GNW - Genworth's Sum Of The Parts May Be Greater Than The Whole

2023-11-21 05:46:34 ET

Summary

- Genworth Financial shares have performed well over the past year, despite the company's struggles in the long-term care insurance business.

- The company's structure protects it from having to inject capital into the struggling long-term care entity, which may eventually go bankrupt.

- Genworth's stake in Enact is worth more than the company's current market value, providing potential upside for investors.

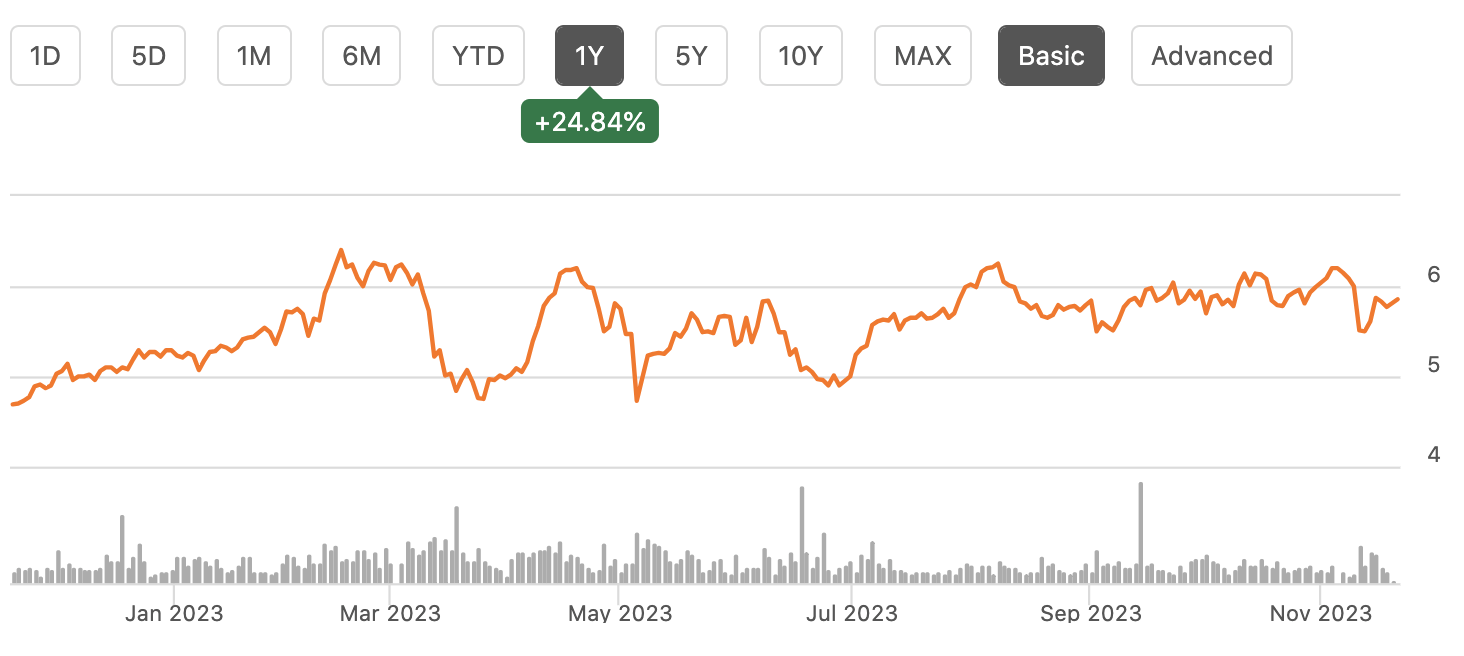

Shares of Genworth Financial ( GNW ) have been a strong performer over the past year, rising by about 25%. This is a company that has had a difficult time. The long-term care insurance business has been a disaster, which is why shares are 62% lower than ten years ago. GNW also spent five years trying to close its acquisition by a Chinese firm before eventually abandoning it due to regulatory scrutiny. However, there is now a compelling opportunity in its shares, given the disconnect between its value and the sum of its parts.

{kind=link}

In the company’ third quarter , Genworth earned $0.09 relative the $0.25 analyst consensus . The company has multiple segments. First, it owns 81.6% of Enact ( ACT ), meaning it consolidates its financials into its results, but it is a separate company. Enact earned $134 million in adjusted operating income, from $156 million last year. Long-term care and life lost $74 million from a $20 million profit last year.

This significant deterioration in long-term care ((LTC)) may seem really concerning, but in reality, I see upside for GNW even if LTC goes bankrupt. I know this sounds very provocative but let me explain. It comes down to how insurance companies work and how Genworth is structured. Most companies you invest in on the stock market are really dozens of legal corporate entities, owned by a parent or “holding company.”

