GTES - Gates Industrial Corp.: A 'Power' Prospect For Your Portfolio

Summary

- Gates Industrial Corporation has seen a decent amount of volatility in recent years, particularly from a profit and cash flow perspective.

- Management also seems optimistic about the future, with core sales, profits, and cash flows likely to grow.

- The stock is just cheap enough that, even with its volatility, it offers some upside potential.

When it comes to valuing companies, I place a tremendous amount of weight on the ability of the business in question to report steadily growing revenue and profit figures. Companies that have a history of volatility are not as appealing to me, but this doesn't mean that I don't sometimes turn bullish on one that fits this description. One example can be seen by looking at Gates Industrial Corp ( GTES ), an enterprise that operates as a global manufacturer of engineered power transmission and fluid power solutions. Over the past few years, the financial picture of the company, particularly its bottom line, has been quite volatile. Even so, shares of the business look cheap, both on an absolute basis and relative to similar firms. If GTES stock wasn't as cheap as it currently looks, I would likely try to find a different prospect elsewhere. But to me, shares are just cheap enough to warrant a soft ‘buy’ rating at this time.

Not for the faint of heart

As I mentioned already, Gates Industrial Corp operates as a producer and seller of engineered power transmission and fluid power solutions. According to management, its portfolio of products is made available to a wide variety of customers, including both replacement channel customers and OEM (original equipment manufacturers). Specific end markets that the company finds its products in include, but are not limited to, off-highway end markets like construction and agriculture, industrial on-highway end markets like transportation, diversified industrial, energy, and resources firms, and elsewhere. By channel, 63% of its sales go to replacement activities, while the remaining 37% go to OEMs.

An estimated 61% of the company's revenue comes from power transmission offerings, while 39% is attributable to the fluid power space. On the power transmission side of things, the company sells products such as elastomer drive belts and related components that are used to transfer motion in a broad range of applications. Meanwhile, the fluid power operations of the business include products such as hoses, tubing and fitting products dedicated to hydraulic fluid processing, and a variety of high-pressure and fluid transfer hoses.

