YMM - Full Truck Alliance: Undervalued Gem With Solid Financials

2023-09-06 07:51:36 ET

Summary

- YMM posted impressive Q2 FY23 results with strong revenue and net income growth.

- The company's financials show a rise in revenues from freight brokerage and value-added services, with minimal increase in operating expenses.

- YMM's balance sheet is strong, with increased cash and minimal debt, making it an undervalued buying opportunity.

Full Truck Alliance ( YMM ) runs a digital freight platform. They connect shippers with truckers in China. YMM recently posted solid Q2 FY23 results with impressive revenues and net income growth. In my opinion, YMM is a great buying opportunity. I will analyze its technicals and financials in this report. I think YMM is undervalued, so I assign a buy rating on YMM.

Financial Analysis

YMM recently announced its Q2 FY23 results . All the figures are in Chinese Yuan. The net revenues for Q2 FY23 were RMB 2 billion, a rise of 23.4% compared to Q2 FY22. Higher revenues from the freight brokerage and value-added services were the major reason behind the revenue increase. The revenues from the freight brokerage service grew by 11.6% in Q2 FY23 compared to Q2 FY22. The expanded user coverage led to the growth in transaction volume, which benefitted the company’s freight brokerage service. The revenues from the value-added services grew by 27% in Q2 FY23 compared to Q2 FY22. Higher revenues from the credit solutions were the main reason behind the revenue rise in value-added services. In addition to a significant revenue increase, its operating expense in Q2 FY23 was just 0.5% higher compared to Q2 FY22, which is quite impressive.

Its net income in Q2 FY23 was RMB 608.9 million, which was RMB 12 million in Q2 FY22. Honestly, after looking at the numbers, I don’t think the financial results can get any better than this. I believe the result was fantastic, and I think the recovery of the transportation industry in China from the pandemic and lockdown has helped the company boost its revenues. And with the industry back on track, I believe YMM might continue to perform in the coming times. Additionally, the balance sheet of the company is looking quite strong. They had cash & cash equivalent of RMB 7 billion by the end of June 2023, which was RMB 5.1 billion at the end of December 2022. So, an increase in cash is a positive sign, and what is more impressive is that the company has minimal debt. So, the company is looking fundamentally quite solid.

