NVS - Gain Therapeutics: Undervalued Based On Drug Development Platform And Lead Parkinson's Asset

2023-05-31 05:55:18 ET

Summary

- Gain Therapeutics is a biotechnology company focused on drug development powered by its SEE-Tx™ target identification platform, which identifies and optimizes binding sites on biological targets that have never before been targeted.

- The company has a potential blockbuster entering a phase 1 clinical trial and several AI drug discovery and gene therapy comps valued in the billions of dollars.

- Gain Therapeutics is significantly undervalued compared to its competitors, and its management and board, consisting of seasoned biotech entrepreneurs and dealmakers, are expected to maximize the company’s value.

There’s a lot of buzz these days about AI and it's no secret about large companies like Google ( GOOG ), well-backed VC darlings like Atomwise, and Big Pharmas such as Novartis ( NVS ) collaborating with Microsoft ( MSFT ) for AI-driven drug development. There are benefits and drawbacks to various approaches to accelerating and improving drug discovery and development, and multiple technologies will likely play a role in the future of pharma R&D, unlocking biology’s unknowns and refining our knowledge of the human body and pathophysiologies.

In this article, we will highlight AI drug discovery-related Gain Therapeutics' ( GANX ) platform and lead assets, which we believe have unique aspects and are significantly undervalued, a market valuation disconnect that may be ameliorated as Gain’s outstanding management moves its lead asset forward and inks drug development deals with larger biopharma companies utilizing Gain’s drug discovery platform, SEE-Tx. This is a well-proven business model with competitors/similar companies inking development deals worth billions in “biobucks” (upfront, milestones, royalties) and subsequently worth hundreds of millions or billions in market capitalizations, despite biotech companies currently enduring the worst biotech bear market ever . We believe Gain is highly undervalued and its management and board, consisting of seasoned, successful biotech entrepreneurs and dealmakers, will maximize the company’s value.

