FELE - Franklin Electric: Moderating Growth Keeps Me On The Sidelines

2023-05-11 11:52:09 ET

Summary

- Franklin Electric reported strong Q1 results.

- However, the growth is expected to moderate in the coming quarters.

- Valuations are at a discount to historical levels but slowing growth keeps me on the sidelines.

Investment Thesis

Franklin Electric (FELE) recently reported strong Q1 results and raised its guidance. While the company has shown a good growth rate over the past few years, I anticipate a moderation in its growth rate in the upcoming quarters and the following year. The company's backlog has been declining, along with a reduction in open orders, which could impact its revenue performance. Additionally, as the year progresses, the pricing comparisons are expected to become more challenging, affecting both revenues and margins. Despite the stock trading at a discount compared to historical valuations, I believe this discount is justified, and I prefer to remain on the sidelines.

FELE Q1 2023 Earnings

Franklin Electric recently reported its Q1 2023 earnings, with GAAP EPS of $0.79 (up 25% YoY), surpassing consensus estimates by 15 cents. Revenues came in at $484.55 million (up 7.3% YoY), exceeding consensus estimates by $8.29 million. Moreover, the company raised its guidance for full-year sales, now projected to be in the range of $2.15 billion to $2.25 billion, compared to the previous range of $2.1 billion to $2.2 billion. Additionally, the full-year 2023 EPS is expected to be in the range of $4.25 to $4.45, up from the previous range of $4.10 to $4.30.

Revenue Analysis and Outlook

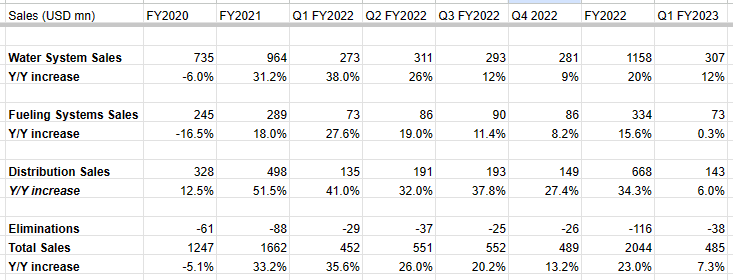

In Q1 2023, Franklin Electric witnessed a 7.3% YoY increase in sales. The water systems segment saw a notable 12% YoY growth, while the Fueling Systems business experienced a modest 0.3% YoY increase in sales. The Distribution sales also recorded a 6% YoY increase. The company achieved YoY revenue growth across all three segments, driven by strong demand for its products and distribution services. The water and distribution business, in particular, reported higher volumes and pricing increases, effectively offsetting the impact of foreign currency headwinds. Furthermore, Franklin Electric benefited from improved supply chain conditions, resulting in a higher backlog-to-sales conversion rate.

{kind=link}

While the company has seen good growth in recent years, I expect its revenue growth to slow down going forward. A good amount of the growth the company experienced in the recent quarters was due to its high backlog. In late 2021 and early 2022, supply chain constraints prevented the company from fulfilling many orders, resulting in an increase in its open orders backlog to $290 million in Q2 last year. As supply chain constraints slowly eased, the company was able to increase shipments, which helped boost revenue over the last couple of quarters. However, as a result, the backlog has started to decrease and is now at $230 million, down approximately $60 million from its peak. Therefore, the open orders in the backlog should be less of a help compared to what we have seen in the past few quarters.

Similarly, in the last year, the company kept increasing its prices as the year progressed due to elevated raw material inflation. However, inflationary pressures have now moderated, and I am not expecting a significant price increase this year. So, the price comparisons should become tougher as the year progresses. Therefore, I am expecting the benefit from higher year-over-year prices to be largest in Q1 and then moderate going forward.

