GTES - Gates Industrial: Encouraging Q3 Report Needed To Finally Create A Floor For The Stock

2023-11-02 13:06:37 ET

Summary

- Gates Industrial's stock has experienced a significant decline since May, raising concerns about its future performance.

- Q3 earnings estimates have been revised down, indicating potential challenges for the company.

- Investors are looking for strong performance and positive guidance to restore confidence in the stock, in our view.

Intro

We wrote about Gates Industrial Corporation plc ( GTES ) back in May when we stamped a 'Buy' rating on the industrial player post the company's first-quarter earnings. Although the cybersecurity incident in February affected Gates' numbers adversely to a degree in the first quarter, both the Fluid Power & power Transmission segments reported growth with energy & construction markets remaining in the fore. Suffice it to say, given the company's valuation & momentum at the time as well as Q1 margin & free cash flow growth notwithstanding Gates' 15% earmarked bottom-line growth rate for fiscal 2024, we believed shares would push on from their present level.

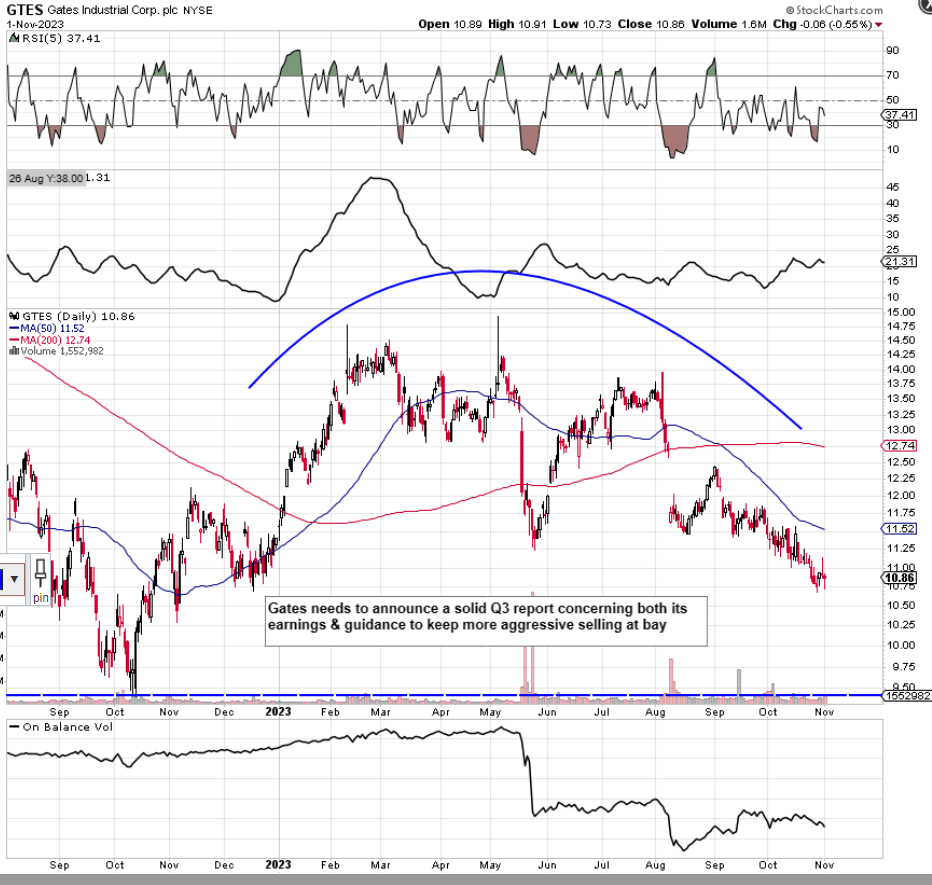

Our bullish assumption however (at least over the short-term) has not panned out as shares now find themselves roughly $3 a share or 21%+ down from our most previous commentary in May. In fact, despite management's bullish commentary regarding sustained EBITDA margin improvements through the first two quarters of this year plus its above-average cash-flow conversion, shares actually topped out in both of its quarterly earnings reports to date. Moreover, repeated announcements regarding secondary offerings of millions of shares did nothing for bullish investor sentiment. Suffice it to say, Gates' present downward trend (confirmed by the sizable bearish gap in early August which has yet to be filled) is a worrying sign as we head into Gates' Q3 numbers which are expected to be announced on the 3rd of November before the market opens. The reason being is that the stock's 2022 lows of under $10 a share are in clear sight now especially if investors are once again not convinced by the quarterly earnings report.

{kind=link}

Q3 Earnings

Gates Industrial is expected to announce a normalized EPS estimate of $0.31 a share for Q3 on revenues of approximately $878 million for the quarter. Unfortunately, both of these estimates have been revised down over the past 3 months (by 4.2% & 1.8% respectively) which explains to some degree the lower lows the share-price has been printing.

Why do we say this? Well, the market is constantly studying the relationship between a stock's valuation and its profitability to ascertain the true value of the company. Now, when a company is primarily unleveraged, forward-looking growth rates are not as important as the stock's valuation or profitability numbers especially if the company in question is generating buckets of free cash flow (which in turn should result in growth in the long run).

Gates though (as mentioned in previous commentary) does not have this luxury as the company's current $2.53 billion of long-term debt resulted in $44.5 million of interest expense in Q2. This means Gates' low-interest coverage ratio of 2.64 and especially its reported debt-to-equity ratio of 0.87 are metrics (regarding its leverage) that the market studies to value the stock. In fact, given that Gates' goodwill & intangible assets make up over 47% of the company's total assets, the company's leverage when compared to its equity may be much larger when measured in real terms.

What Investors Need To See

Suffice it to say that, given that Gates' valuation may not be as compelling as many believe, investors continue to demand stronger growth to compensate, and here is where Gates' worries lie. Although ongoing operational productivity and cost-structure stabilization have improved margins meaningfully this year, management cut fiscal 2023 top-line guidance on the Q2 earnings call to approximately 1% due to sluggish industrial demand in China as well as slower inventory ordering in personal mobility. Although there was no change to the company's EBITDA guidance (but adjusted EPS guidance increased), the market likely very well knows (being a predictive mechanism), that if top-line growth continues to struggle, then it will only be a matter of time before earnings get affected also.

If Q2 trends persist into Q3, we should see further strength in the 'Power Transmission' segment with the Automotive space remaining in the fore. In the 'Fluid Power' segment, we expect to see continued strength in construction, on-highway and the energy verticals to compensate for the declines in diversified industrial. Demand across industrial end markets (in both segments) is the crux of the issue for Gates at present. If Q3 can pave the way for some type of turnaround in these markets, this trend would go a long way in finally putting in a floor in this stock in our view.

Conclusion

Gates Industrial is expected to announce its Q3 earnings numbers for fiscal 2023 on the 3rd of November before the market opens. The normalized EPS estimate is $0.31 a share on revenues of $878 million. If the company can beat, if not at least meet, these estimates but more importantly back this up with solid forward-looking guidance, then the lows may finally be in for this stock. We look forward to continued coverage.

For further details see:

Gates Industrial: Encouraging Q3 Report Needed To Finally Create A Floor For The Stock