GNRC - Generac's Q3 Confirms 2023 Sales Decline Remains A Hold

2023-11-04 01:32:37 ET

Summary

- Generac's Q3 results suggest a significant decline in Y-O-Y sales for 2023. In the absence of some new catalyst to revive sales growth, this could signal stagnation for the foreseeable future.

- There is still the ongoing potential sales growth driver, namely declining public confidence in the grid system.

- Factors such as declining household financial health and purchase & operating affordability issues pose risks to Generac's business model and sales growth.

- For now, the growth-driving factors, and the potential sales-dampening factors could cancel each other out, even as Generac's stock is priced for growth. A lack of a dividend adds to the unfavorable buy & hold investment thesis.

- Some potential growth segments such as solar-powered generators, as well as external factors, could still drive future growth, which is to some extent already priced into the stock, which for now makes it a hold.

Investment thesis: With the post-COVID bump in its stock price behind us, Generac (GNRC) stock is now starting to approach attractive price levels, keeping in mind potential catalysts and opportunities to grow sales, it could potentially see some trends that have the potential to push its stock price higher. One such catalyst is an arguably higher level of household interest in gaining some degree of independence from infrastructures we became accustomed to depending on, such as the power grid. On the other hand, a combination of factors, including increasingly strained household budgets, competing alternative products, as well as potentially internal company-specific issues with execution present an arguably high-risk company profile, which should be factored into the valuation of the company when one looks at a buying opportunity. Despite a decent Q3 report , Generac is still a hold from my perspective as it was in the Spring when I last covered it unless some of the challenges associated with finding a path back to growth are addressed, either internally within the company itself or through external intervening factors.

Q3 was hailed as very positive by the market, even as it confirms that 2023 will be a down year for sales

As I write this, Generac's stock price gained about a fifth in value compared with its pre- Q3 release . While the results were decent, the numbers by no means signal a return to growth it confirms that sales will be down significantly for the year, in the absence of an unlikely blowout result in Q4.

Quarterly sales were down just marginally compared with the same quarter from last year, at $1.07 billion, compared with $1.09 billion for Q3, 2022. For the first nine months of the year, sales were down about 16% compared with the corresponding period in 2022. The part that the market probably cheered was the increase in earnings attributable to Generac shareholders, of $60.4 million, which was up by about 3.5% compared with Q3, 2022. It should be noted that with a profit margin of 6%, it will not take a significant increase in costs of production to erase those earnings.

One rather troubling aspect of the latest results shows a doubling of interest expenses in the first nine months of the year compared with the corresponding period in 2022. Those expenses came in at just under $73 million. As a percentage of total revenues of just under $3 billion, it comes out to 2.4% of revenues. I tend not to be overly concerned about this ratio unless it surpasses about 5% of the total revenues, but the significant increase in interest costs necessitates closer monitoring of the trend from now on.

Generac's stock price has had a very wild beginning of the decade

Just before the COVID crisis, Generac's stock was trading at just over $100/share. It saw constantly impressive sales growth in the years prior, and it was assumed that the crisis we went through would lead to an explosion in demand, in response to fears of societal implosion.

{kind=link}

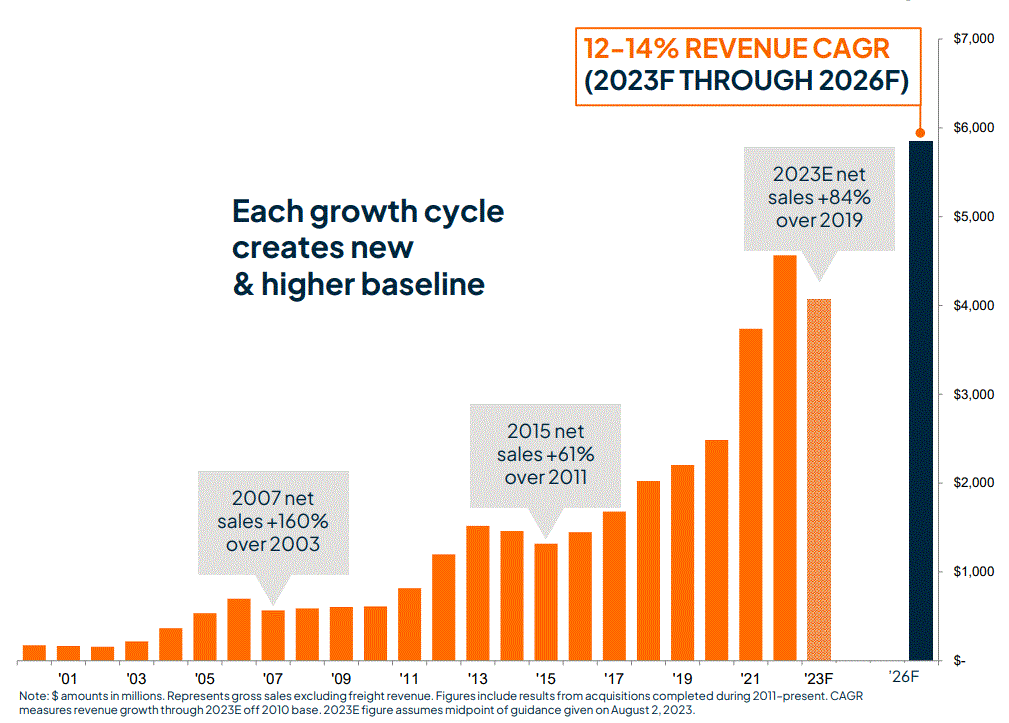

While the crisis does seem to have pushed Generac's sales volumes higher at an accelerated pace, it is not currently clear whether this may have been a peak in sales for the foreseeable future, or whether we will see a continued rise in sales as Generac is forecasting for the next few years to 2026.

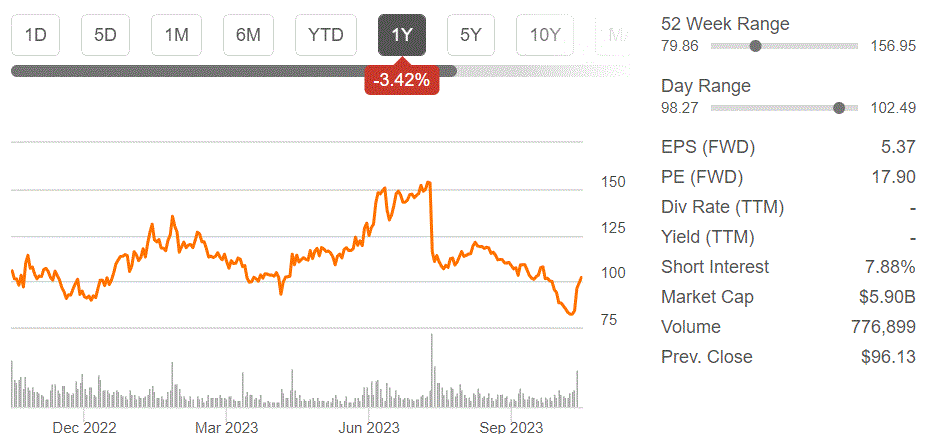

Generac's stock responded to the COVID-driven chaos by rising from just over $100/share at the end of 2019 to over $500/share by November 2021. It is currently down to just over $100/share, which is about the same compared with the end of 2019. Where it will go from here depends to a great extent on whether the company can show that it can continue growing sales and improving profits.

{kind=link}

With a forward P/E ratio of almost 18, it is still priced by the markets for at least some moderate but steady growth. If in the next few quarters Generac fails to show an ability to resume a path of sales growth and better profit margins, its stock price will most likely have another significant decline going forward in the next year or two, as the valuation will most likely rebalance toward a changed market perception that will reflect a new thesis of sales stagnation, at which point it will take some dividend payments and other measures meant to provide long-term shareholders with value to make the stock attractive.