{kind=link}

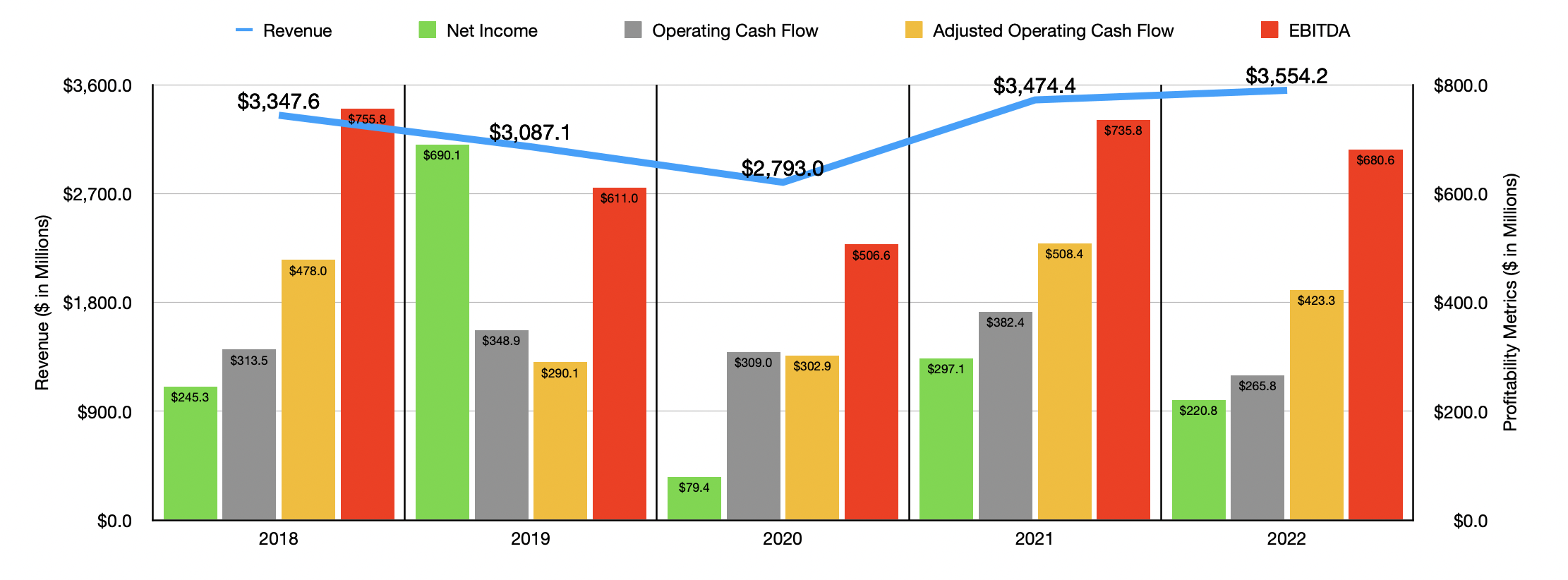

Over the past few years, the financial picture of the company has been somewhat mixed. Between its 2018 and 2020 fiscal years, for instance, sales fell year over year, dropping from $3.35 billion to $2.79 billion. The largest portion of this drop came in 2020 in response to the COVID-19 pandemic. In 2021, however, sales rebounded, hitting $3.47 billion before rising even further to $3.55 billion in 2022. According to management, the increase from 2021 to 2022 totaling 2.3% actually came about despite a $185.1 million hit associated with foreign currency translation. Actual sales would have risen an impressive 7.6%, or $264.9 million, to $3.74 billion had it not been for this. This, in turn, was driven by favorable pricing that added $363.1 million to the company's top line. Unfortunately, the pricing increases did cause lower sales volumes that ultimately hurt the firm. For context, the greatest core sales increase for the company came from its fluid power operations, with revenue spiking 12.6% year over year.

On the bottom line, the picture has been even more volatile. Over the past five years, net income has ranged from a low point of $79.4 million to a high point of $690.1 million. In 2022, profits came in at $220.8 million. This was down from the $297.1 million reported one year earlier. Other profitability metrics have followed a similar theme in that they have also demonstrated volatility. Operating cash flow, for instance, has shown no real trend, bouncing between $265.8 million and $382.4 million over the past five years. If we adjust for changes in working capital, we would have seen an uptrend between 2019 and 2021, with cash flow rising from $290.1 million to $508.4 million. But then, in 2022, the metric fell to $423.3 million. As for EBITDA, it can be said that it remained in a rather wide range over the past five years as well, going between $506.6 million and $755.8 million. For 2022, it came in at $680.6 million.

