GNRC - Generac: Helping To Power An Electric Future Growth Trajectory Appears Sustainable

2023-12-22 22:32:46 ET

Summary

- Generac’s revenue has grown at a CAGR of 11%, owing to an uptick in demand for electricity. This trajectory appears sustainable in the long term.

- We believe Generac will benefit heavily from the impact of climate change, the electrification revolution, increased infrastructure spending, and a broader uptick in demand for backup power.

- Underpinning the industry’s attractiveness is strong development and innovation by the business, which offers a range of products and services for both residential and commercial uses.

- Generac has struggled with a slowdown in demand, owing to current economic conditions. Its growth is negative and margins are declining. We see this as a near-term headwind.

- As a leading business in this space and with a NTM FCF yield of 7.6%, we consider this a good opportunity to buy into the stock.

Investment thesis

Our current investment thesis is:

- Generac is positioned well to achieve outsized growth in the coming years, with the climate change impact, electrification of society, and infrastructure spending key value drivers.

- Generac’s innovation to create market-leading products and services, its international exposure, and its presence in both the Residential and Commercial segments make Generac a top choice for investors seeking exposure to a growing industry.

- The current economic slowdown is causing a material strain on Generac but we see this as a problem that will pass. The fundamental attractiveness of the industry and business is not being diminished and so is primed to improve once interest rates begin to decline.

- Patient investors may be better off waiting for the price to potentially slide further but at a NTM FCF yield of ~8%, we consider now to be a good entry point.

Company description

Generac Holdings Inc., ( GNRC ) headquartered in Waukesha, Wisconsin, is a leading manufacturer of backup power generation equipment and other power products. The company's product portfolio includes generators, transfer switches, and other power-related products, serving residential, commercial, and industrial markets. Generac is known for its innovation in standby power solutions and has a strong presence in the home backup power market.

Share price

Generac’s share price performance has been strong, outperforming the wider market, with much of its gains coming during the post-pandemic period. This development is following a change to the industry dynamics, and global societal conditions, with numerous tailwinds accelerating the company’s future trajectory. The share price volatility following this period has been high, as investors seek to understand the future trajectory of the business.

Financial analysis

{kind=link}

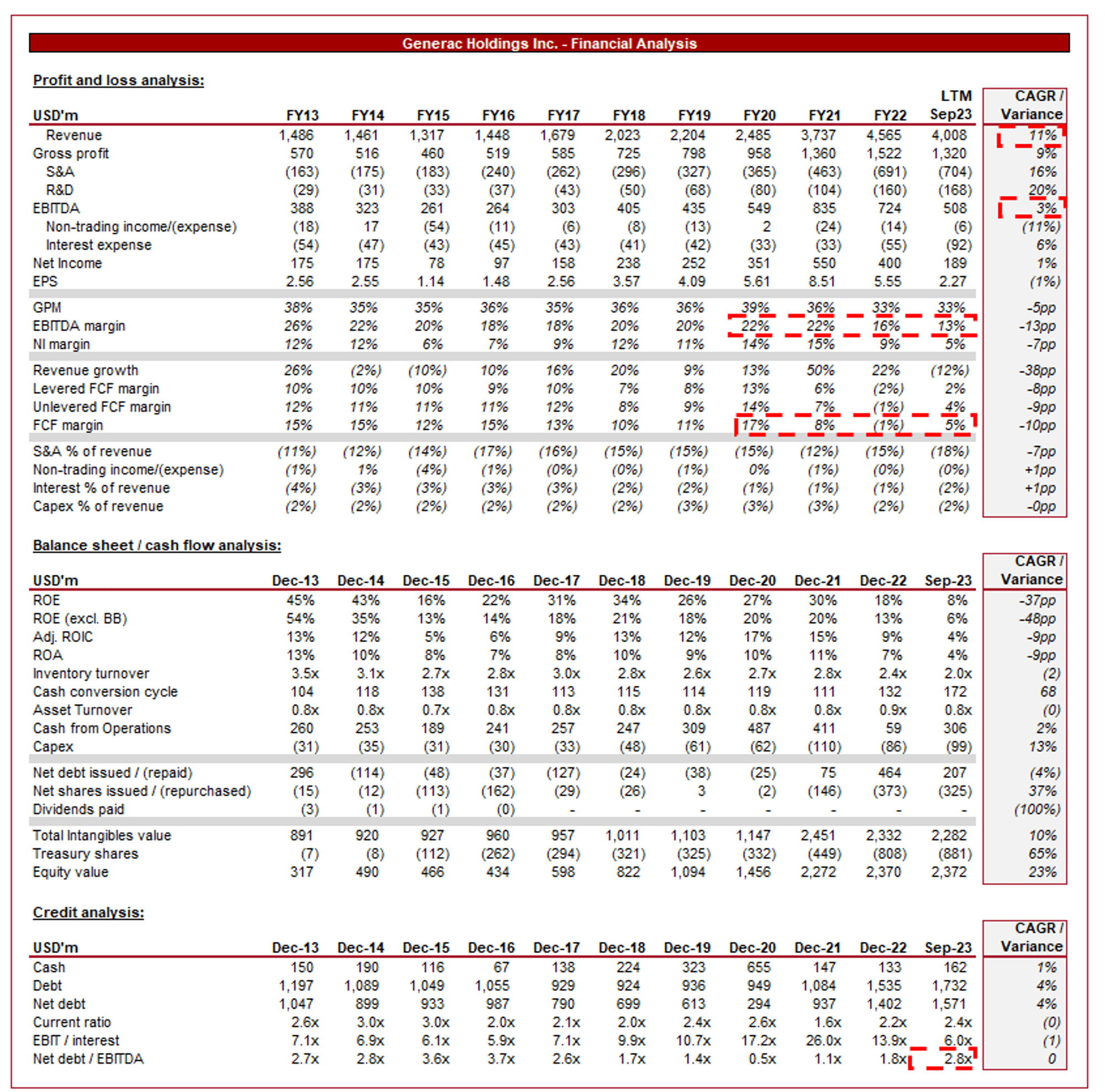

Presented above are Generac's financial results.

