GEAGF - GEA Group: Remember This Fundamentally Solid Industry Player

2023-12-12 21:51:01 ET

Summary

- GEA Group, a systems supplier in the industrial sector, has experienced a challenging year with lower demand and cost increases.

- Despite the current downturn, GEA Group remains a major beneficiary of long-term macro trends and has solid financials.

- The company's 3Q23 results were strong, with increased EBITDA and stable operating costs, and it has positive guidance for 2023.

Dear readers/followers,

The central European industrial sector has not been a generally pleasant sector to invest in this year, looking at returns. Plenty of pain, plenty of cost increases, and plenty of lower demands. GEA Group Aktiengesellschaft ( GEAGF ) is one of them. GEA Group, to remind you of the operational profile, is a systems supplier in the industrial sector, serving various end markets, including food production, beverage production, and the pharma sector. Essentially, if you want to start a plant in any of those sectors, GEA can build the line and systems for you.

The company has solid financials, with billions in revenue, strong margins, and a decent dividend. And yes, that dividend is decent even if you consider today's overall trends.

Even if the company is "down" these days, and it is - since my last article that you by the way can find here, the company is now in the red, GEA group remains a major beneficiary of overall megatrends. To me, the long-term thesis for the company is a relatively simple one. For as long as the company remains operationally sound and under good management that cares about its shareholders, the long-term underlying macro trends will ensure this company's long-term growth.

Let's look at what we have for 3Q23, and for 2023-2024 that could turn things around.

Updating on GEA

I believe the time has come to lift every rock you can to find undervalued quality companies in defensive sectors. This is after an outperforming tech year of 2023, which seems to be coming toward a close. I believe defensive sectors will offer some of the best value, upside, and protection in the near term, and I'm allocating non-trivial amounts of capital to these sectors.

If you follow my work, you know I'm not a big-time tech investor. I have my investments, but they're less than 5% of my total, compared to others who are at 20%, or even higher.

The company we're talking about here trades on the German market under the native symbol G1A. The ADRs are, to my mind, too thinly traded to constitute a decent investment in the company and should be avoided.

The company has gone through a number of changes over the past few years, and those changes have not finished. Management changes are still happening, in this case, a new CFO with over 3 decades in the industry and from relevant capital market segments.

You might think the share price development we've seen since my last article is an expression or reflection of sub-par company operational development.

Such an assumption would be false. 3Q23 was in fact a good quarter. The company has continued taking advantage of the cheap share price to buy back shares, expanding to €400M and canceling shares worth €700M until 2025 in 2-3 tranches, with the first already coming within 6 months.

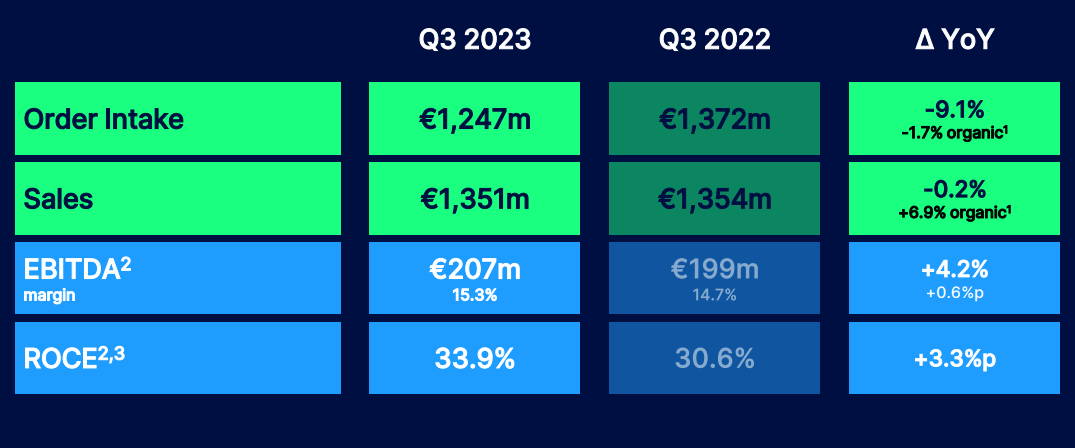

The quarter was strong. Not as strong as YOY, but we have a downturn on the macro, and EBITDA was actually up YoY, as well as RoCE even with a downturn in order intake and a minimal downturn in sales.

