CBL - Former Bankrupt Mall REIT CBL & Associates Properties Is Still Struggling

2023-12-06 15:11:38 ET

Summary

- CBL's latest 3Q results were mediocre, with some metrics improving, but others were very disappointing.

- CBL exited Ch.11 bankruptcy with an irrational reorganization plan.

- Too many of their retail store tenants face a bleak future.

CBL & Associates Properties (CBL) owns mediocre malls, still has the same mediocre management, and has too much debt relative to the quality of their assets. They exited Ch.11 bankruptcy in November 2021 under an irrational reorganization plan. Since I question the long-term viability of CBL I would not be a buyer of this REIT.

2020 Ch.11 Bankruptcy

When looking at CBL & Associates Properties you need to start by looking at their 2020-21 Ch.11 bankruptcy case. I wrote a number of articles on CBL during their bankruptcy process, and I thought I would wait a few years before I wrote another article to give them time to "get their act together" before writing a follow-up article.

Their bankruptcy reorganization plan was irrational and should not have been confirmed by the court, in my opinion. While they did reduce their debt, they exited bankruptcy with too much debt. Creditors should not have received $455 million 10% secured notes as part of their recovery. CBL did not raise $455 million in new cash from these notes - the notes were just given to the creditors as part of their recovery for their claims. The reality is that the notes were given so that the various claim classes would vote to accept the plan that "gifted" new equity to both preferred shareholders and common equity holders. Creditors should have received 100% of the new equity instead of 89% and they should have not been given any notes, in my opinion. [Note: the remaining 10% secured notes were redeemed in May 2022 with funds from a new non-recourse secured loan that is half fixed rate (6.95%) and half variable rate (9.43% 3Q'23)]

The value of the total new equity would increase, in theory, by $455 million without the issuance of $455 million debt without receiving cash for that debt. (Actually, it is not an exact 1 to 1 value because it would be adjusted based on the capital structure optimization factor, but that is beyond the scope of this article.) Therefore, by giving creditors new debt for their claims the result was just increased debt/leverage for the new CBL and not really an increase in the value of their recovery package.

This plan annoyed many unsecured noteholders who received less than full recovery while at the same time, lower priority classes received a recovery. Some preferred shareholders, who received 0.043912176 of a share of new CBL per preferred share, were annoyed because common equity shareholders received a recovery of 0.005457723 of a new share of CBL stock per old CBL despite the fact the preferred shareholders did not receive a full recovery for their claims. (I covered this issue in detail in prior articles.)

One piece of evidence that supports my assertion that they exited bankruptcy with too much debt is a statement contained in their 10-K that was filed on March 31, 2022, only a few months after they exited bankruptcy: "We currently do not have sufficient liquidity to meet these obligations as they become due, which raises substantial doubt about our ability to continue as a going concern." What? They just exited bankruptcy a few months before the 10-K filing and they already included a "going concern" warning. The stated remedy was "management intends to refinance and/or extend the maturity dates for such mortgage notes payable."

This "going concern" statement was also troubling because in order for a bankruptcy plan to be confirmed by the court under section 1129(a)(11) the "confirmation of the plan is not likely to be followed by the liquidation, or the need for further financial reorganization, of the debtor or any successor to the debtor under the plan..." These maturity issues should have been addressed during the Ch.11 process even if the mortgages were not directly part of the bankruptcy. While they were eventually able to deal with this "going concern" issue, this is just another example of poor CBL management who did not "clean-up" all these issues prior to exiting bankruptcy. Basically, the same management, the Lebovitz family, that drove CBL into bankruptcy still runs this REIT.

Retail Tenants

One of the first items many mall REIT investors look at is the list of their major retail tenants to help determine the quality of the mall and the potential lease rejections/defaults by struggling retailers who might file for Ch.11 bankruptcy in the near future. CBL has mostly the typical middle-market mall retailers - nothing upscale like Gucci or Prada.

