CGAU - Galiano Gold: Outperforming And Still Undervalued But Time To Take Some Profits

2023-10-05 15:16:45 ET

Summary

- GAU has outperformed the gold mining sector but has not reached fair value yet.

- Taking some profits here could be considered prudent, due to potential negative short-term catalysts.

- Given the valuation and potential for a sizable premium in the near-term if it's acquired by Gold Fields or another party, it's worth holding some shares.

In my article on Galiano Gold (GAU) back in March - Galiano Gold: You Get The Asanko Gold Mine For Free - I discussed how GAU was trading at cash value, and recent news showed a much-improved outlook for its Asanko gold mine, which the market had yet to acknowledge.

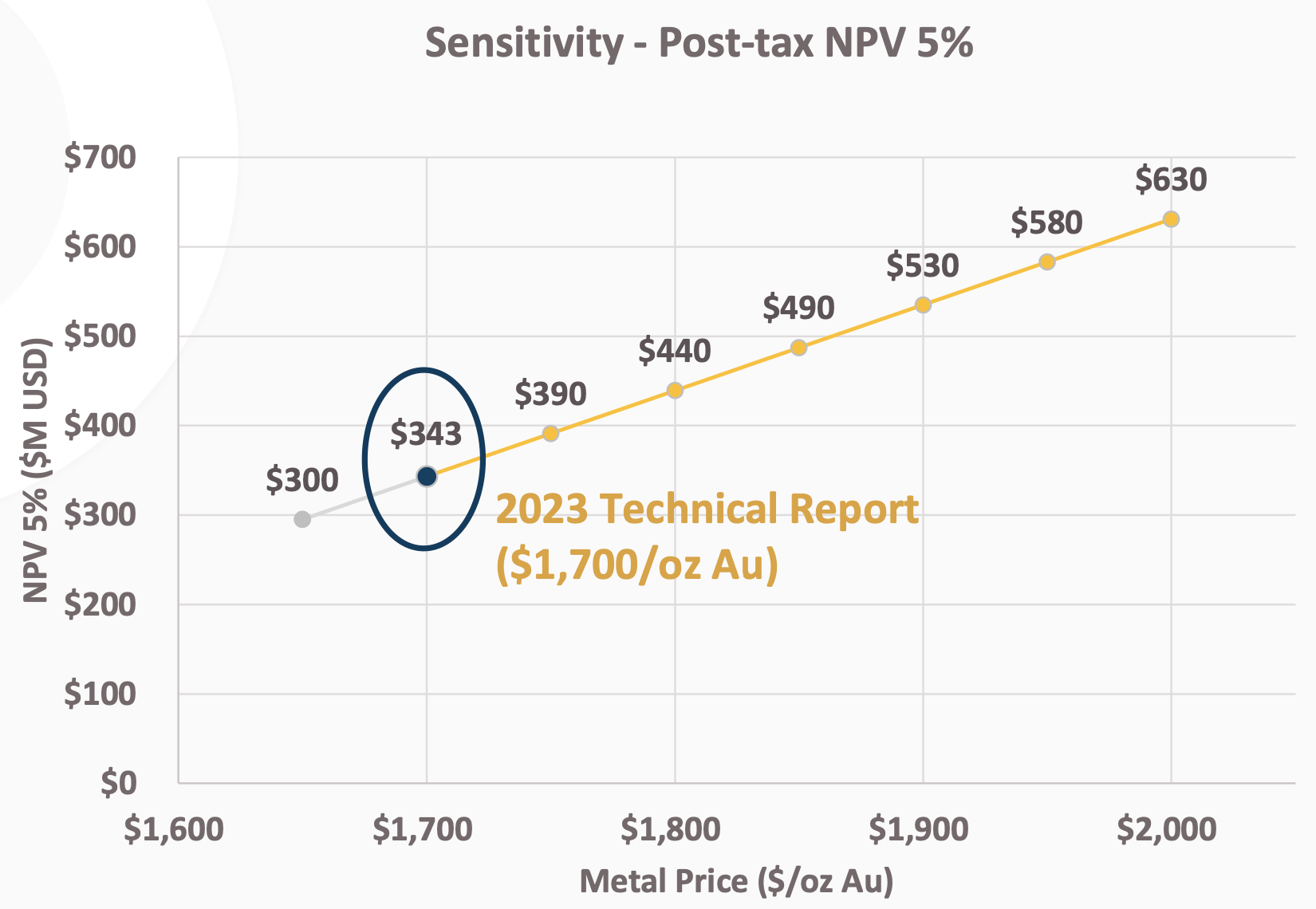

At the time, investors had an opportunity to buy GAU at a substantial discount to fair value, with cash and liquidity of ~US$102 million (and no debt) fully supporting the company's US$103.5 million market cap. This meant that zero value was being applied to Galiano's 45% ownership of the Asanko gold mine - an asset that was expected to generate US$275 million of after-tax free cash flow for the company and had an after-tax NPV (5%) of almost US$200 million, using a $1,800 gold price assumption. The NPV figures below are on a 100% basis.