Margin Analysis and Outlook

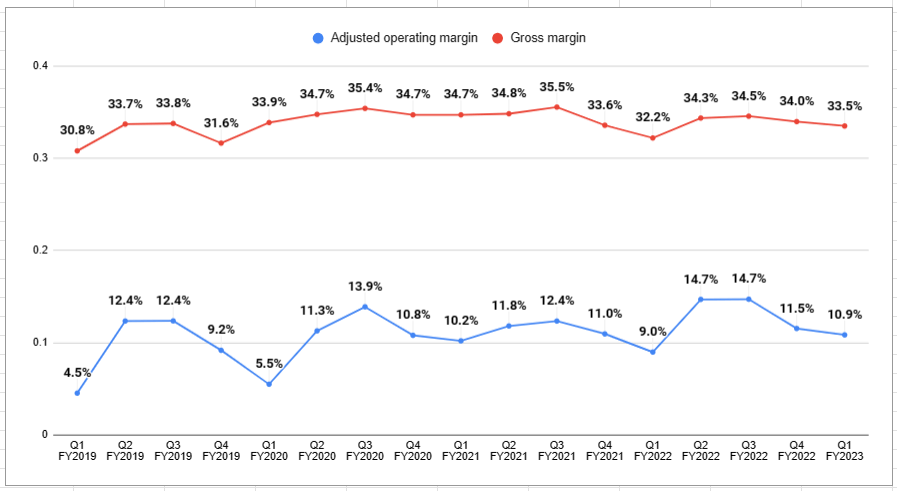

The company demonstrated a strong margin performance in the previous quarter, with both its gross and operating margins showing improvement. FELE's gross margin increased by 130 basis points (bps), rising from 32.2% in Q1 of the previous year to 33.5% in Q1 2023. This improvement can be attributed to factors such as price realization, effective cost management, and the operating leverage gained from higher sales.

In Q1 2023, the operating margin reached 10.9%, surpassing Q1 2022's operating margin of 8.8% (or 9% on an adjusted basis, excluding one-time charges of $0.7 million incurred in Q1 2022). Apart from the higher gross margin, the net operating margin also benefited from 60 bps of selling, general, and administrative (SG&A) leverage.

{kind=link}

Looking ahead, the company is expected to face challenging comparisons on the margin front. In the previous year, Q1 margins were affected by inflationary pressures and disruptions in the supply chain, as pricing actions had not been fully implemented yet. Consequently, the company's Q1 2023 margin growth benefited from favorable comparisons. However, moving forward, the situation is likely to be different, as Q2 2022 witnessed a significant sequential improvement in margins.

Furthermore, while moderating inflation is advantageous for the company's manufacturing business, its distribution business is adversely affected. The distribution business primarily sells commodity-type products, and when prices decrease it must sell its stock inventory. This inventory which was purchased at higher prices, is now sold at lower prices, thereby impacting profitability.

Overall, I don't think investors should get too carried away about Q1 margin performance and I am expecting flattish margin performance in the coming quarters.

Valuations and Conclusion

FELE currently trades at a P/E ratio of 21.35x based on FY23 consensus EPS estimates, and at 20.23x based on FY24 consensus EPS estimates. This represents a discount compared to its 5-year average forward P/E of 24.61. However, I believe there are valid reasons for the stock to trade at a discount to its historical levels.

Although the company has demonstrated strong growth in recent years, it is expected that its growth rate will moderate to a more normalized level in the current year and the following year. For FY23, the sell-side consensus forecasts high single-digit EPS growth, while for FY24, the sell-side consensus expects mid-single-digit EPS growth. These projections indicate a deceleration in growth compared to the robust pace seen in the past.

FELE Consensus EPS Estimates (Company Data, GS Analytics Research) FELE Consensus Revenue Growth Estimates (Company Data, GS Analytics Research)

{kind=link}

{kind=link}

Furthermore, although the company's water business shows promising prospects, its fuelling systems business encounters a secular threat due to the growing adoption of electric vehicles (EVs). As a result, while the company is projected to continue growing its revenue and EPS in the upcoming years, its growth rate is anticipated to decelerate. Given the company's modest mid to high single-digit expected EPS growth, I do not find the current valuation appealing enough. Consequently, I maintain a neutral rating on the stock.

For further details see:

Franklin Electric: Moderating Growth Keeps Me On The Sidelines