Generac's growth prospects & sales decline risks

While Generac continues to forecast robust steady sales growth for the next few years, my personal view is that things could go either way, with several factors potentially having a positive impact, while others could inflict a decline in market demand for Generac's products. It is in my view impossible to make a powerful case for sales going either way. I see a good chance that positive and negative factors may largely cancel each other out, leaving a near-stagnation in sales as perhaps the most plausible scenario.

The main theme that continues to be a driver of optimism regarding future sales prospects for Generac products is the arguably increased public perception of a decline in institutional reliability, including the reliability of the grid system . Whether it may be due to perceptions of higher weather-related risk, due to climate change, or a perceived lack of investment in the grid infrastructure needed to keep it from failing fewer people seem to be confident in it. I don't personally see this perception changing any time soon.

On the negative side, there are arguably plenty of factors working against Generac and its business model. One of those factors is the declining financial health of households. Simply put, as more households are just barely getting by, fewer will be willing to invest in an emergency generator.

{kind=link}

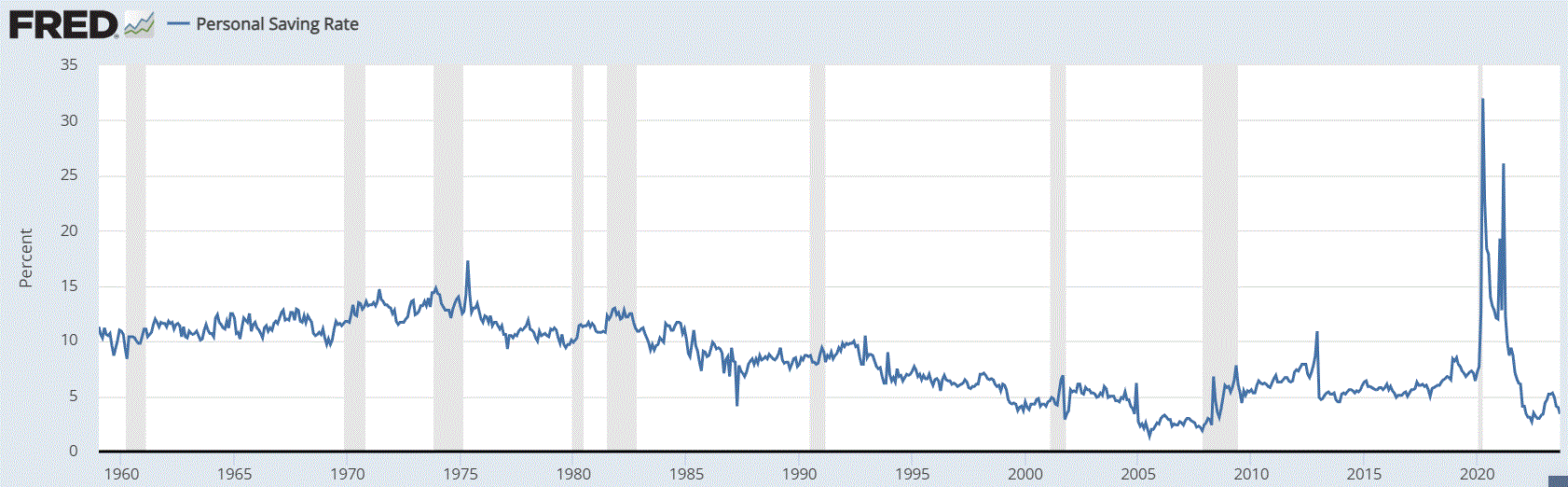

As we can see, personal savings rates are at a very low level, meaning that households are unable to save much money. Coupled with other metrics, such as rising personal debt , which is an indication of consumers being unable to fund their growth in purchases from rising incomes, but rather rely on cutting back on saving money, while increasing their debt load, it paints a picture of an unsustainable situation where consumers are likely to cut back on spending. In such a scenario, immediate needs will take precedence over future needs, or hypothetical needs. It goes without saying that in the absence of a substantial increase in the perceived threat to household safety posed by increasingly unreliable grid power deliveries to households, Generac's products will continue to be seen as a largely hypothetical need, not an immediate need such as buying gas for the car or food for the household.

