ZY - Gingko Bioworks: Near-Term Challenges Trump Downstream Economics

- Shares of Gingko Bioworks have lost over half their value so far in 2022.

- Successful acquisitions and joint ventures, such as with Bayer, could allow for additional customer capture and revenue acceleration.

- Gingko stands to benefit from current market environment as companies reevaluate their own fixed cost infrastructure and opt to outsource instead.

- While analysts may be overly focused on near-term economics, long-term value creation will come from downstream portion of deals (milestones, royalties, etc.).

- DNA is a Hold, as I cannot justify purchase at current levels even for long-term investors given uncertainties in current business model. Key risks include competition and further dilution.

Shares of synthetic biology pioneer Gingko Bioworks ( DNA ) have lost over half their value so far in 2022. The stock is down roughly 70% since going public in September of last year via SPAC (special purpose acquisition company) merger.

While this space has fascinated me to no end (the idea of programming cells much like we do computers), I've been too intimidated to attempt digging deeper until recent Q2 report demonstrated sufficient promise to warrant further investigation.

In July the company also crossed my radar when management wisely pulled off a cheap acquisition via buyout of fellow synbio pioneer Zymergen ( ZY ) for $300M in an all-stock deal (consider that Zymergen had $225M on the balance sheet at the time). Likewise in the same month, the deal with Bayer to expand capabilities in agricultural biologicals also attracted my attention as it granted the company further validation (Gingko even acquired Bayer's 175,000 square foot West Sacramento Biologics Research & Development site).

Let's take a closer look at why skepticism could be turning to optimism and the company could be turning a corner after the Q2 report.

Chart

{kind=link}

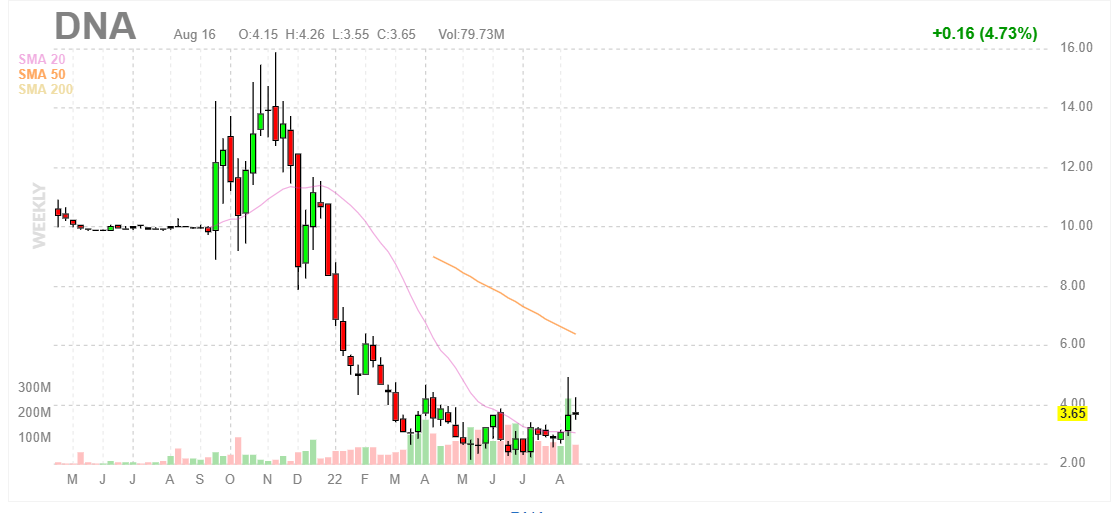

Figure 1: DNA weekly chart (Source: Finviz)

When looking at charts, clarity often comes from taking a look at distinct time frames in order to determine important technical levels and get a feel for what's going on. In the weekly chart above, we can see shares fall a long way from late 2021 highs after going public with bottom currently established around the $3 level. While shares have bounced a good bit after the Q2 report was released, looking at current chart I believe the story is in early innings and risk-tolerant traders could do well purchasing dips in the near term and share price continues higher as sentiment improves.

Overview

Management's presentation at Goldman Sachs gives a better overview of the company and its operations than I ever could:

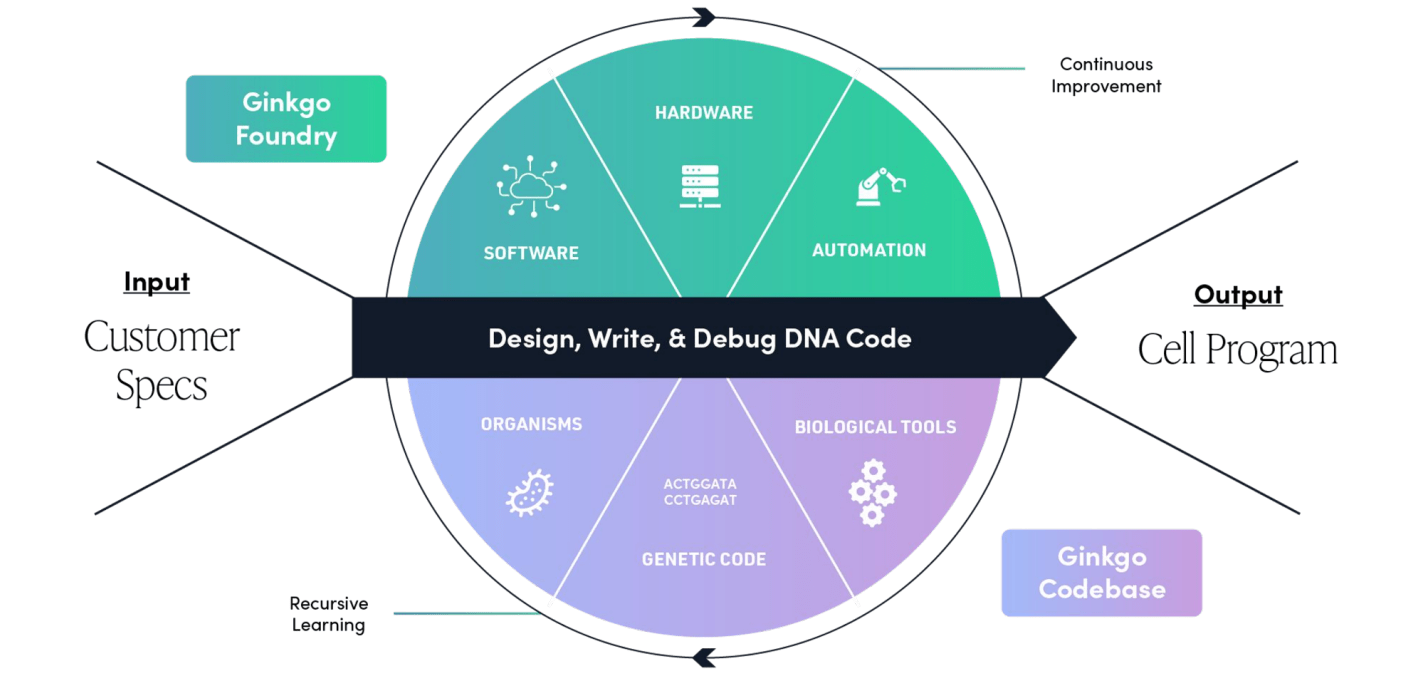

SVP Corporate Development Marie Wagner starts by describing Gingko as being focused on building an integrated, end-to-end enabling platform for companies that are interested in using biology across a range of products for different end markets. Customers come to them with a spec (producing a small molecule, a protein that catalyzes a certain reaction efficiently, a live cell, etc.) and Gingko's job is to design the program and deliver the product they are looking for. They are doing services (but retaining scientific control) and get downstream royalties in form of royalties, equities, milestones, etc.

Leading indicators of the business are a combination of technical developments, expansion of capabilities and scale (including acquisition of Bayer R&D facility where they are essentially outsourcing ag biological R&D to Gingko) and moving into new markets. A more recent transaction was with Novo Nordisk (well-known partner in biological engineering) which provided important validation.

{kind=link}

Figure 2: Gingko platform at a glance (Source: corporate presentation )

There is an ongoing virtuous cycle of value creation and expansion, as new projects completed for customers in a given area spark additional inbound interest from other companies in said area to embark on new projects. They saw that in the cannabinoid space last year, also with new partnerships such as first agriculture deal with Corteva (got a call from third agriculture company that week as it wanted to catch up with competition). There was a natural learning process as they delivered in less sophisticated fields (flavor, fragrance, specialty chemicals, food) to earn their right to move into more complex areas like agriculture and pharmaceuticals.

Platform is comprised of two core components, the wet lab (foundry) uses robotic automation to drive efficiency and scale. The other core asset is Code Base (collection of physical assets, strains, sequences) and digital assets (mapping of genotype to phenotype, enzyme libraries, gene clusters, etc.). They can leverage these when approaching a new problem, like engineering new enzymes with optimized strains for a specific purpose. IP terms are wildly out of market for biotech (CROs do not maintain scientific control of projects), as they own scientific direction of the program and retain ability to reuse the IP. The customer gets an exclusive license for their product and their field (not enabling competitors), but again IP is retained to reuse in other areas. Scaling of the foundry drives scaling of the Code Base (information can be leveraged in the future)- so growth in one result in growth in the other.

Management acknowledges they are currently in a market where cash is important and they are maintaining their cash and cash runway (focusing on cost coverage on deals and derisking in projects without neglecting downstream value). Companies are reevaluating their own fixed cost infrastructure, replacing it with Gingko's capabilities to drive more efficient R&D (thus market environment drives trend to outsourcing more broadly and Gingko stands to benefit). Long term their view is that probability of success gets to a point that is underwriteable and they take most of their value in the downstream rather than the upfront. To maximize TAM and potential value capture, they are aligned with customer in their success and essentially have a toll on the products (the downside is that it will take a LONG time to get to the point where royalties get the company to cash flow positive without charging foundry upfront fees).

In Q4 earnings, they continued to see output of foundry tripling each year (associated with that is 50% decrease in unit cost). The challenge is to keep identifying bottlenecks that they can clear and recent progress is driven by multiplexed operations (run millions of experiments in a single tube with biological tubes, which dramatically reduces costs). More and more tools at their disposal including via acquisitions is helping them deploy this type of technology. Biosecurity industry will emerge, but unlock cybersecurity it will have much more public sector involvement and will be more concentrated. Gingko's biosecurity efforts has earned them seat at the table with US government and international governments (bulk of this will be government contracts to do pathogen monitoring). This will involve a lot of the same tools they use for cell engineering, combined with machine learning to determine whether that DNA is something they should be concerned about. Steady stream of defense contracting business would be a net positive long term.

Bayer partnership in agriculture provided interesting long-term validation for Gingko. This acquisition opens up their capabilities more broadly in this space, as Bayer is committing to much larger collaboration going forward and is allowing them to work with other folks in the space. Agriculture is one of the single most important areas of biology today, these are multi tens of billions of dollars markets they are going after. One of the main competitors is the internal R&D departments within some of the larger companies (had Roche, Biogen and Novo Nordisk come on). Sales cycle here is much longer, unfortunately and is also much more complicated. R&D departments need to validate Gingko's science, which takes time. These are big bets the companies are making, and there can be a mix between testing their toes in the water with a program or two whereas other times they go "all-in". This is a high risk industry so a lot of programs will fail and that needs to be taken into account with calculations.