Overview

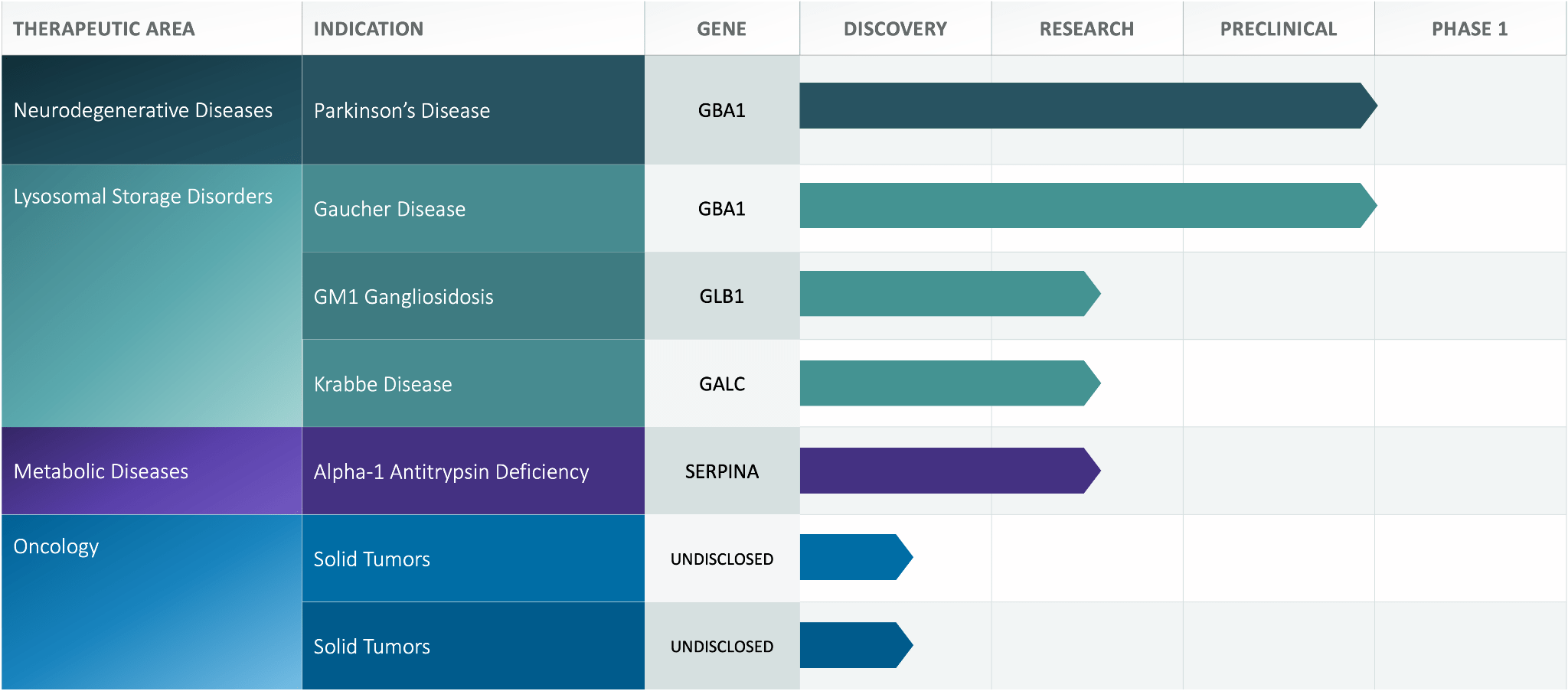

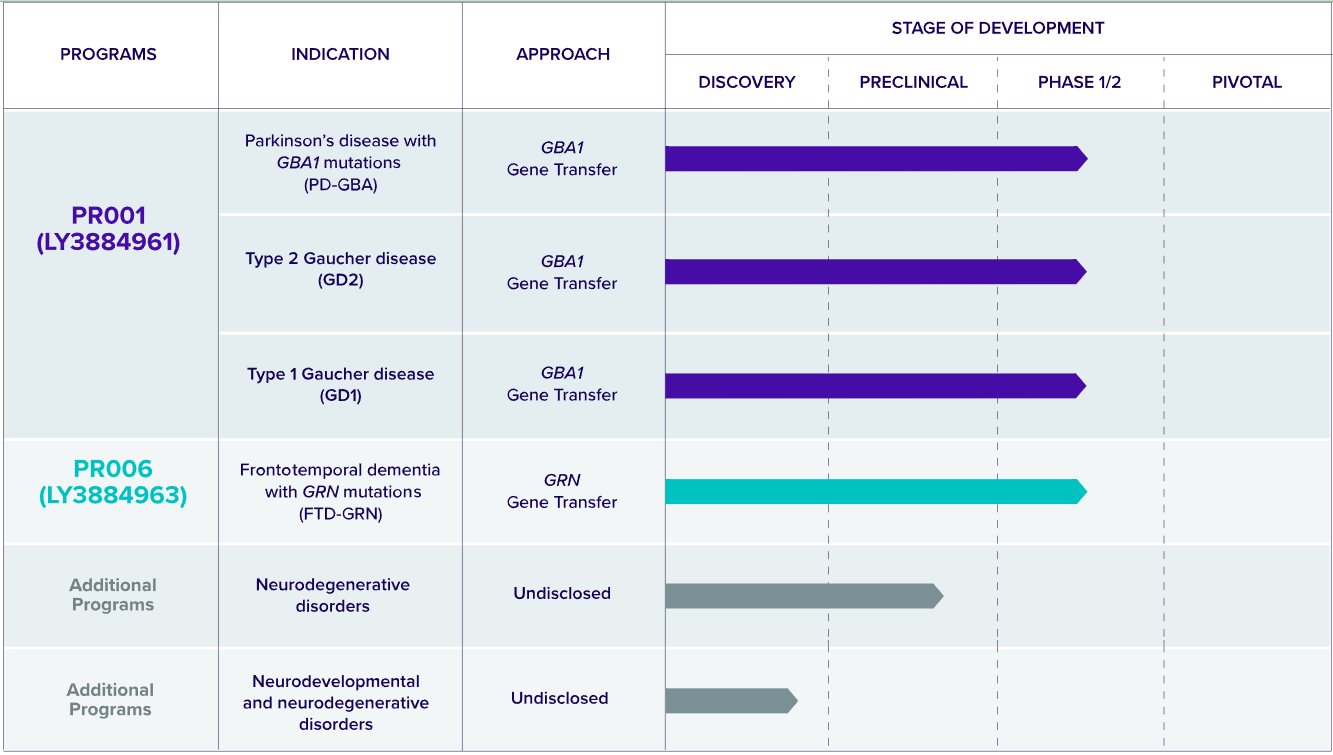

Gain Therapeutics is a biotechnology company focused on drug development powered by its SEE-Tx™ target identification platform. The company identifies and optimizes binding sites on biological targets that have never before been targeted. These include lysosomal enzymes for lysosomal storage disorders (LDSs), and kinases in oncology that are difficult to specifically target. The company has an early-stage but moderately broad pipeline including various rare diseases and Parkinson’s, which shares a target with its lead rare disease indication, Gaucher’s disease. This asset is particularly promising, but more on that later.

{kind=link}

Gain's Pipeline (Gain Therapeutics Website)

There’s more to the company than meets the eye when looking at the pipeline graphic. Management is highly accomplished and their discovery platform is similar to but unique from highly sought-after drug discovery platforms such as Vividion’s, which was bought by Bayer ( OTCPK:BAYRY ) for $1.5 billion, plus $500 million in milestones. One of the reasons Vividion is so highly valued is that its platform enables the development of drugs that bind to “undruggable” targets. About 90% of proteins in the human body are considered undruggable due to a lack of an addressable binding site. Therefore there may be proteins that are understood to drive disease progression but are unable to be exploited by drugs. Vividion’s platform uses a covalent bonding approach (by screening for cysteine sites on proteins). Unlocking the potential to target many undruggable targets undoubtedly drove Vividion’s value. Gain’s SEE-Tx finds ways to target undruggable targets but arguably with more finesse by focusing on allostery (and not necessarily being constrained to covalent bonding which is typically thought of as irreversible), but it appears the market hasn’t made this connection yet.

We believe Gain’s pipeline and its platform are highly valuable.

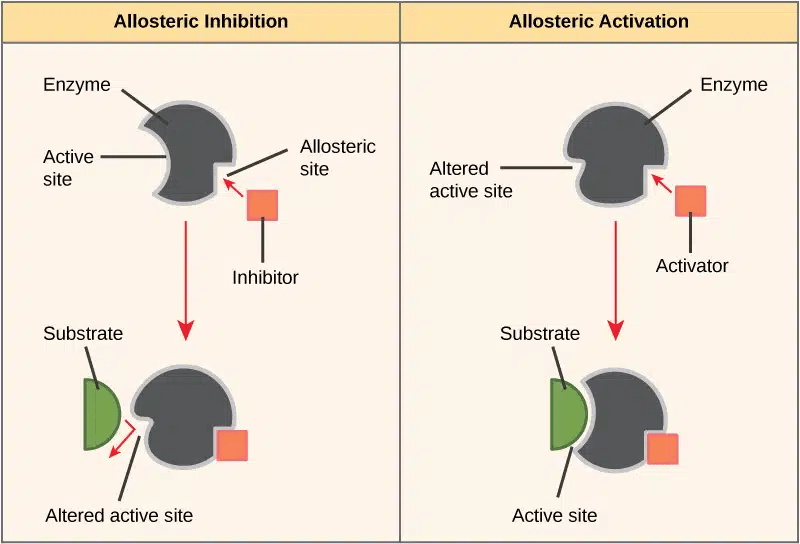

Allosteric Binding

Gain is using its SEE-Tx platform to focus on allosteric binding sites on “undruggable” targets. The reason this allows for more finesse in designing drugs is that allosteric binding sites are basically sites on a protein that don’t compete with the proteins known, normal function. It binds to a different site than the protein's active site and modulates the protein’s activity from that site. This can be used to turn the desired activity up or down, depending on the allosteric site, and affinity, and how the protein changes shape after allosteric binding has occurred. See below.