Revenue & Commercial Factors

Generac’s revenue has grown at a CAGR of 11% during the last decade, with much of the gains being achieved in recent years, although the overarching trajectory is clearly positive.

Business Model

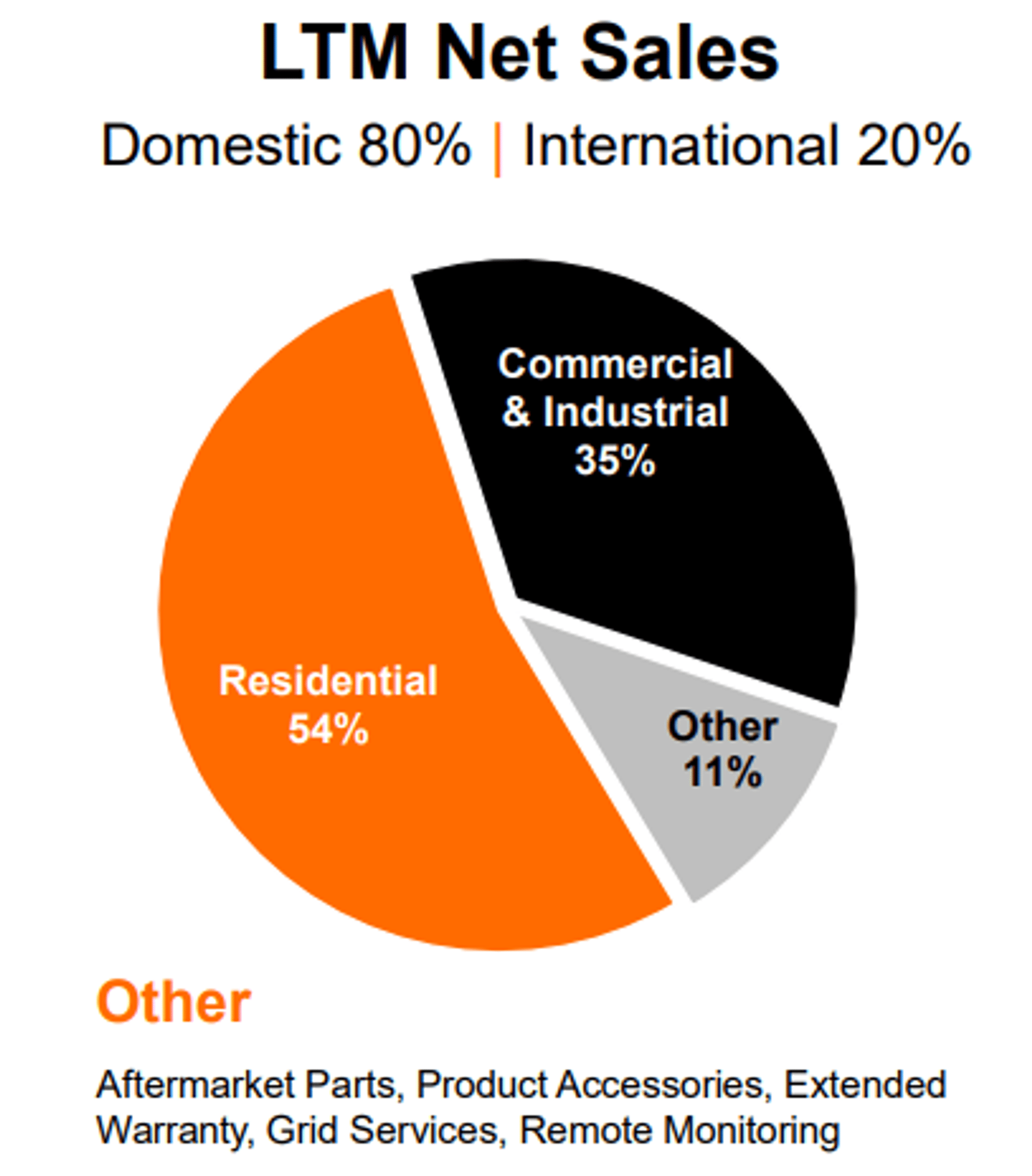

Generac primarily manufactures and sells backup power generators, ranging from portable generators for residential use to large, industrial generators for commercial and industrial applications. They also produce related power equipment, such as transfer switches and power management systems. Unlike many of its peers, the business is weighted heavily toward Residential, with 54% of sales through this channel. The company serves both residential customers who want backup power for their homes and commercial/industrial customers who require reliable power for critical operations. Further, the company is primarily US-based, although has incrementally increased its overseas exposure.

{kind=link}

{kind=link}

In most industries, the commercial segment is preferred, due to resilient demand and growth opportunities with scale. However, we see good opportunities in the residential market, which we will explore later.

Generac offers a wide range of generator models with varying power capacities and features to cater to different customer needs, and importantly, budgets. They also provide various options for fuel sources, including natural gas, propane, and diesel.

Generac invests heavily in R&D, with over 1000 engineers and consistent capex commitments, seeking to continually improve its product offerings. It has introduced innovative features like remote monitoring, automatic self-testing, and clean energy solutions to stay ahead of the competition.