{kind=link}

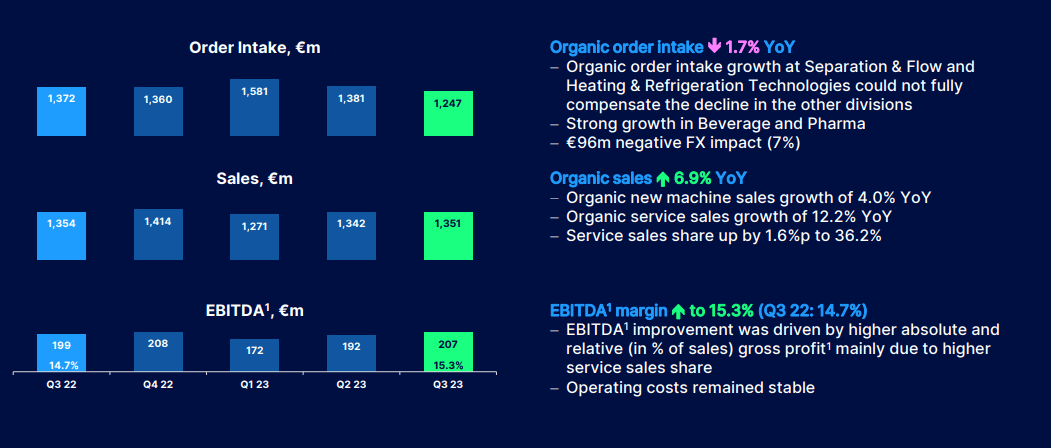

GEA is the sort of company where order intake, due to order size, is going to be a lumpy affair. For 3Q, the company had three large orders versus five larger orders YoY. However, on an organic basis, sales numbers are very solid, and the real advantage here is a good EBITDA increase, due to higher gross profit, as well as a solid trend in operating costs that have remained stable despite everything that's happened on macro.

Net liquidity and cash flow were excellent, and this is despite €56M being spent on company buybacks.

Looking at the yearly and quarterly trends, I don't see any clear indication why GEA should be trading down here, beyond where things are in macro.

{kind=link}

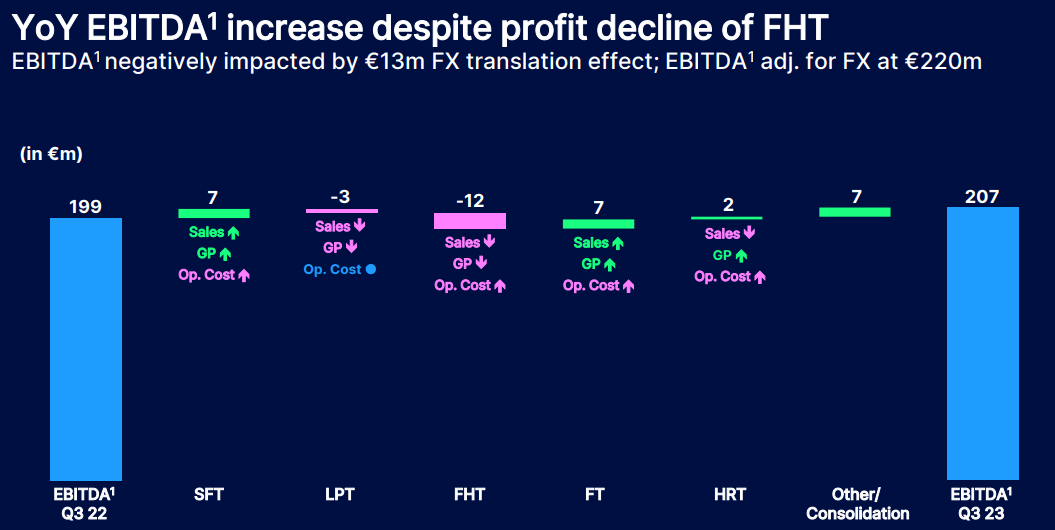

As a reminder, this company is a play on five different segments, starting with Separation and flow, Liquid and power, Food and healthcare, Farming, as well as Heating and refrigeration. Certainly not one of these individual segments saw any sort of remarkable set of growth or results. This is actually encouraging as I see it because it means that the EBITDA improvements are not related to sales, but to operational improvements or mix. And indeed, we're seeing a higher amount of service sales.

And while none of the aforementioned segments are showing superb growth or explosive trends, none of them are going down either.

In fact, the GEA group is remarkably stable for what it does and what it offers.

{kind=link}

The company is also a very efficient operator, with a ratio of net working capital of less than 8.5% to sales - again despite the current macro. The company has a guidance corridor of up to 10% but has been as low as 6.1% during 2Q22.

Also, cash flow and related trends here remain very strong.

All of these positives have an impact on the company's 2023E guidance, which is very positive. The company guides for over 8% sales growth, and EBITDA at the upper part of the guidance range, almost €800M for the year at a margin of over or at 14% in EBITDA, and a ROCE of over 32%.

