JBI - Gibraltar Industries: This Play Still Has A Bit Of Room To Run

2023-09-12 14:36:02 ET

Summary

- Gibraltar Industries, Inc. has seen a significant increase in its stock price, outperforming the S&P 500.

- The company's revenue has been impacted by a drop in demand for solar module installations and challenges caused by the Uyghur Forced Labor Prevention Act.

- Despite the challenges, Gibraltar Industries has been performing well on the bottom line, with net profits increasing year-over-year, and shares look cheap enough to warrant some additional upside.

One of the best-performing companies that I have written about over the past several months is Gibraltar Industries, Inc. ( ROCK ). The firm, which operates as a producer and installer of solar racking and electrical balance systems, as well as other related offerings, has done quite well, especially on its bottom line, over the past few quarters. It's also worth noting that the company produces a wide variety of other products, such as roof and foundation ventilation products and indoor growing systems for cannabis and other plants.

Given how much the stock has shot up, I can understand why some investors might opt to look elsewhere for opportunities. But I would argue that a little more upside is still likely on the table from this point.

Shares are still decently priced

After recognizing the attractive growth rate and the low price of the shares of Gibraltar Industries back in early January of this year, I had no choice but to rate the company a "buy." However, even back then, I did not yet have an idea exactly how much upside shares would see in such a short window of time. Since the publication of that article, the stock has skyrocketed 53.4%. That's at a time when the S&P 500 (SP500) has gone up just 16.8%.