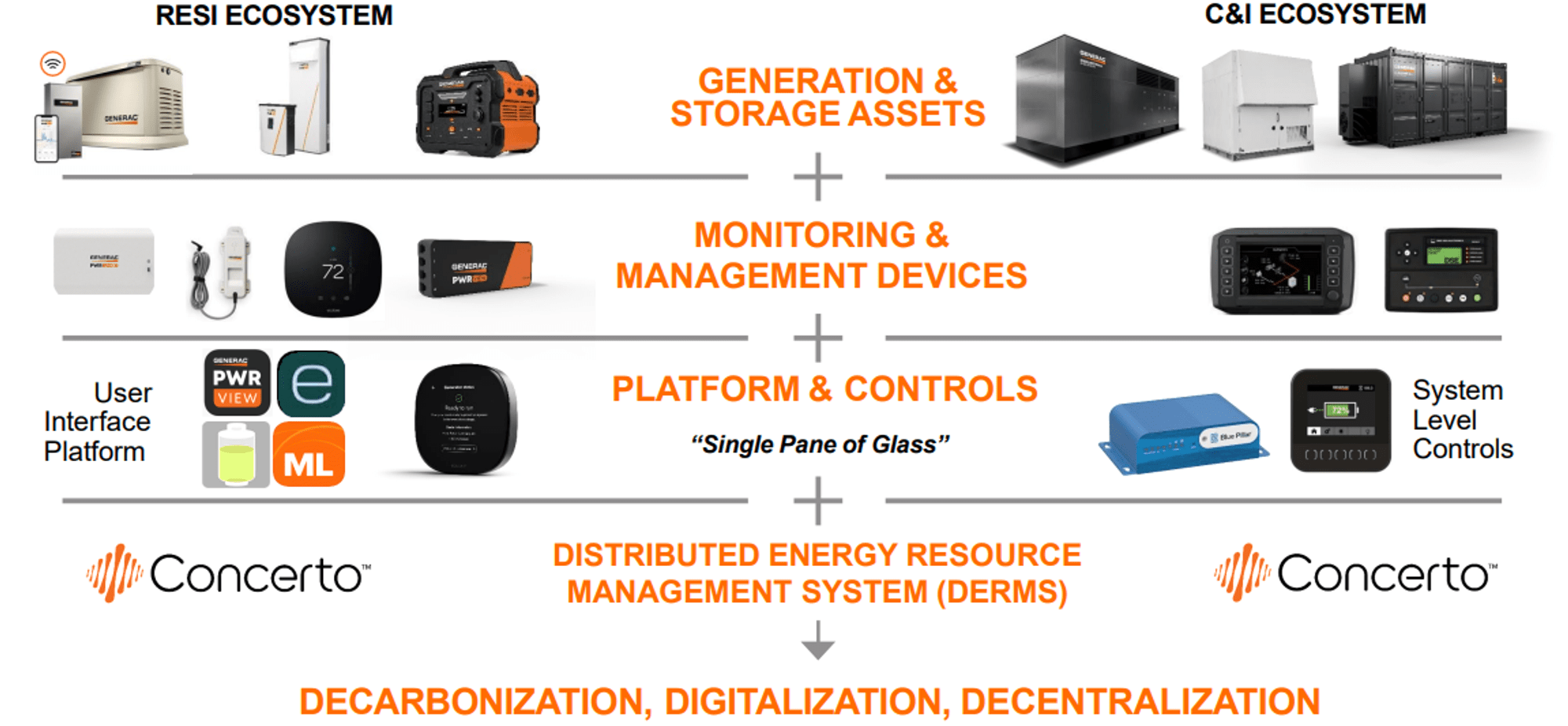

Generac offers maintenance and service plans for its generators, ensuring that they operate reliably when needed. This service-oriented approach enhances customer satisfaction and builds brand loyalty. The company’s objective has been to create an “ecosystem”, with related products, both parallel and enhancing.

{kind=link}

The company distributes its products through a network of dealers, retailers, e-commerce platforms, and industrial distributors. This omnichannel and multi-distributor approach allows it to reach a broad customer base and market its brands. This is critical given the relatively niche nature of its product offering.

Generac has expanded its presence globally, tapping into markets beyond the United States to drive international growth. This allows the business to exploit its deep expertise and enjoy the same tailwinds impacting the US market.

