the other hand, if the bankruptcy is seen as a result of external factors such as economic conditions or unforeseeable events, the impact on BAM's reputation may be less severe. The company's history of successful investments in real estate and other asset classes and its reputation are based on its overall performance and track record over time. As such, while a bankruptcy of BPY would likely have some reputational impact on BAM, it is unlikely to be a catastrophic event for the company as a whole.

Nonetheless, it is worth noting that BAM and BPY have a strong track record of managing economic downturns and financial crises. When liquidity dried up for many financial institutions during the great recession, BAM raised capital and acquired assets. The company has a diversified portfolio of assets and a history of investing for the long term, which may help mitigate the impact of the potential bankruptcy of BPY.

Challenging Economic and Industry Environment

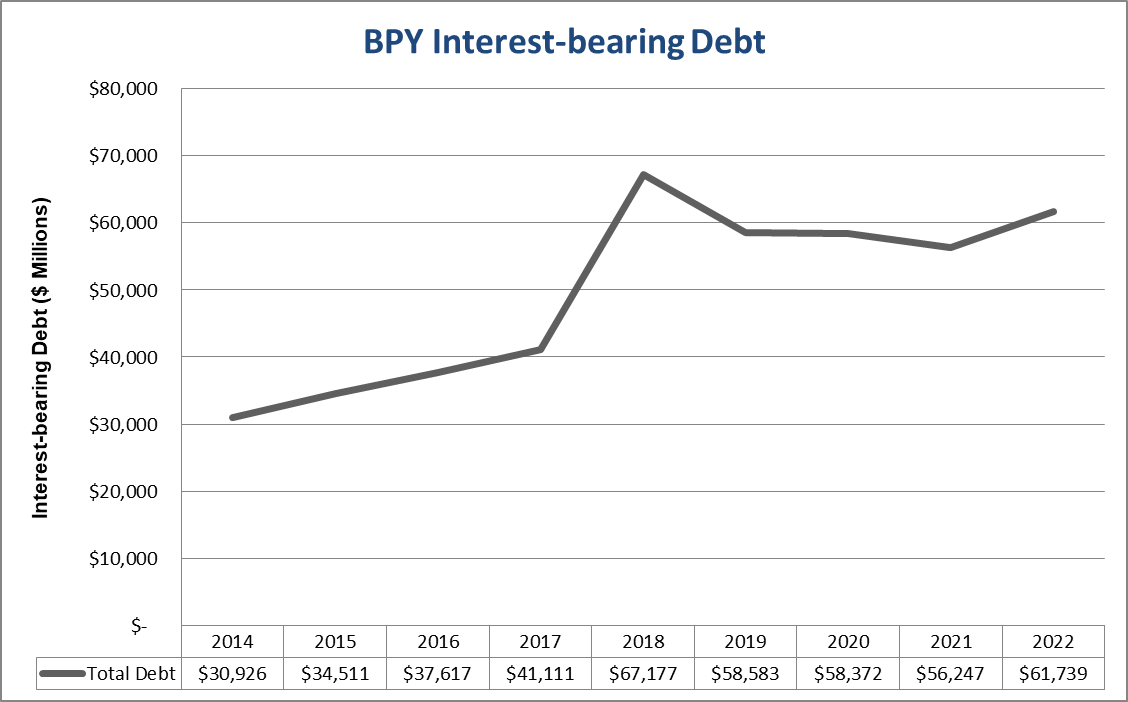

Overall, BPY's financial performance has been somewhat variable in recent years due in part to the impact of the COVID-19 pandemic on the commercial real estate market, exacerbating concerns over macro-trends manifested in increasing share of E-commerce, disrupting the traditional retail sector, as consumers increasingly shop online instead of in physical stores. This, combined with high leverage and rising interest rates, is promoting fears of a disaster, and the debate now is whether BAM will come to the rescue in the worst-case scenario. It is not uncommon for leveraged real estate companies to experience financial distress.