{kind=link}

Teach Me Physiology

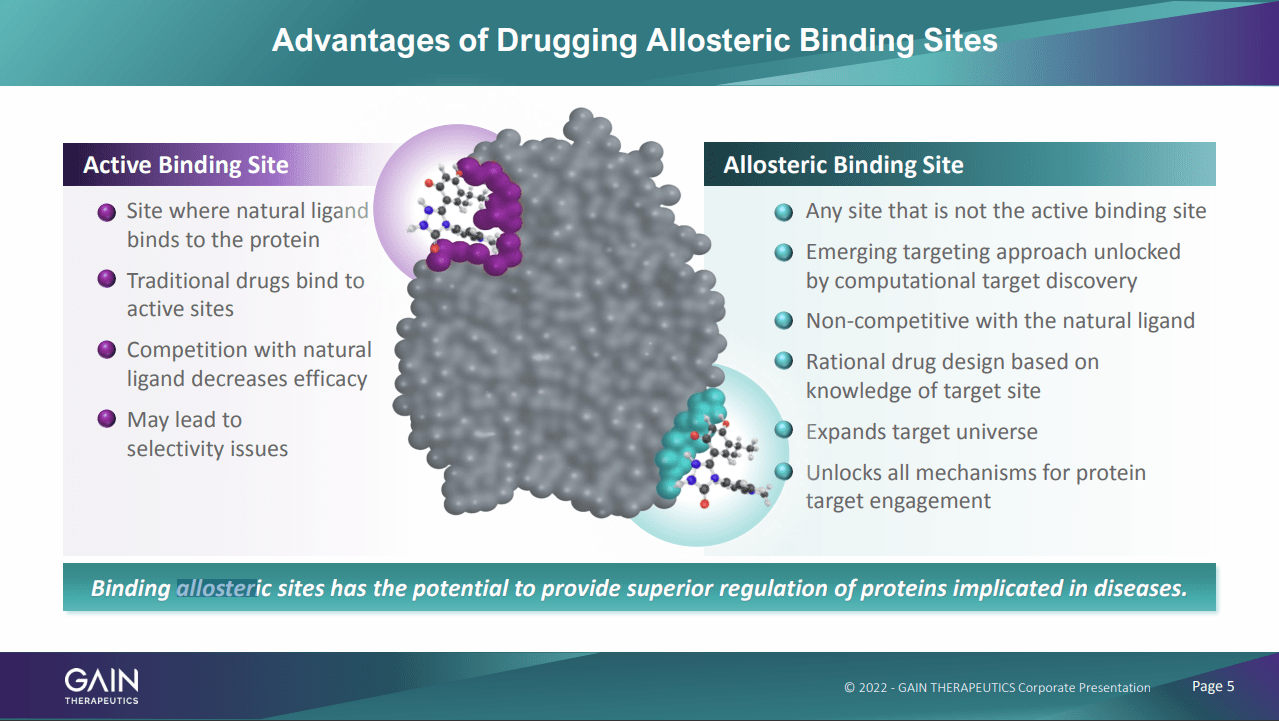

Put simply, allostery allows for proteins to be turned “up or down” instead of “on or off.” There are other advantages, and Gain has a nice graphic on these points:

{kind=link}

Advantages of Drugging Allosteric Binding Sites (Gain Therapeutics Investor Presentation)

SEE-Tx: How It Works

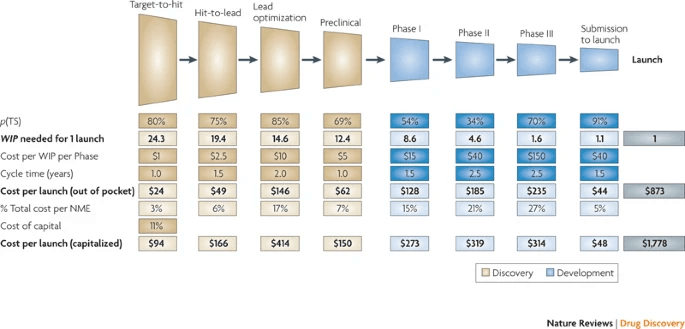

Drug discovery platforms are, in general, used to accelerate drug discovery while ideally increasing the accuracy of and decreasing the cost of drug development. Gain’s platform focuses on the early stages of drug discovery where targets are identified and a lead drug candidate is desired. This process is typically started with high throughput screening ((HTS)) by testing a massive number of chemicals against a target. SEE-Tx works by using proteins with known and published structures, and a physics-based program run through supercomputers, to identify allosteric sites and virtually screen drug candidates. This requires no machine learning, just a protein structure, and then experimental validation at the end of the process. Recently, AlphaFold was made open source which effectively doubles Gain’s potential targets as they don’t need 3D crystal structures anymore.

The program has shown ~100x target hit rate improvement (from 0.1% to ~10%) over HTS while reducing the typical lead time of R&D efforts for SEE-Tx-generated lead compounds from about 2.5 years down to about 3 months. This is estimated to save drug developers about 2 years of work and a significant amount of money in the process while selecting novel targets in an allosteric manner. The chart below gives one an idea of the cost and time involved in reaching a lead compound.

{kind=link}

Nature Reviews (How to improve R&D productivity: the pharmaceutical industry's grand challenge)

The discovery platform is just part of the story for now as it hasn’t been fully monetized with pharma partnerships. In the case the drug discovery platform part of the bull thesis is wrong, we believe the company’s lead asset, GT-02287, is significantly valuable.

