DTM - FPL: Impending Merger Creates Opportunity For Significant Gains (Rating Upgrade)

2024-01-17 06:56:37 ET

Summary

- The First Trust New Opportunities MLP & Energy Fund provides a way for retirees and savers to invest in master limited partnerships and midstream infrastructure companies.

- FPL has a yield of 6.47%, higher than some energy infrastructure corporations and the S&P 500 Index. It is, unfortunately, lower than what peer funds possess.

- The fund's performance has been strong, outperforming the Alerian MLP Index and delivering better returns even after distributions are included.

- FPL has been targeted for conversion into an ETF structure during the second quarter. That event will result in capital gains for shareholders.

- The fund is still trading at an attractive discount on NAV and is covering its distribution.

The First Trust New Opportunities MLP & Energy Fund ( FPL ) is a closed-end fund that provides an easy way for investors to add master limited partnerships and other midstream infrastructure companies to their tax-advantaged accounts. This has long been a problem for retirees, as the generally stable cash flows and high yields possessed by most master limited partnerships make them a great vehicle for generating income in retirement, but tax laws have made it very difficult to include these vehicles in most retirement accounts. This fund provides an easy way around that problem because it handles all of the tax problems on the fund level while still distributing most of the income produced by the partnerships in the portfolio. As most master limited partnerships have very high distribution yields, we can expect that this fund will as well. Indeed, the First Trust New Opportunities MLP & Energy Fund boasts a 6.47% yield at the current price, which is not nearly as attractive as many partnerships, but it is still higher than some energy infrastructure corporations possess, and it is substantially higher than the S&P 500 Index ( SP500 ).

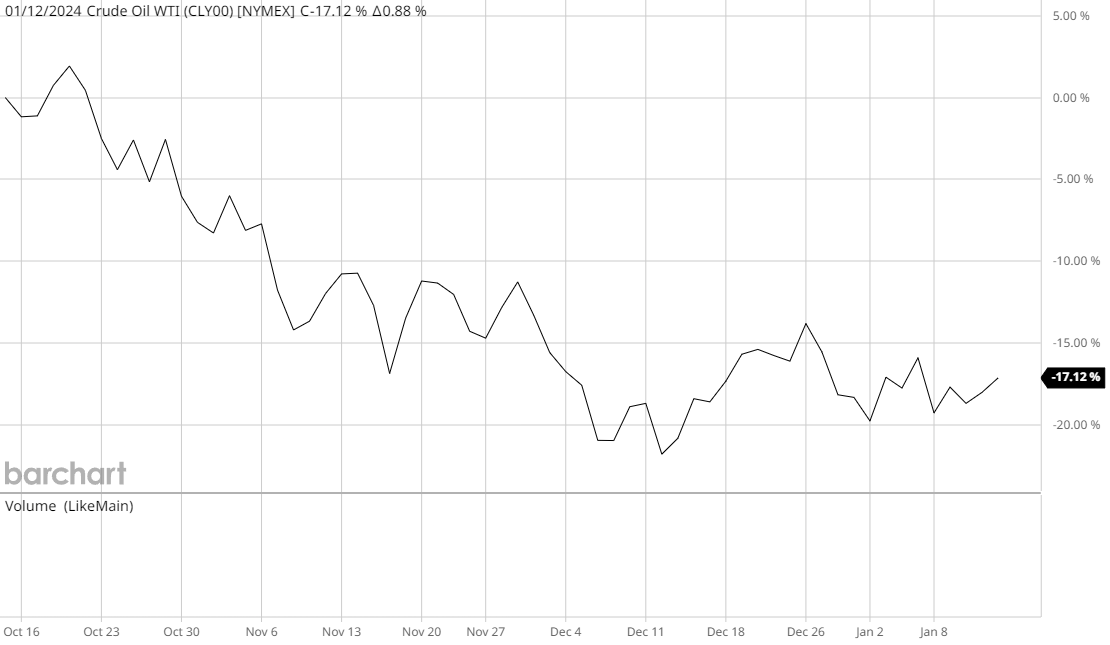

As subscribers can likely remember, we previously discussed the First Trust New Opportunities MLP & Energy Fund in late October 2023. That was right around the time that the market was shifting into the bull market run that it engaged in during the final two months or so of last year. That bull run did not benefit energy stocks nearly as much as companies in other sectors though, and indeed the spot price of West Texas Intermediate crude oil is actually down 17.12% over the past three months:

{kind=link}

This is one of the reasons why the headline inflation numbers came in weaker than the average person notices in their daily lives. For example, both shelter and services showed fairly large year-over-year increases in the most recent inflation report.