Affordability issues, not only for the system itself but also fuel costs-related issues may also come into play. The propane generators can cost as much as $220/day to run non-stop assuming propane costs of $2.50/gallon. The natural gas line connected generators can use almost 10 cubic meters of natural gas per hour, for about 240 cubic meters/day. Given average natural gas prices in recent months of about $300/1,000 cubic meters, the costs can amount to about $70/day. If propane or natural gas prices were to spike, those costs could rise significantly.

The costs of a prolonged outage can look prohibitively expensive to cover, in addition to the cost of the generator's purchase & installation. There is also the issue of running out in the case of propane, in the event of a longer emergency. Natural gas supply disruptions in an area may be the culprit responsible for the grid outage to begin with, therefore depending on a steady supply of natural gas may not be as appealing to some potential customers.

Generac does have alternative systems, such as solar-powered backup generators, but it remains to be seen how much traction these products can gain. Because solar-powered generators have the potential to negate some of the disadvantages that propane or natural gas-powered generators pose to customers, I see this path as being the most promising for the long term. From my perspective, a solar-powered generator has the distinct advantage of providing prolonged minimal comforts in case of a risk of major, prolonged disruptions to the power grid, whatever the cause may be. It should be noted however that when it comes to such generators, there is already sizable competition to deal with, which I foresee to greatly amplify going forward.

Investment implications:

Just before the Q3 results were announced, I was tempted to take up a small position in Generac stock, as it was trading in the low $80s/share. In the end, I decided not to, given that investing just before quarterly results come out tends to be a bit of a gamble, rather than an educated bet, based on fundamentals. Taking a step back, Q3 still signals at best stagnation in Generac's sales growth. Worse, the macro trends I cited, mostly focused on the state of the consumer, suggest that fewer households will have the financial resources needed to satisfy a desire to ensure well-being in case a hypothetical threat becomes reality. More and more households will most likely focus on immediate needs while trying to rein in spending.

In the absence of a solid long-term sales & earnings growth thesis that could be made based on current information available, I do not see a very strong case to invest, given that its current P/E ratio is reflecting a market consensus that seems to expect relatively robust growth. As I pointed out in my last article on Generac, I would like to see a P/E ratio closer to 5 than somewhere between 15 and 20 where we are right now, given a less-than-certain outlook for growth. For that to happen, we would have to see an improvement in profitability, a further decline in its stock price, or both.

I am watching for signs that a catalyst may occur that could re-constitute Generac's growth story. Perhaps a better solar-powered backup generator solution will take off. Perhaps there will be an amplified feeling of public insecurity, which will make more households eager to purchase a generator, just in case they will need to become more self-reliant. Having said that, when we reach such high levels of public insecurity or the perception of it, economic insecurity may come with it, making it less likely for many households to consider major purchases, including backup generators.

Whether we will see new Generac products taking off, gaining a foothold in the market, or whether an external catalyst will lead to a surge in sales, there is still a growth story thesis that can be made in favor of this company for the future. For now, however, there is no indication in my view that Generac is poised to see a surge in sales, while the P/E ratio that it trades at has significant growth priced in. The lack of a dividend also makes a buy & hold at current valuation levels less attractive. A dividend would have the net effect of lessening the investment risk for its stock in the long term while acting as a return-enhancing mechanism if Generac's stock price sees some significant upside from current levels. The lack of a dividend makes a long-term buy & hold position unappealing, given the lack of confidence I currently have in Generac's ability to grow sales & improve profits. The stock therefore remains a hold at current levels in my view, unless a catalyst will come along to change the thesis.

For further details see:

Generac's Q3 Confirms 2023 Sales Decline, Remains A Hold