GAU - Galiano Gold: After A More Than 100% Gain There Are Better Opportunities In The Sector

2024-01-17 17:15:30 ET

Summary

- The bullish thesis on GAU has played out as expected.

- Recent news of Galiano acquiring Gold Fields' stake in the Asanko mine has led to a spike in GAU's stock price.

- Net cash will be far lower than before once the deal closes this quarter, and the Asanko mine's cash flow is back-end loaded.

- GAU is still heavily discounted, but many stocks in the sector are trading at similar or even lower valuations and offer more diversification and/or a lower-risk mining jurisdiction.

In my March 2023 article on Galiano Gold Inc. ( GAU ), I discussed how investors were getting the company's 45% stake in the Asanko gold mine (Ghana) for free, as GAU had ~US$102 million in cash, gold, and receivables and no debt, and a market cap of US$103.5 million.

My bullish thesis highlighted how Galiano was trading at cash value, yet recent news showed a much-improved outlook for the Asanko gold mine, which the market had yet to acknowledge.

At $1,800 gold, Galiano's 45% economic interest in Asanko would generate after-tax free cash flow of US$275 million for GAU and had an after-tax NPV of almost US$200 million, or roughly $1 per share of value. GAU was trading at just under $0.50, and after taking into account the cash on hand, the fair value was ~$1.50 per share, or more than 3x its price at the time.

Since then, the bullish thesis has played out as expected. GAU has increased by over 110%, smashing the performance of the HUI (an index of gold mining stocks), which has returned just over 4%. GAU has spiked over the last month as investors reacted positively to the news of the company acquiring Gold Fields' ( GFI ) 45% stake in the Asanko mine, which I forecasted would happen. While there is still value in GAU, there are now better risk/reward opportunities in the sector. As a result, GAU is a sell. Let's discuss why in more detail.

It's been my argument for the last few years that the Galiano/Gold Fields JV ownership of Asanko should be consolidated, as I saw no reason for GAU to remain a public company. Galiano either needed to be acquired or purchase Gold Fields' 45% stake. The latter would be bullish news, too. I didn't believe the joint venture would continue under its ownership structure, and as mentioned in an article last October, I leaned towards GAU buying out GFI's stake as I wasn't convinced the cash flow was enough for Gold Fields or that it would be willing to pay close to fair value for GAU.

In late December 2023, GAU announced that it was acquiring Gold Fields' 45% stake in the Asanko mine (the government of Ghana owns the other 10%). The deal was applauded as it only requires GAU to issue US$20 million in shares upfront, with GFI also keeping its share (or US$65 million) of the JV's cash position. Over half of the total consideration is deferred and as follows:

- US$25 million on or before December 31, 2025

- US$30 million on or before December 31, 2026

- A contingent consideration of US$30 million once 100,000 ounces of gold are produced (on a 100% basis) from the Nkran deposit, which isn't expected to occur until the end of 2028.

GFI also receives a capped 1% NSR royalty on the Nkran deposit, which only goes into effect once 100,000 ounces are produced.