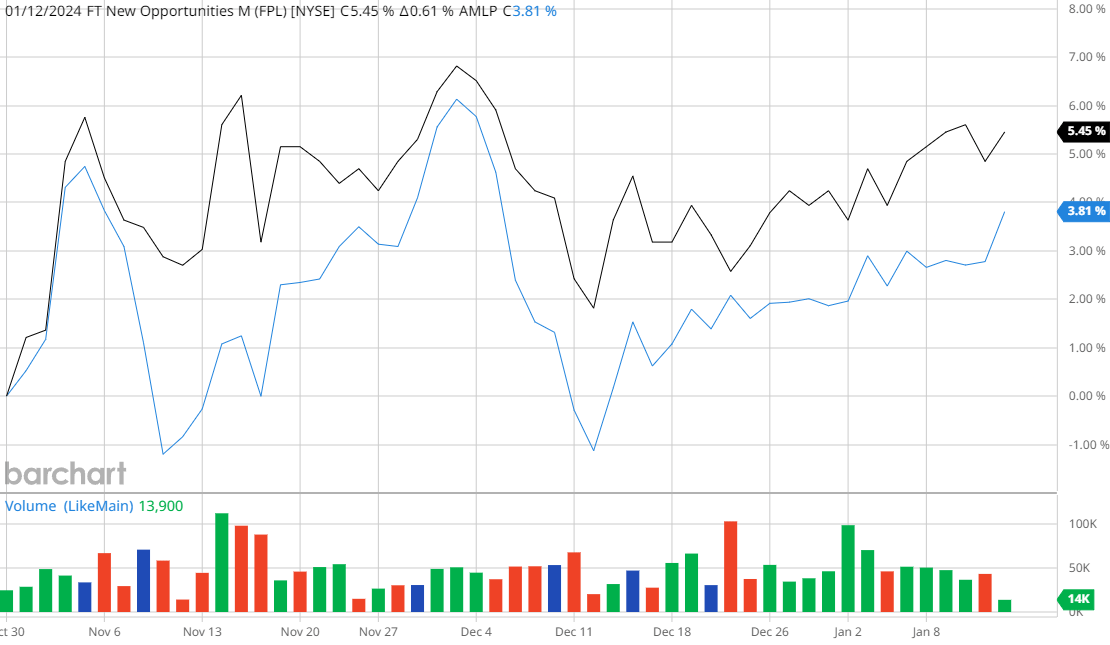

Fortunately, midstream companies have proven to be somewhat resistant to the decline in energy prices. We can see this in the fact that the share price of the First Trust New Opportunities MLP & Energy Fund is actually up 5.45% since the last time that we discussed the fund. This is better than the 3.81% gain that the Alerian MLP Index ( AMLP ) delivered over the same period:

{kind=link}

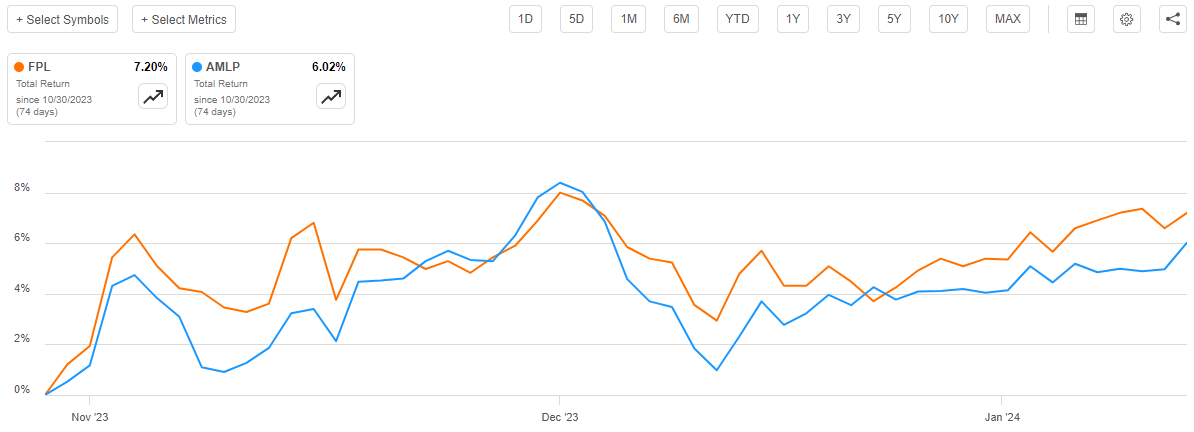

The First Trust New Opportunities MLP & Energy Fund actually managed to deliver a better performance than the index even once the distributions are included, despite the fact that the index actually has a higher yield:

{kind=link}

This certainly seems to be quite surprising when we consider that midstream master limited partnerships usually deliver a market performance that correlates with energy prices, even though their cash flows are not really affected by short-term changes in energy prices. It is possible that the strong performance here is being driven by yield-chasing, as the market's current expectations that the Federal Reserve will substantially cut interest rates despite the fact that inflation remains very persistent has revived the "cash is trash" mantra that heavily influenced the markets during most of the 21st century. In such an environment, it is obviously better to own pretty much any asset than cash.

There could be another factor driving the performance of this fund specifically, however. This is that First Trust announced that it will be merging this fund with its other energy infrastructure funds and converting them into an exchange-traded fund. This move would erase the double-digit discount that has long plagued this fund and present investors with the opportunity to earn some significant gains. For this reason, I am upgrading this fund to a strong buy rating today.

About The Fund

According to the fund's webpage , the First Trust New Opportunities MLP & Energy Fund has the primary objective of providing its investors with a high level of total return. As is usually the case with First Trust funds, the website provides a very detailed description of the fund's objectives and strategy:

First Trust New Opportunities MLP & Energy Fund is a non-diversified, closed-end management investment company. The Fund's investment objective is to seek a high level of total return with an emphasis on current distributions paid to common shareholders. The Fund seeks to provide its common shareholders with a vehicle to invest in a portfolio of cash-generating securities, with a focus on investing in publicly traded master limited partnerships, MLP-related entities and other companies in the energy sector and energy utility industries that are weighted towards non-cyclical, fee-for-service revenues. Under normal market conditions, the Fund will invest at least 85% of its managed assets in equity and debt securities of MLPs, MLP-related entities and other energy sector and energy utilities companies that the Fund's Sub-Adviser believes offer opportunities for growth and income.

This description explicitly states that the fund invests in a combination of both equity and debt securities that are issued by companies in its target industries, which are primarily midstream companies and utilities. However, right now the fund is entirely invested in common equities, although it does have a small amount of cash on hand:

CEF Connect

As such, the fund's focus on total return certainly seems appropriate. After all, common equities are by their very nature total return vehicles. Investors purchase the common equity issued by a company in order to receive an income in the form of distributions and dividends as well as benefit from the capital gains that should accompany the growth and prosperity of the issuing company. This combination of direct payments and capital gains is the very definition of total return.

With that said master limited partnerships tend to deliver the majority of their total returns in the form of direct payments to their unitholders. This is mostly due to the fact that these companies tend to have fairly low growth rates, so the market is unlikely to reward them with especially high earnings multiples. In addition, tax laws incentivize master limited partnerships to pay out a substantial proportion of their cash flow to their investors in the form of distributions. That makes it quite difficult for them to reinvest capital in their own businesses, although ever since the energy bear markets of 2015 and 2020 a growing number of partnerships are opting to retain some of their capital to finance their growth projects internally. Finally, the market in general has been unfriendly to fossil fuel companies over the past decade so it increasingly makes sense for these companies to pay out a lot of money to their shareholders in order to provide some sort of investment return. These reasons are why the Alerian MLP Index has consistently had a higher yield than even the domestic preferred stock and bond indices over most of the past decade. This remains true today as the index yields 8.12% at the current level.

