GVDBF - Givaudan: European Quality Compounder Is Fairly Valued

2023-10-27 13:59:36 ET

Summary

- Givaudan is a global leader in fragrance & beauty and taste & wellbeing products with a high-quality business model.

- The company has a wide moat, strong customer retention rates, and a track record of impressive growth and shareholder returns.

- Givaudan's recent performance was slightly below expectations, but its profitability remained intact. At 28x forward EPS, we think the valuation is hefty and issue a hold rating on the stock.

We present our note on Givaudan ( GVDBF ) ( GVDNY ), a global leader in fragrance & beauty and taste & wellbeing with a Hold rating. We appreciate Givaudan’s high-quality business model underpinned by R&D and innovation, and the business’ highly cash-generative nature. However, we are concerned about the current environment, do not see an attractive risk/reward, and are neutral on the stock at this price. We will provide a brief overview of the company, analyze key drivers, value the shares, and describe the main risks.

Introduction to Givaudan

Givaudan is a leading Swiss multinational that manufactures and markets fragrance & beauty and taste & wellbeing products (including compounds, ingredients, and integrated solutions) from both natural and synthetic ingredients. The products are sold to manufacturers of food, beverages, perfumes, and other consumer goods.

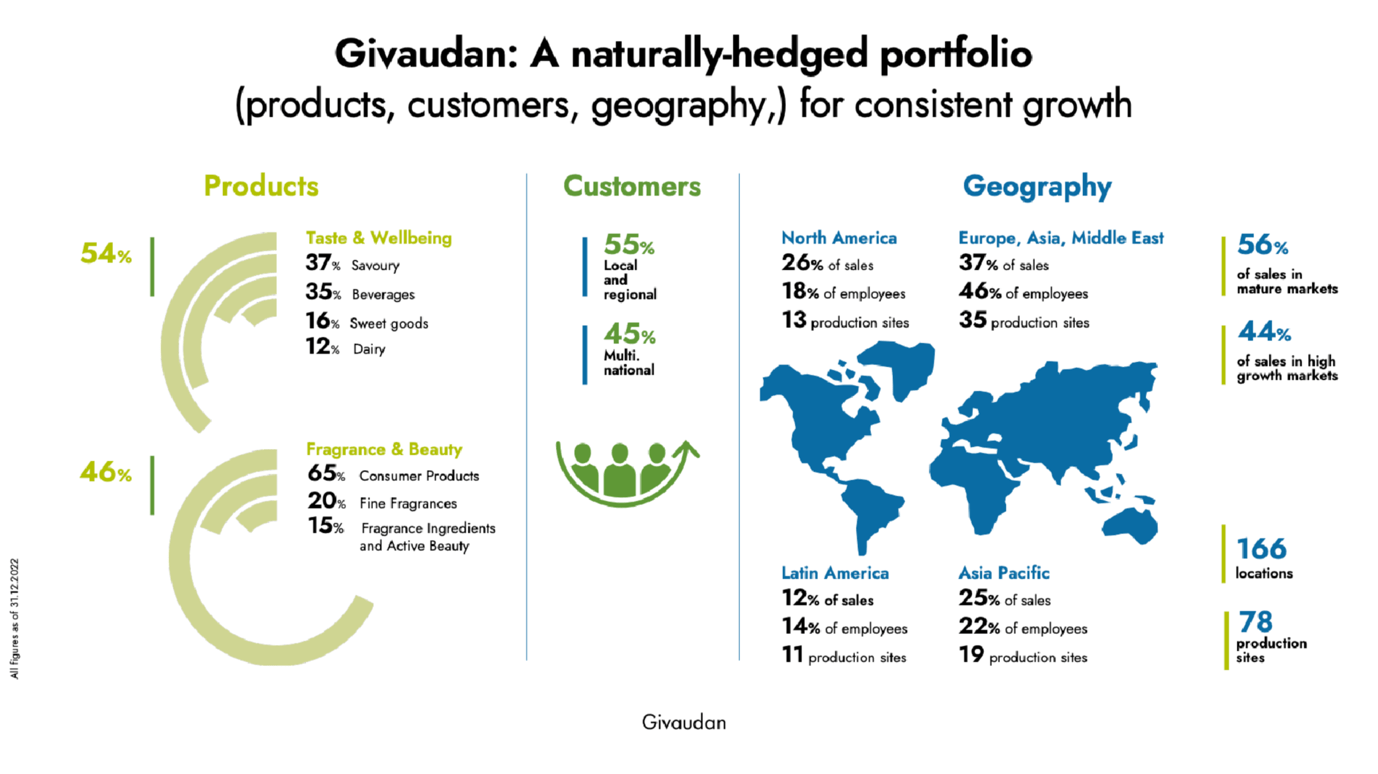

Givaudan is present in more than 160 locations with 78 productions across EMEA, North America, Latin America, and Asia Pacific. Givaudan is listed on the SIX Swiss Stock Exchange and has a current market capitalization of CHF26 billion.

{kind=link}

A high-quality business model with a wide moat