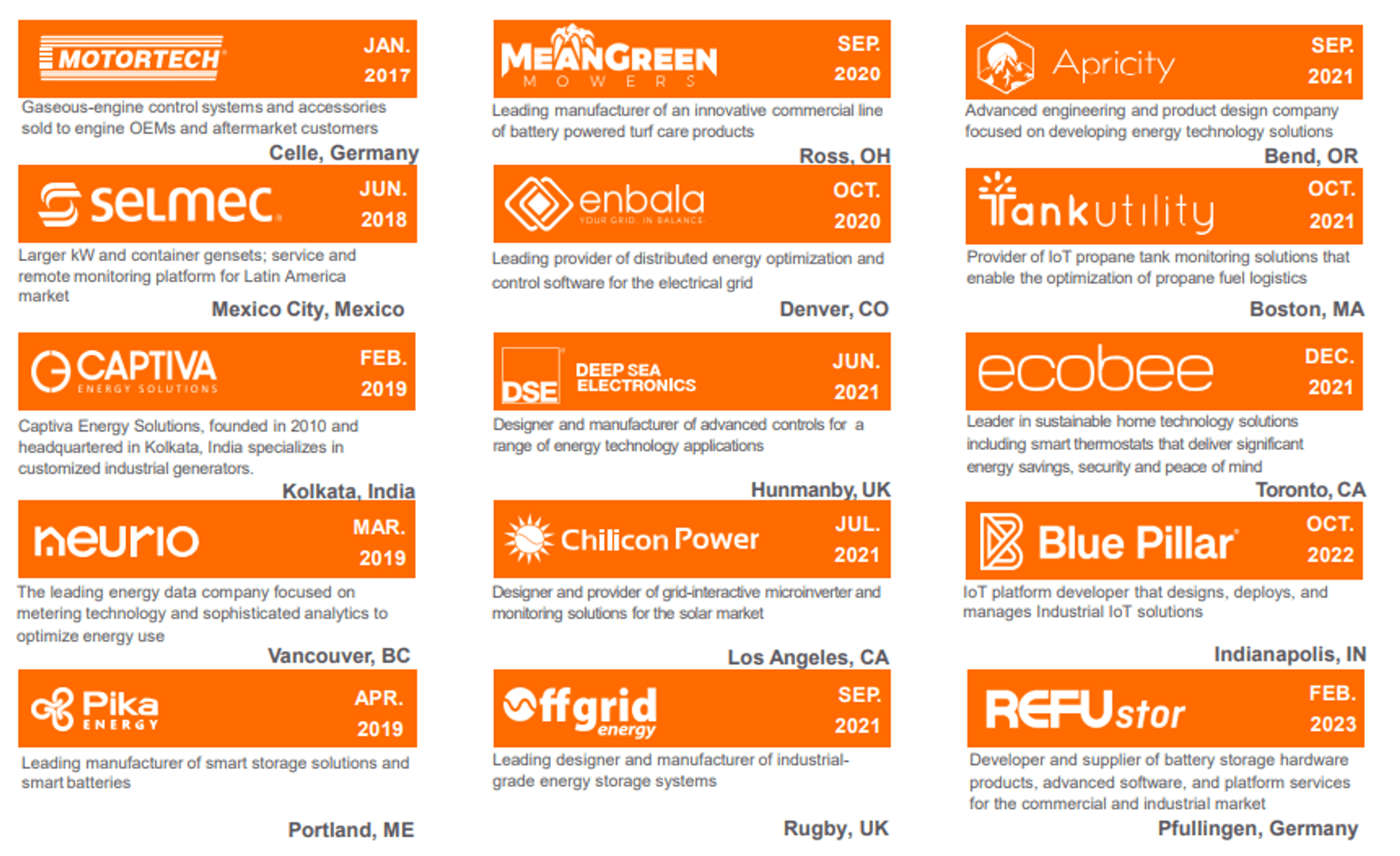

M&A has been a key strategy for the business, with a track record of acquiring and integrating innovative, global businesses. Generac has acquired ~28 businesses since 2001, allowing for a rapid expansion of services and a deepening of expertise. We believe this will continue to be a key growth driver, not only for incremental revenue but also due to the development of its services.

{kind=link}

Growth Opportunities and Industry Tailwinds

Management estimates that its total Served Addressable Market has grown by 5x ($66b from $14b) since 2018, representing the monumental trajectory of the business (both organic and M&A), as well as the development of the wider industry.

We believe this amount will only increase in the coming years, contributing to an improvement in Generic’s growth trajectory. Value drivers include:

-

Increased Demand for Backup Power - Growing awareness of the vulnerability of power grids to outages due to a strain on infrastructure. ~25% of US households are at risk of resource adequacy shortfalls during normal seasonal peaks.

-

Climate Change and Weather Events - (In conjunction with the above), extreme weather events are becoming more frequent and severe due to climate change, with a growing need for reliable backup power solutions.

-

Electrification of All - There has been a significant increase in demand for electricity, with the future trajectory appearing noticeably upward. This is driven by the “electrification of everything”, including EVs (and other transportation methods), smart technologies, and economic development.