Naturally, there are some master limited partnerships that yield significantly higher levels than the market index. Energy Transfer ( ET ), for example, has an 8.92% yield today. MPLX ( MPLX ) also has historically boasted a yield that is higher than the index, as its 9.10% current yield is one of the highest in the industry. Naturally, the First Trust New Opportunities MLP & Energy Fund does not invest only in those companies with a yield that is higher than the market index. It also includes a number of companies that the Alerian MLP Index does not, such as midstream corporations. Here are the largest holdings in the fund as of the time of writing:

First Trust

Here are the current yields of each of these companies:

| Company |

| Current Yield |

| Enterprise Products Partners ( EPD ) |

| 7.63% |

| Energy Transfer |

| 8.92% |

| Cheniere Energy Partners ( CQP ) |

| 5.90% |

| The Williams Companies ( WMB ) |

| 5.13% |

| MPLX |

| 9.10% |

| ONEOK ( OKE ) |

| 5.41% |

| Plains All American Pipeline ( PAA ) |

| 8.05% |

| Kinder Morgan ( KMI ) |

| 6.29% |

| DT Midstream ( DTM ) |

| 5.08% |

| Hess Midstream ( HESM ) |

| 7.66% |

As expected, the distribution and dividend yields here both beat and come in under the yield of the Alerian MLP Index. However, all of these companies substantially beat the 1.39% yield that is offered by the SPDR S&P 500 ETF Trust ( SPY ). These companies are also generally offering higher yields than most money-market funds as well as the ten-year U.S. Treasury. This therefore supports the argument that midstream companies are generally an attractive sector for investors who are seeking to earn a high level of income from the assets in their portfolios. We also notice that the master limited partnerships have substantially higher yields than the companies that are structured as corporations. This is also to be expected due to the fact that the partnerships do not have to pay taxes on a corporate level.

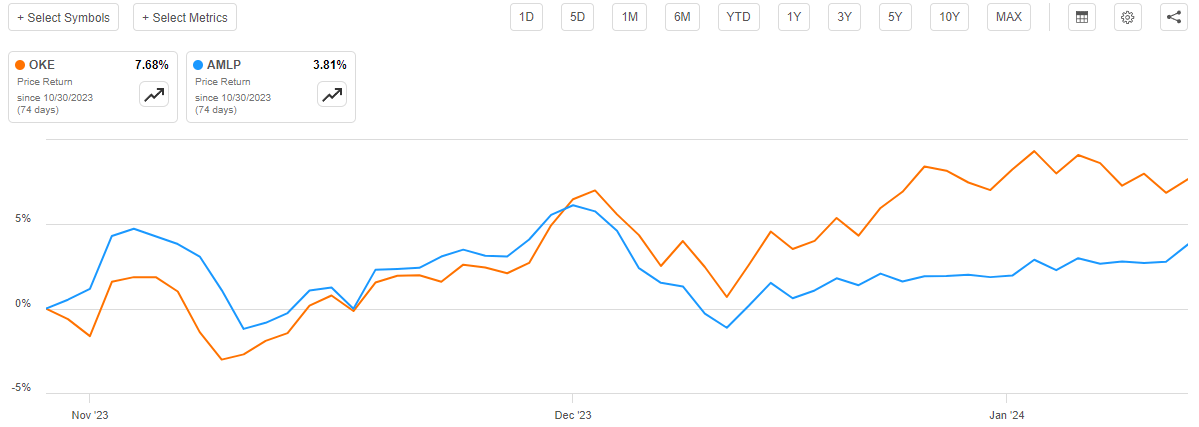

For the most part, the largest positions of the fund are the same as the last time that we discussed it. However, the weightings of a few companies have changed significantly. In particular, the fund's allocation to ONEOK has decreased from 6.43% of its assets at the end of September to 5.09% of assets today. This has boosted the weightings assigned to a few other companies by default. It is unclear what the cause of this decision was, particularly since ONEOK has outperformed the Alerian MLP Index since the last time that we discussed the fund:

{kind=link}

It is possible that there was something about ONEOK's acquisition of Magellan Midstream Partners that the fund's management did not particularly like. Indeed, I too thought that ONEOK was better off before the merger as its pure natural gas focus was somewhat better for growth than the company's prospects with Magellan's slower-growth liquids business attached to it. As the stock has been outperforming though, it seems highly unlikely that the reduction in the weighting that we see over the intervening period was caused by the other assets in the fund outperforming ONEOK. Rather, the fund's management intended to sell off some of its position. An asset sale like this is a fairly rare event, as the fund's 33.00% annual turnover is very low for an equity closed-end fund as well as being a bit lower than First Trust's other energy infrastructure closed-end funds.

ETF Conversion: The Reason For The Rating Upgrade

In the introduction to this article, I mentioned that First Trust has the intention of merging the First Trust New Opportunities MLP & Energy Fund with its other energy infrastructure closed-end funds and then converting the combined fund into an exchange-traded structure. The fund manager discussed this in a late October press release :

First Trust Advisors, L.P. announced today that the Board of Trustees of each of First Trust Energy Income and Growth Fund ( FEN ), First Trust MLP and Energy Income Fund ( FEI ), First Trust New Opportunities MLP & Energy Fund, and First Trust Energy Infrastructure Fund ( FIF ), each a closed-end management investment company managed by FTA and sub-advised by Energy Income Partners, LLC, approved the Merger of each respective Target Fund into First Trust Energy Income Partners Enhanced Income ETF, a newly created actively managed exchange-traded fund managed by FTA and sub-advised by EIP. The Mergers have also been approved by the Board of Trustees of EIPI. EIPI will be the surviving fund.

Under the terms of the proposed transactions, shareholders of each Target Fund would receive shares of EIPI with a value equal to the aggregate net asset value of the Target Fund shares held by them and would become shareholders of EIPI, with the Target Funds terminating. It is currently expected that the transactions will be consummated during the second quarter of 2024, subject to requisite shareholder approvals and satisfaction of applicable regulatory requirements and approvals and customary closing conditions. Each merger is expected to qualify as a tax-free reorganization for federal income tax purposes. Each transaction is subject to shareholder approval and is a separate Merger, and no Merger is contingent upon any other Merger. There is no assurance when or whether such approvals, or any other approvals required for the transactions, will be obtained.

As we can see in the quoted paragraphs from the official press release, the transaction will be conducted at the net asset value of the First Trust New Opportunities MLP & Energy Fund. This presents us with a very strong opportunity to earn some capital gains as this fund historically has traded at a very large discount to net asset value. This is still the case today, as the fund has traded at an average discount of 8.14% over the past month. This is a narrower discount than the fund has had on average in past months, which is likely because of this merger.

The transaction should result in anyone who purchases the fund at a discount earning some capital gains from the merger transaction as long as the assets held by this fund hold their value. There is no guarantee of that, especially because there is a risk that the Federal Reserve will disappoint the market by not reducing interest rates at the March meeting, but midstream companies in general have been rather insensitive to interest rates lately because of the influence that energy prices have on the headline inflation rate. As such, it might actually make sense to start dollar cost averaging into this fund with the intent of capitalizing on the removal of the discount on net asset value once the merger is complete.

Leverage

As is the case with many closed-end funds, the First Trust New Opportunities MLP & Energy Fund employs leverage as a method of boosting its effective yield and total return above that of any of the assets in its portfolio. I explained how this works in my previous article on the fund:

In short, the fund borrows money and uses that borrowed money to purchase the common equity of master limited partnerships, corporations, and utilities. As long as the purchased assets have a higher total return than the interest rate that the fund has to pay on the borrowed money, the strategy works pretty well to boost the effective yield of the portfolio. Since this fund is capable of borrowing at institutional rates, which are considerably lower than retail rates, this will usually be the case. It is important to note though that this strategy is less effective today with rates at 6% than it was eighteen months ago when rates were essentially 0%. This is because the difference between the total return of the purchased assets and the interest rate that the fund has to pay on the borrowings is much narrower than it used to be.

