FLL - Full House Resorts: Anticipating The Chamonix Earnings

2024-01-18 05:43:20 ET

Summary

- Full House Resorts operates casinos in the United States and owns seven casinos in various states.

- The company has had stable revenues and has achieved a CAGR of 4.3% in revenues from 2012 to current trailing figures with mostly stable profitability.

- Full House Resorts has made significant investments in new casino openings, including The Temporary by American Place in Illinois and Chamonix Casino Hotel in Colorado.

- The Temporary's earnings contribution is significant, but Chamonix's earnings profile is yet to be seen as the casino opened in December, making the stock an intriguing watchlist stock.

- The valuation suggests some upside in my baseline scenario, but due to volatility in expected earnings and Full House Resorts' highly leveraged balance sheet, the investment case is still very volatile making a hold rating constituted.

Full House Resorts (FLL) operates casinos in the United States. The company owns seven casinos; one in Mississippi, one in Indiana, two in Nevada, two in Colorado, one of which has been opened in late December of 2023, and one in Illinois, opened in February of 2023. In addition, the company operates online sportsbooks.

The stock has seen its fair share of turbulence in past years, but the return has overall been good despite the pandemic in between - in five years, Full House Resorts' stock has compounded at a CAGR of 14.8%.

{kind=link}

Long-Term Earnings Profile

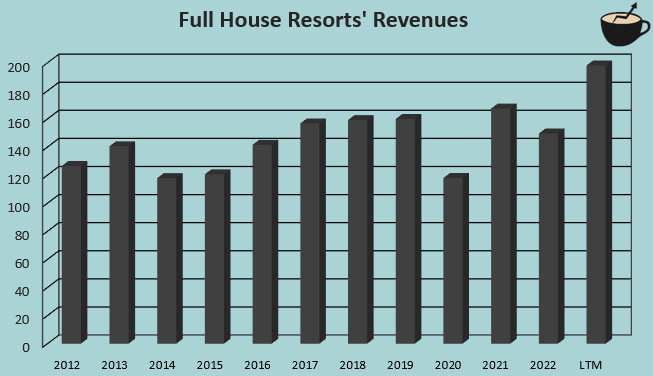

Full House Resorts has mostly had quite stable revenues when excluding the pandemic. From 2012 to current trailing figures, the company's revenues have grown at a CAGR of 4.3%, with an acceleration beginning in 2023 due to extensive investments in recent years attributed to new casino openings.

{kind=link}

Usually, I believe that EBIT margins are more representative of a company's earnings than an EBITDA margin, but for Full House Resorts, an EBITDA margin seems reasonable. The company has had relatively low maintenance CapEx in the long term. The depreciation related to the new casino opening in Illinois is lowering Full House Resorts' earnings through depreciation unrelated to the company's cash flow capabilities, making the EBITDA margin more representative. Historically, the company has achieved an average GAAP EBITDA margin of 13.8%, with the current trailing figure of 14.0% very near the figure.

{kind=link}

The Temporary by American Place

Full House Resorts has started to invest heavily in growth. In February of 2023, Full House Resorts opened The Temporary by American Place in Illinois. The casino was first proposed in 2021 , and investments have begun in Q4 of 2021 scaling significantly afterwards. Capital expenditures have scaled due to investments related to The Temporary by American Place, as well as the construction of Chamonix casino in Colorado - quarterly CapEx increased from a quarterly average of $1.34 million in 2019-2020 to a peak of $54.8 million in CapEx in Q4/2022.

{kind=link}

After the casino became operational in February, Full House Resorts' earnings have increased significantly. In Q3, as operations in the American Place have continued to build up, revenues from the casino reached $23.9 million . The amount represents 33.4% of Full House Resorts' entire revenues in the period, and 33.0% of the company's adjusted EBITDA, already making the new casino a highly meaningful contributor to the company's bottom line. With the operations still only ramping up, as told in the Q3 earnings press release , revenues from the casino could still go up quite well as quarters go on.