Genworth Financial’s holding company is the entity you are really buying equity in when you buy GNW stock. This is the entity that buys back shares or would pay dividends (in theory as GNW does not pay a dividend). The holding company however does not write the insurance policies, and it is not responsible for paying out policyholders.

Rather, the holding company owns 100% of the equity in an insurance operating company, which is the entity that collects premiums, writes policies, and pays claims. This structure is in place to protect insurance policyholders. The holding company cannot simply withdraw cash from the operating company. Rather, the operating company must have sufficient capital, and if not, regulators can block capital transfers to the holding company, essentially starving the HoldCo and public shareholders to keep capital in the operating company to pay out as many claims as possible.

Now just over a decade ago, as described in the below portion of the 10-Q, Genworth was able to do a restructuring of its legal entities in the recognition that long-term care insurance was significantly mispriced. It essentially created the insurance equivalent of a “bad bank/good bank” structure to isolate the long-term care and life insurance exposures.

{kind=link}

At this point, Genworth is essentially just running this operating company for the benefit of policyholders, trying to find ways to pay the highest share of claims as possible. This below is the key point from the company’s latest earnings presentation . GNW is not going to put in good money after bad, and it will not move any cash into these bad bank entities. By the same token, given their weak capital and solvency position, GNW does not assume it will ever be able to withdraw capital from them either, and as it manages the holding company, it assumes zero value from these operating companies.

Genworth Financial

This is why I say investors should not worry that much about long-term care’s results. At some point, the entity may well go bankrupt (to be clear, I am not saying it will definitively, just that is a very real risk). However, GNW has no legal obligation to inject capital into it to pay policyholders. It cannot take capital out given the magnitude of its liabilities, but it has no requirement or interest in putting cash in. That is why I say the entity is being run for policyholders—there is essentially no equity value. It is a matter of trying to pay out as much in claims as possible.

When an insurance company faces insolvency, regulators often allow it to increase premiums on customers, essentially retroactively re-writing contracts. Since 2012, GNW has reduced its potential benefits payout by 48.8%. Regulators approve this because it is better for all policyholders to receive something, than for early claimants to receive 100% and have nothing left for later claimants. This has reduced the present value of Genworth’s long-term care costs by $25 billion. Considering the entity has just $3.2 billion in statutory capital, the savings are gigantic. These cuts are the only reason the operating company is still operating, and it also shows how wildly mispriced long-term care insurance was.

Genworth continues to take rate actions to try to and reduce its liability further to extend the lifespan of the operating company. It has primarily focused on reducing the most favorable benefits. For instance, there has been a 46% reduction in policies with unlimited benefits and a 28% drop in those paying 5% inflation annually. In Q3, it filed for $273 million in new premium actions and registered $83 million of approvals. Interestingly, lengthening the lifespan of long-term care, even if it eventually fails and is seized by regulators, does provide some benefit to shareholders.