{kind=link}

Effectively, the Asanko mine was worth roughly $1 per share, but the stock was trading just under $0.50, implying a fair value of ~$1.50 per share for GAU including the net cash on hand, or more than 3x its price at the time.

Since then, GAU has massively outperformed the sector, increasing by over 25%, while the HUI (an index of gold mining stocks) and [[GDXJ]] (a junior gold miner ETF) have dropped by 6% and 7%, respectively. However, GAU is far from reaching fair value.

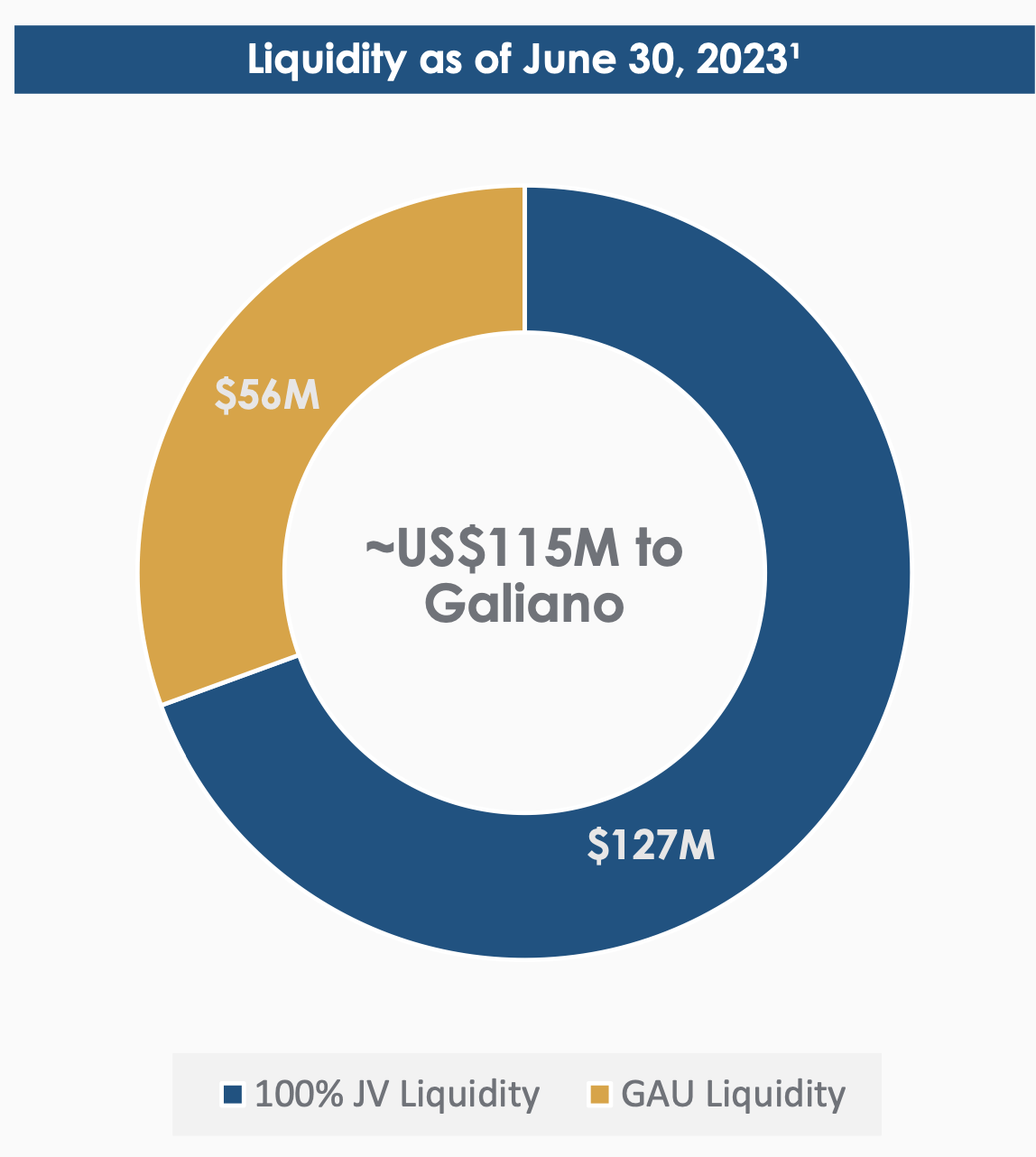

While the company's market cap has expanded to ~US$130 million over the past seven months (or a $25-$30 million increase), its corporate and JV cash balance increased to US$106 million as of June 30, 2023, or US$115 million including physical gold and gold receivables on the balance sheet (which is an $11-$12 million QoQ increase). So, almost half of Galiano's market cap expansion since March is supported by the increase in liquidity. In other words, today's current discount isn't too much different than it was in March, despite the ~25% surge in the stock price.

