FORM - FormFactor: Disappointing Q1 Results Value Erosion Risk

2023-05-27 00:40:57 ET

Summary

- Lower revenue in Q1 2023 with broken promises.

- Here at the Lab, probe players will benefit from a secular megatrend growth.

- Technoprobe is gaining market share and is still trading at a discount compared to FormFactor.

Here at the Lab, in 2022, we already provided a comps analysis on two leading companies in the probe sector Technoprobe S.p.A. (THNBY) our Clear Winner, and FormFactor (FORM). After having analyzed the Q1 results and 2023 expectations, we believe that FormFactor is currently overvalued. Before going deeper into the analysis, it is important to report our latest publications on Infineon Technologies AG and STM . Both companies report a solid order backlog and in the last weeks, chip manufacturers' stocks were all up thanks to the good indications coming from their latest press release. What surprised the most the Wall Street investor community was the Micron president and CEO's words . In detail, he explained his confidence about the long-term earnings trend and predicted that the memory chip industry will see a record year in 2025 in terms of market size thanks mainly to artificial intelligence. At the same time, inventories are improving and the top manager expects gradual improvements in the balance between supply and demand within the sector. This announcement was also backed by the German Infineon higher 2023 guidance . Probe cards are going to play into the AI words. Nvidia's data center's strong performance is powered by semis (and the semiconductor needs to be verified before commercialization).

Potential downside

Aside from the financials comps analysis that we will present later on, there is a negative consideration to report. The Biden administration released a sweeping set of export controls to limit Chinese semiconductor chips. These rules are set to limit the Chinese supercomputing systems development and represent the biggest shift in US policy toward technology exports to China since the 1990s. This policy could hamper China's chip-making industry; however, these restrictions will hit US companies that are providing direct or indirect support to Chinese enterprises involved in advanced semiconductor production. In detail, the export will be prohibited for the Logic family components with semis production nodes below 16 nanometers or memories with production nodes below 18 nanometers. Other machinery parts used in the semis production process will also be prohibited. High-end probe cards are mainly used for tests on wafers connected to semis production, and here at the Lab, we believe that FormFactor might be hit (and the latest sales data might already support this thesis). On the other hand, Technoprobe might take advantage of this momentum and we are not surprised to see that is already increasing its market share penetration.

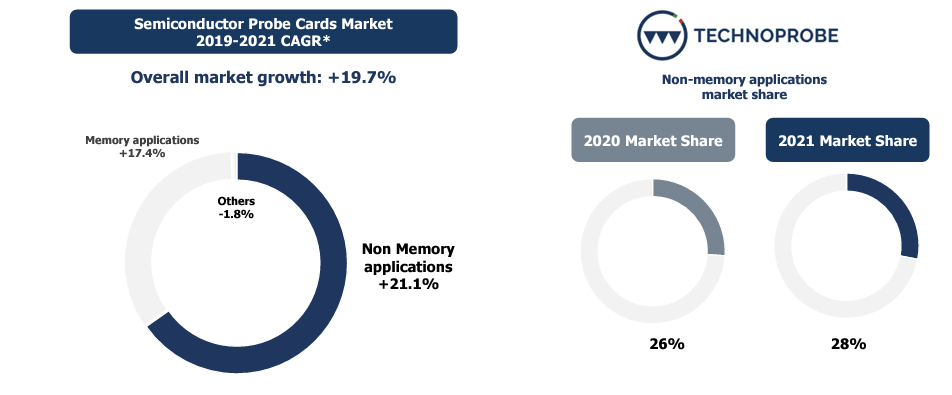

Technoprobe higher market share

{kind=link}

Aside from the US restrictive regulation, for the sixth consecutive year, Technoprobe was the best-rated supplier in the tech satisfaction survey and was ahead of FormFacto r.

Technoprobe survey

Q1 results

This second part follows our previous publication titled: " the story continued - Part 1 ". Below are the main takes from FormFactor's latest financial.