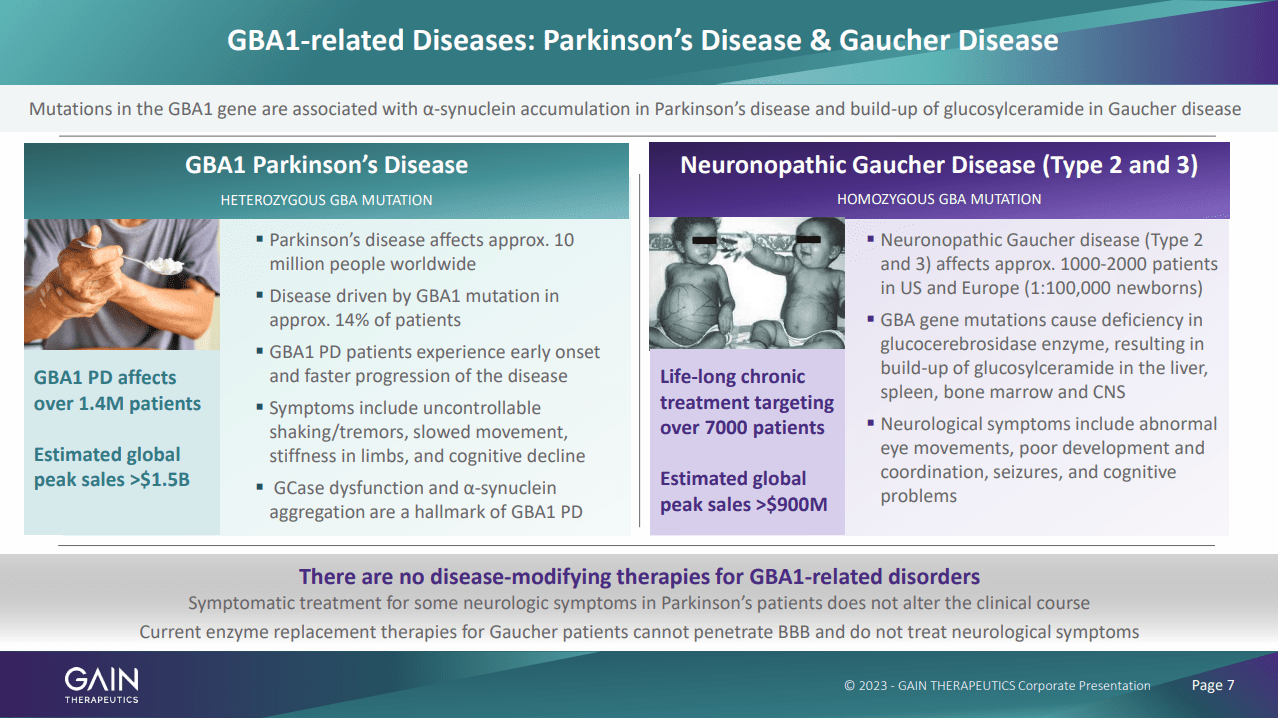

GT-02287: GCase/GBA1-targeting Gaucher’s and Parkinson’s

Gain’s lead asset, GT-02287, which was discovered using SEE-Tx, just completed IND-enabling tox studies as mentioned in the recent 10-Q and expects to submit a regulatory package for phase 1 in Parkinson’s in Australia. The drug is being developed for a rare LSD, Gaucher’s disease (Type 2 and 3), and a multi-billion dollar neurodegenerative chronic disease, Parkinson’s disease. Presumably, the dual use case of the drug is why Gain chose this target. Global peak sales estimates are $900 million for Gaucher’s, and $1.5 billion for GBA1 Parkinson’s. Notably, the drug may work on a larger set, if not all Parkinson’s patients.

{kind=link}

Gain Therapeutics Investor Presentation

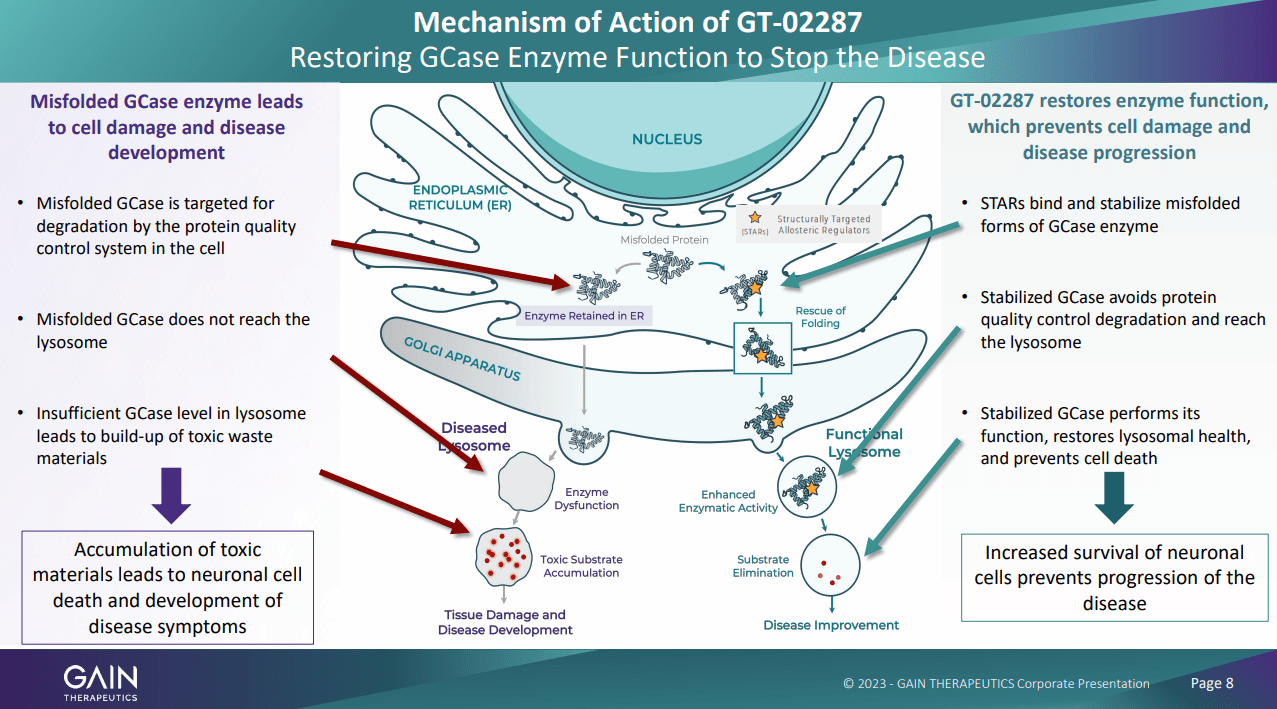

The drug works by stabilizing and increasing working levels of GCase, a lysosomally active enzyme essential for the degradation of complex lipids and the turnover of cellular membranes. Loss of GCase function is a hallmark of Gaucher’s disease as Gaucher’s is caused by GBA mutations. GBA encodes GCase, and so the disease is driven by a lack of GCase function as well as buildup of misfolded GCase .

{kind=link}

Gain Therapeutics Investor Presentation

Current solutions include ERT (enzyme replacement therapy) which does not correct for the existing misfolded GCase nor does it correct severe brain involvement in Gaucher’s Type 2 and 3. Thus the drug can work as an orally-bioavailable “ERT,” working to stabilize and increase GCase levels across different GBA mutations.