{kind=link}

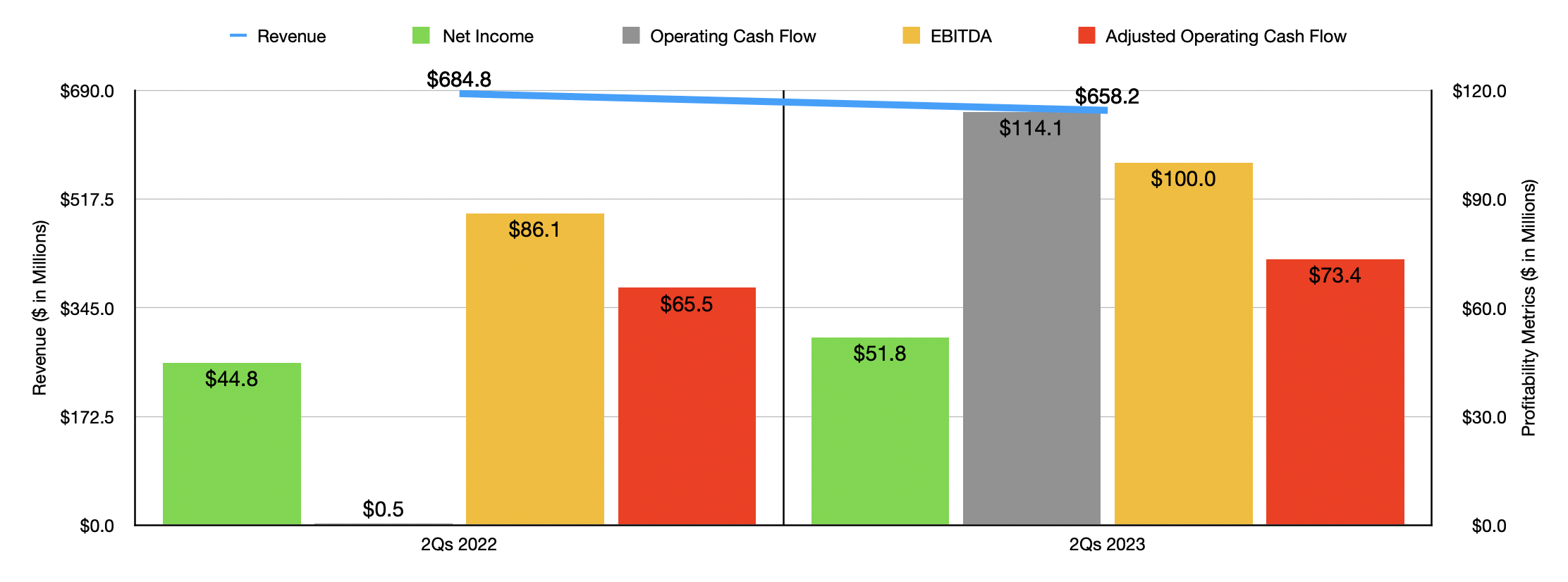

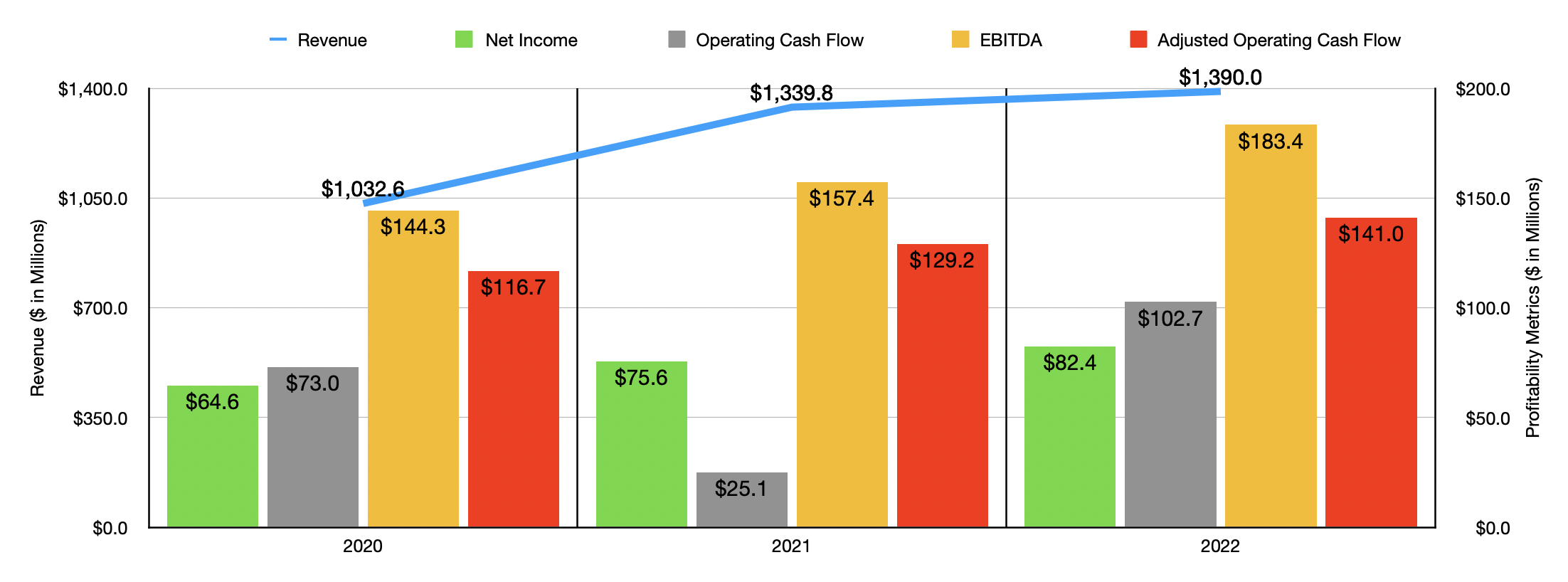

This significant appreciation can mostly be chalked up to strong bottom line results. This is not to say that the company hasn't done okay on the top line. After all, in 2022 , revenue of $1.39 billion beat out the $1.34 billion the company reported in 2021. But we have seen revenue falter some since then. For the first half of 2023, for instance, management reported sales of $658.2 million. This is actually down 3.9% compared to the $684.8 million the business reported one year earlier.

From an organic perspective, sales so far this year have been down across three of the firm's four operating segments. The only one to see some upside was the smallest, known as the Infrastructure segment. Revenue there popped from $38.6 million to $42.9 million. That increase, totaling 11.1% year-over-year, was due to solid market demand thanks to infrastructure investments initiated and supported by the federal government. To make things even more exciting, strength is expected to continue on this front. I say this because, year-over-year, the backlog for that segment is up 46%.

It is true that the Residential segment also performed well, with revenue climbing $28 million from $379.7 million to $407.7 million. But this was driven by a $39.8 million contribution from the company's acquisition of QAP. Without that, revenue would have fallen by $11.8 million. This leaves us with the Renewables and Agtech segments. Both of them took a beating. Sales under the former plummeted $43.7 million, or 24.2%, while for the latter sales were down $15.2 million, or 17.7%.