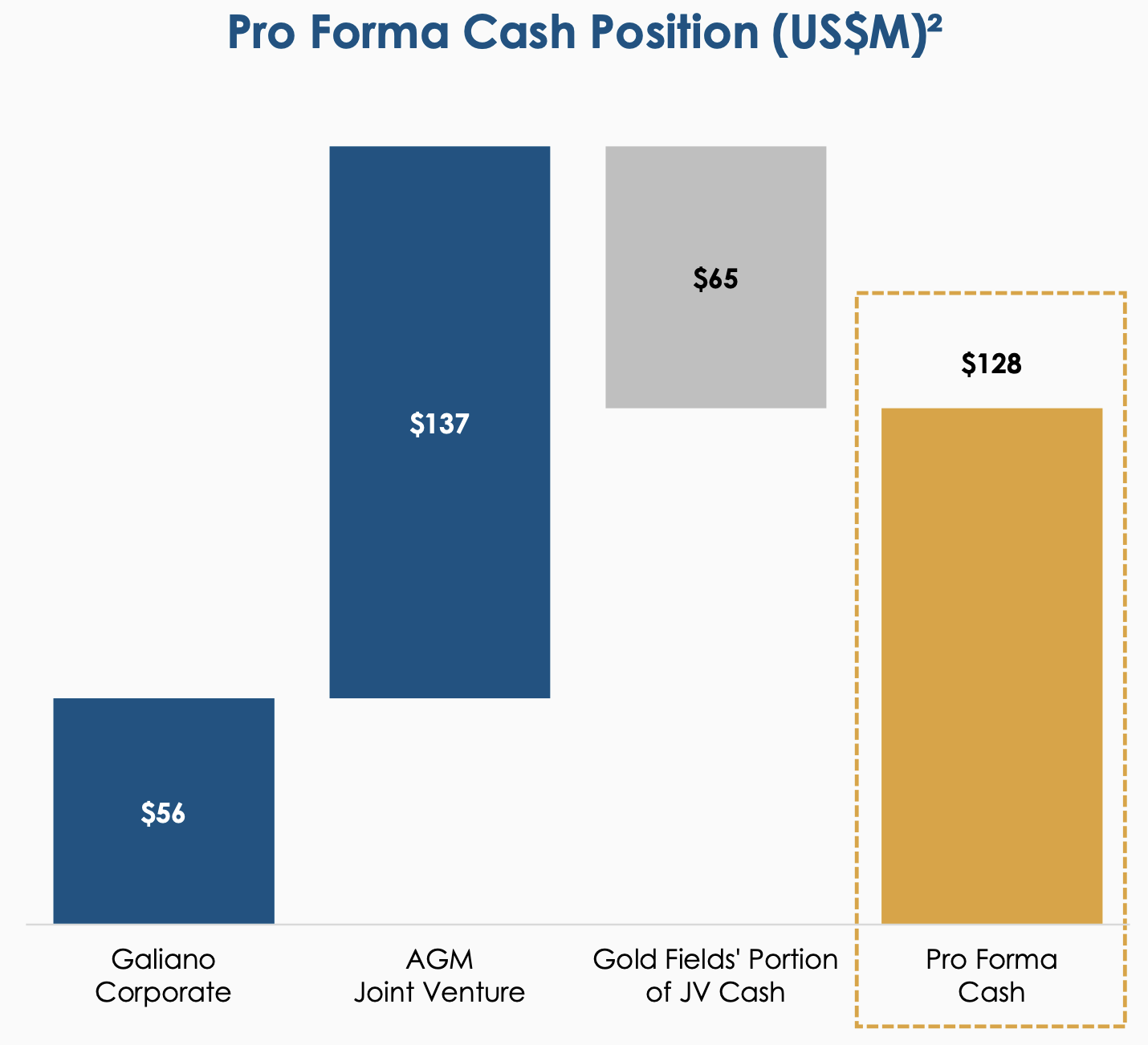

This deal gives Galiano 90% control of Asanko, doubles its gold production to 240,000 ounces per year, and the company still has $128 million of cash.

{kind=link}

Galiano Gold

However, there is now as much as US$85 million of debt because of the deferred payments, so net cash will be far lower than before once the deal closes this quarter.

The back-end loaded cash flow of the updated mine plan also complicates the scheduled debt payments.

The Asanko mine will average 240,000 ounces of gold production per year at an AISC of $1,063 per ounce over its remaining ~8-year mine life. On paper, it sounds like a strong mine plan, but the vast majority of net cash flow isn't realized until late in the mine life due to the ~US$230 million of pre-stripping required at the Nkran pit from 2025-2027 (which is excluded from the AISC). This is why the pre-tax cash flow chart below (using a $1,700 gold price) shows only modest net pre-tax cash flow through 2027. The deferred cash payments in 2025 and 2026 will mean cumulative net cash flow is close to zero over the next four years at that same gold price. At the current gold price of $2,000+, which I feel is a more realistic price assumption, the pre-tax cash flow each year will be much higher, leading to far greater net cash flow by the end of 2027, but it's still heavily weighted toward the last few years of the mine life. The mine's production will increase this year, while AISC is expected to be US$1,581 per ounce per the mine plan. Last year's AISC was much lower than forecast, so it's possible that the trend will continue. If it doesn't, then I only expect modest free cash flow from Galiano in 2024.