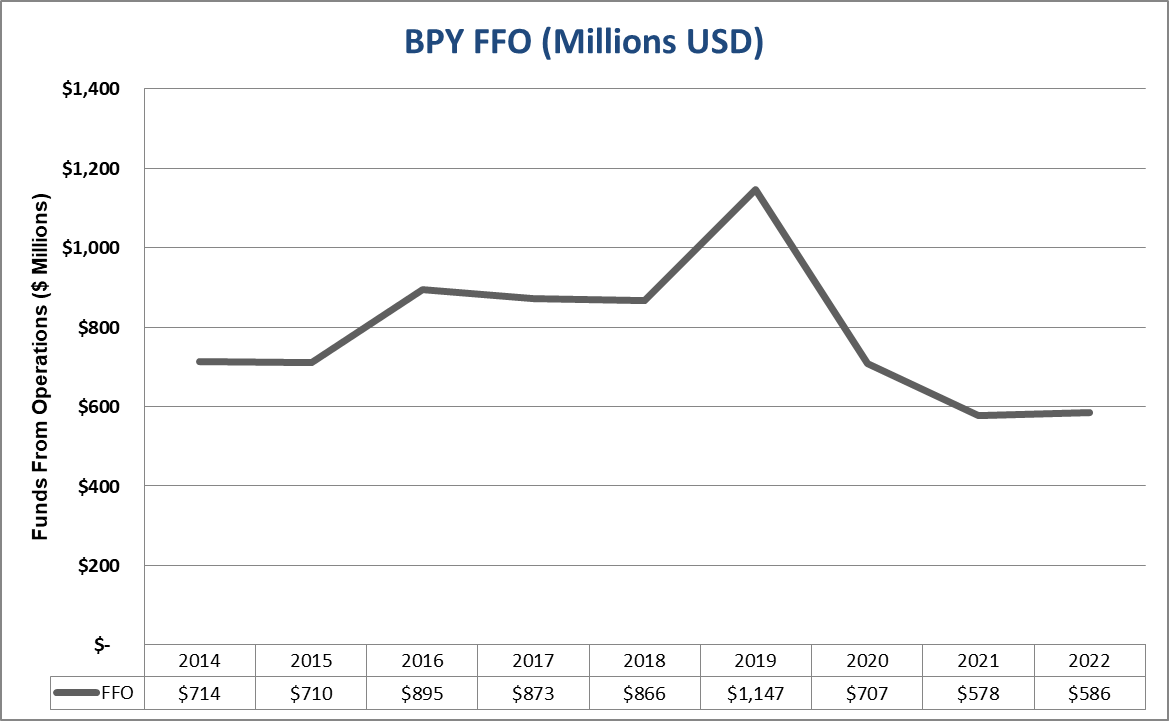

BPY reports its financial performance using a metric known as funds from operations "FFO," which is a widely used measure of the cash flow generated by a real estate company. FFO is calculated by adding depreciation and amortization expenses and subtracting asset mark-ups and gains from property sales to net income. As shown below, BPY's FFO peaked in 2019 and has declined in the past few years. Last year, management cited increasing pressure from rising interest rates.

Author's estimates based on BPY filings

{kind=link}

Last year, management cited increasing pressure from rising interest rates, as a significant portion of its obligations is tied to variable rate notes.

Author's estimates based on BPY filings

{kind=link}

Should preferred equity shareholders be concerned? Well, the price of preferred depends on the credit score of BPY, which is influenced by its profitability. However, the FFO, which is currently around the $600 million mark (net of interest expense), is more than enough to cover preferred dividend obligations, which stand at $44 million. Preferred distribution has seniority over Partnership Units distribution, which are approximately 10x the preferred, a sizable cushion demonstrating high interest and preferred dividend coverage.

BPYPO, BPYPN, and BPYPP are perpetual preferred, and redemption is at the discretion of BAM and BPY at $25 per share. While reading the preferred prospectus, I stumbled on an interesting provision:

In the case of certain change of control events following which our non-voting limited partnership units ("L.P. Units") and/or the Series 2 Preferred Units are not publicly listed, we may, at our option, redeem the Series 2 Preferred Units or increase the distribution rate per annum by 5.00%, as described under Description of the Offered Securities. BPYPO Prospectus found on BPY Website

The provision indicates that if a "change of control event" occurs, which typically refers to a significant change in the ownership of the company, and the L.P units or the preferred units are no longer publicly listed, the company has the option to either redeem the preferred units or increase the distribution by 5% per annum. This means that the company may choose to either buy back the preferred at a redemption price of $25 per share or pay a higher annual distribution rate to the holders of these units to compensate for the change in the company's ownership of listing status. The maturity date of BPYPO is March 2024. Thus, if I understand correctly, the provisions of the offering give a significant incentive for BAM/BPY to retire the preferred next year at a redemption price of $25 per share. BPYPO currently trades at $15 per share, which translates to 56% Yield to Maturity if BAM/BPY retires the preferred next year.

Summary

The price of BPY's preferred has declined significantly in the past few months, driven by a challenging macro environment. Hawkish Fed policy and rising interest rates increased BPY's operational expense, exacerbated by robust leverage and indebtedness. Moreover, allowed investors to seek other income investment opportunities.

Declining profitability and incremental decline in occupancy rates in its office buildings raised concerns over broader industry trends manifested in an increased share of E-commerce and remote working, which have an impact on demand for traditional retail commercial real estate and office properties. However, I believe that the demand for up-scale commercial property will withstand these trends. BPY holds some of the most iconic buildings in the world, and sales per square foot show an upward trend, thanks to an active management strategy focused on upscale and luxury products tenants attracting affluent customers where online buying is not feasible.

The FFO generated by BPY towers over its preferred distributions, offering a sizable safety cushion. While BAM and BPY are separate entities, BAM has a significant economic interest in BPY. Given the seniority of preferred disruption over common equity payments, investors in BPYPO, BPYPP, and BPYPN will always receive dividends before BAM gets a penny.

For further details see:

Forget Brookfield L.P. Units. Buy The Preferreds For A 56% Yield To Maturity Opportunity