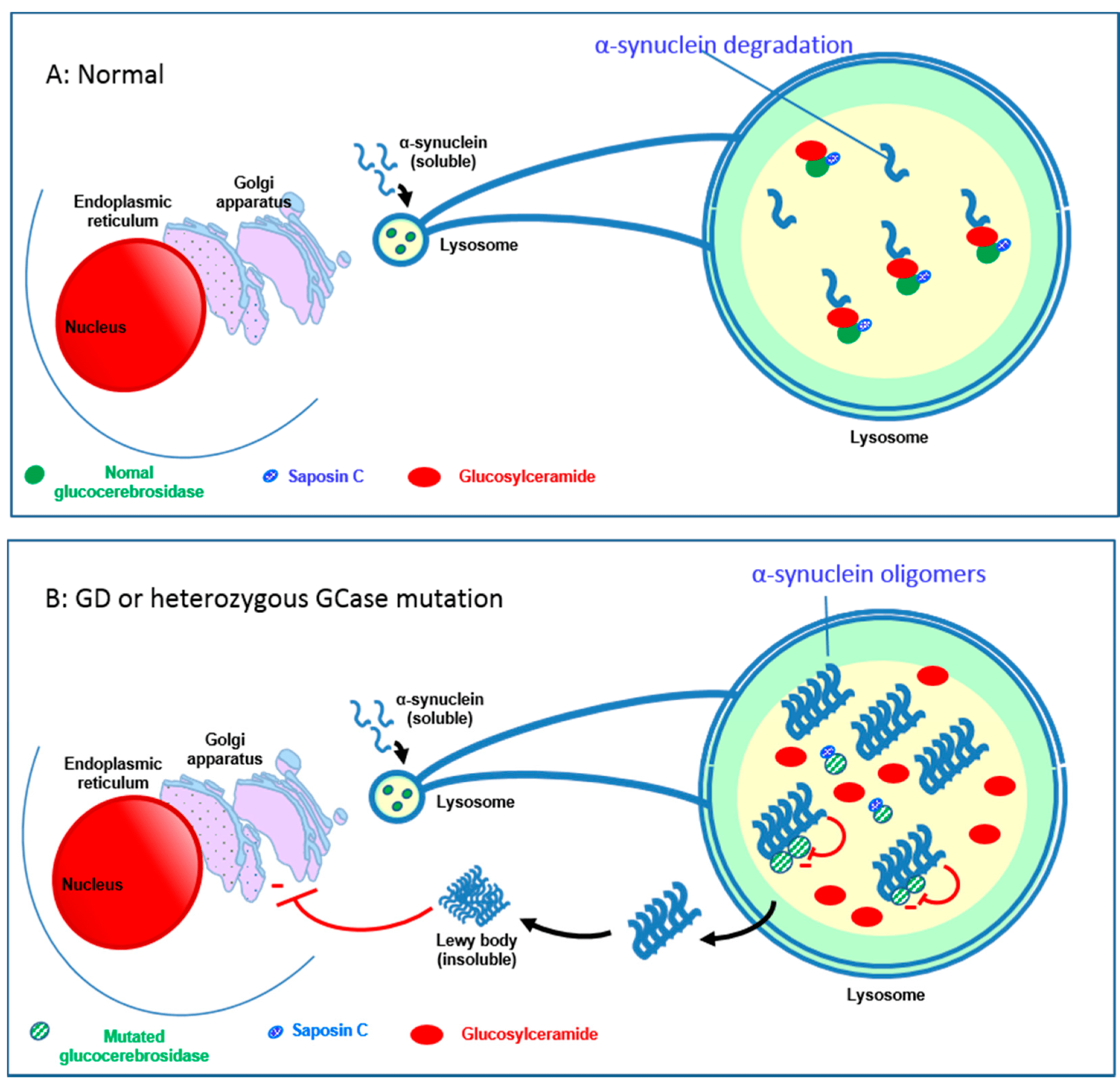

Notably, GCase activity is also decreased in Parkinson’s, driving neurodegeneration to some extent. A lack of GCase forms a feedback loop with alpha-synuclein aggregates (aka Lewy bodies, a hallmark of Parkinson’s). Alpha-synuclein drives GCase levels lower, and the lack of GCase also increases these Lewy bodies. This may propagate Parkinson’s disease development.

{kind=link}

A Review of Gaucher Disease Pathophysiology, Clinical Presentation and Treatments

About 5-15% of Parkinson’s patients are estimated to have a GBA mutation, and certain studies have indicated that 56% of Parkinson’s patients have at least one LSD variant, with 21% carrying multiple alleles. GBA is the most common. GBA mutant Parkinson’s patients are also known to have more severe , early-onset disease.

