FTHY - FTHY: Discount Deepens Further

2023-05-17 17:18:40 ET

Summary

- FTHY's discount has moved wider since our last update, potentially opening up an opportunity.

- I felt that distribution coverage was lacking and that a cut could be possible to the distribution.

- However, the fund recently raised its distribution despite a lack of coverage.

Written by Nick Ackerman, co-produced by Stanford Chemist. This article was originally published to members of the CEF/ETF Income Laboratory on May 16th, 2023.

Since our last update on First Trust High Yield Opportunities 2027 Term Fund ( FTHY ), the fund has slipped to an even deeper discount. That could potentially offer an even better entry level. The fund is a term structure, so at some point, the discount should be realized. Although, we still have quite a few years before that becomes a more important factor.

The discount widening came as the share price slipped a touch while the NAV rose. Here's a look at the performance since our prior update on a total share price and NAV return basis.

Ycharts

With the current economic outlook for a slowdown and a recession highly forecasted, there are credit risks to consider before jumping into this fund. The fund's discount and the underlying discount in the underlying debt portfolio are compelling, and some of this is factored in already.

Interestingly, the fund raised its distribution since our last update as well. In that update, I noted a lack of coverage, so I was cautious about a cut going forward. Seeing a raise was certainly a bit of a shock, but I don't believe the coverage really improved.

The Basics

- 1-Year Z-score: -0.73

- Discount: 11.90%

- Distribution Yield: 11.40%

- Expense Ratio: 1.95%

- Leverage: 17%

- Managed Assets: $688.4 million

- Structure: Term ( anticipated liquidation around August 1st, 2027)

FTHY's investment objective is "to provide current income." They intend to do this by "investing at least 80% of its Managed Assets in high yield debt securities of any maturity that are rated below investment grade at the time of purchase or unrated securities determined by the Advisor to be of comparable quality. High-yield debt securities include the U.S. and non-U.S. corporate debt obligations and senior, secured floating-rate loans ("Senior Loans")."

The fund's expense ratio is always something I'll point out on this fund. It is quite high, and so far, the expense ratio hasn't necessarily been justified in any sort of outperformance. The fund invests in a fairly standard portfolio, so that isn't necessarily one of the reasons for a higher expense ratio that we can see from other funds.

While the fund is mildly leveraged, they are still leveraged. That increases risks to the downside (as well as potential moves higher) and means higher volatility. When including the fund's leverage costs, the expense ratio goes up to 3.09%. Their leverage is based on SOFR plus 0.90%.

Since our last update, the fund has slightly increased its leverage. We noted this previously because they had deleveraged significantly from the $306 million they were carrying at the beginning of 2022 .

FTHY Leverage Stats (First Trust)

Performance - Attractive Discount

The fund's lack of performance since launch isn't really that hard to explain. In this case, the fund launched in mid-2020. It enjoyed an actual strong market with 0% interest rates where it could thrive for around a year and a half. However, as soon as interest rates started to take off in 2022, this fund took a big hit. This wasn't out of the ordinary, as all fixed-income funds took a big hit too. The leverage in this fund meant a relatively sharper drop than non-leveraged ETFs, but the overall trajectory was the same.

I include iShares iBoxx $ High Yield Corporate Bond ETF ( HYG ) and Invesco Senior Loan ETF ( BKLN ) for some context in the performance chart below. This seems appropriate as FTHY is split between high-yield and bank loans.

Ycharts

As we can see, FTHY has delivered negative returns since its launch. Even HYG provided some positive returns through this period, and FTHY seems to correlate quite highly with HYG, too. The losses here seem to be that FTHY dropped harder due to the higher leverage they carried at one time. When the recovery happened, they were already deleveraged, so the bounce wasn't quite there.

Where the performance particularly detracted was the fund's total share price relative to the fund's NAV. That's what drove the actual discount widening that we've seen in this fund and where the overall bigger opportunity potentially is. We aren't quite near the lows that the fund touched in 2022, but the current discount is still quite appealing.

