GTES - Gates Industrial Corporation: Breaking Records And Driving Growth

2023-08-14 08:08:04 ET

Summary

- Gates Industrial Corporation broke record sales with $936 million and is experiencing increased demand in manufacturer end markets.

- GTES focuses on power transmission and fluid power solutions, serving diverse industries such as construction and agriculture.

- Despite volatility in profitability metrics, GTES has strong financials, a solid cash position, and a lower valuation compared to peers.

Investment Rundown

In a recent report form, Gates Industrial Corporation ( GTES ) has been showcasing why they are a solid investment opportunity right now. The company broke record sales by netting $936 million of it, up about 4% despite macroeconomic challenges. This proves that demand is still there and GTES is able to capture it too. As more and more manufacturer end markets in both the United States and outside are beginning to see demand, the outlook for GTES is intriguing. The company had some issues earlier on in the year as they faced some cybersecurity issues that seem to have since been resolved, though.

Some of the efforts the management of GTES continues to do to bolster investor value is share repurchases and Q2 of 2023 was no different as $250 million was used to buy back shares, this is up from a year ago when the company spent $175 million instead. But with a 100% FCF conversion rate, this becomes easier. Investors have a lot to gain from investing in GTES, and I am rating it a buy.

Company Segments

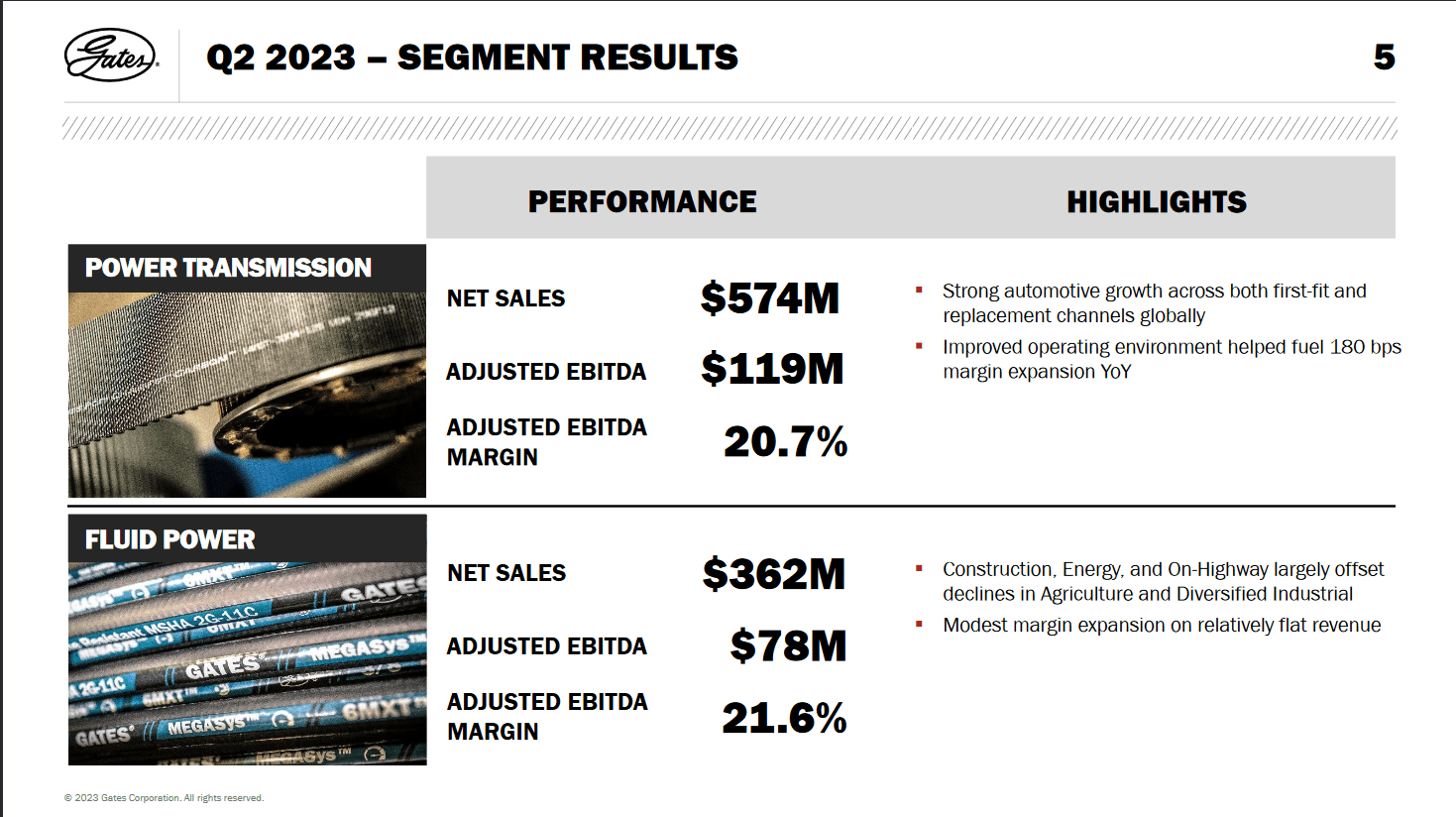

GTES stands as a global provider of engineered power transmission and fluid power solutions. Operating on a worldwide scale, the company is divided into two segments: Power Transmission and Fluid Power.