As for the very difficult competitive landscape in synthetic biology, Gingko has taken the approach of being a platform company with picks & shovels appeal as opposed to single product risk. There are three buckets of customers, including the 99% who are doing it themselves and platform companies in specific niches/application areas (i.e. antibodies). Gingko chooses not to compete in antibodies because there is vertical specific competition in that space. The third area is companies with platforms across industries (predominantly industrial biotech) and those companies focus on having product (high risk bets on individual products). It is very expensive and takes a long time to build a competitive horizontal platform, and Gingko accomplished that in 2016 (8 years after they started). In terms of competitive moat, new horizontal platforms have to slog through the scaling process where they have equivalent efficiency and most capitals won't have enough capital or patience to get to that point.

Other Information

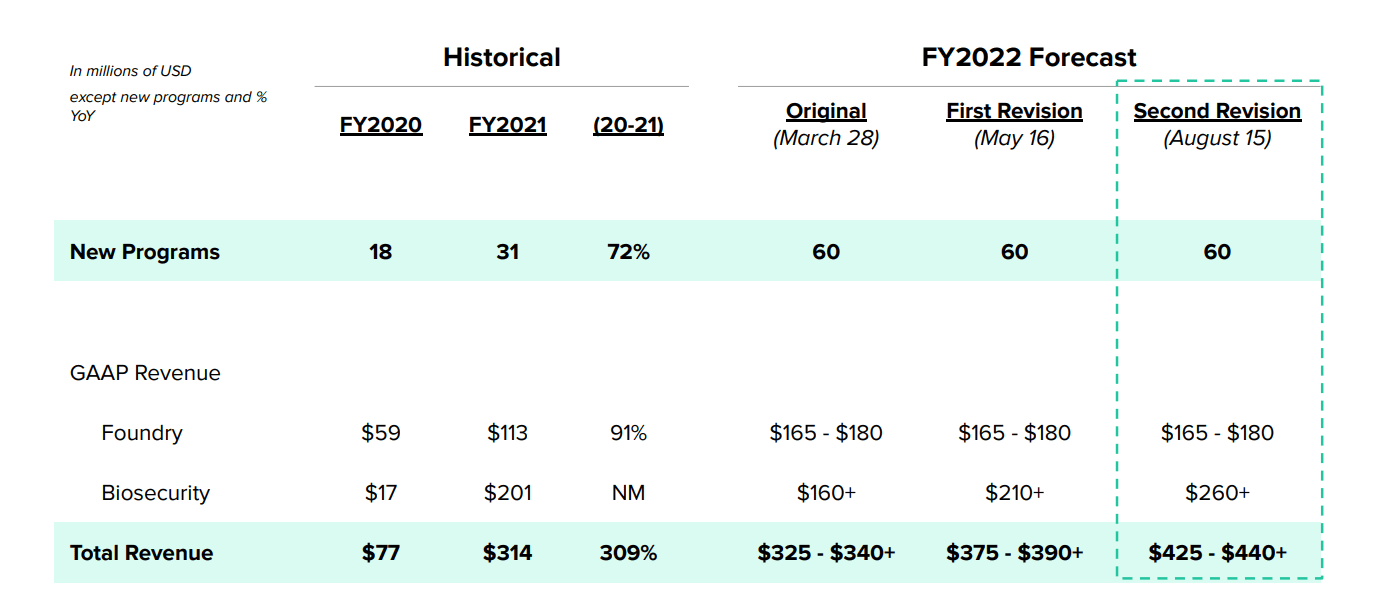

For the second quarter of 2022, the company reported cash and equivalents of $1.4 billion. Q2 total revenue rose 231% to $145M, while Foundry revenue rose 105% to $44M. Biosecurity revenue totaled $100M with 36% gross profit margin. Q2 loss from operations, however, was a whopping $607M and adjusted EBITDA improved to $(23) million.

Encouragingly, the company expects to add 60 new Cell programs to the Foundry platform this year and provided an upward revision for total revenue (increasing from $375M-$390M to $425M-$440M). Uncertainty inherent in the Biosecurity division should be noted, but they still expect strong performance with 2022 revenue of at least $260M (Foundry revenue to come in the range of $165M to $180M).