-

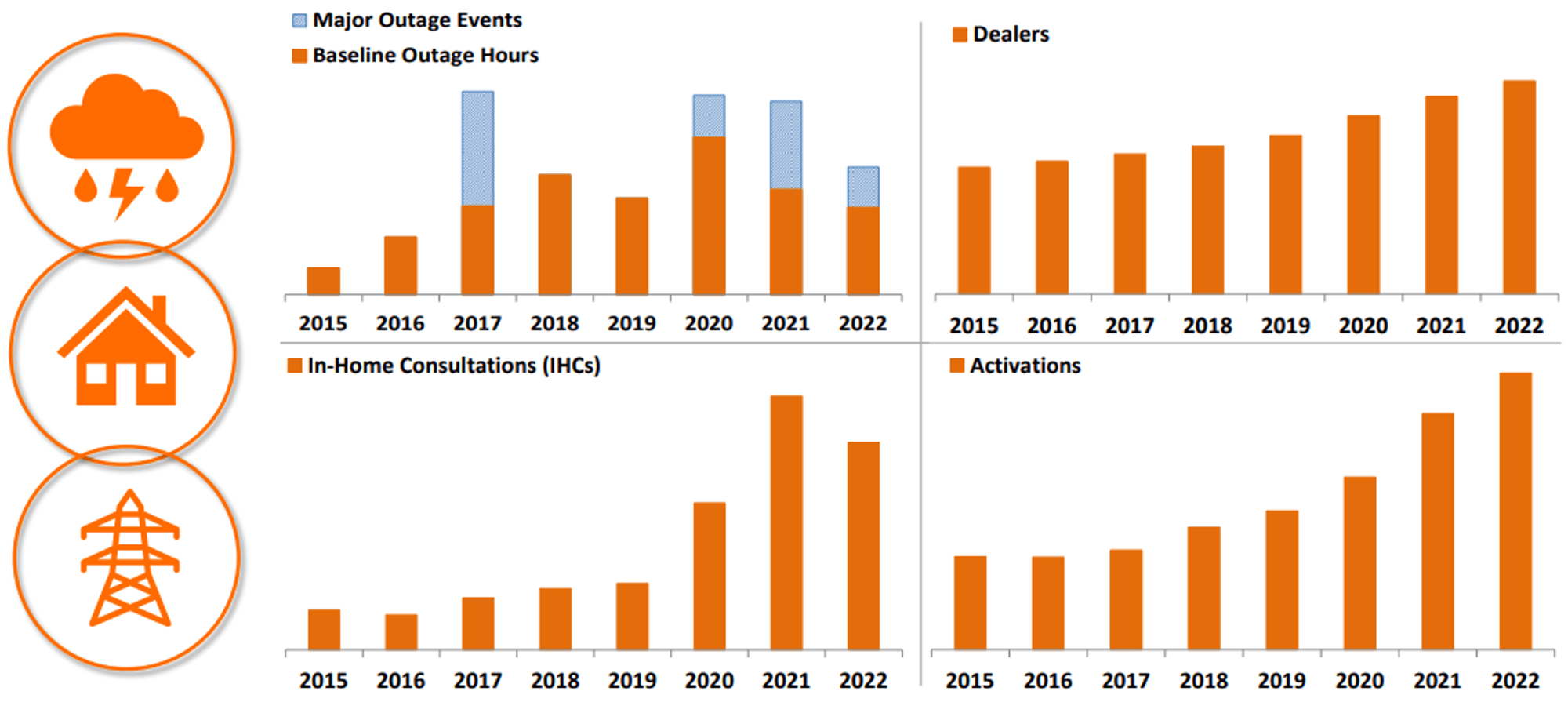

Infrastructure Spending - Western nations have criminally underfunded infrastructure during the last few decades, with a slow realization creeping in. The US has committed to its IIJA plans, with many other nations proportionately as aggressive. This underinvestment has led to many consumers “taking matters into their own hands” (leading to increased spending), while the expectation for increased investment will also drive demand. The following graph illustrates points #1-4 (in particular), with a growing level of demand and pressures on the current infrastructure.

{kind=link}

- Clean Energy Revolution (Incl. NatGas) - The shift towards cleaner and more sustainable energy sources presents an opportunity to expand its clean energy product offerings, such as solar and battery storage solutions.

-

Telecom Industry Investment - The 5G revolution is encouraging infrastructure investment to enhance the current network, with a particular focus on backup power solutions.

-

“Home as a Sanctuary” - With increased working from home, an aging population, and technological reliance in the home, consumers are spending more time than ever at home. Many, particularly the rich, are investing heavily in the development of home infrastructure (although remains a mainstream trend). As costs decline, we suspect this trend will become more pronounced.

-

Regulatory Environment - Continued regulatory action to encourage clean energy and infrastructure spending should support the industry’s growth.

These tailwinds will be supported by the following underlying factors:

- Strategic Acquisitions - Generac has a strong brand and platform for businesses within this industry. We expect a continuation of its acquisitive nature, ensuring it maintains its market-leading position.

- Product Innovation - In conjunction with M&A, the company's commitment to innovation has allowed it to offer cutting-edge products that meet customer needs, including quieter and more efficient generators, home energy management systems, and grid-interactive solutions. With Capex spending of 2-3%, this can be “cheap” for investors while again protecting the company’s competitive position.

- Market Penetration - Management estimates that its current market penetration in the US is ~5.75%, with its largest markets being at 15-20% (and still growing well). This gives the company significant runway to continue, and likely enhance, its current trajectory. For this reason, even if industry development is slow (i.e. realization of the above tailwinds), growth can still be attractive.

- Geographic Expansion - Generac's international expansion strategy has already shown itself to be beneficial, with the same needs the US has overseas. This allows for it to copy-paste its approach, with adjustments for local intricacies (appreciating this is a simplified attitude).

- Commercial and Industrial Applications - All the points above can easily translate to the commercial/industry segment, contributing to a diversified revenue profile.

Given how lucrative the industry is, it is reasonably competitive, with both traditional players and new entrants. For this reason, continued innovation and differentiation is key to maintaining its market leadership. We are confident of this given Management’s focus on developing an ecosystem.

Economic & External Consideration

Current economic conditions are potentially problematic for the business, but only in the near term. With elevated interest rates and high inflation, the ability and willingness to finance these projects are noticeably reduced. We believe this will continue in the coming quarters, although will not diminish the broader industry tailwinds.

The key takeaways from Generac’s most recent quarter are:

- Net sales declined by (2)% following a difficult Q2 when sales declined (23)%. This is in part due to an impressive set of quarters in the prior year, with a substantial backlog reduction subsequently. Residential product sales is down (15)%, while Commercial & Industrial is up +24%. This reflects the resilience of the C&I segment and why maintaining strong exposure is key.

- Demand has declined as expected, with Management now believing this is below what was previously projected. The extended period of high interest rates, and the changing future projections, is likely a primary reason for this. This said, Management is of the belief the end-market demand is still attractive.

- Margins have also deteriorated due to an unfavorable product mix and lower demand. A small positive is that the business has been successful in lifting prices and is also seeing inflationary pressures subside.

This is clearly not a good period for the business. We suspect this will continue to be the case (cyclicality) as industry tailwinds take their time to unfold. This said, investors should not be interested in this stock for short-term gains. The question is whether this represents an opportunity to attractively enter the stock.