Top 25 Tenants 2022 Based on Revenue

{kind=link}

It is interesting to note that two major anchor tenants did not make the top 25 tenant list based on revenue. There are 17 JC Penney store leases (CBL-owned stores) with 1,828,329 sq. ft. and eight Macy's ( M ) store leases with 905,442 sq. ft. I am not sure if the seven Bed Bath & Beyond closed stores (189,770 sq. ft.) have new tenants yet. (I am assuming that some of the $3.147 million uncollectable revenue at the end of 3Q was related to BBBY.)

There are a few retailers on their top 25 list, such as Express ( EXPR ) (30 stores/246,437 sq. ft.), and I have serious concerns that they will be in bankruptcy within the next year or two. If the economy weakens over the next few quarters, I also worry about JC Penney. (Note: for those interested in following the liquidation process of retail stores you should follow Copper Property CTL Pass Through Trust (CPPTL), which is the trust that is liquidating many former JC Penney stores.)

B and C Malls

I have been in many of CBL's malls, and it seems in order to maintain cash flow they have been controlling costs by controlling the amount of maintenance labor expense. In B and C malls I guess consumers tolerate these minor maintenance problems, but the malls are not welcoming and too often do not offer an enjoyable experience. To compete with e-commerce, malls need to be really an enjoyable experience - they are not.

There are frequent assertions that these malls and their associated parking lots/parcels might be able to be sold or partially sold for new developments as the mall's usefulness ends. That is often easier stated than accomplished. In some cases, any needed zoning changes or exemptions are just rubber-stamped by local governments, but too often there is local opposition that delays or even kills these proposals. For example, Pennsylvania Real Estate Investment Trust (PRET), which is currently trading at $0.015 after adjusting for a reverse stock split, had a number of proposals that met major local opposition that significantly impacted this mall REIT. In one case they wanted to build an apartment building on their property but there was major opposition based partially on the expected increase in sewage use would put strain on their existing nearby sewer lines.

Some of CBL's malls seem to be transitioning to entertainment centers instead of traditional retail shopping malls as restaurant/bar, gaming, and health club leases continue to increase. The problem for the remaining retailers is that those going to the mall to work at a gym or drink at a bar may not be wearing their "shopping hat" - their purpose for going is very different than the foot traffic that is going shopping. You may have a high level of foot traffic, but not shopper foot traffic in the mall. They are also taking up parking spaces that may make it more inconvenient for actual shoppers.

A Look at One Mall - Brookfield Square

In order for investors to get a better "feel" for their specific properties I want to focus on one of their malls - Brookfield Square, which CBL acquired in 2001. This mall was built in the mid-1960s in a suburb of Milwaukee and was one of the first fully enclosed malls built in Wisconsin. The Brookfield/Elm Grove market area in the 1960s was mostly single-family residences with an upper-level management/professional head of household. The comfortable homes had little or no mortgages. When the mall opened it had Sears, JC Penney, Boston Store, and T.A. Chapman's as anchor tenants. There was very little other commercial real estate in this rapidly growing suburban area.

Over the last 55 years, the market area has dramatically changed. The residences now often have two heads of household working at mid to low level management/blue collar jobs with large mortgages. This demographic change means less discretionary income per capita can be spent at Brookfield Square stores. The population for Brookfield/Elm Grove grew very little from 2000 to 2020 (51,280 to 54,485). The population of Milwaukee is indicative of the rust belt decline - went from 741,099 in 1960 to 577,222 in 2020.

Brookfield Square now only has JC Penney left as a major anchor tenant. There are many other retail stores that have been built over the years near the mall that compete for foot traffic. The entire area has been grossly over-built and there are a large number of retail store spaces available to lease. The poor Brookfield Square $242 sales per square foot and 79% leased metric in 2022 reflects these problems. To add insult, the variable interest rate on the Brookfield Square secured recourse loan was 8.23% for 3Q 2023.