{kind=link}

Gain Therapeutics Presentation, Oppenheimer Event

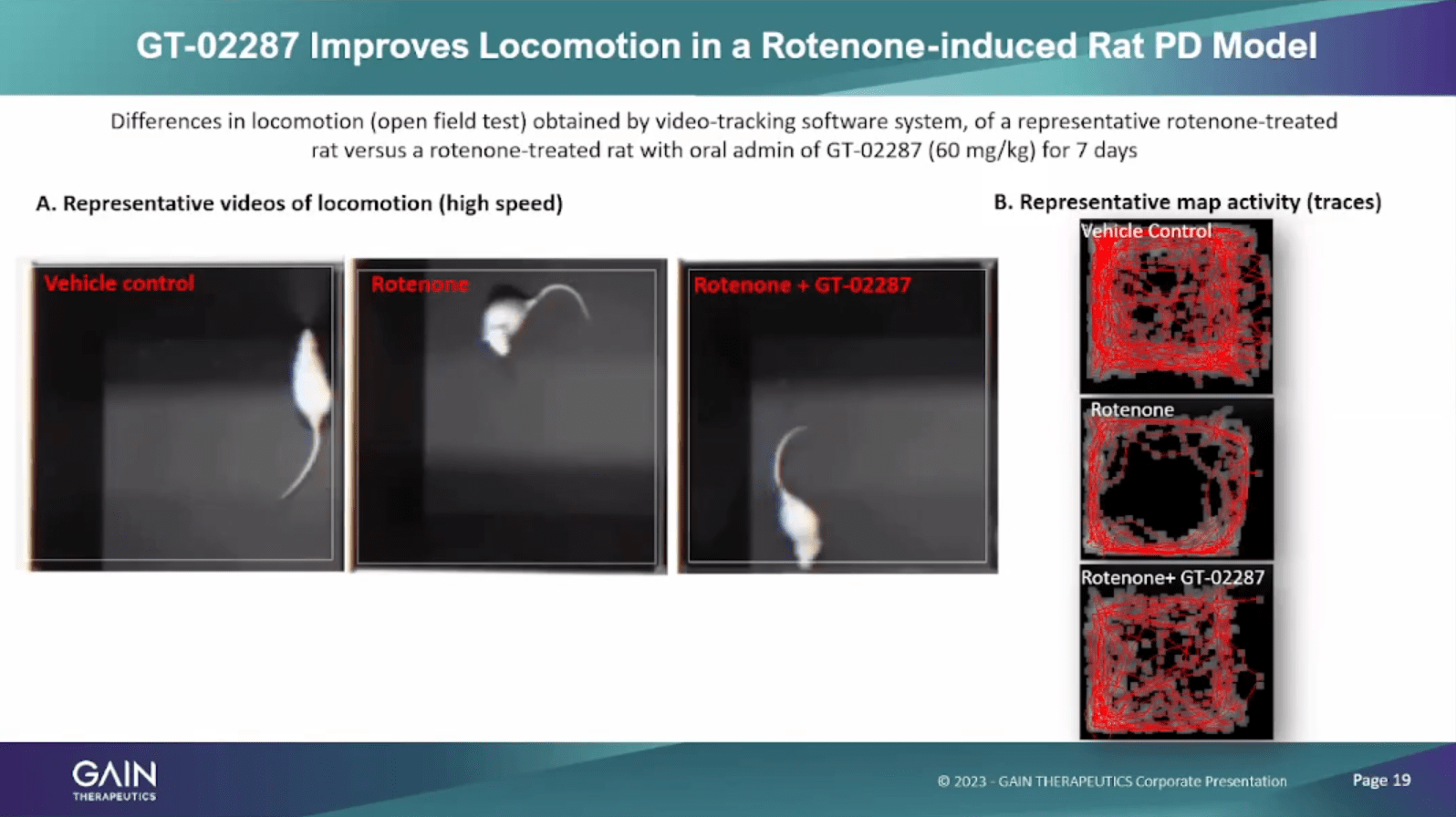

This potential to address more than just GBA1 Parkinson’s is supported by Gain’s work in rotenone-induced (toxin-induced, depleting dopamine) Parkinson’s models, which are unrelated to GCase function when compared with their CBE-induced (GCase inhibitor) models, and GBA mutant IPSC models (derived from GD patient neurons). The bottom line is that they’ve shown positive drug activity across different preclinical models (including rat and human) and endpoints including biomarkers and how rats are moving. These preclinical results are robust, showing:

Increased GCase enzyme levels, depleted toxic substrate (GlcCer), improved lysosomal function, increased trafficking to the lysosome, depleted alpha-synuclein, and reduction of inflammatory cytokines (in IPSC models done by a key Pfizer ( PFE ) advisor) , and Depletion of toxic substrate and alpha-synuclein, increased survival of dopaminergic neurons, increased dopamine levels, reduced inflammatory cytokines, and improved locomotion (in rotenone and CBE rodent models) .

The locomotion results are particularly striking, especially given they were part of the rotenone model.

{kind=link}

Gain Therapeutics Presentation

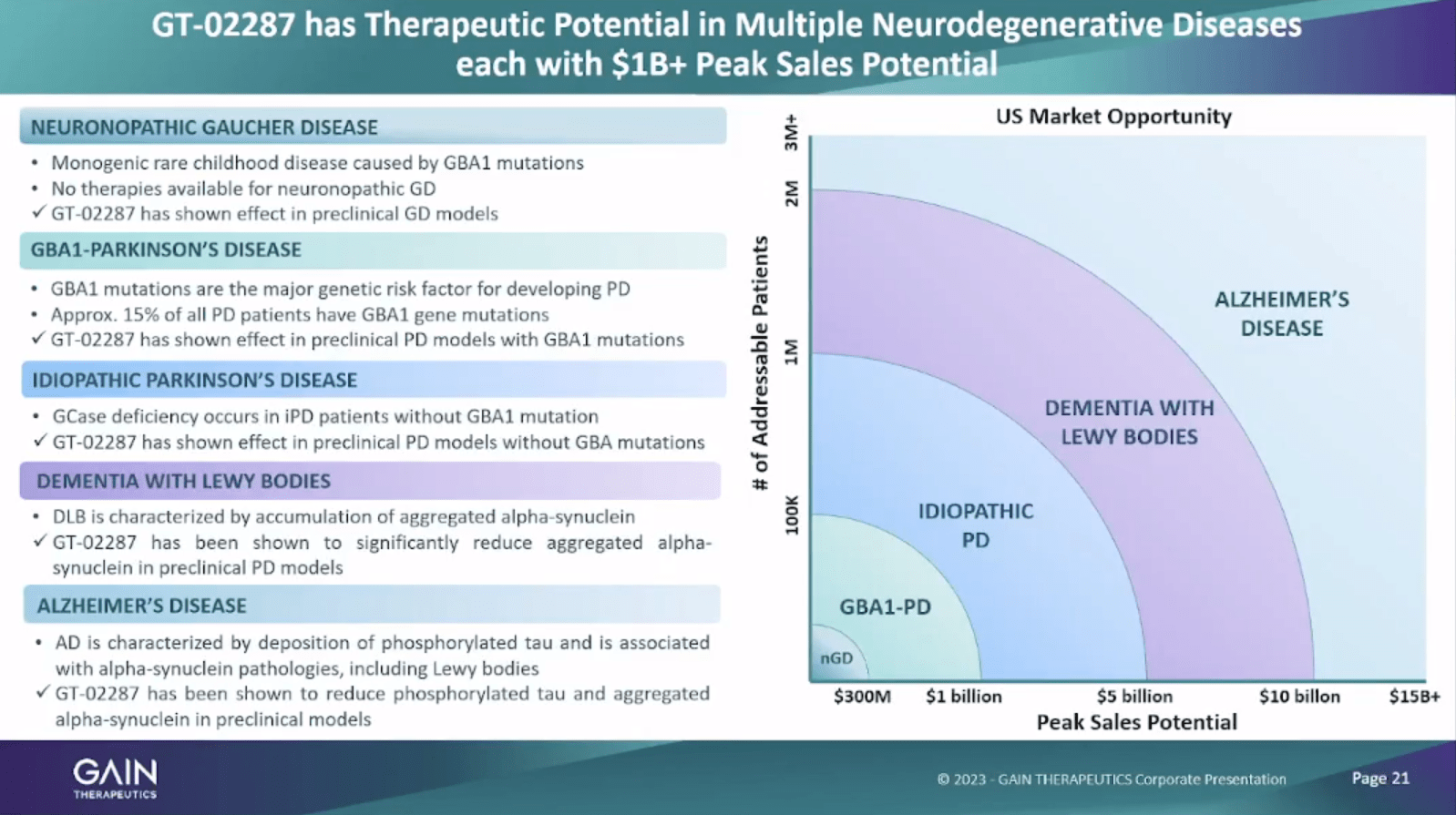

There’s also the potential for the drug to help with Alzheimer’s ( AD) treatment, but the promise and chances of success are lower for this indication compared with PD and Gaucher’s, in my opinion, given decades of failed AD trials, controversial new AD drugs from Eli Lilly ( LLY ) and Biogen ( BIIB ), all pointing to a lack of understanding on AD pathogenesis and how to treat the disease, making a significant impact beyond slowing cognitive decline.