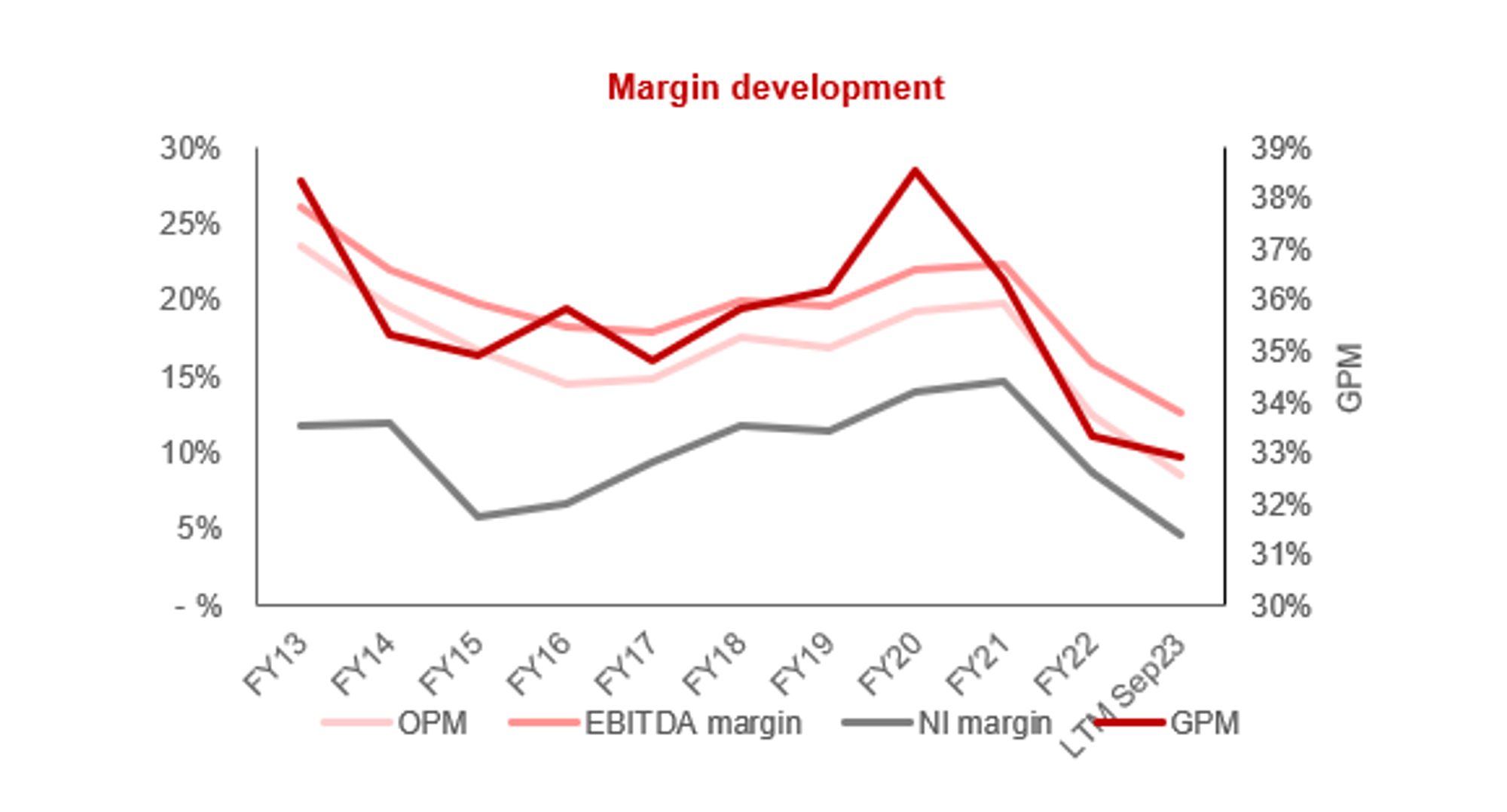

Margins

{kind=link}

Prior to its recent performance, Generac’s margins broadly traded sideways, which is expected given the expansionary focus. The degree to which it has declined is concerning, particularly with FCF grinding to nil.

We believe its prior level of c.22% EBITDA-M is sustainable in the long term, with scope for improvement. Its strong competitive positioning and the development of its business model give us confidence that as demand improves, margins will rapidly rise, also.

Balance sheet & Cash Flows

A key factor contributing to margin and FCF deterioration is inventory levels. Generac has found itself hoarding stock following an unanticipated decline in demand. With an inventory turnover of 2x, the business is far below its decade average. The risk is that discounting activities contribute to further margin deterioration.

Management has utilized historically strong cash flows to buy back shares, with scope for this to return once FCF improves. Management has rightly switched focus given the near-term cash constraints.

