ASHTF - Giverny Capital Asset Management Q3 2023 Letter

2023-11-02 11:35:00 ET

Summary

- Giverny Capital Asset Management, LLC is a partnership between Giverny Capital of Montreal and David Poppe, the former president and chief executive officer of Ruane, Cunniff & Goldfarb, LLC.

- Giverny Capital Asset Management's model portfolio performed well in the third quarter, driven by the strong performance of tech giants Alphabet and Meta Platforms.

- The portfolio's other stocks also outperformed the broader market, with an average return of 6.1%.

- The firm made some adjustments to its portfolio, selling positions in Ciena and SS&C, and adding to positions in Charles Schwab and Ashtead Group, as well as establishing new positions in Fiserv and Ferguson Plc.

To Our Clients & Friends:

This letter is arriving a bit later than usual, but many of our clients got to hear from us at our investor meeting on October 6 th in New York. Francois Rochon and I enjoyed being with you, whether in person or online, and taking your questions about the portfolio. As a reminder, I also expect to take part in the spring 2024 investor meeting held by my partners at Giverny Capital Inc. in Montreal. This gives clients two opportunities each year to hear us present our ideas and ask us questions.

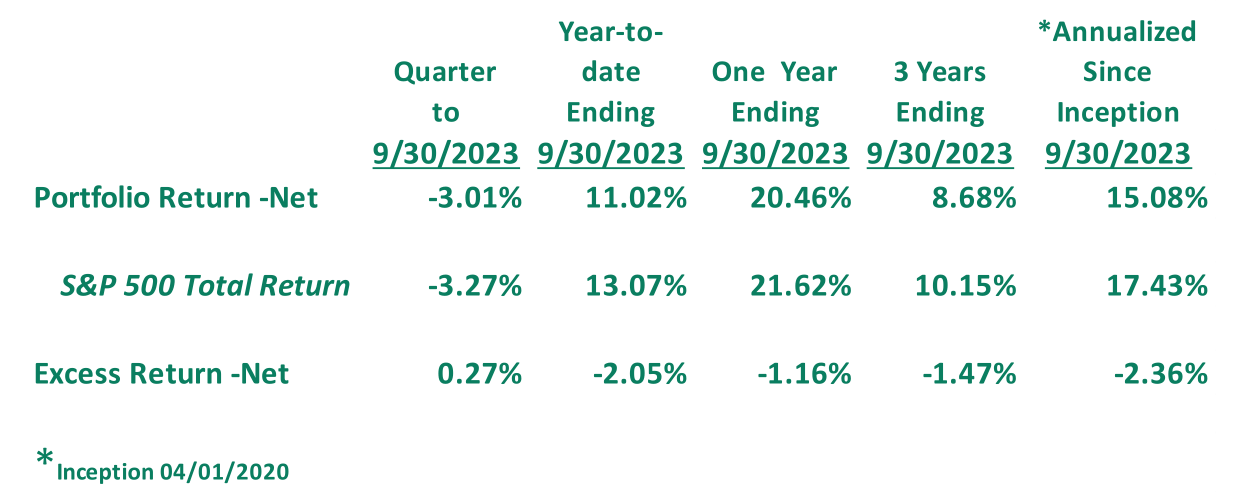

For the third quarter ended September 30, 2023, the Giverny Capital Asset Management model portfolio, which is a Poppe family account [1] , performed as follows [2] :

{kind=link}

As we discussed at our meeting (and in our second quarter letter), the S&P 500 ( SP500 , SPX ) performance this year has been driven by seven giant tech stocks. In fact, those seven constituted 27% of the S&P 500 as of September 30. They rose by 55% on a weighted basis during the first nine months of the year and accounted for 84% of the S&P Index’s total return. The other 493 stocks in the Index rose, on average, about 2.8% for the year to date.

In our portfolio, tech giants Alphabet and Meta Platforms rose 75% through September (again on a weighted basis) and constituted 14.6% of the portfolio at quarter-end. Their performance drove 59% of our total return.

Our other 23 stocks rose on average by 6.1%, well ahead of the “other 493” of the Index. A little visualization might help. The blue sections below represent the return generated by tech giants for us and for the Index. The green represents the return generated by the rest of the portfolios.