Ycharts

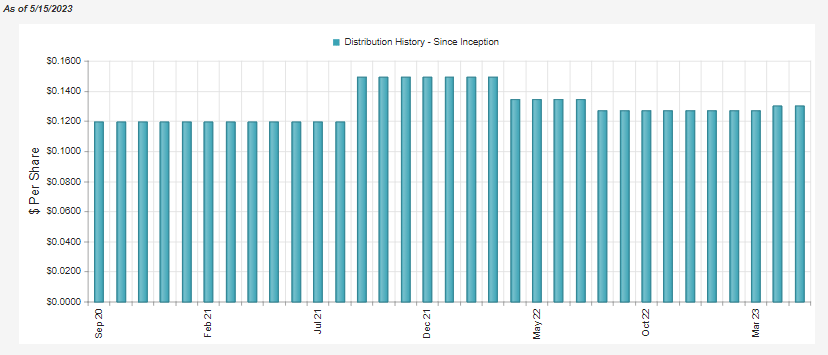

Distribution Gets A Bump

Now this is where there was a bit of a shock. The fund increased its distribution recently .

{kind=link}

We haven't received any new reports to look at earnings since our last update , but at that time, coverage was quite lacking.

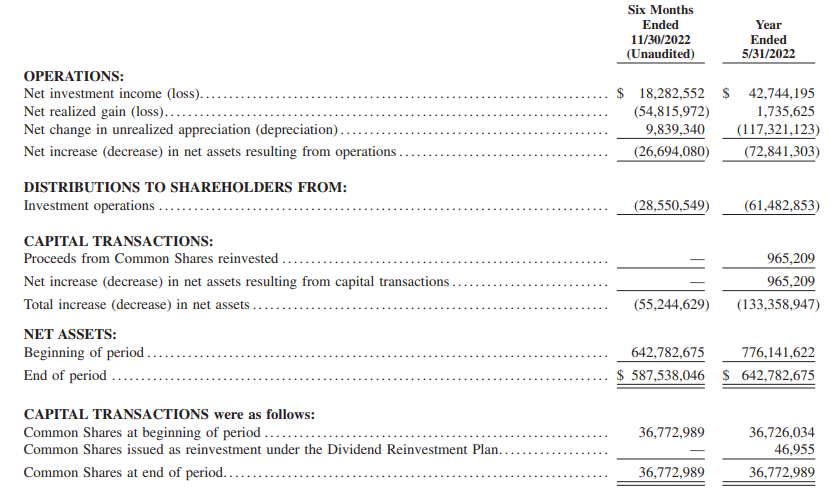

The reduction in leverage meant their overall total investment income dropped from $30.185 million to $27.534 million . Due to leverage costs rising, "interest and fees on loan" increased to $3.425 million from $1.345 million in the year-ago six-month period.

Overall, further distribution cuts in the future wouldn't be surprising in the least.

Deleveraging played a large role in seeing the actual net investment income decline.

{kind=link}

In terms of a per-share basis, NII for the semi-annual report was $0.50 or around $0.0833 per month.

They leveraged up another $10 million since our prior update, but that certainly wouldn't seem to be enough to close the gap. In fact, the Fed even increased interest rates further since then, meaning that their NII could have taken a further hit.

This reminds me of when they raised their distribution the first time after launching. They were covering the distribution initially, but it meant they weren't after the raise. They then cut twice after raising, as we can see in the chart above.

The silver lining that could be driving the latest increase would be that the yield to maturity on their portfolio is around 10% currently. This would be factoring in the assumption that they receive par back at maturity. On a NAV basis, the distribution comes to a 10.04% rate, which is more reasonable in the current interest rate environment. However, they still have to earn their elevated expense ratio on top of this. So even looking at the YTM rate, it would be a stretch to consider it covered.

Therefore, while the fund's distribution rate of 11.40% certainly looks appetizing, I can't say that it should be expected to be earned or continued indefinitely. Instead, this could be an effort by management to try to narrow the fund's discount potentially.

FTHY's Portfolio

The fund splits its portfolio between high-yield bonds and senior loans. With interest rates rising, senior loans should have benefited from increased income. However, the high-yield bond portion of the portfolio would have taken a bigger hit.