{kind=link}

While the valuation remains exceptional, and I don't believe now is the time to sell out of GAU completely, taking some profits here could be considered prudent. For a few reasons:

1) It Makes Sense To Rotate Into Other Gold Mining Stocks, Given The Divergences And Similar Discounts To NAV

One of the keys to outperforming in this sector is to play the divergences. With GAU outpacing the group by a wide margin this year and many stocks in the sector in capitulation mode and hitting multi-year lows, it makes sense to rotate some profits out of GAU and into one or two other gold stocks that have been beaten down.

GAU is trading at around 0.4x NAV, but there are a host of much larger, far more diversified gold miners trading at similar discounts to their NAV. Centerra Gold (CGAU) is an example, and you can read more about why in an article that I posted this week.

2) Galiano Could Buy Out Gold Fields' Stake In The Asanko Mine

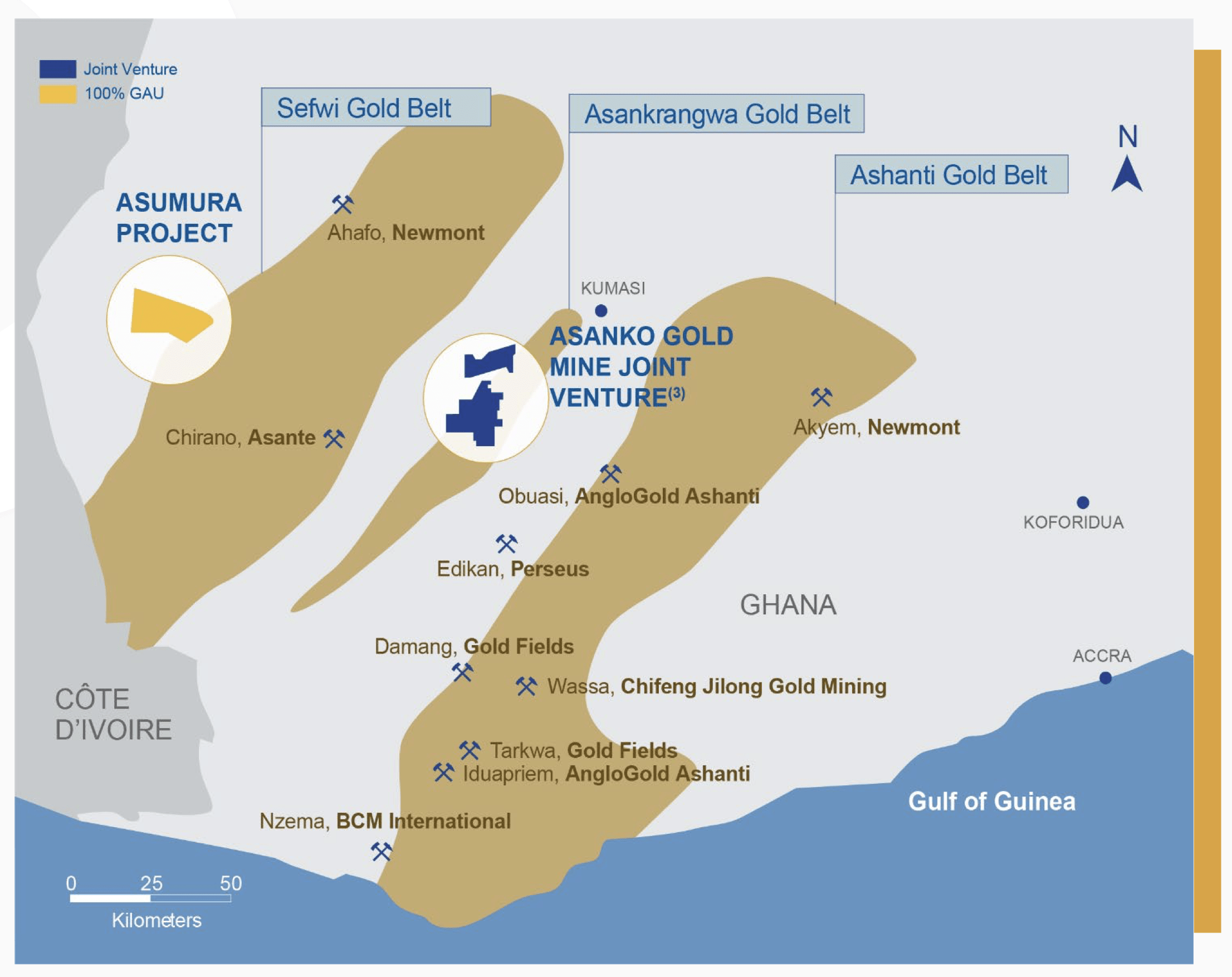

Galiano and Gold Fields (GFI) each own a 45% stake in the Asanko mine, with the government of Ghana owning the remaining 10%.

As I said about GAU in my previous article on the company, the ownership should be consolidated, and I don't think the joint venture will continue under the current ownership structure.

I see no reason why GAU should be a public company. It either needs to be acquired (which should command a sizable premium to today's price) or buy out Gold Fields' 45% stake (which would be bullish news, too, but the market might initially perceive it as bearish, depending on the price paid).

At the Denver Gold Forum two weeks ago, Gold Fields' interim CEO told Bloomberg that the company is "exploring all the options" for the Asanko mine and will decide within the next four months whether to divest or increase its ownership. Quote: "One way or another, I think in the next three or four months we'll have a resolution on the way forward with Galiano."

I'm not 100% confident which way this will go, but I lean towards GAU buying out GFI's stake instead of GFI acquiring GAU, as I'm not sure if the cash flow is enough for Gold Fields or that it would be willing to pay close to fair value for GAU.

This isn't a situation where the acquirer is similarly undervalued and modestly larger in size, and GAU shareholders would be able to shrink any fair valuation gap as the acquirer is re-rated. GFI is too large, and the deal would be too dilutive for GAU shareholders to see any substantial re-rating by holding GFI.

For a buyout to make sense for GAU shareholders, GFI needs to offer 75-80% of the fair value, or ~$250 million for Galiano, which is an ~85% premium to the current price. That would be a fair, risk-adjusted value.