Recent Results

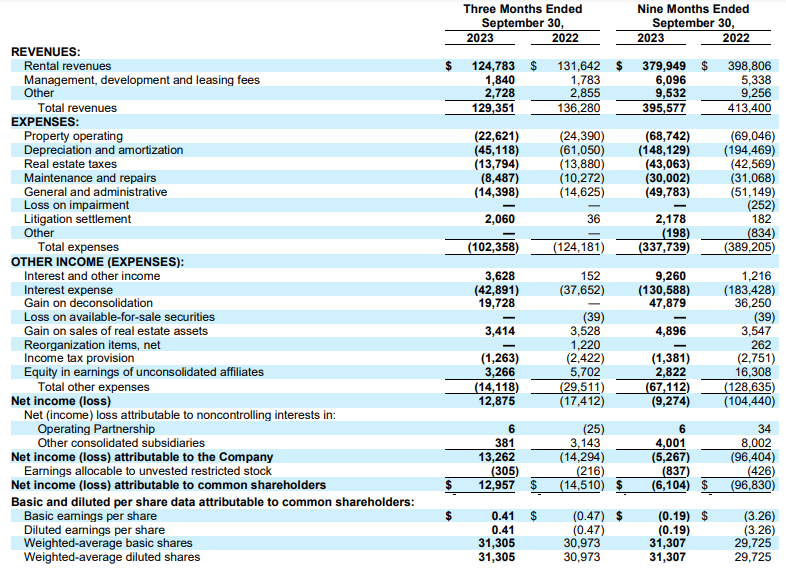

Before looking at the 3Q results it is important for investors to remember that CBL used "fresh start" accounting after they exited Ch.11 in early November 2021, which impacted some 2022 numbers.

3Q and Nine Months Income Statement 2023 and 2022

{kind=link}

CBL's stock price has increased significantly over the last few weeks mostly because interest rates have dropped (10-year UST yields dropped 80 basis points over the last six weeks) and not because of some specific improvement for this REIT. Their 3Q results were mediocre. A few metrics improved, such as the total portfolio occupancy rate increased by 30 basis points to 90.8% and FFO per share increased to $1.93 from $1.55 in 3Q '22. Some other metrics, however, moved in the wrong direction. Same-center NOI only increased 0.4% from 3Q '22, which is less than the 3.7% inflation rate. Adjusted FFO decreased to $1.60 from $1.85. The metric that really caught my eye was that the average gross rent per sq. ft. declined 4.0% in 3Q. This was very disappointing considering this was a bright spot in 2Q23 when it increased an impressive 9.1%.

