GCI - Gannett: Cash Flows Are Buried By Debt

2023-09-26 23:28:43 ET

Summary

- Gannett operates local news publications as well as a digital marketing platform.

- The shift towards online news and declining trust in newspapers pose challenges for Gannett's future success.

- Although the industry is facing issues and GCI is buried with debt, I believe the issues are mostly factored in; I have a hold rating for the stock.

Gannett ( GCI ) operates media stations across the United States. The company has a very large debt balance, leveraging the business significantly. Although the company is very risky with the current amount of debt and a non-thriving industry, I believe the issues are largely priced in; I have a hold rating for the stock.

The Company

Gannett operates local news publications on the company's USA TODAY Network brand, under which the company has numerous local operators. The company also owns LocaliQ, a digital marketing platform that helps businesses in marketing through automation, CRM and other tools. Most of the company's revenues come from the local news segment though - digital marketing solutions accounted for only 18% of the company's revenues in Q2.

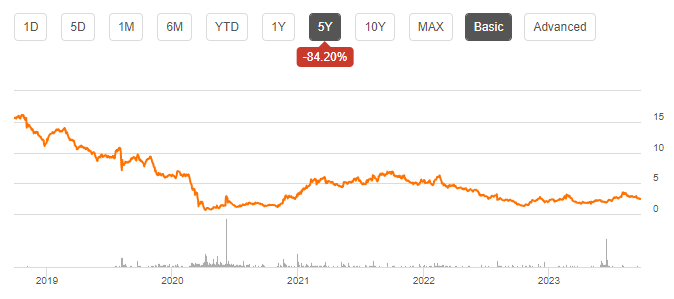

The company's stock hasn't thrived on the stock market in the medium-term past - the past five years' return for the stock is -84%:

{kind=link}

The News Are Getting Old

As Gannett operates local news publications, the company could be faced with a hard time - news is changing more and more into an online format, with many platforms such as X and TikTok informing the younger generations instead of mainstream news. Also, as Sara Fischer writes on Axios, the general population's trust in newspapers and television news is falling - trust in newspapers has around halved from 1993 to 2022. Although Gannett is trying to adapt to a more digital world, the company is ahead of a long journey of change, for better or for worse.

Financials

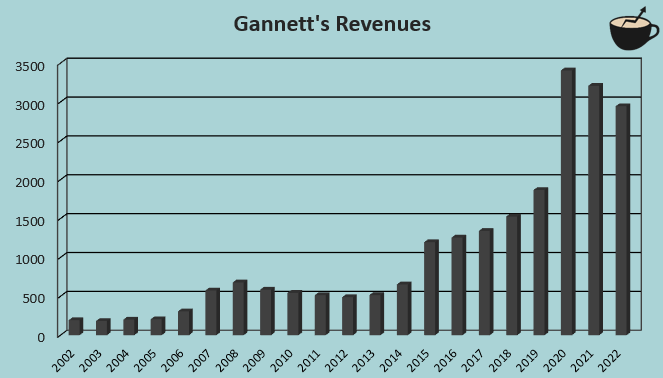

Gannett's long-term revenue history seems very good at first glance - the company has achieved a compounded annual growth of 14.6% from 2002 to 2022:

{kind=link}

A large amount of the achieved growth seems to be inorganic though; Gannett has a significant amount of cash acquisitions as the company's strategy has partly revolved around buying news publications and finding synergies in the acquired companies. The company's revenues seem to have hit their all-time high in 2020 if Gannett doesn't find new acquisitions - revenues have declined in every quarter on a year-over-year basis beginning in Q3 of 2021.

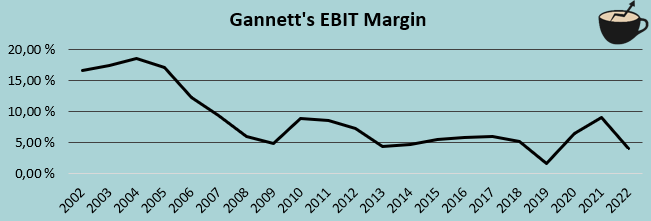

Profitability has been another partly troubled facet for Gannett - the company's EBIT margin has fallen significantly from the early 2000's level:

{kind=link}

Although the EBIT margin seems quite thin, Gannett's cash flows seem to be quite healthy - operating earnings are disturbed by a high amount of depreciation and amortization, which don't affect cash flows.

A concerning factor in Gannett's financials is the company's large long-term debt balance - Gannett currently holds around $1121 million of long-term debt, compared to the company's market capitalization of around $358 million. Of the debt, around $64 million is in the current portion - although Gannett's cash flows seem to be quite healthy, the debt does pose a considerable risk for investors.

