YMM - Full Truck Alliance Performs Well As Chinese Road Freight Market Improves

2023-11-08 12:30:47 ET

Summary

- Full Truck Alliance Co. Ltd. provides a road freight logistics platform in China.

- China is seeing a rebound in road freight volume growth.

- Full Truck Alliance is performing well and the stock appears to be undervalued.

- My outlook on Full Truck Alliance Co. Ltd. stock is a Buy at around $6.90 per share.

A Quick Take On Full Truck Alliance

Full Truck Alliance Co. Ltd. ( YMM ) operates an online freight platform to facilitate shipments across a range of types, weights and distances in China.

I previously wrote about YMM with a Hold outlook due to concerns about a slowing Chinese economy.

However, road freight volumes have been increasing, and the firm’s recent performance is enticing.

My outlook on Full Truck Alliance Co. Ltd. is a Buy at around $6.90 due to its prospects for improving profitability and reasonable growth in a rebounding Chinese road freight market.

Full Truck Alliance Overview And Market

China-based Full Truck Alliance Co. Ltd. has created a digital logistics platform assisting truckers and shippers in locating, negotiating, booking and tracking road shipments in China.

The firm is led by founder, Chairman and CEO Peter Hui Zhang, who was previously regional manager of the B2B unit of Alibaba Group.

The company’s primary offerings include:

-

Freight listing service

-

Freight brokerage service

-

Online transaction service.

FTA seeks customers via word of mouth and online marketing channels.

According to a market research report by Mordor Intelligence, the Chinese market for road transportation services is expected to grow at a CAGR (Compound Annual Growth Rate) of 6.23% from 2016 to 2028.

Logistics participants tend to be concentrated in the Southwest and South Central regions of China.

The largest industry served by end-user type from 2022 to 2028 is the wholesale and retail trade sector, with less-than-truckload being the fastest-growing segment of the road transportation industry.

The chart below shows the market growth profile from 2022 to 2028 by user sector:

Mordor Intelligence

Major competitive or other industry participants by type include:

-

Carriers

-

Brokers

-

Freight matching companies

-

Tech-driven freight transportation firms.

Full Truck Alliance’s Recent Financial Trends

Total revenue by quarter (blue columns) has risen in recent quarters; Operating income by quarter (red line) has turned decisively positive in the most recent quarter ( Q2 2023 ):

Seeking Alpha

Gross profit margin by quarter (green line) has fluctuated seasonally but has been trending higher over time; Selling and G&A expenses as a percentage of total revenue by quarter (amber line) have trended lower in recent quarters:

Seeking Alpha

Earnings per share (Diluted) have made steady progress in recent quarters:

Seeking Alpha

(All data in the above charts is GAAP.)

