PGJ - Global Asset Allocation Viewpoints Q1 2023: Half Agony Half Hope

Summary

- Strains are building, and the U.S. will likely enter recession in the second half of 2023. By then, Europe will likely be emerging from recession, while China and Emerging Asia may be enjoying a COVID-reopening-inspired recovery.

- