GNW - Genworth Financial: Beaten Down Valuation Makes It A Buy

2023-06-20 17:45:10 ET

Summary

- Genworth Financial's stake in Enact Holdings is worth over $3 billion, making the company undervalued with a market cap of around $2.4 billion.

- The company has improved its balance sheet, reduced debt, and built a solid investment portfolio, supporting the investment case at current price levels.

- Risks include losses in the long-term care insurance segment and potential impact on financial strength ratings.

Investment Rundown

Genworth Financial, Inc. (GNW) is a company that offers mortgage insurance, life insurance, and long-term care insurance. Its primary subsidiary, Enact Holdings (ACT), plays a significant role in generating net profits.

One of the main appeals of investing in GNW right now is the sheer stake they have in Enact. GNW has a market cap of around $2.4 billion right now and over $3 billion in its Enact stake , given the current market cap of Enact. That means right now GNW is trading at a much lower valuation than it should given their assets. I think this opens up a lot of upside potential that investors will be able to capture if buying in at these prices. The impact Enact is having on the operating incomes of GNW is steadily growing and in the last quarter, it amounted to $143 million, up from $135 million a year prior. The positive impact of higher interest rates are having is showcased by the growing incomes for GNW. In the long run, a stake like this should help provide strong appreciation to an investment and GNW is therefore a buy at these prices.

Company Overview

Genworth has made it a priority to give back to its shareholders as they continue to buy back shares at a decent rate. GNW managed to return $68 million to their shareholders in the first quarter of 2023 through buybacks. It's only quite recently that GNW is actually managing to enact a yearly decline in their share count. Historically , they have been diluting shares but this shift in trends is playing into the bullish thesis regarding the company. Even if they don't see a valuation reflecting the true value of the business I think repurchases like this will help bring value to investors nonetheless.

Company Debt (Macrotrends)

Supporting this move by the company is a much more manageable balance sheet. Over the last few years debt reduction has been a key focus for the company, leading to a decrease in outstanding debt. Moving forward, these efforts will enhance the business model. Additionally, the company's board has approved a share repurchase program, aimed at delivering significant value to shareholders. This improved business model has meant a lot as they received improved credit ratings from rating agencies. This is a crucial factor for an insurance company as it allows for attracting competitively priced premiums through strong financial strength ratings. Going into the coming quarters I think it's reasonable to expect a continuation of this trend and that GNW will maintain a strong balance sheet with cash and liquid assets increasing for the $223 million they had in Q1 2023.

Strong Portfolio

Historically the revenues of GNW have been anything but consistent. They seemed to have peaked around the $8.7 billion mark back in 2014 and right now sit at a TTM of $7.4 billion. Over those years the shares outstanding have risen and little share appreciation was had, as the share price is down 53% on the 10-year chart.