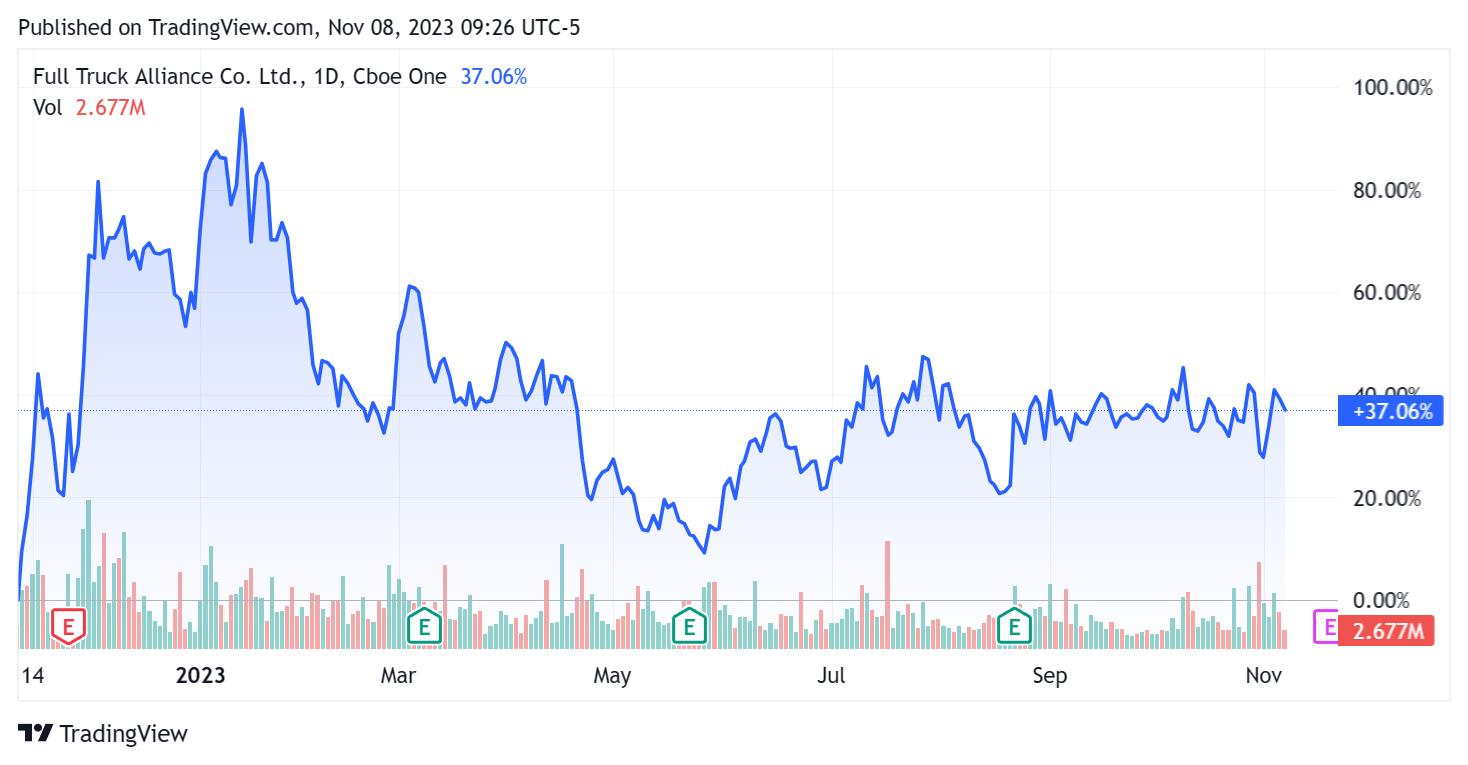

In the past 12 months, YMM’s stock price has risen by 37.06 net, with up moves in response to recent earnings reports:

{kind=link}

For balance sheet results, the firm ended the quarter with $3.4 billion in cash, equivalents and short-term investments and no debt.

Valuation And Other Metrics For Full Truck Alliance

Below is a table of relevant capitalization and valuation figures for the company:

| Measure (Trailing Twelve Months) |

| Amount |

| Enterprise Value / Sales |

| 4.1 |

| Enterprise Value / EBITDA |

| 41.6 |

| Price / Sales |

| 7.3 |

| Revenue Growth Rate |

| 32.1% |

| Net Income Margin |

| 21.4% |

| EBITDA % |

| 9.8% |

| Market Capitalization |

| $7,600,000,000 |

| Enterprise Value |

| $4,210,000,000 |

| Operating Cash Flow |

| -$2,250,000 |

| Earnings Per Share (Fully Diluted) |

| $0.22 |

| Forward EPS Estimate |

| $0.32 |

| SA Quant Score |

| Strong Buy - 4.69 |

(Source - Seeking Alpha.)