This confirmation of guidance comes after a May 2023 guidance increase.

GEA group is a great "sleeper" stock. I've made over 50% TSR in a short time more than once on this company. This time around, I've been slower in upsizing my position due to the opportunities available on the market, but I'm getting to larger stakes now, with my total company allocation slowly reaching that 1% mark.

It's important to note that just like my fertilizer or other food investments, this player is a core participant in key sectors.

{kind=link}

The trends above are enough, I believe, that you should seriously consider adding a non-trivial stake to your portfolio, provided this company meets your stated investment goals.

It has drawbacks. No doubt about that. The company has no credit rating, it's less than €6B in market cap, and its dividend, in a world where 5% isn't rare, is barely 2.76%, and that's after dropping quite a bit.

However, at the same time, the risks are comparatively minor compared to the upside I see.

Risks & Upside

The risks to GEA are not mainly operational. The company is a volatile stock and can, during times, such as we saw during 2013-2019, see several years of poor returns - though in this case, this was related to operational issues at the time and ongoing restructuring. Since 2023, the company has significantly improved its operating specifics, and I would liken it quite a bit to KION ( KIGRY ) and where that business currently is.

Over 1.5% of my portfolio is in KION.

I believe that GEA offers incredible value for where it's going , and even if you state categorically that the company's premium is not valid, you still have a market-beating upside to consider.

Any risks here, including the volatility and the yield, are low enough that I view the ratio as favorable and a good investment possible to be made.

Valuation

GEA Group typically trades at a P/E of 25-27x. This is obviously not going to happen in this market. However, with operational improvements confirmed, and guidance based on very strong 2023 trends so far, I don't see a massive downside for GEA. I would say a 16-19x P/E for this company is completely fair - and even 14-15x P/E gives a double-digit upside here. At 18-19x P/E normalized, you're seeing a 24% annualized RoR, or almost 60-65% TSR in less than 3 years possible here. Even if you normalize the company's multiples over as much as 20 years, you get the company trading at 21x P/E, which comes to over 31% per year, or 75% in less than 3 years.

This is another way of me saying that on the basis of historical multiples , which had worse operational fundamentals than the current ones, the company would be set to only outperform.

Analysts believe the company is worth at least €41/share here, or an upside of almost 20%. That's 16 analysts going from a low of €30/share to a high of €48/share. 9 out of 16 analysts are at a "BUY" or similar positive rating here. My own target is actually also at €41/share, so in this particular case, I'm very much in agreement with these overall considerations.

When I look at GEA, I consider above other things the fundamental safety of the operations and allow a premium for this.

As before, I've also looked at engaging in selling cash-secured puts, as well as trying for the buy-write covered calls option, but none of these give me the returns that I'm looking for. For this reason, straight investment into the common share is the preferable way to go for me here, and remains this as of this particular article and December 2023, going into 2024.

I accept and expect the company to see some cyclicality to its results and trends, but overall I expect the company to normalize its valuation, which will leave me "richer" than before.

For that reason, my thesis on the company is as follows.

Thesis

- GEA Group is a market-leading name in the food processing and other processing systems industry. The company is a market leader with excellent tradition and overall safety. It has no net debt, and it's a net beneficiary of overall macro trends, including demographics, urbanization, and food consumption. This is the sort of company I like buying.

- I want a 15% annualized RoR for this company. At this valuation and these prospective growth rates, that is not an easy estimate to find on a realistic overall basis. We find it at around 19x P/E, which constitutes a significant discount even to a 20-year premium of 22x P/E.

- I consider it likely for the company to be worth around a 20-21x P/E long term, and for that reason I consider the company a "BUY" with a €41/share PT - but the upside here isn't large. So if you "BUY" GEA, you should do so for quality - because there are companies with better upsides out there.

- Nonetheless, at €34/share, I continue to buy, and I'm now even longer GEA than I was in my last article.

Remember, I'm all about:

1. Buying undervalued - even if that undervaluation is slight, and not mind-numbingly massive - companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

2. If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

3. If the company doesn't go into overvaluation, but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

4. I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria and how the company fulfills them ( italicized ).

- This company is overall qualitative.

- This company is fundamentally safe/conservative & well-run.

- This company pays a well-covered dividend.

- This company is currently cheap.

- This company has a realistic upside based on earnings growth or multiple expansion/reversion.

This means that the company fulfills every single one of my criteria except being excessively cheap, making it relatively clear why I view it as a "BUY" here.

Editor's Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

For further details see:

GEA Group: Remember This Fundamentally Solid Industry Player