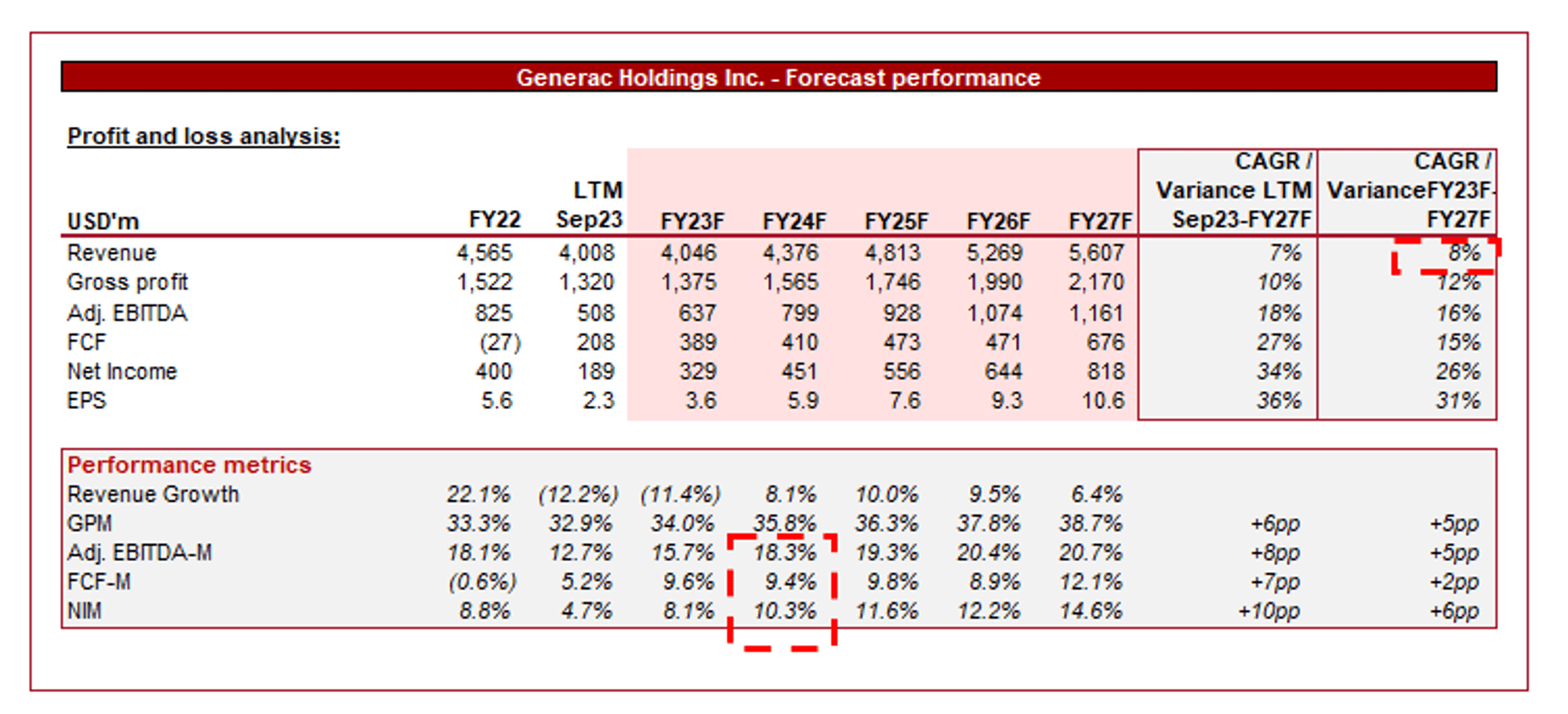

Outlook

{kind=link}

Presented above is Wall Street's consensus view on the coming 5 years.

Analysts are forecasting a 7% average growth rate into FY27F, with consistent margin improvement to its historical levels. The growth rate appears conservative in our view, given the tailwinds ahead and the performance to date. As previously discussed, a return to prior margins is expected.

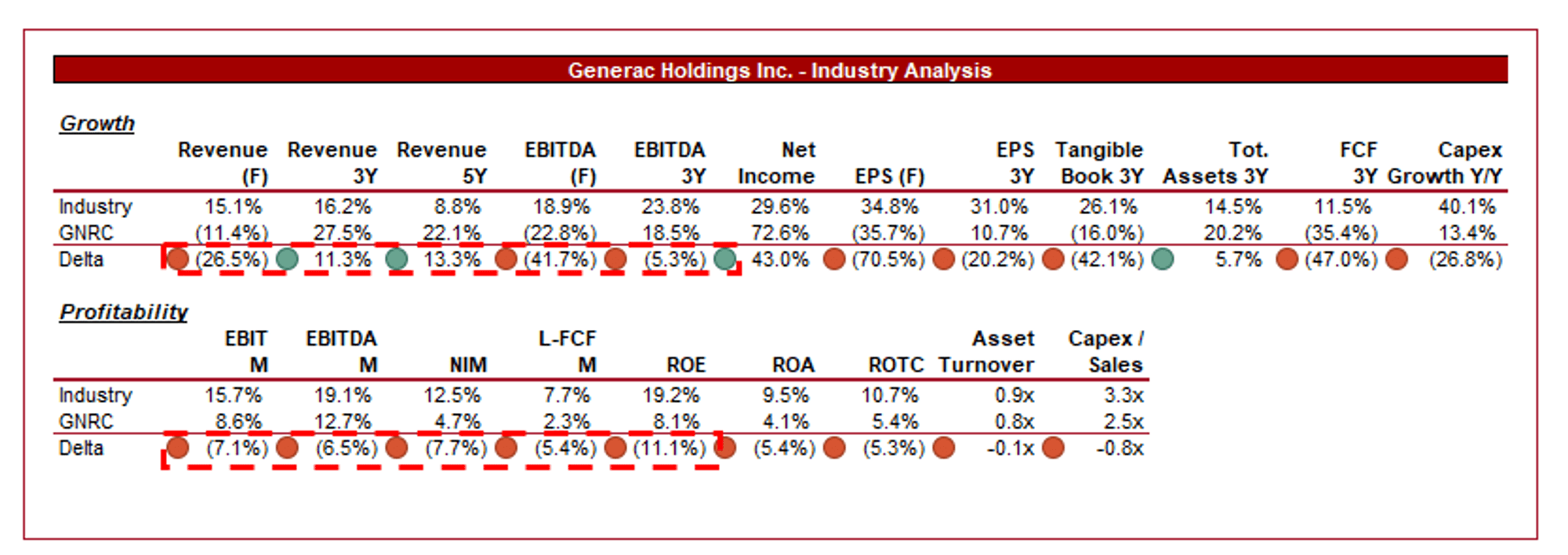

Industry analysis

{kind=link}

Presented above is a comparison of Generac's growth and profitability to the average of its industry, as defined by Seeking Alpha (30 companies).

Generac’s current performance is underwhelming. The company has achieved strong revenue growth despite the clear slowdown, although its profitability development leaves more to be desired. The biggest concern, however, is that the business is significantly exposed to economic conditions, which is not the case for the wider industry (reflected in the forward guidance).