Either way, GT-02287 has morphed from a rare disease drug into a drug for various neurodegenerative diseases over time and it has the potential to be a mega-blockbuster able to improve the brain’s recycling capacity, though its development is still very early. Fortunately, there is a top-notch team leading Gain.

Select Key Personnel

Gain’s team has an impressive track record and I’ll leave it at that.

Matthias Alder

CEO and Board Member Matthias Alder took over from the company's former CEO and current board member, Eric Richman, in 2022 when Richman, a highly successful biotech investor, stepped down as CEO, a position he only took in the first place due to how promising he believed the company was. Alder has billion under his belt in pharma licensing and M&A deals and is highly qualified to lead the company’s business development efforts. The management team has $13 billion in total transactions as a whole. What is telling is Alder’s employment contract which was published when he was initially hired that includes large performance incentives to close a deal (100,000 RSUs) with a large pharma company or equivalent.

Dr. Khalid Islam

The board has aggregated $30 billion in deals, and Dr. Islam, their Chairman, being involved is exciting. Apparently, he was instrumental in the sale of Immunomedics to Gilead Sciences ( GILD ) for $22 billion.

Valuation: Comps

It's difficult to use traditional methods to value an early-stage biotech company with a very valuable drug discovery platform because traditional risk-adjusted discounted cash flow valuations or peak sales multiples don’t mean much when the company may be pursuing business by inking partnership deals to leverage its platform beyond its own pipeline and balance sheet’s capabilities.

Therefore, the company can be valued like a hybrid traditional biotech for its lead asset and also as an AI drug discovery company using comps. So, we use a blend of peak sales multiples and comps for our valuation. There’s a lot of focus on comps in this section, and that’s why—it's difficult to value a drug discovery platform where the potential revenues (milestones, royalties) from various licensed products are not yet known.

Comps: AI Drug Discovery

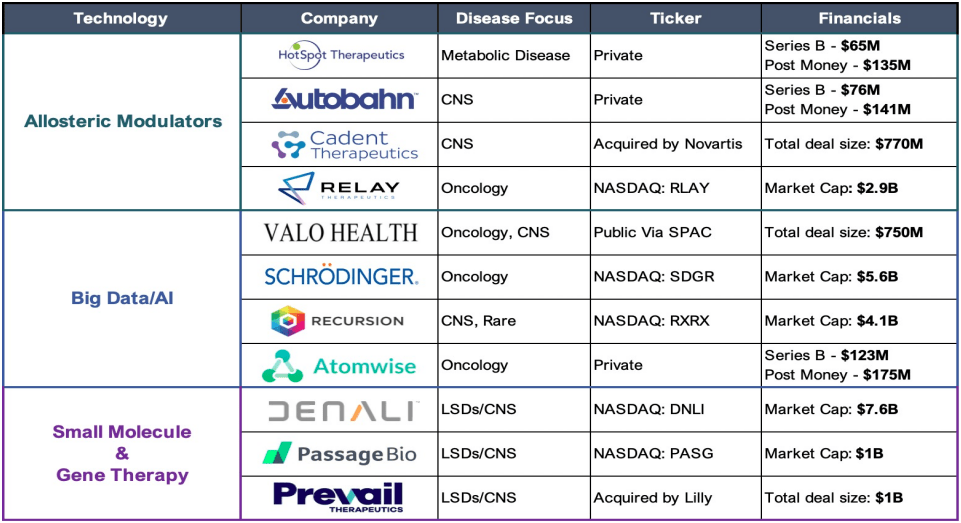

There are quite a few large and small companies with a wide range of approaches using AI, machine learning, big data, or simply intensive computation to find targets or drugs, design trials, etc. However, there are simply too many of them to review and their valuations vary. However, the ones with approaches and pipelines that advanced similarly to Gain’s are typically in the billions in market capitalization or value.

Gain provided a comp table in one of their presentations which is fairly reasonable, but certain companies in my opinion are more worth comparing than others. It appears that the AI/drug discovery comps that more closely match Gain dwarf it in valuation.

{kind=link}

Gain Therapeutics Presentation

First, Relay Therapeutics ( RLAY ) is a good comp for Gain as they use their platform “to effectively drug-protein targets that have previously been intractable or inadequately addresses” using their computationally powered discovery platform. All of their pipeline candidates are phase 1 or earlier-stage cancer-focused drugs. Relay currently trades for $1.34 billion ($460m EV).

Recursion Pharmaceuticals ( RXRX ) is another good comp that is trading for $1.7 billion ($1.3 billion EV). They use a massive experimentation machine learning approach, focusing on rare diseases and cancers. Their pipeline, however, is a bit more advanced than Relay and Gain, probably a few years ahead.

Schrodinger ( SDGR ) is a $2.6 billion company ($2.16 billion EV) using a physics-based drug development platform. It has a more extensive pipeline, more collaborators, and a machine learning element to its methods. It’s also using the platform for materials science for other sectors. However, Gain is worth about 1/50th of Schrodinger despite similar capabilities.

There is also theoretically the potential for Gain to improve aspects of their physics-based See-Tx platform to include machine learning or AI elements or refine aspects of its computations further. The beauty of their current platform is its accuracy in using existing data. Gain’s Perspectives page explains that:

AI algorithms need experimental data and previous knowledge on the system to train, parameterize and build the predictive models.

On the contrary, SEE-Tx methodology is based on first principles, meaning it doesn’t need any training data or previous knowledge on the system, which makes it applicable to any target with an available 3D structure.

Additionally there is no uncertainty in the datasets with SEE-Tx . The 3D structures have been well documented in literature and the protein’s role in disease has been validated. As data sets improve, AI approaches will no doubt as well-but there will always be some degree of uncertainty in the training site.

SEE-Tx is a solution to the inefficiencies of the drug discovery and development process by greatly reducing the time and cost in discovering novel targets. Currently, there is no known AI algorithm able to induce the opening of hidden or “cryptic” binding sites. This requires complex and specific coordination of ligand effects on the protein surface which can only be done with SEE-Tx.