Again, it's not clear if GFI is willing to pay that much. I think it really comes down to how much exploration potential it sees. That will likely determine whether Gold Fields increases its stake in the Asanko mine to 90%.

It's a prospective region, as Asanko is sandwiched between the Sefwi and Ashanti gold belts, both of which host large-scale gold mines/deposits. Gold Fields owns two key mines in the region - Tarkwa and Damang - and there are synergies with the Asanko mine. GAU also owns an early-stage project on the Sefwi belt that is close to Newmont's (NEM) Ahafo mine. Buying Galiano would be a relatively inexpensive way for Gold Fields' to increase its presence in Ghana and West Africa, but to reiterate, it likely depends entirely on how much resource expansion GFI believes exists at Asanko and the entire land package.

{kind=link}

There is nothing to stop GFI from offering a lower premium and the Board of Galiano accepting the buyout, but it would be a disservice to shareholders of GAU and a tough sell by the management and Board of Galiano to its investors.

If GAU purchases the other 45% of Asanko from Gold Fields, which I believe is the more likely outcome, the initial reaction in GAU could be negative, even though it would be a bullish event. I would expect this to be an all-share deal, which could see GFI taking a 30-40% stake in GAU, and the knee-jerk reaction would be on the amount of dilution from all of the shares issued. But much depends on the price paid. If GAU can pick it up at a relatively cheap valuation, then the market should eventually applaud the deal.

By exchanging its stake in the Asanko mine for shares of GAU, Gold Fields would realize immediate value for an asset that is likely receiving little value in its portfolio. In addition, holding a sizable ownership in Galiano instead of the Asanko JV, Gold Fields could realize additional value if GAU continues to be re-rated. Typically, in situations like this where a large mining entity sells a smaller, non-core asset, we will get the standard boilerplate reasoning, something along the lines of " we believe Galiano can extract more value from the Asanko mine and we are happy to hold shares of GAU during this exciting time for the asset and the restart of mining ."

Another potential scenario is a third party buying out both Galiano's and Gold Fields' stakes. That's a definite possibility and a win-win for both GAU and GFI.

3. Q3 And Q4 AISC Will Be Significantly Higher Than The Previous Two Quarters

The Asanko mine has generated considerable free cash flow lately as it processed stockpiled material. However, the second half of 2023 will be much more capital-intensive as the mine ramps back up.