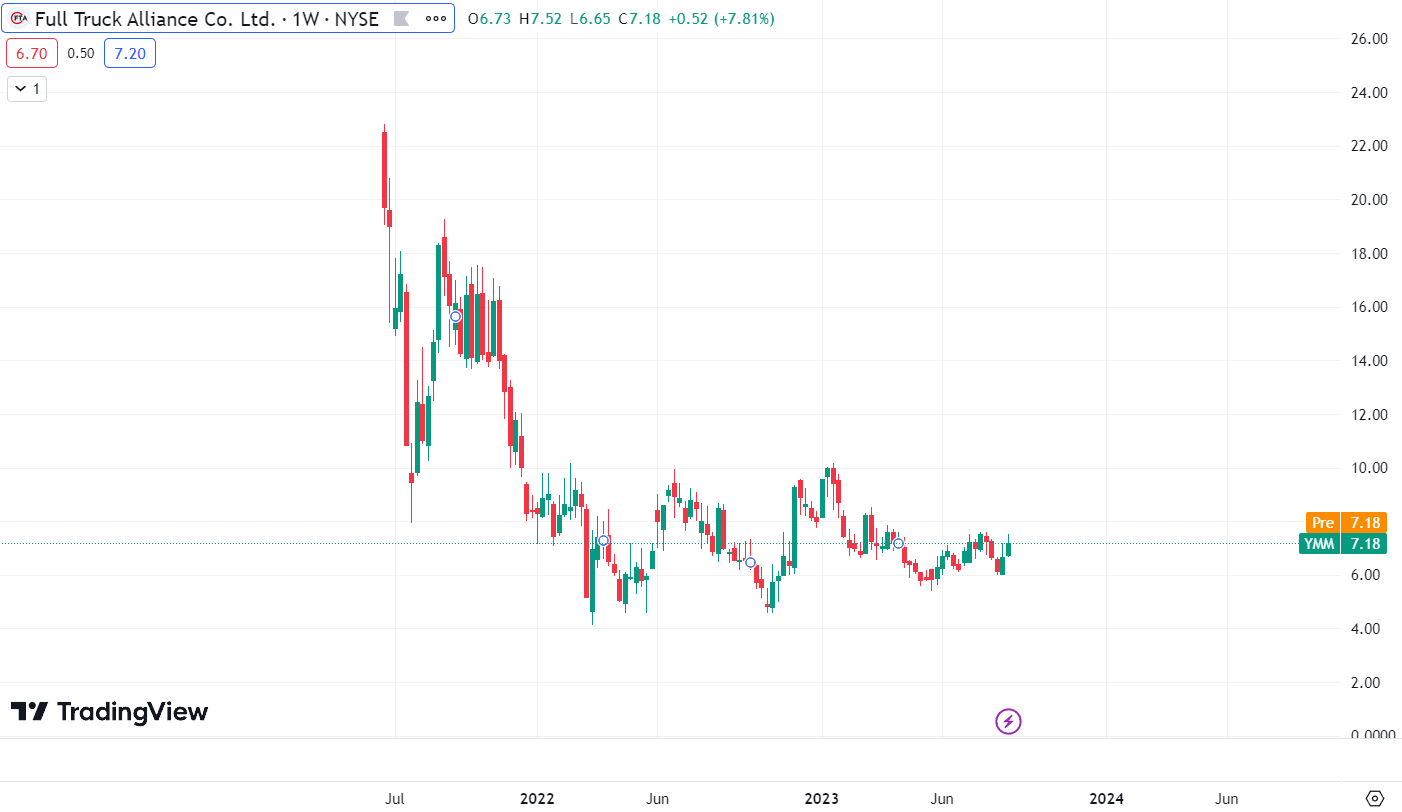

Technical Analysis

{kind=link}

YMM is trading at $7.18. The stock is down 63% from its IPO level, which I believe can be a great opportunity for bottom fishing because the price action here is positive and is showing early signs of trend reversal. The stock has made a double-bottom pattern, which is one of my favorite reversal patterns. The solid financial result can be the reason behind the recent positive price action. The stock followed a similar pattern in October 2022 and increased by 70% in three months. So, I believe the stock has great upside potential, and one can buy it at current levels. Hence, I assign a buy rating on YMM.

Should One Invest In YMM?

The company performed exceptionally well in Q2 FY23, and the company's outlook for the next quarter is positive. They are expecting their revenues to grow around 20% in Q3 FY23 compared to Q3 FY22. The freight and transportation industry in China is huge and is growing rapidly. China's freight and transportation market is expected to reach $1.13 trillion by the end of 2023 and around $1.54 trillion in 2029. The digital freight industry in China is increasing rapidly and is expected to grow at a CAGR of 24% till 2027, and YMM is among the top five market leaders. So, I believe YMM has a lot of potential to grow because even though the digital freight industry is growing rapidly, it still has a lot of market to capture. Until 2020, the digital freight industry could only capture 4% of the total freight industry in China. So, I believe the scope of the digital industry is huge. But with huge market opportunities, there is a risk for the company. With the growing market, many competitors are entering the digital market, even though YMM is among the five biggest digital freight companies in China. The market share that the big companies have is not huge. So, the increasing competition in this industry can be a concern for the company because to survive in the industry with huge competition can be a tough task, and to capture the market, the company might have to spend heavily and might also have to lower its commission rates to attract the customers. So this might affect the profitability of the company in the coming times. So this can be a concern. But for now, I think the company is in a great position.

In addition, if we look at YMM’s valuation. YMM has a PEG [FWD] ratio of 0.54x compared to the sector median of 1.73x, and it has a Price / Book ratio of 1.57x, which is lower than the sector median of 2.61x. So, I believe YMM is providing great value here. Their financial result has been solid, and they have a positive outlook. In addition, their balance sheet is looking quite strong, so getting a company at a low valuation with such positives is great. Hence, I believe YMM can be a great opportunity to provide solid returns in the coming times. Hence, I assign a buy rating on YMM.

Risk

Changes in political and economic conditions and the PRC government's stance on foreign exchange can all impact how much the Renminbi is worth in relation to the U.S. dollar and other currencies. Foreseeing future changes in the exchange rate between the U.S. and Chinese currency is challenging due to market forces, PRC policy, or U.S. government policy. The PRC government is still under intense international pressure to implement a more flexible monetary policy, which would cause the Renminbi's value in relation to the U.S. dollar to fluctuate more. The appreciation of the dollar against the Renminbi, on the other hand, would have a negative impact on their available U.S. dollar amounts if they choose to convert Renminbi into dollars in order to pay dividends on their Class A ordinary shares or ADSs or for other company-related activities.

Bottom Line

In my opinion, YMM is providing great value here. Despite performing well financially, their share price is still quite low, which I think is great because investing at the current level might provide great upside to the investors. The company’s valuation is also quite low, and the technical chart indicates a potential trend reversal, so after considering all the aspects, I assign a buy rating on YMM.

For further details see:

Full Truck Alliance: Undervalued Gem With Solid Financials