GLPEY - Galp Energia: A Promising Outlook For 2023 Will Support The Share Price

Summary

- Galp Energia is the second largest oil-producing company on the Iberian peninsula, behind Repsol.

- The company's balance sheet is very healthy and will soon see a cash inflow from the sale of its Angolan assets.

- The investments in renewable energy assets are being boosted, and the capacity will almost triple by 2025.

- Galp anticipates to generate about 1B EUR per year in free cash flow, including growth investments, over the next few years.

Introduction

Galp Energia (GLPEF) (GLPEY) is a Portuguese integrated oil and gas company. It has a production rate of just over 100,000 barrels of oil-equivalent per day, owns a refinery and has recently been investing in renewable energy sources. The stock is still trading below the 15 EUR level it was trading at when I last discussed the company in 2019 , despite just having completed a year with phenomenal oil prices which boosted the free cash flow result to almost 1.7B EUR , which is in excess of 2 EUR per share. 2023 likely won't be as strong as the oil prices have been trending lower, but in this article I'll explain why the official guidance for 2023 still makes Galp relatively appealing.

{kind=link}

Galp's primary listing is on Euronext Lisbon where the stock is trading with GALP as its ticker symbol . There are currently approximately 815M shares outstanding after completing a 150M EUR share buyback program in 2022, resulting in a market capitalization of just over 9.8B EUR. As Galp has announced a 500M EUR share buyback , one could expect the share count to decrease by almost 5% this year, to less than 780M shares. The average daily volume in Lisbon is approximately 2.2 million shares.

A look at the 2023 guidance reveals a high base case oil price

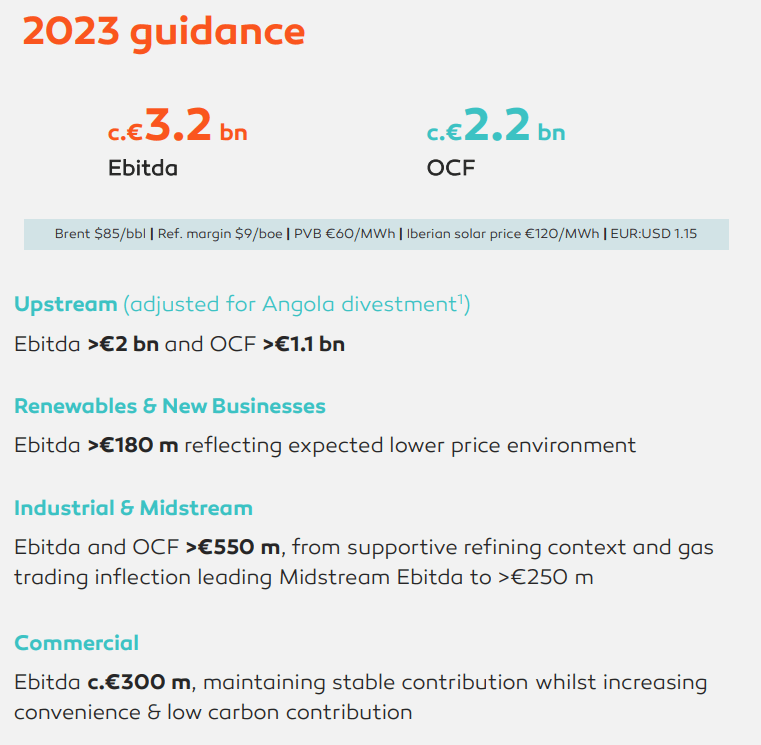

Galp's guidance for 2023 is pretty straightforward. The company anticipates an EBITDA of 3.2B EUR and an operating cash flow of 2.2B EUR this year, mainly thanks to another strong result in the upstream segment. Adjusting for the sale of the Angolan assets, Galp anticipates its upstream segment to generate north of 2B EUR in EBITDA and an operating cash flow of in excess of 1.1B EUR.

{kind=link}

The industrial and midstream assets will contribute about 550M EUR in EBITDA and operating cash flow, while the commercial segment will also contribute a few hundred million Euro. The renewables division should generate about 180M EUR in EBITDA and as such, will represent just over 5% of the anticipated consolidated EBITDA. So unlike its Iberian peer Repsol (REPYY) (REPYF), Galp still is very fossil fuel heavy.

What's interesting is that Galp is using a Brent oil price of US$85/barrel in its base case scenario and that's not really conservative. On the other hand, the company does use an EUR/USD exchange rate of 1.15 which is about 8% more conservative than the current FX rate which gets you 1.07 USD for every Euro. This also means that $85 Brent at a 1.15 conversion rate is just under 74 EUR per barrel while the current Brent oil price expressed in Euro is 79 EUR. So although $85 Brent optically looks pretty high, it's actually a slight discount to the current price when expressed in Euro.