Givaudan has a high-quality business model and a track record of impressive growth and shareholder returns. The company has massively outperformed indices and returned in excess of CHF30 billion to shareholders since its IPO. Givaudan has a significant moat due to know-how, R&D, complexity, and regulation. The company produces mission-critical goods with high impact and low cost (from 0.5% to 6%). Its products are an important factor in customer decisions on whether to repurchase or not, and thus are key to client success. Products are largely co-creations with customers and are highly differentiated, resulting in high switching costs, and high customer retention rates, and a predictable stream of cash flows. Competition is not destructive and is driven by quality rather than price. R&D plays a crucial role in Givaudan’s success, with a research-driven innovation approach. Givaudan has more than 4000 active patents and dedicates in excess of CHF500m or ~7% of yearly sales to R&D.

The client base is highly diversified across geographies and categories and offers exposure to emerging market growth and urbanization themes. In addition, Givaudan is exposed to other supportive megatrends including increasing longevity, sustainability, self-care, etc. Givaudan has a successful history of growth through M&A, with CHF4 billion invested in 19 acquisitions between 2014 and 2021. The high quality of the business is reflected in excellent sector-leading profitability, high returns on capital, high cash generation, and capital returns (e.g., an average annual dividend yield at ~10.5% or more than 2x the SIX average).

Recent performance

Givaudan reported Q2 results slightly below consensus expectations, with a decline in Taste & Wellbeing, particularly in the North America region. This was the lowest organic growth in the last six years and led to concerns among investors. However, quarters can be somewhat volatile for Givaudan, and comps were tough, and we are not concerned about midterm targets that were maintained. Meanwhile, profitability was intact despite volume issues, with EBITDA coming in a few percentage points above the consensus.