{kind=link}

Figure 3: Full year 2022 outlook has been increased (Source: corporate presentation )

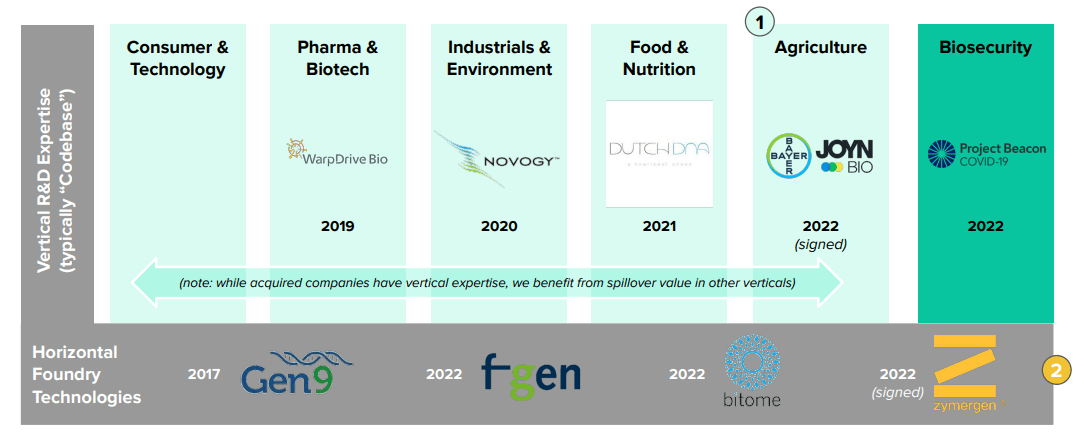

On the conference call , management highlights the planned acquisitions of Zymergen and the ag biologicals assets from Bayer. They hope to be able to minimize incremental recurring expenses, also to grow revenue at Bayer and other potential customers. Zymergen will help them improve the platform, increase efficiency & probability of success which in turn gives better unit economics and net present value per program. The virtuous cycle of value creation I described above is mentioned, essentially positive feedback from new programs driving further customer growth.

{kind=link}

Figure 4: Gingko's history of technology acquisitions to build horizontal & vertical capabilities (Source: corporate presentation )

While scale is important, they've needed to adjust the risk-sharing aspect of partnerships and collaborations in the currently difficult environment. sometimes, they choose to prioritize upfront fees rather than downstream value share (giving up some long-term upside to generate more cash and margin in the near term). On the other hand, especially for cash-strapped customers it can make sense to allow for a lean upfront payment and focus on downstream economics (especially those with higher probability of success). One clear negative of the current model of operation that I don't like is timing of realizing those downstream economics, such as milestones and royalties. Customers have to bring products to market in order for those to be realized and it makes it near impossible for myself (as well as many analysts on Wall Street) to model their revenues with any degree of accuracy.

One red flag for me here is their accumulated deficit, which I know one could argue is necessary to build a wide moat business with economies of scale. Still, accumulate deficit of $2.297 billion (with no end or minimization of cash burn in site) is both impressive and clearly stands out (in a negative light).

As for key holders of the stock, CEO and Co-Founder Jason Kelly owns 82 million shares or 5.8% of the company (nice to see some skin in the game). Co-Founder Reshma Shetty owns a whopping 11% stake. The fund Viking Global Investors owns a 9.7% stake and UK-based Baillie Gifford owns a 15.5% stake.

As for executive compensation, while cash component of the salary seems reasonable for a company this size, stock awards are clearly excessive to a degree that I CANNOT ignore (CEO Jason Kelly with $380M of stock awards where there has been little in the way of value creation to warrant such a gift). The important thing is to avoid companies where the management team is clearly in it for self-enrichment instead of creating value for shareholders, and looking at compensation is one of several indicators in that regard.