However, the use of debt in this fashion is a double-edged sword. This is because leverage boosts both gains and losses. As such, we want to ensure that the fund is not employing too much leverage because that would expose us to too much risk. I usually like to see a fund's leverage remain under a third as a percentage of its assets for this reason.

As of the time of writing, the First Trust New Opportunities MLP & Energy Fund has leveraged assets comprising 20.30% of its overall portfolio. That is relatively in line with the 20.08% leverage that the fund had the last time that we discussed it, and it is also well below the one-third maximum that I normally consider to be acceptable for an equity closed-end fund. As such, there is probably no reason to worry too much about the fund's leverage right now.

Distribution Analysis

One of the biggest reasons why investors purchase shares of master limited partnerships and energy infrastructure companies, in general, is because of the relatively high yields that these companies typically possess compared to other things in the market. As already mentioned, the Alerian MLP Index has an 8.12% yield at its current level and there are several partnerships that have higher yields than that. The fund invests its assets in a portfolio that consists of these companies and naturally receives distribution payments from each of them. It then borrows money and uses that borrowed money to collect distribution payments from more midstream companies than it could own with just its own equity capital. The fund combines all of these payments with any capital gains that it manages to realize from the assets in its portfolio and pays the money out to its own shareholders, net of its expenses. We can probably assume that this business model would result in the fund's shares having a very high yield themselves.

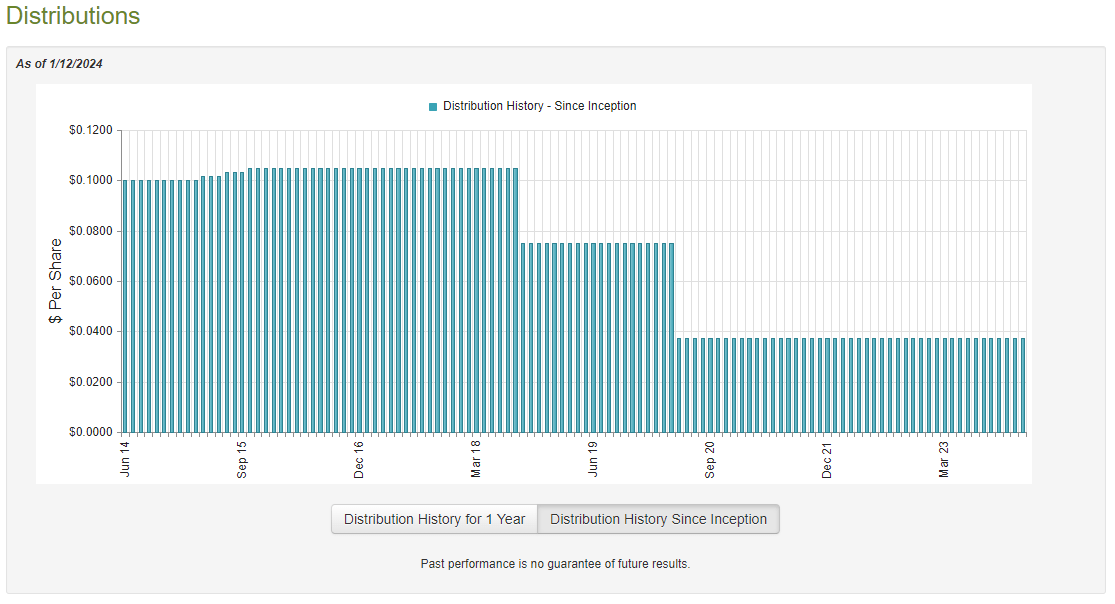

This is certainly the case as the First Trust New Opportunities MLP & Energy Fund pays a monthly distribution of $0.0375 per share ($0.45 per share annually), which gives it a 6.47% yield at the current price. That is, admittedly, not nearly as good as the Alerian MLP Index but it is important to keep in mind that this fund invests in a wider range of assets than the index, such as midstream corporations and utilities. Unfortunately, though, the fund's distribution history leaves a lot to be desired as it has cut its payout twice over its history:

{kind=link}

One thing that we note here is that the fund failed to hike its distribution following the 2020 cuts. This is rather disappointing, especially considering that some of the companies that comprise large positions in its portfolio have increased their own dividends and distributions over the period. It is also disappointing considering that today's high level of inflation means that we need to have a steadily increasing income just to maintain our standard of living. This fund has failed to accomplish that goal and thus investors who depend on this fund for income have felt as though they are falling behind and getting poorer. This is not at all what we desire as investors, and it could reduce the fund's appeal to those looking to earn the money that they need to pay their bills and support themselves from the assets in their investment portfolios.