Strategy 2025, valuation, and investment recommendation

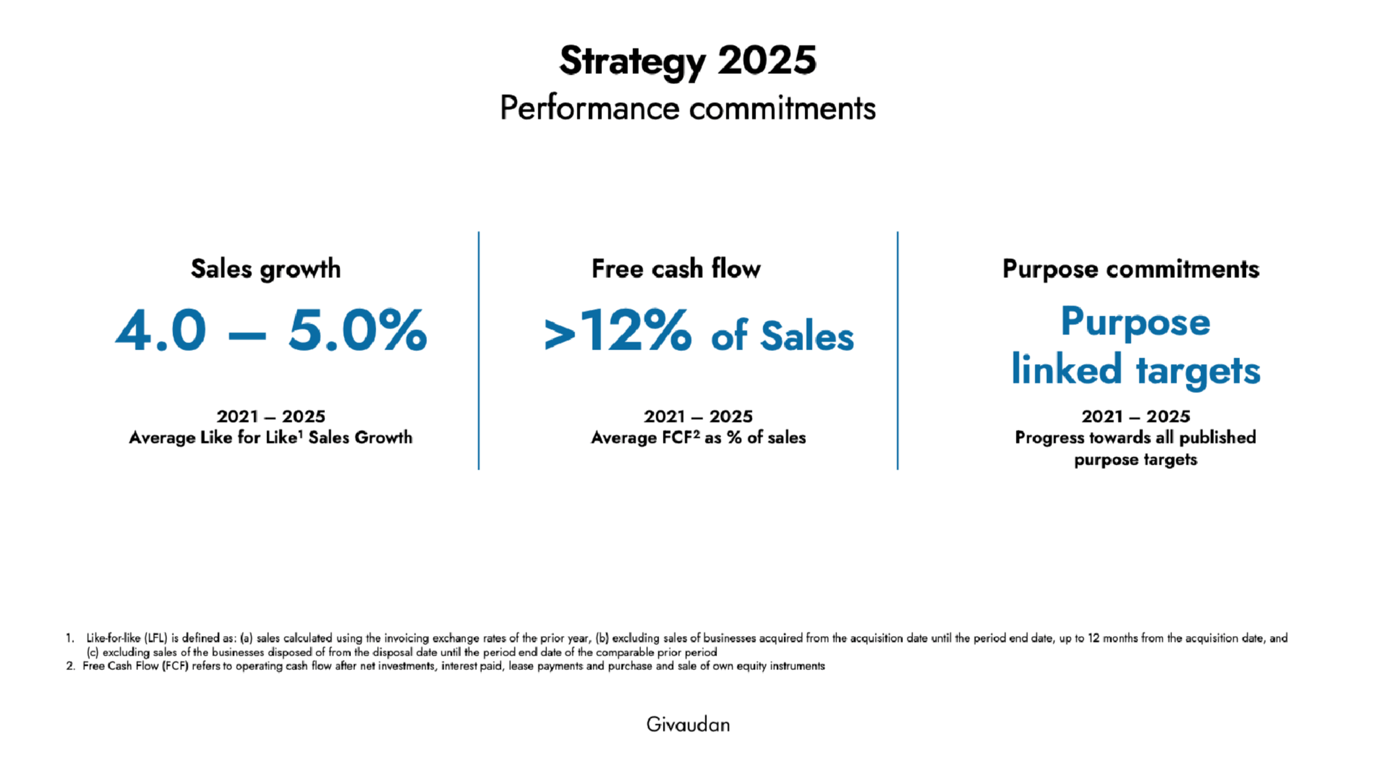

We value Givaudan using PE multiples given the sector and capital structure. Sector multiples have been relatively high in the last few years and reflect the underlying organic sales growth, high and sustainable margins, and rerating of defensive quality stocks. Our estimates are largely in line with sell-side analyst consensus expectations. We assume 4% top-line growth (lower end of Strategy 2025 ’s target of 4-5% like-for-like growth) in FY2024 and estimate net sales of CHF7.2 billion. We expect an EBIT of ~CHF1.3 billion, with 120 basis points of operating margin improvement from mix. We then forecast a net income of CHF970 million and an EPS of CHF105, implying a forward PE ratio of 28x. Moreover, our FCF estimate is CHF1.02 billion, i.e. 14% of sales vs. the stated target of more than 12%. We then forecast mid-single-digit EPS growth in the mid-term driven mostly by organic sales growth and a few basis points of operating margin improvement. We note the current and forward PE multiple is in line or in the upper end of the last 5 and 10 years (on a normalized basis, excluding one-offs like 2020). We think the valuation is hefty, and we would value Givaudan at a 25x exit multiple in 2025 post the execution of the plan. At an EPS of CHF115 in FY2025, this means a share price of CHF2875, or ~1% lower than today. Even more optimistic, exit multiples of one to three turns higher of EPS would give a limited upside of at most 10%. Combined with an average 2.5% dividend yield, the returns from here do not look compelling, and we issue a Hold rating on the stock. Only a significant outperformance vs. consensus could change that.

{kind=link}

Risks

Downside risks include but are not limited to a deterioration of macroeconomic conditions resulting in lower sales growth, competition from new technologies, an increase of raw materials prices resulting in lower margins, supply chain issues, higher interest rates impacting quality defensive stock valuations, value destructive M&A, and misallocation of capital.

Conclusion

While we appreciate Givaudan’s quality business model, we have a neutral rating on the equity at the moment given the risk/reward. Givaudan remains in our European quality compounders list, and we will keep a close eye on the company and revisit the investment case if there are any major changes.

For further details see:

Givaudan: European Quality Compounder Is Fairly Valued