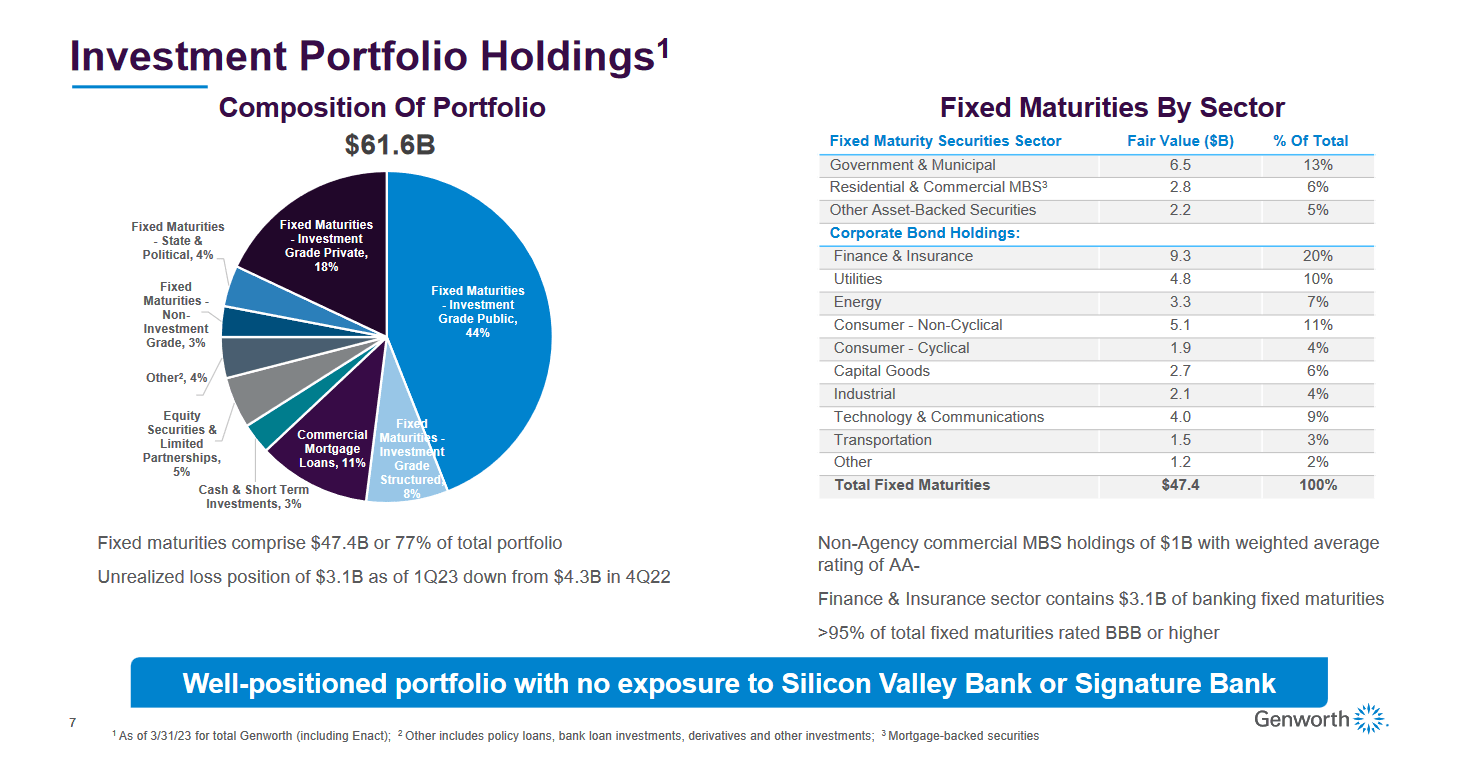

But with GNW improving its balance sheet and in turn, its rating increased as they maintained a strong amount of liquidity. The investment portfolio of the business has grown strongly and now sits at $61.6 billion, where fixed maturities comprise 77% of the overall portfolio.

Investment Portfolio (Investor Presentation)

{kind=link}

GNW also maintains 16% of the total investment portfolio in real estate, and with the overall weighted average rating for this BBB+, with a solid combination of asset compositions which helps protect their credit and also aids in preserving higher principles. All in all, GNW has built up a solid portfolio that further supports the investment case at these price levels.

Risks

One of the main risks regarding GNW is not their balance sheet, but rather one of the segment in the business. Most notable is the "long-term care insurance" segment. GNW is still noting a loss in this part of the business. A negative operating income of $37 million will (if not improved) start to dig into the earnings of the business and that is a good argument for the lower valuation which the company is currently receiving. When improvements are made here, then I think we will see the share price climbing higher to reflect the equity reserves they have on hand.

Earnings Q1 (Earnings Report Q1)

The losses did grow on a yearly basis which further has helped to keep the share price within the $5 - $6 range the last few months. Ratings are an important part of the insurance market as I mentioned before, with GNW having $3.1 billion in unrealized losses if they see this amount increasing it might hurt their image a fair bit. The lower financial strength of the business would make it much more difficult to write both premiums and obtain further reinsurances.

Final Words

As mentioned, the main attraction going with GNW right now is the amount their stake in Enact is worth right now. The TTM p/b is just 0.33 right now as the stake in Enact is worth somewhere over $3 billion, more than the market cap of GNW right now. With a book value per share right now of $15.26 the upside potential right now seems too good to pass up on and not rate GNW a buy. The book value may have gone down over the last few years as in September GNW sold off some of their stake in Enact. With Enact responsible for a substantial amount of the operating income for GNW this should be a strong tailwind going forward until GNW is able to raise the margins in their long-term care insurance segment. The insurance market is steadily growing and I think GNW has set itself up very well to capture a similar growth rate. The valuation right now offers plenty more upside potential than downside risk in my view, and so Genworth Financial Inc is rated a buy.

For further details see:

Genworth Financial: Beaten Down Valuation Makes It A Buy