Valuation

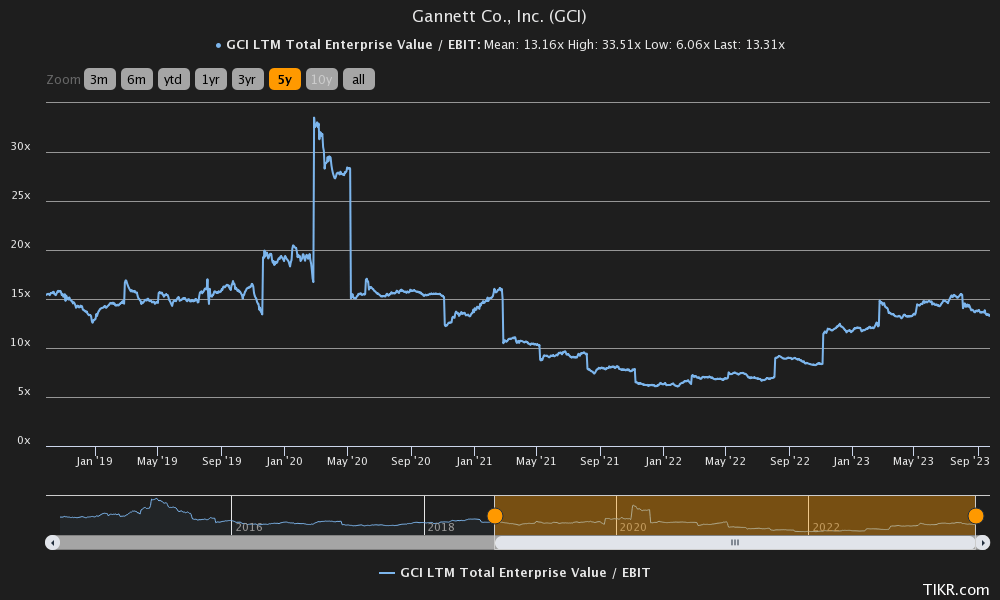

Near the company's five-year average, Gannett currently trades at a trailing EV/EBIT ratio of 13.3:

{kind=link}

The valuation has fluctuated widely as the company has had turbulent financials.

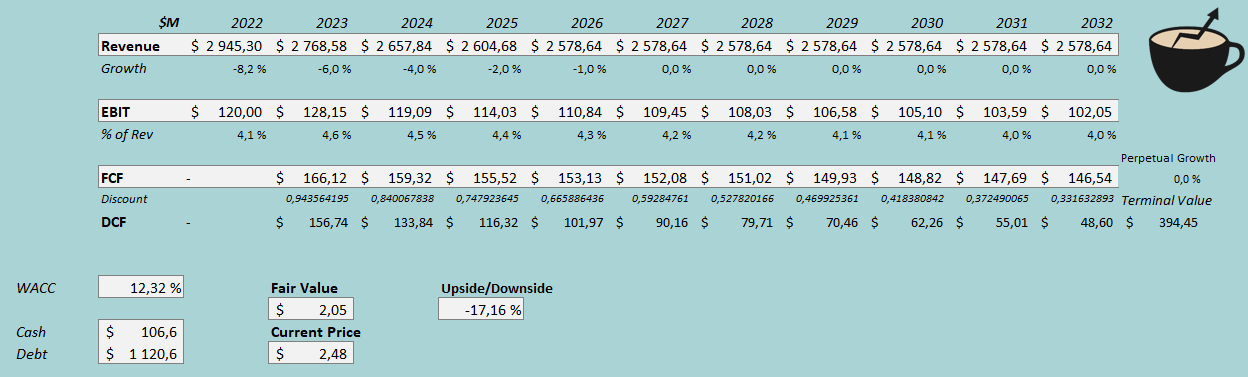

To estimate a fair value for the stock, I constructed a discounted cash flow model of Gannett. In the model, I estimate Gannett's revenues to have a poor future as the print media industry is facing long-term issues - I factor in slight revenue decreases from 2022 to 2026. After the years, I expect Gannett to find a sustainable revenue level with a growth of 0% from 2027 forward; the growth would correspond to negative figures in real terms.

Gannett has achieved an increasing margin in the first half of 2023 despite negative growth. I believe the efforts should boost Gannett's margin for a long time, but as I estimate deteriorating revenues, I don't think the margin for 2023 is sustainable - I estimate the company's EBIT margin will achieve an increase of 0.5 percentage points in 2023, but fall back by 0.7 percentage points in the coming years into an EBIT margin of 3.9% in 2032. The company's high amount of amortization and depreciation distort the company's EBIT to show a largely too thin margin compared to the company's cash flows - I estimate that Gannett's free cash flow level is significantly above the company's EBIT level as shown in the DCF model. These estimates along with a cost of capital of 12.32% craft the following DCF model with a fair value estimate of $2.05, around 17% below the current price:

{kind=link}

The used average weighted cost of capital of 12.32% is derived from a capital asset pricing model:

CAPM (Author's Calculation)

In Q2, Gannett had $28.56 million in interest expenses. With the company's current interest-bearing debt balance, the company's interest rate comes up to 10.19%; as the company has leveraged an unhealthy amount of debt, it needs to pay a very high interest rate. Although Gannett is working on reducing debt, I believe the company will still have a very high amount of debt for a long period of time - I estimate a long-term debt-to-equity ratio of 60%.

The risk-free rate of 4.54% is the United States' 10-year bond yield , which I believe to be the most accurate figure for the purpose. The equity risk premium of 5.91% is Professor Aswath Damodaran's estimate. As Gannett's operations are highly leveraged due to the company's large debt balance, the company has a beta of 2.42 in Yahoo Finance's estimates. Finally, I add a liquidity premium of 0.5% into the cost of equity, crafting the figure at 19.34% and the WACC at 12.32%, used in the DCF model.

Takeaway

As Gannett has a very high amount of debt, the investment case is extremely volatile - a very small change in earnings has a considerable effect on the stock's fair value. At the current price, my DCF model points toward a modest downside for the stock. Although the company is faced with significant risks considering the company's debt and industry, I don't see a sell rating as necessary - the investment case's volatility can work both ways and create a good amount of shareholder value in Gannett if the company's operations prove to be better than I expect. For the time being, I have a hold rating.

For further details see:

Gannett: Cash Flows Are Buried By Debt