{kind=link}

Galiano Gold

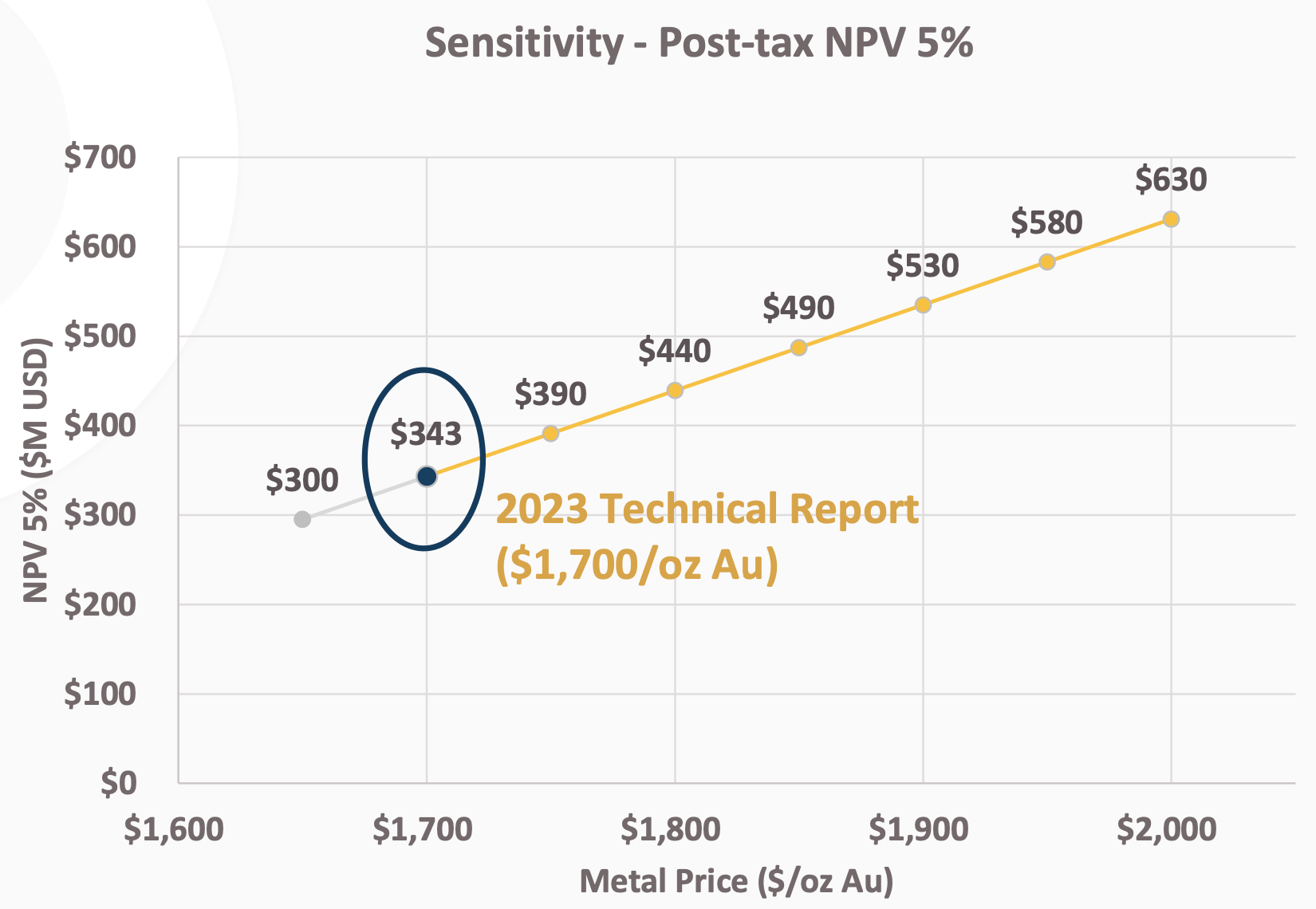

Accounting for the additional shares to be issued to GFI, the market cap of Galiano at its closing price today is US$258 million. The after-tax NPV (5%) at $2,000 gold is $630 million on a 100% basis. Factoring in the pro-forma net cash and 90% ownership, GAU is still trading at less than half its fair value. However, many stocks in the sector are trading at similar or even lower valuations and offer more diversification and/or a lower-risk mining jurisdiction. Other than a major discovery, there aren't any near-term catalysts to drive GAU much higher vs. the rest of the group. I don't believe GAU will be able to continue to push north without the rest of the group also participating, and even then, I think GAU will, at best, perform roughly in line with its small-cap peers. Therefore, I see better opportunities elsewhere in the sector.

{kind=link}

Galiano Gold

I've said it countless times: one of the keys to outperforming in this sector is to play the divergences. With GAU gaining considerable ground over the last 9-10 months, this is the perfect opportunity to rotate into mining stocks with better or equal value that have near-term catalysts to drive outperformance.

For further details see:

Galiano Gold: After A More Than 100% Gain, There Are Better Opportunities In The Sector