{kind=link}

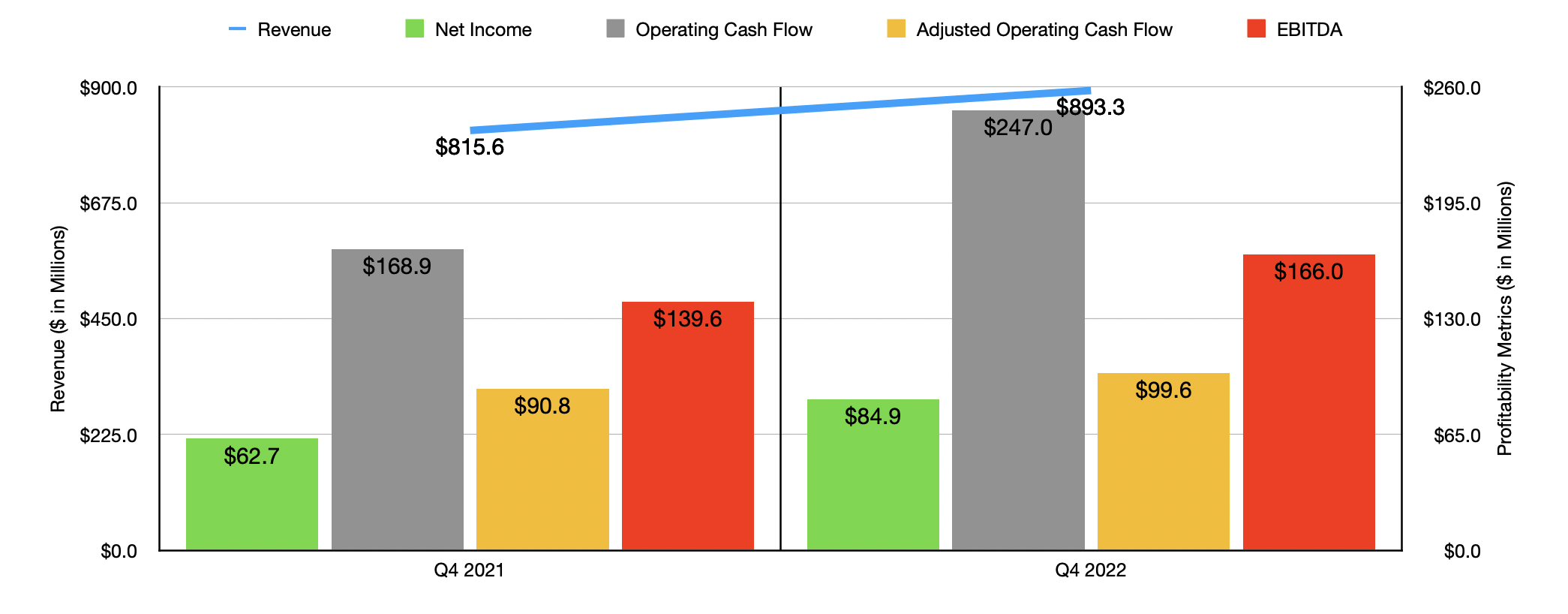

For those worried about any potential weakening, it’s worth noting that the most recent quarter alone, the fourth quarter of its 2022 fiscal year, was quite impressive. Pricing actions initiated by management were helpful in causing revenue to come in at $893.3 million. That's 9.5% higher than the $815.6 million reported one year earlier. Net income jumped from $62.7 million to $84.9 million. Operating cash flow jumped from $168.9 million to $247 million, while the adjusted figure for this expanded from $90.8 million to $99.6 million. Even EBITDA reported a year-over-year increase, rising from $139.6 million to $166 million.

Management also seems optimistic about what the future holds. Core revenue for 2023 is expected to rise by between 1% and 5%. The company also said that EBITDA should range between $700 million and $725 million. At the midpoint, that would be 7% higher than what the business reported in 2022. Earnings per share should be between $1.13 and $1.23, while operating cash flow should be around $436.2 million.