The last comp we will list is a company recently acquired by Bayer, Vividion Therapeutics. Vividion was considering an IPO in 2021 and was bought before that process took place with Bayer paying $1.5 billion upfront and $500 more in milestones. Although Vividion’s pipeline looks large now, at the time of acquisition the graphic was much more modest.

Vividion August 2021 S1

Vividion’s S-1, August 2021 , shows net cash of $22 million, 108 employees, and two impressive collaborations. Their library and platform come from researchers at Scripps. The company focused on finding candidates for undruggable targets and its platform uses chemoproteomic screening technology along with its chemical library to find binding sites on targets, focusing on cysteine-reactive groups. Cysteine is unique and can make disulfide bonds, which can technically be reversed under reductive conditions, but generally, these would be considered irreversible covalent reactions. According to Vividion, many of these drugs/targets are allosteric sites. One of the selling points of their methods was the ability to globally test drugs for off-target binding. Gain has promising assets that are further in development than Vividion’s (at the time of acquisition). They both use structural computational methods to aid in the rapid discovery of compounds that can selectively target the 90% of “undruggable” targets in the human body.

Comps: Parkinson’s Disease/Gene Therapy

Gain’s lead asset competes with gene therapy minus the costs and complications of those cutting-edge technologies. One beneficial aspect of GT-02287 is that it not only increased GCase activity but will reduce misfolded GCase, something that gene therapy may not do. Misfolded GCase causes cellular dysfunction, so the drug may be beneficial in combination with gene therapy or may outperform gene therapy in theory. That being said, there are some close comps in the GBA gene therapy space as well as Parkinson’s. The first one is Prevail Therapeutics.

{kind=link}

Prevail Therapeutics Website

Eli Lilly acquired competitor Prevail Therapeutics in December 2020 just days after it received orphan designation for frontotemporal dementia ((FTD)) from the European Commission and dosed the first patient in its phase ½ AAV9 gene therapy, called PR006, for FTD. This deal was for an aggregate of approximately $1.040 billion (with $880 million upfront), while the company was carrying $114.3 million in cash as of its last quarterly report. Thus the approximate EV is $890 million. This acquisition was in a much stronger biotech market as was Vividion’s; however, Gain is now in a similar phase of development in the two exact same lead indications (Gaucher’s and Parkinson’s) with a similarly-sized pipeline with a drug discovery platform. It’s a very good comp, in our opinion, and one that in theory derisks Gain’s endeavors as the company has had success with GCase through gene therapy in many of the same types of experiments.

Voyager Therapeutics ( VYGR ) is another good comp in the gene therapy and CNS space, with a market cap of ~$575 million and a ~$275 million EV. The company has entered into a partnership with Neurocrine ( NBIX ) in which they received a $39 million equity investment from Neurocrine at a significantly higher valuation than Gain, with Neurocrine paying them an aggregate of $175 million total upfront cash (including the investment) for their GBA1 Parkinson’s program and three new gene therapy programs, which are undisclosed. The deal also included $1.5 billion in milestones as well as tiered royalties, program funding, and some other options. The company focuses on using its TRACERTM AAV Capsid Platform to address CNS-targeting difficulties of gene therapy with improved dosing to the CNS. Since Gain optimizes brain-penetrant small molecules to improve these misfolded proteins in genetic diseases, the approaches are comparable.

This suggests that Gain might be able to pull off a deal for their GBA1 Gaucher’s and Parkinson’s programs and leverage See-Tx for the other targets. Voyager’s GBA1 Parkinson’s program is also in the preclinical stage and they have stated they expect to file its IND in 2025 . However, since that announcement, they have partnered with Neurocrine and so this timeline may have been accelerated. Either way Gain is arguably ahead of them as they have completed tox studies which Voyager stated they were going to do in 1H 2024.

Blended Valuation

We use a blended approach to value GANX shares, weighing 50% using a discounted, risk-adjusted peak sales multiple for Gain’s lead asset, and weighing 50% using the average comp from the list above. Gain compares favorably to its peers on EV.

| Company |

| Enterprise Value () |

| Relay |

| 460 |

| Recursion |

| 1300 |

| Schrodinger |

| 2160 |

| Vividion |

| 2000 |

| Prevail |

| 890 |

| Voyager |

| 275 |

| Average Comp |

| 1180 |

| Gain |

| 40 |

For the discounted peak sales multiple, we use a 15% discount rate, a 10% probability of success Parkinson’s and Gaucher’s, worldwide peak sales of $2.4 billion, a peak sales multiple of 4, and peak sales reached in 12 years. The result is a $180 million valuation for Gain’s lead asset.

Blending the two approaches, we arrive at a value of $680 million EV, or $56/share using 12.1 million shares outstanding .

Financials

As of March 31st, 2023, Gain had $17.8 million in cash and short-term investments. The company currently burns $5 million per quarter, so they have about 9 months until they might run out of cash. They are also starting their phase 1 Parkinson’s trial, so this is concerning. However, the company has been well supported by grants, the Michael J. Fox Foundation (of which David Einhorn, an almost 5% holder of Gain, is on the board), and recently received a $2.8 million grant for this program. The company is also conducting this trial in Australia and so it is eligible for a 43.5% refundable tax offset . However, going forward, if the company doesn’t secure nondilutive funding via partnerships, it will likely need to turn to the capital markets to raise money.

Risks

Gain is an early-stage, pre-revenue biotech. With that comes risks including but not limited to dilution, running out of money, clinical and preclinical study failures, and high market volatility.

Speculation: Partnerships

Many of the other AI/drug discovery companies are focusing on cancer. Gain has undisclosed oncology targets listed in its pipeline slide. We suspect that partnership opportunities may arise in the oncology arena. After all, Sam Broder, former head of NCI under Reagan, spoke at GANX R&D day last year . He explained how allosteric binding sites offer potential benefits such as greater specificity and selectivity of activity, such as binding a specific kinase and not having to deal with off-target effects related to other kinases with similar active sites.

Conclusion

Gain Therapeutics is furthering drug development in a unique way and its SEE-Tx platform may be useful for a larger pharma company. The company also has what is shaping up to be a very valuable early-stage asset. Given the company’s management has a strong track record in business development and comps have inked large deals with big pharma, we believe the company will monetize SEE-Tx and also advance its lead asset. With comps valued in the billions, Gain shares appear significantly undervalued. This undervaluation may change if the company ramps up its business development and licenses out assets, SEE-Tx, or is sold in its entirety.

For further details see:

Gain Therapeutics: Undervalued Based On Drug Development Platform And Lead Parkinson's Asset