Although CapEx has begun to come down from 2022 highs, a high investment level is far from over. Full House Resorts has an agreement to build a more permanent American Place casino; the currently operational casino is called The Temporary by American Place. While the timeline for the investments is quite unclear, the construction has been instructed to begin sometime after the company's new Colorado casino has been operational. In August of 2023, the permanent location was anticipated to open within three years of the opening of The Temporary.

Betting it All on Colorado

The other significant source of the recent years' CapEx is the recently opened Chamonix Casino Hotel. Full House Resorts opened its doors in its new Colorado casino on the 27th of December in 2023. While The Temporary had an estimated $100 million in investments, Chamonix Casino Hotel's budget was estimated at $250 million as of January 2022 - the Colorado casino is Full House Resorts' most significant investment so far.

As such, Chamonix Casino Hotel's earnings should be even more meaningful than The Temporary's earnings that already added to 33.0% of Full House Resorts' adjusted EBITDA in Q3 - investors should be looking at the company's outlook carefully, as beginning in Q1 investors can get a rough estimate on Chamonix's long-term revenue level. The opening could provide investors with high upside, but also disappoint investors - analysts already expect Full House Resorts' revenues to grow by 42.8% in 2024.

The company's highly leveraged balance sheet makes a successful performance from Chamonix critical. To finance both the American Place and Chamonix, Full House Resorts has had to resort to a dangerously high debt level. Currently, the company has $464 million in long-term debt compared to a market capitalization of only $168 million. Also, interest expenses in the past twelve months cover around 88.1% of the company's GAAP EBITDA, making the financing situation highly leveraged. Payments still have some wiggle room as a large portion of Full House Resorts' debt is senior notes due 2028 , leaving Full House Resorts with some years to gain cash flows from the new casinos.