Put simply, I feel fine about how we’re doing. The tech giants are outstanding companies, but they also sport enormous market valuations and trade for demanding price-to-earnings multiples. Lipper Analytical reports that the seven tech giants constituted 29.9% of the Index by valuation in mid-October but will contribute 15.6% of its earnings this year, resulting in a forward PE of 27.6x. The rest of the Index trades at about 17x earnings. Maybe that premium will be sustainable as the giants possess strong competitive positions. But I prefer our exposure to smaller businesses with less demanding valuations and room to grow. We have more than 30% of our portfolio invested in companies with market capitalizations below $22 billion. For the S&P 500, that number is 7%. I like our exposure to midcaps – companies like Installed Building Products ( IBP ), Ashtead Group ( ASHTF ), Five Below ( FIVE ), Floor & Décor ( FND ) and CarMax – that should have years of growth ahead.

We had a few transactions during the quarter. We exited our small position in Ciena ( CIEN ) at a loss. Ciena is a technology leader in network communications infrastructure. It’s largest competitor, the Chinese company Huawei, has been banned from many Western nations for fears that it cooperates with the Chinese government in spying on customers. We bought Ciena with an expectation that its future looked bright given healthy demand from both telecom and cloud computing customers, plus a less competitive bidding environment.

Unfortunately, we were disappointed with Ciena’s difficulties managing its supply chain, inventory level and backlog. We opted to sell the stock in the belief we could find better opportunities elsewhere.

We exited a larger position in SS&C ( SSNC ) during the quarter. We’re fans of this business and its founder and CEO Bill Stone, but SS&C financed a large acquisition in 2018 by issuing debt at floating interest rates. As rates climbed over the past two years, SS&C’s interest payments on its debt have risen from about $202 million in 2021 to an estimated $460 million this year. This heavier burden of debt service is devouring modest underlying profit growth. SS&C will report lower earnings per share in 2023 than it did in 2021 entirely because of the burden of interest payments.

Bill Stone owns more than 30 million shares of SS&C; no one has a stronger interest in making prudent financial decisions than Bill. We could revisit SS&C at some point if it made significant progress in reducing its floating rate debt. But with the debt burden currently high, the cost to service the debt rising, and the business growing slowly, it feels like SS&C made a capital allocation error that will take time to unwind.

We modestly trimmed Arista Networks as it reached an 8% weight in our portfolio. As I write this, Arista is up about 60% for the year, and it continued rising after our trims. Arista remains our second largest holding, ending the quarter at 7.1% of the portfolio.

With the proceeds of these sales, we added to our positions in Charles Schwab and Ashtead Group, and established new positions in Fiserv and Ferguson Plc.

I have written about Schwab in prior letters, but at the risk of being repetitive I believe it offers a strong value proposition both to individual investors and professional investment advisors who run their businesses on the Schwab platform. It has chosen to reduce the fees it charges for trading and other services to win investor trust and fuel growth. Consequently, it may be overly dependent on its practice of sweeping customer cash balances into its bank, where it reinvests those deposits into safe fixed income securities and pockets the interest. As interest rates have risen over the past 18 months, many Schwab customers are leaving less idle cash in their accounts and putting more of their funds into US Treasuries or money market funds. This leaves Schwab with lower earnings.

Importantly, Schwab continues to add hundreds of thousands of new accounts every month. The issue of customers leaving less cash in their accounts has leveled off recently, meaning Schwab should begin growing again as it keeps adding accounts. Even if so-called cash sorting never levels out, Schwab has significant pricing power it could tap while remaining a low-cost provider for customers, including charging more for some trades, margin loans or wealth management services, or perhaps charging modest custodian fees to investment advisors, a common industry practice. It has tools in the toolbox to offset a long-term loss of interest income, even if it prefers not to use them. The combination of steady account growth and pricing power tell me Schwab’s earnings won’t be permanently impaired.

Ashtead Group operates the second-largest US equipment rental business, Sunbelt Rentals. The market seems concerned that a slowdown in commercial construction will hurt Sunbelt, but I believe federal infrastructure projects, new semiconductor plants and warehouse and factory construction combine to create a healthy market. Ashtead has a terrific management team and a number of advantages of scale. We felt comfortable adding shares at about 15x earnings.