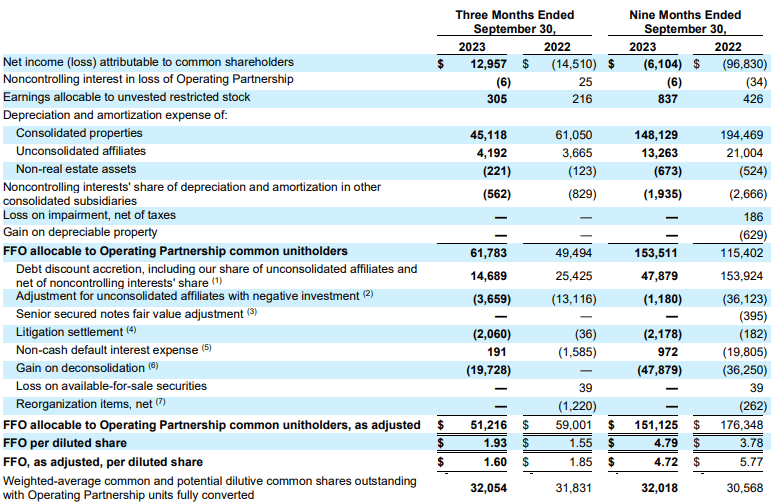

FFO and Adjusted FFO

{kind=link}

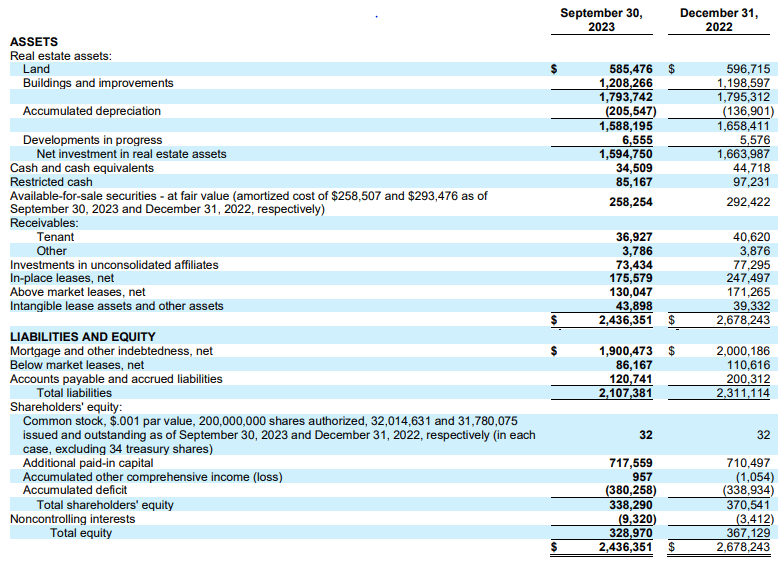

The balance sheet below is for the end of 3Q, but as of November 2, the secured term loan is now non-recourse. There is another metric that I find troubling and that is the total debt of $1,900 million minus total cash/securities ($34.5 million + $85.2 million + $258.2 million)/ net investment real estate assets of $1,595 million = 95.5%. Historically many real estate assets have a market value significantly higher than their GAAP balance sheet numbers, but in some parts of the country, such as the rust belt that is not always the case. I assume many REIT investors seeking higher income are comfortable with high GAAP accounting balance sheet leverage, but I am not. I also think it was irrational for management to approve the new $25 million share repurchase program, especially since they only have a 'B' issuer credit rating by S&P. As many readers already know, I am absolutely against share repurchases. The cash should be used to reduce debt or be paid as a dividend. Many REIT investors are seeking dividend income holding a REIT and are not stock traders.

3Q and Nine Months Balance Sheet 2023 and 2022

{kind=link}

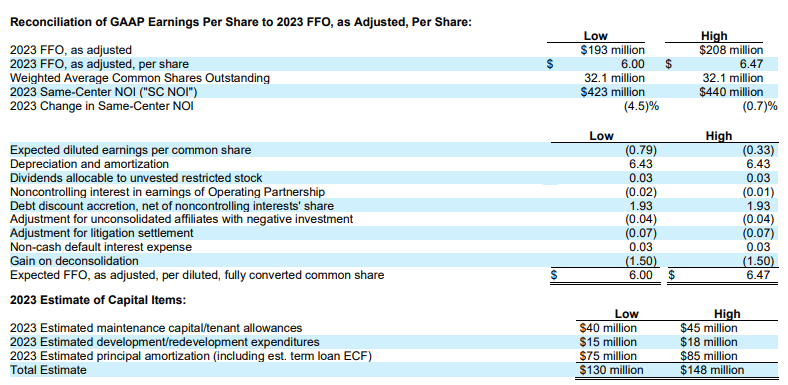

Management 2023 Guidance

{kind=link}

Why I am Not Recommending CBL

My negative opinion of CBL is based mostly on its long-term outlook. While CBL stock price might increase modestly if interest rates continue to decline, especially since much of their debt has variable interest rates, there are other better investments with brighter long-term outlooks that will also benefit near-term by lower interest rates. Their current dividend yield of 6.28% is not that impressive relative to UST note yields.

CBL has too many major retail tenants with questionable futures. If you buy a mall REIT you are effectively buying a portfolio of retailers who are their tenants, and too many of their retail tenants I consider "sells", such as Express. At this point, I rate CBL a hold, but investors should consider selling into any future strong rally from interest rate cuts.

For further details see:

Former Bankrupt Mall REIT CBL & Associates Properties Is Still Struggling