Galp also uses a refining margin of just $9/barrel. That's also pretty conservative given the strong fourth quarter on the refining side.

Fortunately Galp also provided a sensitivity analysis. For every $5 difference in the Brent oil price, the operating cash flow will move by 85M EUR. So applying a Brent oil price of $70 would remove about 255M EUR from the operating cash flow, which would subsequently come in at approximately 1.95B EUR. And for every dollar difference in the refining margin, the operating cash flow will move by 65M EUR.

{kind=link}

So if we would apply $75 Brent, a $10 refining margin and an EUR/USD exchange rate of 1.10, the operating cash flow would be just 25M EUR lower than the base case scenario of 2.2B EUR. The main takeaway here is that the anticipated cash flows appear to be pretty robust.

Investment thesis

Galp Energia is often overlooked in the energy space. Repsol is by far the most important oil and gas company on the Iberian peninsula and Galp is for sure its smaller brother, but let's not neglect the Portuguese company. Even if the oil price doesn't come in at $85 Brent throughout the year, odds are Galp will still generate in excess of 2B EUR in operating cash flow. And considering the capex (including growth capex) is budgeted at - on average - 1B EUR for the years to come, I think it's okay to assume Galp will pretty consistently generate about 1B EUR in free cash flow per year. Keep in mind Galp only provides guidance on the 'net' capex, so it remains to be seen if we will see any divestments beyond the Angolan sale in the future.

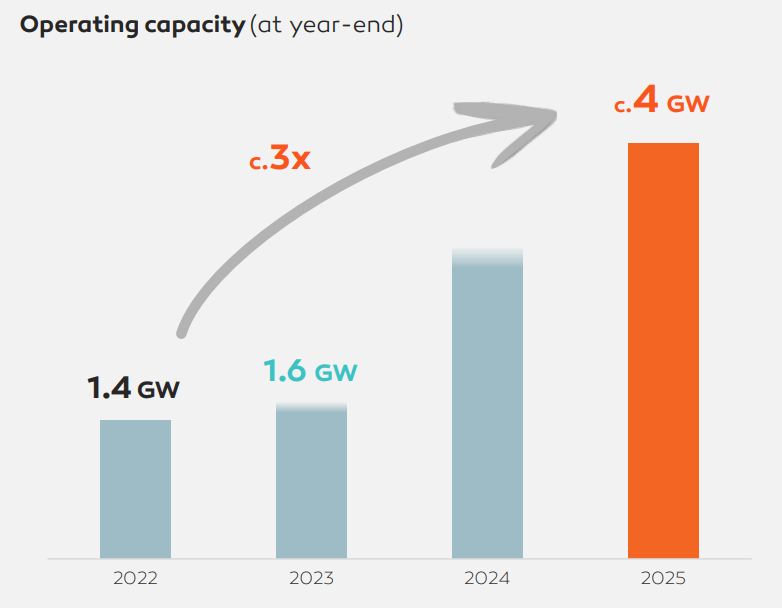

This represents approximately 1.35 EUR per share and although that doesn't make the stock look extremely attractive at first sight (its peers are trading at a higher free cash flow yield), keep in mind this includes some serious investments in the renewable energy space where the company wants to almost triple its operating capacity by 2025.

{kind=link}

Given the strong balance sheet with a net debt of 1.56B EUR (excluding lease liabilities) and a TTM EBITDA of approximately 3.7B EUR (also excluding lease payments), the debt ratio is just around 0.4. Even if one would apply the lower EBITDA of around 3B EUR in 2023 (the 3.2B EUR guidance minus the anticipated lease payments), the net debt level will be just around 0.5 times EBITDA. That excludes the proceeds from the anticipated sale of the Angolan assets . Galp entered into an agreement to sell its Angolan upstream business for total net proceeds of 830M USD (on an after-tax basis) including $175M in contingent payments based on the Brent oil price. The US$655M upfront cash payment represents approximately 600M EUR and will further reduce the net debt to less than 1B EUR (of course subject to the pace of the 500M EUR share buyback this year). As the EBITDA guidance already assumes the sale of the Angolan assets, the debt ratio will thus drop below 0.35. This also makes Galp a pure play on Brazil .

I'm encouraged by Galp's guidance so I will keep an eye on this company with renewed interest.

For further details see:

Galp Energia: A Promising Outlook For 2023 Will Support The Share Price