{kind=link}

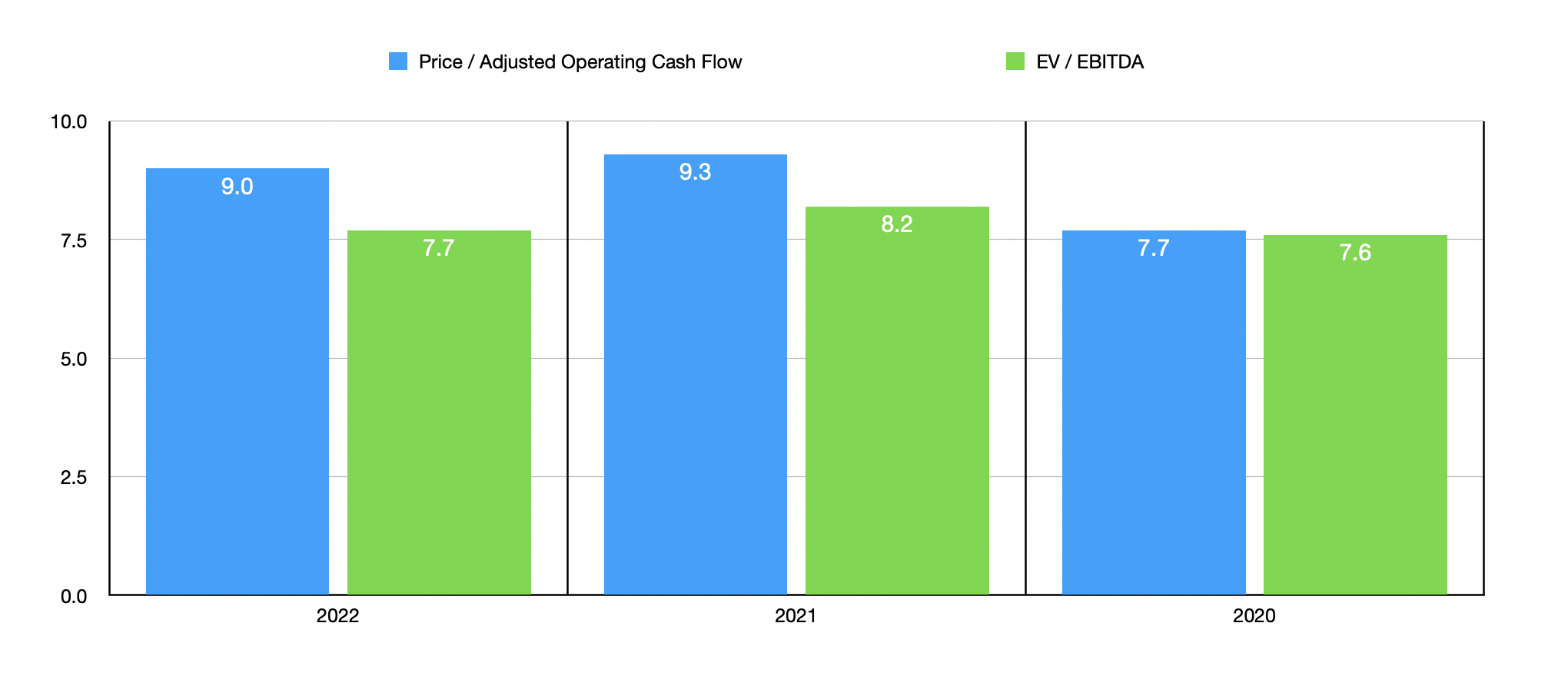

Based on these figures, the company seems to be trading at a forward price to adjusted operating cash flow multiple of 9 and at a forward EV to EBITDA multiple of 7.7. Using data from 2022, these multiples would be 9.3 and 8.2, respectively. And if we were to use data from 2021, these multiples would be 7.7 and 7.6, respectively. As part of my analysis, I compared the business to five similar firms. On a price to operating cash flow basis, these companies ranged from a low of 5.7 to a high of 99.6. Meanwhile, using the EV to EBITDA approach, the range was from 3.8 to 24.2. In both of these cases, only one of the five firms was cheaper than our prospect.

| Company |

| Price / Operating Cash Flow |

| EV / EBITDA |

| Gates Industrial Corporation |

| 9.3 |

| 8.2 |

| Altra Industrial Motion Corp ( AIMC ) |

| 33.5 |

| 24.2 |

| Mueller Industries ( MLI ) |

| 5.7 |

| 3.8 |

| Franklin Electric Co ( FELE ) |

| 99.6 |

| 15.1 |

| John Bean Technologies ( JBT ) |

| 25.3 |

| 18.7 |

| Albany International ( AIN ) |

| 25.3 |

| 15.6 |

Takeaway

Although I find the business model employed by Gates Industrial Corp to be interesting, I do not much care for the historical track record of the business. I don't like volatility in my investments and, as a result, I often stay away from firms like this. Having said that, shares do look very cheap, both on an absolute basis and relative to similar businesses. This affordability, combined with the recent strength and management guidance for 2023, has led me to throw caution to the wind and rate the firm a soft ‘buy’ rating at this time.

For further details see:

Gates Industrial Corp.: A 'Power' Prospect For Your Portfolio