With that said, our thesis for investing in this fund today is a short-term one because the merger is expected to be completed sometime during the second quarter of this year. Thus, the most important thing for most of us today is how well the fund is covering the distribution right now. We certainly do not want it to be engaging in unnecessary net asset value destruction, after all. However, even if the fund is depleting its net asset value to sustain the distribution, it is probably not that big of a deal today because it just means that we get some of the returns today instead of in a few months.

Fortunately, we have a very recent document that we can consult for the purpose of our analysis. As of the time of writing, the fund's most recent financial report corresponds to the full-year period that ended on October 31, 2023. This is a much newer report than the one that we had available to us the last time that we discussed this fund, and it is also newer than the financial reports that we have available from almost any other closed-end fund. The date on this report is quite nice because the market was pretty much all over the place during that full-year period. The end of 2022 displayed rather challenging conditions for most assets, while the first half of 2023 had an artificial intelligence bubble. There was even a period of rising energy prices and rising interest rates during the last four months or so of the period of time that is covered by this report. As such, this report should give us a very good idea of how well this fund managed to perform during wildly divergent market environments.

During the full-year period, the First Trust New Opportunities MLP & Energy Fund received $4,538,786 in dividends and $274,310 in interest from the assets in its portfolio. We have to subtract out the foreign withholding taxes that the fund paid on some of this income in order to arrive at a total investment income of $4,608,748 during the period. The fund paid its expenses out of this amount, which left it with $3,069,273 available to shareholders. As might be expected, that was nowhere near enough to cover the $10,564,660 that the fund paid out in distributions during the period. At first glance, this might be concerning as the fund clearly did not have sufficient net investment income to cover its payouts.

However, the fund has other methods through which it can obtain the money that it needs to cover the distributions. For example, a significant portion of this fund's income comes from master limited partnerships. That money is not included in total or net investment income, however, as it is considered to be either a return of capital or a capital gain. In addition, the fund might realize capital gains, which are also not considered to be investment income for tax or accounting purposes.

The fund had a great deal of success at deriving income from alternative sources during the full-year period. It reported net realized gains of $12,594,659 that were partially offset by $2,269,602 net unrealized losses. Overall, the fund's net assets increased by $1,519,188 after accounting for all inflows and outflows during the period. Thus, it appears that this fund is covering its distribution fairly well and we should not have to worry about its ability to sustain it until the merger occurs.

Valuation

As of January 12, 2024 (the most recent date for which data is available as of the time of writing), the First Trust New Opportunities MLP & Energy Fund has a net asset value of $7.52 per share but the shares currently trade for $6.88 each. This gives the fund's share an 8.51% discount on net asset value. This is reasonably in line with the 8.14% discount that the shares have had on average over the past month. The current price therefore appears to represent a reasonably good entry point.

Conclusion

In conclusion, the First Trust New Opportunities MLP & Energy Fund is well-positioned to deliver significant gains in the near future as a result of an upcoming merger and conversion into an exchange-traded fund. As the shares are selling at a price that is well below the net asset value, the fund is providing investors with an opportunity to profit from this event. It may be best to dollar cost average into the fund's shares though, as there is a risk that the fund's price might decline in the event of a market correction that occurs prior to the merger date. We can also expect that the discount will slowly decrease as the merger date approaches, which could position this fund to outperform peers from other fund managers. I am upgrading this fund to a strong buy due to the potential for fairly substantial near-term profits from the merger.

For further details see:

FPL: Impending Merger Creates Opportunity For Significant Gains (Rating Upgrade)