In the case of the Renewables segment, the company experienced downside because of a drop in demand for solar module installations. Timing delays resulting from a longer permitting process hit this segment. But even more significant, it seems, were challenges caused by the Uyghur Forced Labor Prevention Act. Because of human rights abuses in the Xinjiang region of China, the government here in the U.S. passed the bill, known as the UFLPA for short, to prevent the importation of components that are sourced within that region. Add in the fact that we already are dealing with supply chain issues in general, and this makes the problem worse for companies like Gibraltar Industries that rely on panels shipped from China to the U.S. By comparison, the pain under the Agtech segment was far more mundane. Its drop was driven by customer-driven delays in project starts on the commercial side.

{kind=link}

On the bottom line, however, Gibraltar Industries has been performing quite well. Net profits went from $44.8 million in the first half of 2022 to $51.8 million at the same time this year. This follows a trend of year-over-year improvements on the bottom line. As you can see in the chart above, from 2020 through 2022, net profits for the company rose year after year, climbing from $64.6 million to $82.4 million. Management actually expects this trend to continue. With revenue likely to come in at between $1.36 billion and $1.41 billion for this year, earnings per share, at the midpoint, should translate to net profits of $109.2 million.

Other profitability metrics have also improved during this time. Operating cash flow, for instance, has gone from only $0.5 million to $114.1 million. If we adjust for changes in working capital, we would see an increase from $65.5 million to $73.4 million. Meanwhile, EBITDA for the business jumped from $86.1 million to $100 million. As was the case with net profits, the general trend for each of these profitability metrics has also been better year-over-year. Unfortunately, management has not provided any guidance for 2023 as a whole. If we assume that these other profitability metrics will rise at the same rate that net income should, we would get an adjusted operating cash flow of $186.9 million and EBITDA of $243 million.