Turning to our new positions, we have been following Fiserv ( FI ) for a couple of years now and finally bought a position during the third quarter. Fiserv has two businesses that reinforce each other: it is a key technology provider to several thousand global banks and credit unions. Mid-sized financial institutions need to offer a full complement of digital banking services to compete with larger national banks, but they can’t afford to build out an internal tech capacity. It’s more cost effective to outsource to Fiserv.

Fiserv’s other business is, broadly, payment processing: when you tap and pay at your favorite restaurant or retailer, you may be using a Fiserv device. That device, in turn, may connect directly to the business owner’s bank – and Fiserv built out the bank’s tech stack. The synergy here is important. Fiserv can sell terminals to the restaurant itself, but banks may also sell Fiserv products as part of their customer relationships. There is terrific distribution synergy.

For the next few years, Fiserv’s growth should be led by Clover, a payments acceptance system that offers merchants faster transaction times, better fraud protection and stronger operational controls than many existing acceptance networks. While Clover is a clear leader in acceptance, it has a small market share today and could grow at double digit rates for some years. In turn, that should drive solid earnings growth for Fiserv. I believe the stock trades for a low-teens multiple of likely 2024 earnings, an attractive price for a steady compounder.

Ferguson ( FERG ) is the nation’s leading distributor of plumbing supplies and is growing in the related field of HVAC (heating, ventilation and air conditioning). It’s a good business: pipes, valves, boilers, water pumps and the like are mostly unbranded products. There are a lot of manufacturers with limited pricing power. On the other side, plumbing and HVAC contractors are mostly small businesses without a lot of negotiating clout. The distributor sits in the middle with more buying power than the manufacturers and more pricing power than the plumber. It’s a competitive industry, not a monopoly, but Ferguson is #1 in most of its categories. With its size, it offers good service and a deep inventory position to contractors.

Earnings have compounded steadily over time, but likely will be flat in the coming year, partly because residential home construction is off. We bought the stock for about 15 times 2024 earnings and feel like that’s a good value given Ferguson’s financial strength and long-term outlook.

Finally, I’m delighted to report to you that we have hired an analyst to work with me in New York. John Bleday is a 2022 MBA graduate of the Columbia Business School’s value investing program whom I met about two years ago. John interned for GCAM in the spring of 2022 and, after a short stint at a hedge fund, he and I started talking about him working here. Prior to business school, John earned his CPA license and worked for several years in venture capital. He’s a graduate of Dartmouth College, where he ran on the track team and was Ivy League champion at 3,000 meters.

I believe John will help us uncover and research more potential investment ideas. When he worked with me in 2022, I was impressed with both his idea generation and research process. This investment in the business reflects our growth and my belief that, along with our partners in Montreal, we have a lot of good investment ideas worth research time.

With every good wish,

David M. Poppe

Top 10 holdings as of September 30, 2023

| 9.1% |

| Arista Networks ( ANET ) |

| 7.1% |

| Constellation Software ( CNSWF ) |

| 7.1% |

| Progressive Corp. ( PGR ) |

| 7.1% |

| META Platforms |

| 5.6% |

| Heico Class A ( HEI ) |

| 5.0% |

| CarMax ( KMX ) |

| 4.8% |

| Charles Schwab ( SCHW ) |

| 4.8% |

| 4.6% |

| Ametek ( AME ) |

| 4.1% |

| Total |

| 59.3% |

Footnotes[1] The family account does not pay a management fee. The returns presented herein assume the deduction of an annual management fee of 1% to show what a client account’s performance would have been if it had been invested the same as the family account during the period. Past performance is not necessarily indicative of future results. [2] The S&P 500 Index returns include the reinvestment of dividends and other earnings. The Index is an unmanaged, capitalization-weighted Index of common stocks of 500 major US corporations. The Index does not incur expenses and is not available for investment.

|

Editor's Note: The summary bullets for this article were chosen by Seeking Alpha editors.

For further details see:

Giverny Capital Asset Management Q3 2023 Letter