{kind=link}

Figure 5: Executive compensation summary table (Source: proxy filing )

As for useful DD nuggets from ROTY Chat, Grimthorn notes that he owns the stock in both his ROTH and regular investment accounts. He references this helpful article , which is worth a read.

Manzil likewise chimes in and notes the following:

DNA has a nice technology platform and strong balance sheet. Most of their cash revenue seems to come from their Covid testing business ("biosecurity") which I see as having minimal direct relationship to their core Foundry business. Perhaps it could be lucrative, though, if new global virus threats become the norm. As for Foundry, I wish they'd break out cash vs equity-based revenue. My assumption is most, if not all, Foundry revenue is equity based, which would be subject to future mark-to-market adjustments--which also seems to suffer from a degree of opaqueness. To me, DNA is a bet on the value of downstream royalties/equity earned from providing outsourced cell programming . I find it to be a very interesting business but at a $6B+ MC for an unproven business model--it's a little outside my risk appetite.

As for playing devil's advocate, this Twitter thread from Fallacy Alarm on Q2 earnings ("the emperor has no clothes") is quite helpful. Alarm notes that 80% of 1H 22 were Covid testing revenues with Foundry revenue of just $55M. He highlights a fact that I view as true, namely that non-cash revenue with clients Gingko partially owns and little commercial feedback cannot be viewed the same way as cash revenues. Losses obviously do not cover Foundry revenue and the company is continuously booking losses investments ($38M I believe in Q2). The other side of the coin again is that these downstream economics require investors to take a VERY long-term view, and perhaps that is quite difficult with an unproven management team (at least in terms of running a public company).

As for other useful nuggets from the 10-K filing (you should always scan these in your due diligence as many companies like to sweep undesirable elements under the rug), I'm reminded that I'm not a fan of the capital structure either (multi-class stock structure entitles employees to hold Gingko Class B stock which has greater votes per share than Class A, also issuance of Class C common stock could increase the concentration of voting power in Class B which in turn could discourage potential acquisitions of business and adversely affect trading price). Again, it's rather confusing and I'm a fan of the simple.

Final Thoughts

To conclude, on the pro side I would not be surprised to see share price head back up above $5 or so near term as sentiment improves after the Q2 "beat and raise". While this positive event was driven by Covid testing in schools, it seems that the company could beat its 2022 Foundry guidance as well (which in turn is diversified into other areas such as vaccines, antibiotics and cell therapies). Management is projecting addition of a target of 60 new programs for the year, and should this be met or exceeded rerating of the valuation higher could be merited.

However, I still think the novel business model here (focused on downstream economics) is too unproven to support a higher valuation. Competitive landscape is quite difficult, though management has wisely adopted a "picks and shovels" approach versus single product risk.

The downside of a bet here for investors is that it will take a LONG time (if ever) for Gingko to get to the point where royalties (milestones and equity stakes sold) get the company to cash flow positive (or even meaningfully minimizing burn rate). A key challenge for them near term is to optimize foundry fees for the admittedly difficult market environment, and long term again get to the point where downstream value of royalties meaningfully impacts their bottom line.

For readers who are interested in the story and have done their due diligence, I still CANNOT recommend the stock in good conscience as I need to follow it for a few more quarters to gain a better sense of management execution and understanding the strength & scale of the underlying business model.

Key risks include additional dilution in the near to medium term, wise management of the balance sheet in light of ongoing operating losses, overpaying for acquisitions and then successfully leveraging inherent synergies and especially competition they face from customers' internal R&D departments as well as other research solution providers. Additionally, competing platforms may emerge from various sources, including from joint ventures and partnerships between well-capitalized technology and life sciences companies.

Author's Note: I greatly appreciate you taking the time to read my work and hope you found it useful. Lastly, be aware that most of my articles appear first to members of the ROTY community.

For further details see:

Gingko Bioworks: Near-Term Challenges Trump Downstream Economics