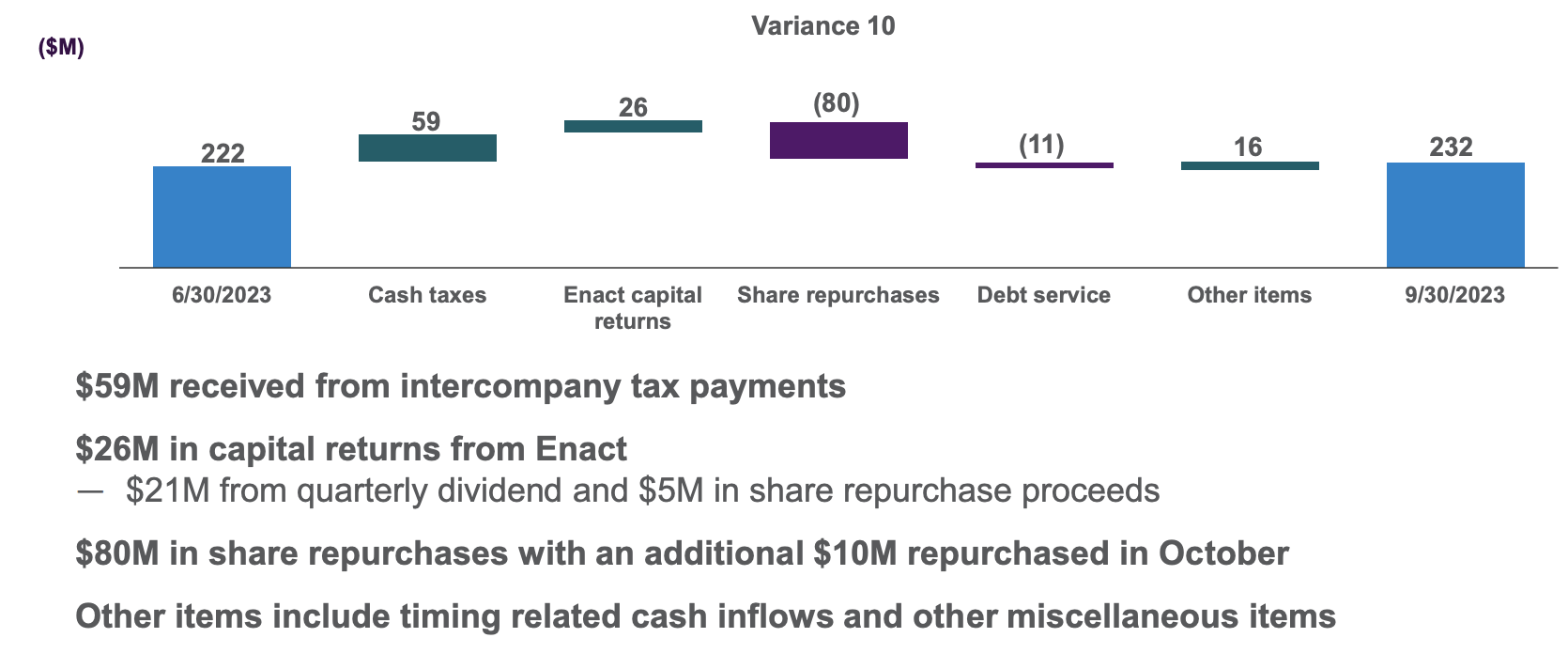

While GNW’s holding company cannot take capital out of the operating company, taxes do flow up. In the quarter, $59 million of taxes have been sent to the holding company. The holding company is the entity that pays taxes, just like how it is the one who makes share repurchases. However because of all of the losses from LTC over the years, GNW has a $1.58 billion deferred tax asset.

{kind=link}

The operating company sends cash to the parent for the theoretical tax bill on the interest it earns on its portfolio, but GNW does not actually have to send all of those funds to the applicable federal, state, and foreign governments, instead using its deferred tax asset. While its GAAP tax liability has been $140 million (it also has a tax liability from ACT dividends and capital gains), it has only paid $5 million in taxes. Because tax accounting is different than GAAP or statutory accounting, it received an intercompany cash payment for taxes even as LTC had a $71 million operating loss.

This is why I view GNW as a really interesting investment opportunity. As noted above, GNW owns 81.6% of Enact. That stake is worth $3.61 billion at today’s share price. Genworth is worth $2.71 billion today. That is a $900 million disconnect. Now, GNW does have a consolidated debt load of $1.6 billon. However, remember it consolidates Enact, which has $744 million of debt and is already reflected in where its shares trade. GNW’s holding company has $856 million in debt, against which it also has $232 million in cash, for a net debt position of $524 million. GNW has also been repurchasing debt below par, reducing its net debt load accretively.

Combined, GNW has a $3.35 billion enterprise value, but its stake is worth $3.61 billion in Enact. That provides an 8% upside to shares to close that gap. However, that is before considering the tax payments the LTC unit sends to the parent, which it can largely use for share repurchases, given its deferred tax asset. In Q3, GNW received $236 million in annualized cash taxes. Below, I showed what the next six years’ payments would look like assuming 10-50% annualized declines in this tax bill.

{kind=link}

Even if we assume 30% declines between now and 2029 and that the LTC operating company ceases operations by then, the present value of those payments is $386 million, discounted at 10%, or $0.83 per share. That provides an additional 15% of upside to fair value, or 23% in total. Additionally with GNW aggressively buying back stock, this valuation gap is widening. It has bought back about 8.5% of the company over the past year. Even if LTC is doomed to fail, every extra day GNW keeps it operating is another day in which it receives tax payments that end up rewarding shareholders as it works down its large deferred tax asset, primarily to state governments.

This is why I view GNW as a compelling, sum of the parts value play. It start out 8% cheaper to just buying shares in ACT, assuming no value in its own insurance operating companies. However, while they have no equity value, their cash tax flow is actually value-creative given GNW’s holding company’s tax position. Now, as noted, the company is paying some cash taxes, given limitations around DTA usage, but the company should continue to receive more in tax payments than it pays out to taxing authorities.

For conservatism in setting a price target, I would use the down 40-50% annualized tax benefit, alongside the assumption of no residual value in this entity. That ~$0.50 benefit combined with the 8% discount to its ACT equity position, provides about 16% upside, and I look for shares to trade to $6.75-$7.00 over the next year. If management proves to be able to get enough rate actions to make LTC a solvent long-term business, that provides even more upside, but I do not assume this will occur in reaching my price target.

For further details see:

Genworth's Sum Of The Parts May Be Greater Than The Whole