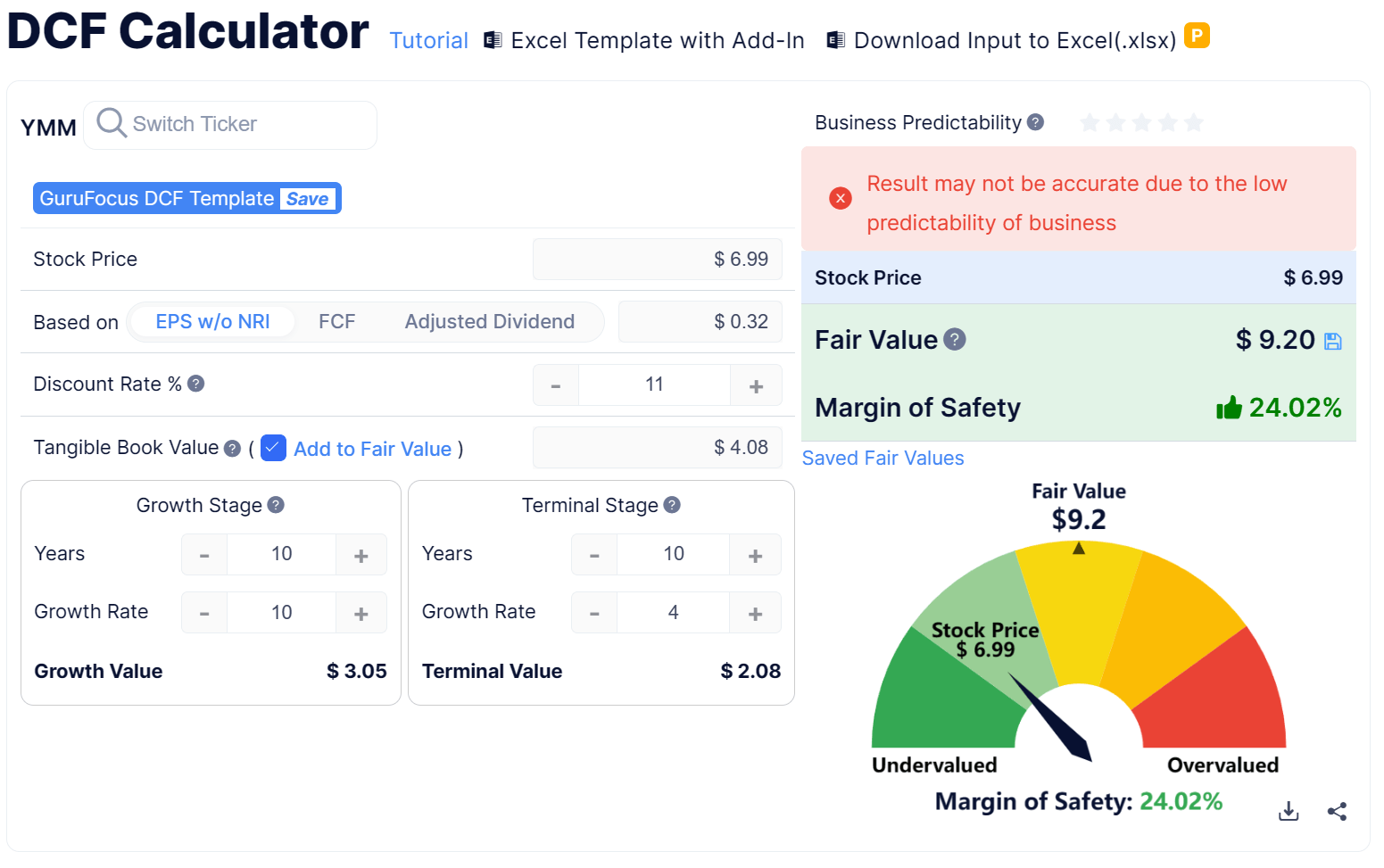

Below is an estimated DCF (Discounted Cash Flow) analysis of the firm’s projected growth, earnings and tangible book value:

{kind=link}

Based on the DCF, the firm’s shares would be valued at approximately $9.20 versus the current price of $6.99, indicating they are potentially currently undervalued.

Commentary On Full Truck Alliance

In its last earnings call (Source - Seeking Alpha ), covering Q2 2023’s results, management’s prepared remarks highlighted its strong focus on long-haul full truckload business.

The company launched a number of new product functions:

"including a streamlined shipping process, standardized entrusted shipment services, a comprehensive truckers' rating system and more efficient order recommendation strategies for truckers, which significantly improved the shippers' experience, particularly direct shippers, as well as strengthened truckers stickiness, driving the number of fulfilled orders to 40.2 million, an increase of 44.5% year-over-year."

Notably, the company will increase its investment in technology to improve its efficiency and continue to transition to a "more digitally empowered platform."

Analysts asked management about fulfillment orders and rates, margin improvement and shipper membership growth.