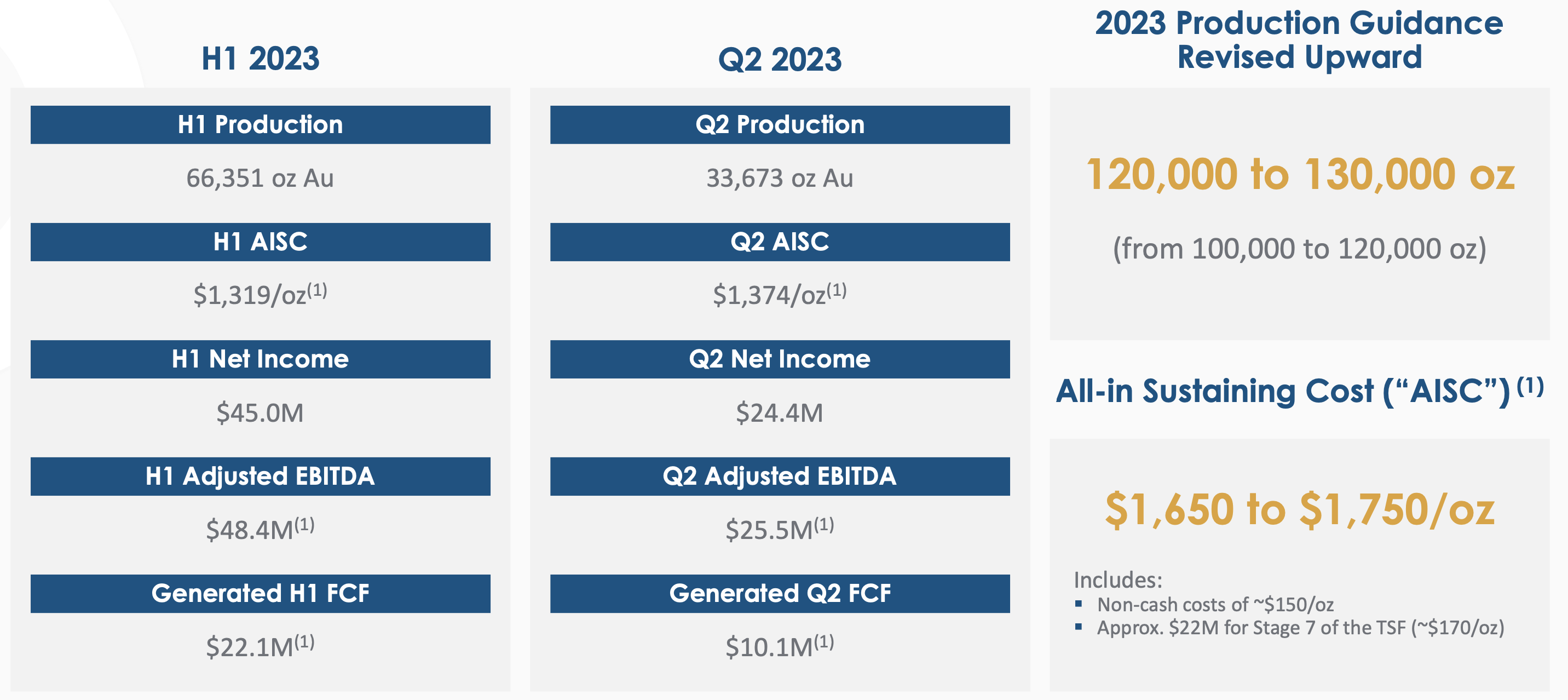

In H1, AISC was $1,319, but guidance for 2023 is $1,650 to $1,750 per ounce. GAU discussed revisiting AISC guidance, as the mine has outperformed expectations and costs could be lower than estimated for the year, but Q3 and Q4 AISC will still be significantly higher than the previous two quarters. Most investors are likely unaware of this, and when results are released and free cash flow is weak (or maybe negative), the stock might come under some pressure.

{kind=link}

In addition to the higher sustaining capital, there is development capital as well. Much depends on prevailing gold prices, but the cash balance at the JV level could be flat or contract somewhat over the next several months compared to end-of-Q2 levels.

Summing It Up

There are short-term negative catalysts for GAU (e.g., higher AISC, potential cash burn, and a possible buyout of Gold Fields' stake in the Asanko mine), but GAU could be acquired within the next few months and realize a sizable premium to today's price.

I feel the best course of action is to lower exposure to GAU and take advantage of the outperformance in the stock, tuck those profits into similarly undervalued gold stocks, but still hold a position in the shares, given the valuation and the potential for a sizable premium in the near-term if it's acquired by Gold Fields or another party.

For further details see:

Galiano Gold: Outperforming And Still Undervalued, But Time To Take Some Profits