Its profitability delta is less concern, as the business has a good runway to at least catch up to the average level, with better growth prospects than average due to its greater cyclicality.

The company’s underwhelming financials must be contextualized with the commercial potential of the company. Its growth runway is large, with growing importance and scale creating the potential for margin improvement. This will contribute to a downward pressure on trading multiples. For this reason, we see a justifiable premium on its valuation.

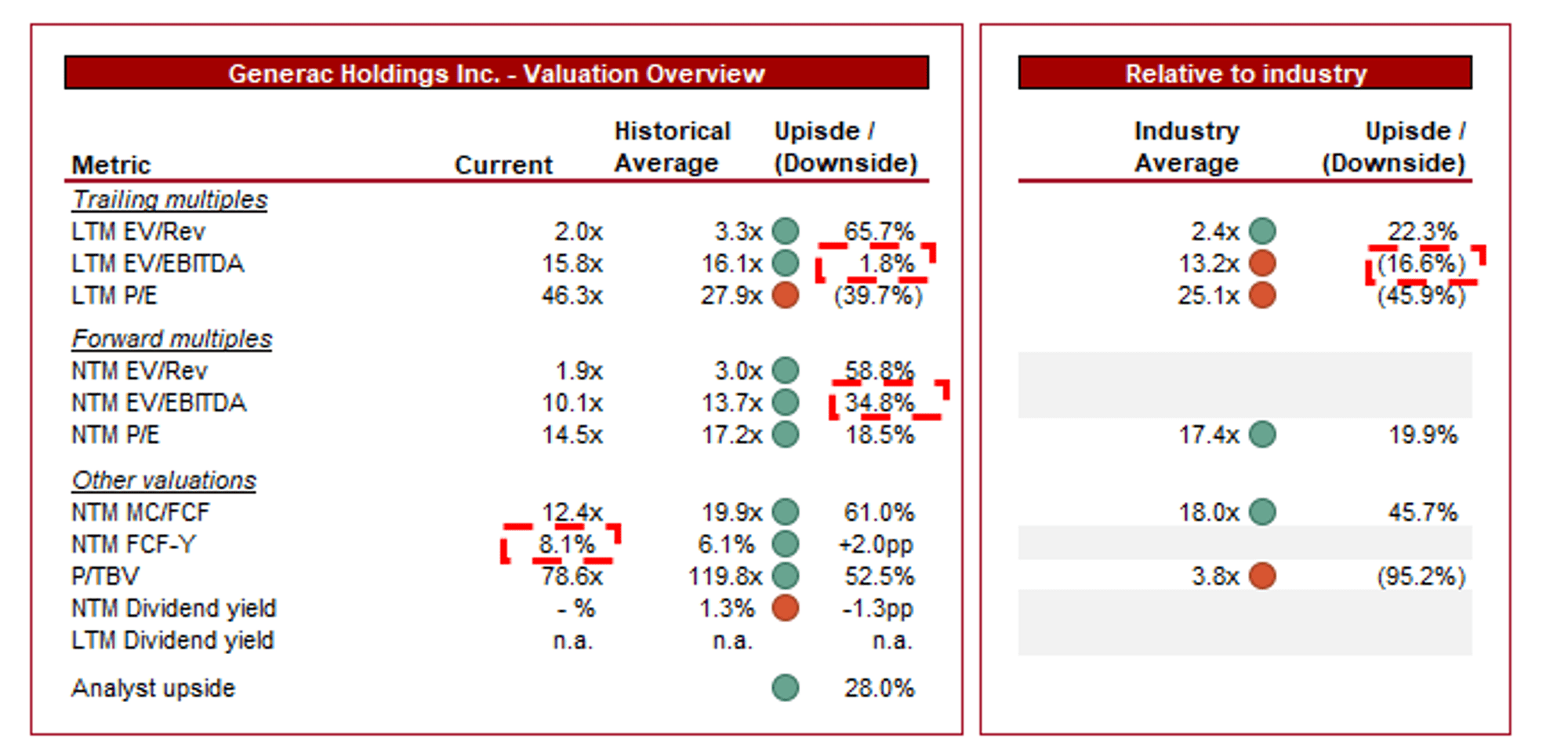

Valuation

{kind=link}

Generac is currently trading at 16x LTM EBITDA and 10x NTM EBITDA. This is a discount to its historical average.

The discount valuation is a reflection of the decline in profitability and near-term financial concerns. This is not necessarily a large discount, however. A portion of investors are confident that the business will achieve margin improvement and return to its growth trajectory. This is the same reason for the LTM premium to its peer group.

Our view is that the current share price now represents a good entry point from which to start building a position. The company’s NTM EBITDA multiple is at a discount to its historical average, as is its NTM P/E compared to its peers. Further, its NTM FCF yield is sufficiently above the average and at an attractive level.

Key risks with our thesis

The risks to our current thesis are:

- Macro conditions. Current macro conditions are the primary risk associated with Generac. A revival of fortunes is inevitable but the timing of this remains uncertain. Economic expectations are changing regularly and there is yet to be a clear consensus as to when rates will decline.

Final thoughts

Generac is a highly attractive business in our view. The company is benefiting from a range of tailwinds, underpinned by the quality development of its business model. The timing of growth improvement remains uncertain, particularly due to economic conditions, but nevertheless, we see this as a solid long-term investment.

With scope for an EBITDA-M of ~22% and a comparably attractive FCF, shareholder returns will accelerate. At a current FCF yield of ~8%, the returns already appear attractive. We rate the stock a soft buy, with a good opportunity to buy in over the coming quarters.

For further details see:

Generac: Helping To Power An Electric Future, Growth Trajectory Appears Sustainable