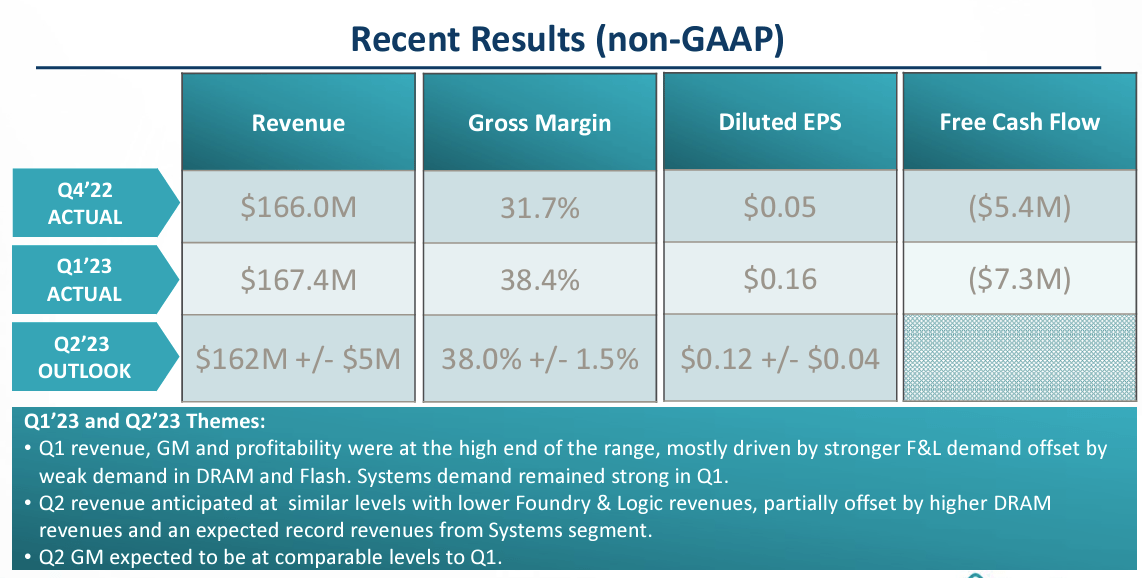

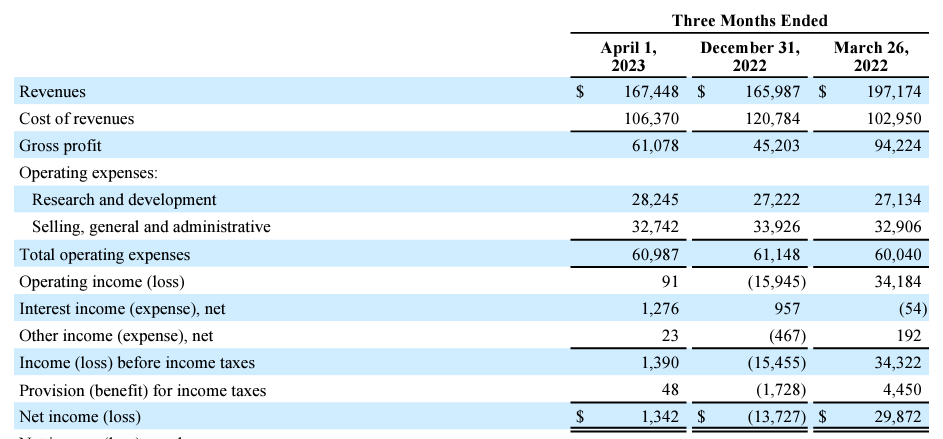

- In 2022, Technoprobe sales reached €549 million and were up by 40%, while FormFactor decreased its top-line sales by 2.8%, and in Q4, turnover further decelerated signing a minus of 19%. This negative trend was also confirmed in Q1, FormFactor revenue decreased by an additional 15%. Going down to FormFactor P&L analysis, both gross margin and EBITDA were cut. Q1 net income significantly declined and reached only $1.3 million;

- Related to point 1), FormFactor announced that they " delivered revenue above the outlook range against a challenging industry environment ". This is true; however, they were not able to lower their operating expenses and their core margin further declined;

- Similar negative results were performed in the net cash flow from operating activities. In detail, net cash flow was at $12.3 million compared to the $44.2 million achieved in the same quarter last year;

- In Q1, key to note is their respective Net Cash position, Technoprobe reached a net position of €404 million. At the current market cap, the cash position represents 10% of the company's value while FormFactor's cash position stood at $235 million;

- In Q4, FormFactor forecasted a significant gross marg in improvement and " a return to typical excess and obsolete inventory costs ". This was not in line with Q1 results.

{kind=link}

Fig 1

{kind=link}

Fig 2

Conclusion and valuation

Our internal team is confident that both Technoprobe and FormFactor are secular winners due to the positive semiconductor momentum. These positive trends are: 1) more everyday life electronics 2) more technology in our electronics (let's think about electric toothbrushes with pressure sensors) 3) 5G network developments , 4) data centers, 5) more semis in the automotive industry both in BEV and ICE productions, 6) industry 4.0 and smart cities, and 7) AI. It is key to recall that new semis are more powerful and smaller and this increased probe card uses. As already mentioned, testing will always be needed and this will support FormFactor's valuation. However, looking at the numbers, FormFactor is trading at a higher multiple on an EV/EBITDA adjusted basis compared to its closest peers. In detail, our American player is currently trading at 16.4x with a 2024 estimated at almost 20x. Technoprobe is at 15.98x and this higher discrepancy is also recorded at the price-earning level (FormFactor at >30x vs Technoprobe at <25x). US new regulation could trim FormFactor export sales, and Technoprobe, with also more cash for M&A optionality, should at least deserve a premium valuation. For this reason, we believe that FormFactor should be traded at a price-earnings ratio of no more than 19x, and with an implied 2023 EPS of $1.25, we arrive at a valuation of $23.75 per share. Therefore, we decided to decrease our rating to a sell.

For further details see:

FormFactor: Disappointing Q1 Results, Value Erosion Risk