Leadership responded that fulfillment order growth was due to an expanded user base through its promotion efforts, especially high-quality direct shippers. They expect continued order growth in Q3.

The firm is seeing high retention rates for its shipper base. Notably, competitive platforms are lowering maximum commissions and membership fees due to recent regulatory changes, so management plans to diversify revenue streams through new products and services.

Margin improvement was driven by a mix shift to higher margin commission-based and value-added services from freight brokerage and partially due to tax rebate timing differences.

Total revenue for Q2 2023 rose by 14.0% year-over-year, while gross profit margin improved by 2.8%.

The firm’s 12-month shipper retention rate was stable at 80%.

Selling and G&A expenses as a percentage of revenue fell 8.9%, indicating a strong improvement in efficiency for this metric.

Operating income rose sharply to $46.0 million for the quarter, an impressive result.

The company's balance sheet is quite strong, with $3.4 billion in cash and no debt. We don’t have cash flow figures for the current quarter.

Looking ahead, consensus topline revenue estimates indicate growth to be 13.9% over 2022.

If achieved, this would represent a significant decline in revenue growth rate versus 2022’s revenue growth rate of 37.3% over 2021.

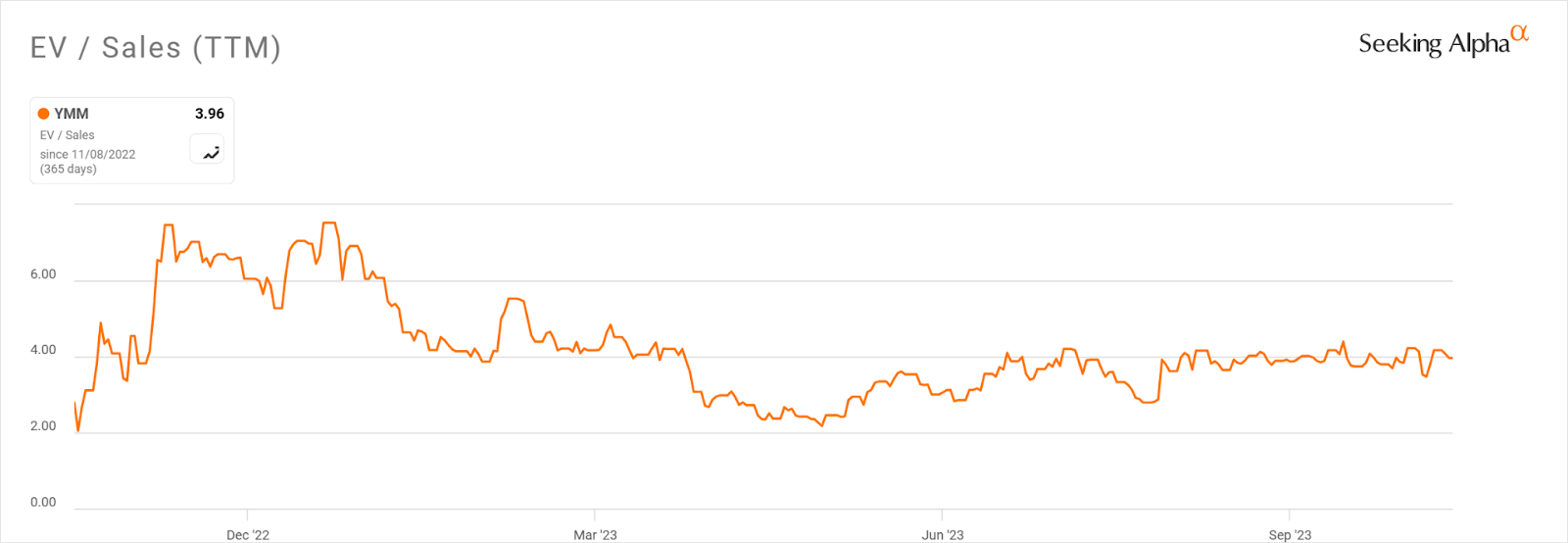

In the past twelve months, the firm's EV/Sales valuation multiple has risen by about 42% net, as the chart from Seeking Alpha shows below:

{kind=link}

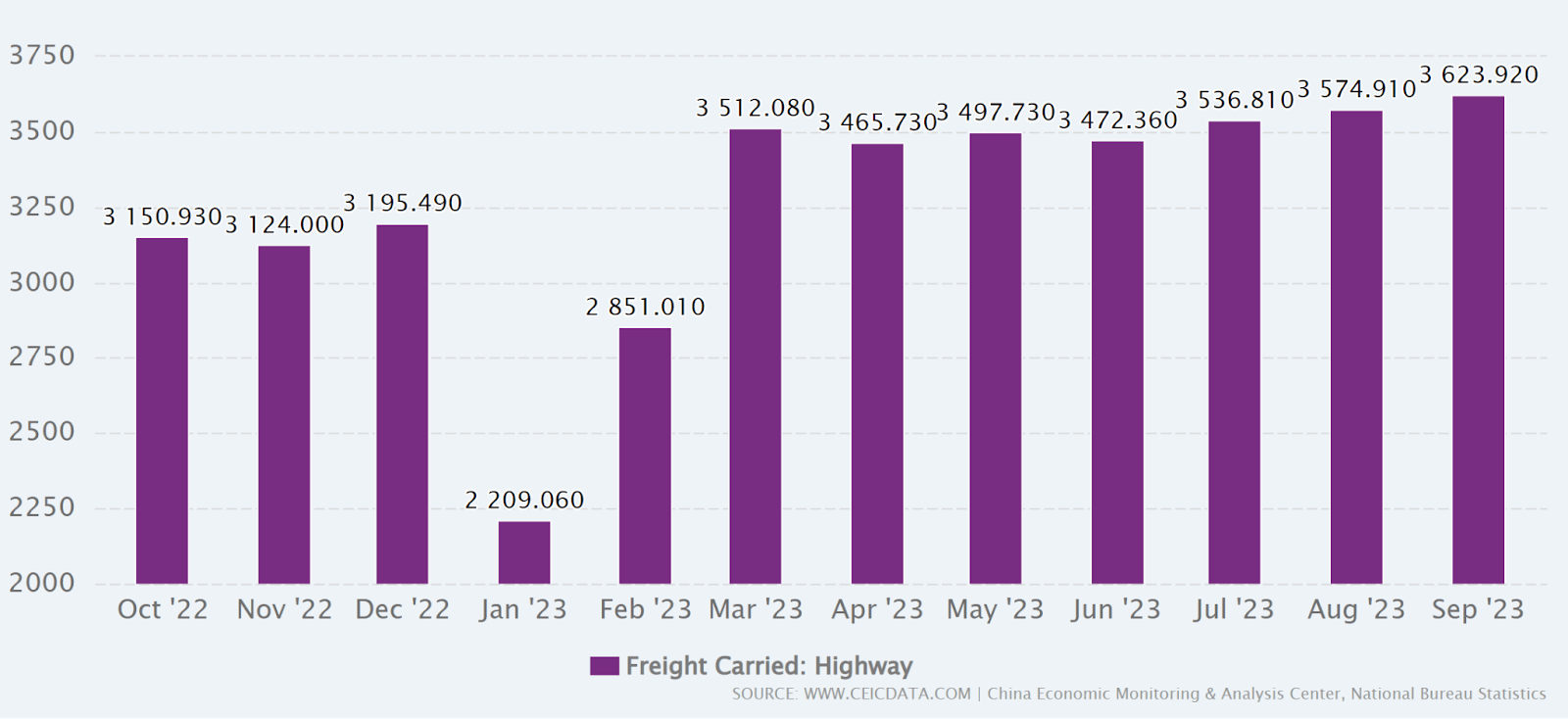

As the chart shows below, the Chinese freight market is continuing to see increased volumes in recent months:

{kind=link}

This bodes well for logistics service providers like YMM.

My discounted cash flow calculation indicates the stock may be materially undervalued at its present price level of approximately $6.95.

While topline revenue growth may be settling down, earnings growth for YMM looks enticing.

My outlook on YMM is a Buy at around $6.90 due to its prospects for improving profitability and reasonable growth in a rebounding Chinese road freight market.

For further details see:

Full Truck Alliance Performs Well As Chinese Road Freight Market Improves