The portfolio is invested in below-investment-grade debt instruments of high-yield bonds and senior loans. This is truly a "junk" portfolio, with very limited exposure to any investment-grade rated debt and ~20% in CCC+ and lower.

FTHY Portfolio Credit Rating (First Trust)

The bond side of the portfolio is the largest part of their portfolio, which is something I mentioned as being a bit odd. Given the increasing interest rates, I felt the fund really should have leaned into senior loans and then swapped into bonds.

To a certain extent, this is something they did sort of do. Nearer to the time of their launch , they were split around 66/33 between bonds and loans. Today, that split is around 80/20.

FTHY Asset Breakdown (First Trust)

By reducing senior loans now and potentially locking in higher-yield fixed-rate bonds, I believe the fund is well positioned in terms of its split now. The idea is that if the Fed cuts rates in the next year or two, the high-yield bonds will continue generating the same predictable income for the fund. While at the same time, the senior loans in the portfolio would start to see their yields start to drop - the opposite of the benefit we saw when rates were rising and therefore generating higher income.

On the other hand, this has to be balanced with the risks between the two debt securities. Senior loans sit higher on the capital stack than corporate bonds; thus, the hit to corporate bonds could be larger than the senior loans should defaults and bankruptcies start to tick higher.

Helping to limit the fund's hit is not only the discount that the fund is currently sporting at the fund level, but it is also the weighted average price of FTHY's underlying portfolio. They last listed that the average price of the debt securities in their portfolio comes to $89.20. This is virtually identical to the $89.18 they listed at the end of January 2023.

FTHY Portfolio Stats (First Trust)

The portfolio characteristics also give us the important effective duration metric below. At 3.58 years, that indicates that for every 1% change in interest rates, the fund's underlying portfolio would move 3.58%. That's to the upside or downside. Therefore, should the Fed cut, that can mitigate some downside of defaults as some debt security prices could see an improvement.

To further help mitigate damage to the fund during a recession, the fund is split quite diversely amongst many different industries. They carry around 213 holdings, according to CEFConnect. That's many holdings, and the split between different industries should help. However, with that said, the fund's top ten holdings are fairly concentrated relative to what we see from other high-yield funds.

FTHY Top Ten Holdings (First Trust)

For example, BlackRock Corporate High Yield Fund ( HYT ) - something I consider a bit of a gold standard for the traditional high-yield corporate bond space - comes in with over 1250 positions . The top position came in at 2.51%, and the second largest weighting drops to 1.56%. By holding number ten, we are sub-1% at a 0.90% allocation.

Credit Suisse High Yield Bond Fund ( DHY ) is another example. While they only carry 222 holdings as of their last fact sheet , the top position makes up only a 1.69% weight. The entire top ten make up only 11.73%. So you can have a relatively lower number of holdings while simultaneously being more diversified through a lower weighting to each holding.

To sum up, that could mean that FTHY is diversified but not as much as some peers. However, these are also pure-play high-yield bond fund comparisons, and FTHY also incorporates senior loan exposure. That could see them underperform if a few key top holdings perform badly. Conversely, it could also mean some outperformance should they perform better.

Conclusion

This fund could be providing investors with an opportunity currently at its deep discount and discounted underlying portfolio. However, there are certainly risks to consider. The fund has a high expense ratio, the fund's underlying portfolio is quite junky, and the fund's distribution - while just raised - is not being covered. At least, it isn't being covered unless they dramatically shifted the portfolio since the last report. Because at that time, they were earning around $0.0833 per month, and they now are paying $0.13 per month.

That's certainly a lot of negatives to consider but is factored in by these discounts. Additionally, I believe the fund is well-positioned for the current environment. The higher allocation to high-yield bonds means if the Fed cuts rates, these should be able to be maintained - if defaults during a recession aren't too detrimental.

At the same time, they still carry a fairly meaningful allocation to senior loans, which are higher up in the capital stack than bonds. Finally, the fund's low utilization of leverage at this time means it could be relatively less volatile than its peers. It also means they have quite a bit of capacity to take advantage of any buying opportunities should they find some deals.

For further details see:

FTHY: Discount Deepens Further