Volatile But Intriguing Valuation

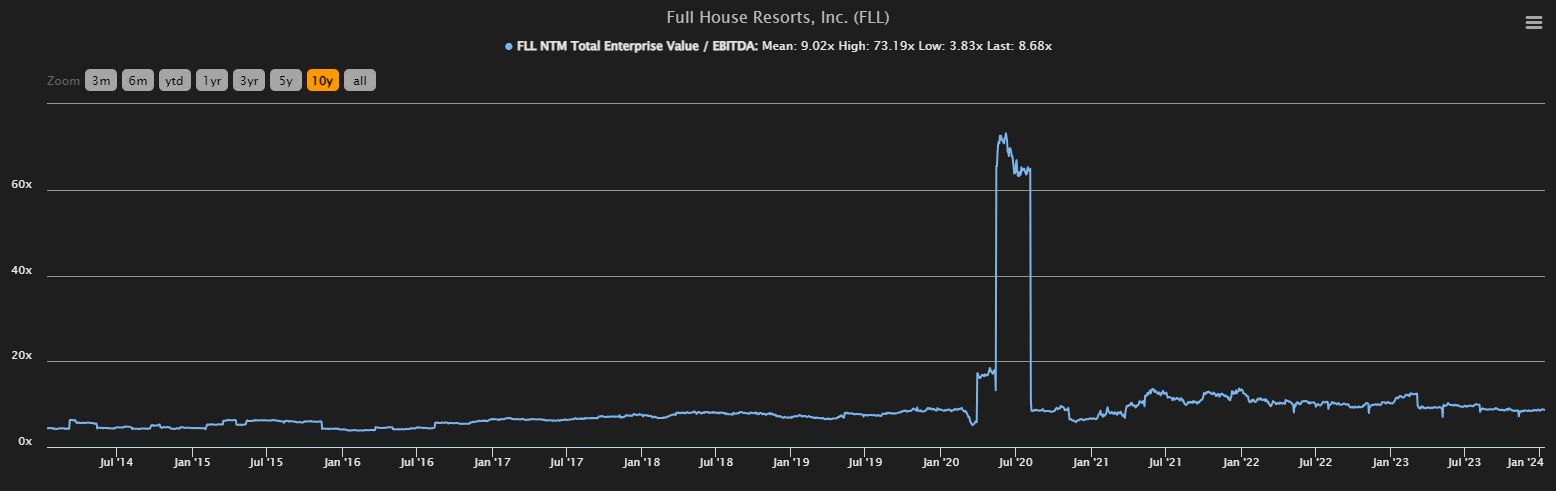

Full House Resorts currently trades near the company's ten-year average forward EV/EBITDA with a current figure of 8.7 compared to the average of 9.0.

{kind=link}

The new casino openings and Full House Resorts' leveraged balance sheet make the investment case very volatile. To contextualize the valuation and to estimate a fair value for the stock, I constructed a discounted cash flow model as usual. In the DCF model, I factor growth from the new openings significantly for 2023 and 2024, with revenue growths of 50% and 45% respectively - the 2024 estimate accounts for good revenues from Chamonix, and some continued growth from The Temporary. Afterwards, I estimate the growth to stable with stabilizing operations into a perpetual growth of 2%, with some elevated growth from 2025 to 2027 from a permanent American Place casino and slowly increasing customer visits in the two casinos.

As for the EBITDA margin, I estimate some leverage from the newly opened casinos - I estimate the EBITDA margin to rise from 13.9% in 2023 into 17.5% in 2025 as a result of slight operating leverage and the extensive investments that have gone into building the casinos into large operators. Full House Resorts has also had a good amount of pre-opening costs associated to the new casinos in 2023, making the level likely lower than a sustainable long-term margin level going forward. I estimate the heavy investments to continue into 2024 and 2025 due to American Place's permanent casino construction and some leftover investments for Chamonix, but to be relatively good afterwards.

With the mentioned estimates along with a cost of capital of 7.25%, the DCF model estimates Full House Resorts' fair value at $5.79, around 23% above the stock price at the time of writing. The stock seems to have some undervaluation with my estimates, but as the long-term revenue rates for new openings are still largely guesses, and as the uncertainty is highly leveraged by the company's balance sheet, the valuation is still highly volatile and could easily turn into estimating an overvalued stock.

{kind=link}

The used weighed average cost of capital is derived from a capital asset pricing model:

CAPM (Author's Calculation)

In Q3, Full House Resorts had around $6.7 million in interest expenses. With the company's current amount of interest-bearing debt, Full House Resorts' annualized interest rate comes up to 5.75%. I estimate the debt-to-equity ratio to stay near the current level, being well above the equity's market capitalization at 275%. For the risk-free rate on the cost of equity side, I use the United States' 10-year bond yield of 4.08% . The equity risk premium of 4.60% is Professor Aswath Damodaran's latest estimate for the United States, made on the 5th of January. Yahoo Finance estimates Full House Resorts' beta at a figure of 1.96 . Finally, I add a small liquidity premium of 0.75% and ESG addon of 1.5%, crafting a cost of equity of 15.35% and a WACC of 7.25%.

Takeaway

Full House Resorts is investing heavily in two new casinos. The Temporary has already started to contribute very well into mostly stable long-term revenues, generating adjusted EBITDA margins mostly in line with the entire operations. More recently, the Chamonix casino was opened in December of 2023 after very heavy investments. The company has had to leverage a heavy amount of debt to finance the investments, making the successful launch of Chamonix critical. While I estimate some upside from the stock's price into a fair valuation in a baseline scenario, I am not yet confident in a buy rating - the future financials are likely to vary from my estimates as Chamonix's earnings are largely unknown, and the leveraged balance sheet makes volatility very high for shareholders. While the investment case isn't a full house yet, investors have flopped top pair. As such, I keep a close and keen eye on the stock, but have a hold rating for the time being.

For further details see:

Full House Resorts: Anticipating The Chamonix Earnings