{kind=link}

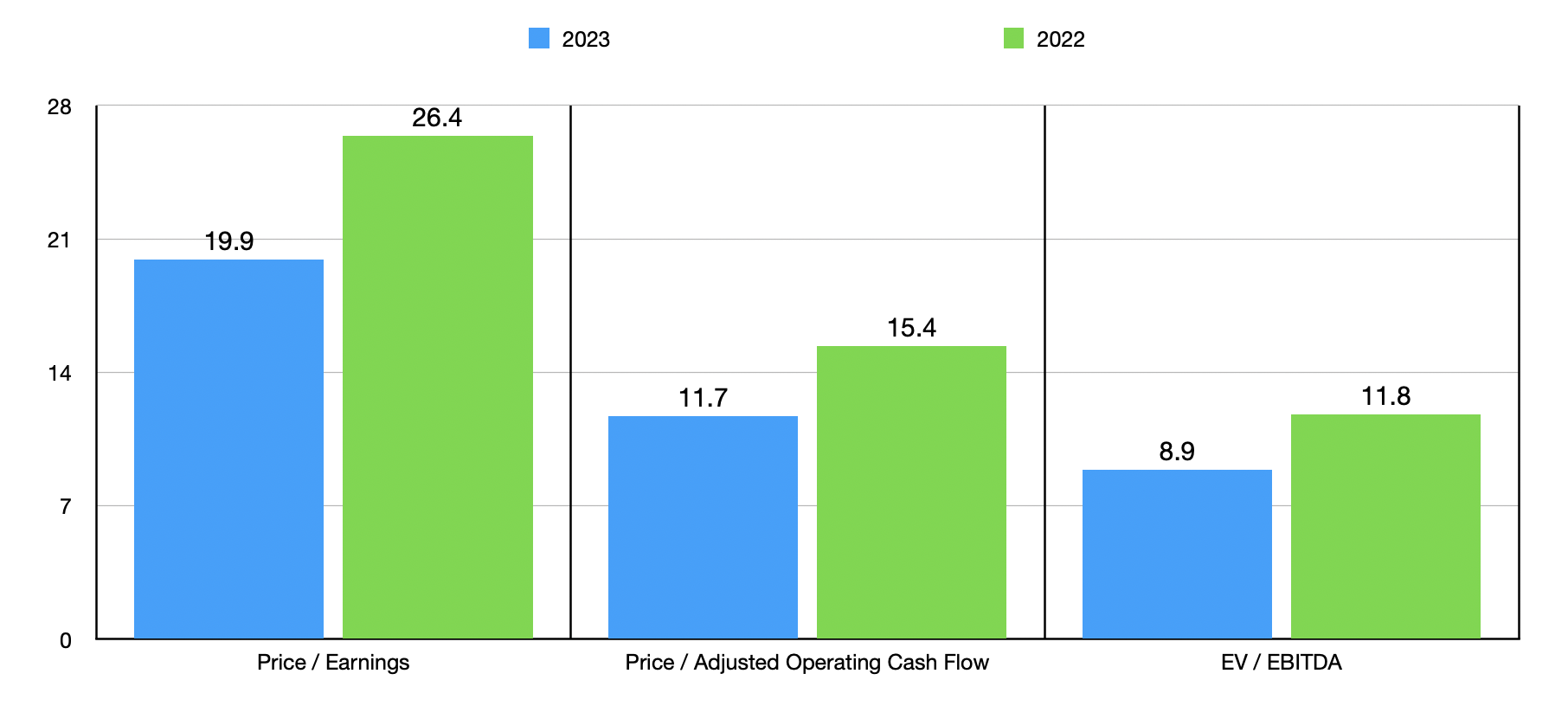

Using these figures, I was able to create the chart above. It prices the company using forward estimates for 2023 and using historical results for 2022. Using the 2022 figures, I would argue that the stock looks more or less fairly valued. But on a forward basis, it does still seem to offer a bit of upside. As part of my analysis, I also compared it to five similar companies. In the table below, you can see that, on both a price to operating cash flow basis and on an EV to EBITDA basis, three of the five firms were cheaper than Gibraltar Industries. And when it comes to the price to earnings approach, four of the five were cheaper.

| Company |

| Price / Earnings |

| Price / Operating Cash Flow |

| EV / EBITDA |

| Gibraltar Industries |

| 19.9 |

| 11.7 |

| 8.9 |

| Janus International Group ( JBI ) |

| 12.1 |

| 10.9 |

| 7.7 |

| Tecnoglass ( TGLS ) |

| 8.5 |

| 14.2 |

| 5.5 |

| PGT Innovations ( PGTI ) |

| 15.7 |

| 9.6 |

| 9.5 |

| CSW Industrials ( CSWI ) |

| 28.7 |

| 18.1 |

| 16.9 |

| Masonite International Corporation ( DOOR ) |

| 12.7 |

| 5.9 |

| 7.7 |

One other thing that I would like to touch on is what the future might hold for the business. Earlier in this article, I mentioned the impact that the UFLPA has had on sales. Very likely, it has also impacted profits. But we don't know the extent to which this is the case. In a recent investor update, management said that customers in general expect panel flow to improve in the second half of this year. There are also some other improvements being made. For instance, in a final report issued by the Department of Commerce in August of this year, three out of eight suppliers were found not circumventing restrictions, and they were able to export to the US without being hit with a duty. And it was also ruled that if four out of six non-wafer components are sourced outside of China, then no duty would be applied for the panels, irrespective of other components.

I see this as very much a short-term problem. In the long run, this is still a very attractive market for Gibraltar Industries to play in. Back in 2020, for instance, the total U.S. solar market was estimated to be worth $14 billion according to management. This should climb to $22 billion by 2025. However, Gibraltar Industries does not play entirely in this space. The specific market segments that they focus on were worth about $4.8 billion in 2020. That number should almost double to $8 billion by 2025. So the overall growth of this addressable market is quite attractive. But it also means that the other market segments could be areas that the business expands into. In fact, they see their Renewables sales climbing from $238 million in 2020 to as much as $700 million by 2025. That's almost double the $378 million the segment was responsible for last year.

Obviously, the other segments that the company has are also going to continue to be focused on. For instance, management expects to grow the Agtech segment from about $161 million in 2022 to $320 million by 2025. However, some of this growth will be offset by a decline in the Residential segment from $767 million to $700 million. As the company focuses on the growth areas it is targeting, it also is likely to continue rewarding shareholders directly through share buybacks and other initiatives. In fact, the company is currently working its way through a $200 million share buyback program. In the second quarter of this year alone, management repurchased $17.8 million worth of shares, taking total buybacks up to 56% of the $200 million that they can between now and 2025. That is great progress.

Takeaway

Fundamentally speaking, Gibraltar Industries is a solid company. Yes, revenue is taking a hit this year so far. However, management expects overall sales to be roughly in line with what they were last year. Profitability, meanwhile, is faring incredibly well.

Relative to the 2022 fiscal year, shares are a bit lofty. Gibraltar Industries, Inc. stock is also a bit pricey compared to similar firms. But on a forward basis, shares do look reasonably attractive. Due to this factor, as well as the temporary nature of some of its problems, I've decided to keep the firm rated a soft "buy" for now.

For further details see:

Gibraltar Industries: This Play Still Has A Bit Of Room To Run