The power transmission segment provides a range of synchronous and asynchronous belts aimed at a set of diverse industrial applications. From versatile V-belts to specialized CVT belts and Micro-V belts. Accompanying these belts are a variety of related components, such as sprockets, pulleys, water pumps, tensioners, and various accessories. These components act as an important connector in the intricate machinery that drives industries forward.

Q2 Results (Investor Presentation)

{kind=link}

The fluid power segment of the GTES portfolio focuses on providing solutions for both stationary and mobile drive systems. Fluid power systems, which rely on the controlled application of pressurized fluids like hydraulic oil, play an important role in countless industrial operations. GTES offerings in this area include a diverse set of products that include hydraulic hoses, couplings, adapters, and other components vital to effective fluid power transmission.

Market Position (Investor Presentation)

{kind=link}

With a diverse set of end markets that the company's products serve, varied demand should be expected, with some parts performing better than others. While the company's reach extends far and wide, some key sectors stand out as critical domains where its solutions find indispensable utility. Among these end markets are the off-highway sectors, which include the likes of construction and agriculture. In these environments, where heavy-duty machinery and equipment are broadly used, the company's products play an important role in providing the means for that. From robust belts that power construction equipment to specialized solutions that enhance the efficiency of agricultural machinery, the company's presence here has been met with a lot of demand.

Guidance (Investor Presentation)

{kind=link}

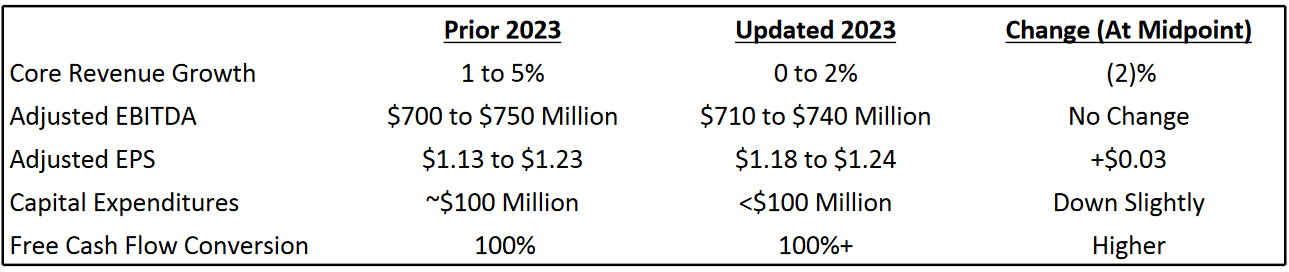

Looking at the guidance for 2023 I think the demand is still present as the company narrowed down on the projections. The core revenue growth is set to be between 0 - 2% and adjusted EBITDA to and between $710 and $740 million. This would come out to an EPS of $1.18 - $1.24 for the year, supported by strong buybacks recently. Despite the revenue growth being revised slightly, I think the company remains an appealing buy as the bottom line expands.

Risks

The profitability metrics of GTES paint a picture of volatility that seems to stick around. For example, during the pandemic, the company saw its net margins grow very quickly but have since plummeted from those levels but are trending upwards still though least. The last two quarters for the company have had a net margin around the 6% mark, but the operating margins have increased by nearly 1% in just 2 quarters to nearly 12%. For GTES that is a decent shift, that of course is positive. Among these key metrics, net cash flows stand as an illustrative example. Over the past five years, its trajectory has been far from a steady upwards trend. Instead, it has gone up and down within a range, between positive $200 million to relatively deep in the negatives some years. This increases the difficulty of properly assessing the company's future ability to buy back shares.

Cash Flows (Macrotrends)

The chart above highlights the company's exposure to a multitude of factors, both internal and external. Economic shifts, industry dynamics, and corporate decisions can all contribute to the fluctuations witnessed in these metrics. Some of these have notably been the Covid-19 pandemic and also higher interest rates which have discouraged some companies in certain end markets from investing and spending too much capital.

Financials

Diving deeper into the financials of GTES we discover that the company is doing very well. The total assets sit at $7.2 billion, which is almost twice as much as the total liabilities. This underscores that GTES has the potential to further leverage itself in the pursuit of driving more growth in the future.

Balance Sheet (Earnings Report)

The cash position sits at $565 million right now, which would cover around 20% of the long-term debts if all were used. Comparing the net debt to the TTM EBITDA we get a ratio of 3.2 which perhaps might be a little on the higher end of the scale, but I think as the short-term headwinds ease like higher materials costs and wage inflation there will be a better chance for the margins to grow as well. This will continue to assert GTES as a financially sound company.

Industry Comparison

One of the appealing factors with GTES above peers like Regal Rexnord Corporation ( RRX ) is the valuation. GTES sits at a p/e of just above 10 compared to RRX which has one over 15. Regal may have a dividend being distributed, but GTES has a solid buyback program which seems to be driving more shareholder returns than RRX. Since 2022 the shares outstanding have been reduced by around 3%, and I think the trend will continue as long as margins remain solid and trending upwards.

Looking beyond valuation and at the profitability of the two companies, it becomes clear that GTES is outperforming here too. The net margins sit at 6% compared to RRX which has 4%. This limits the downside risk for investment in GTES as they have more of a margin of safety. This leads me to prefer GTES over RRX right now.

Final Words

Investors that want to get into a company that is both growing the top and bottom line at a good rate and buying back shares should consider GTES right now. The company is included in the industrial sector, where it serves a variety of end markets, all of which seem to be placing good demand on GTES. The valuation is appealing, and I am rating the company a buy.

For further details see:

Gates Industrial Corporation: Breaking Records And Driving Growth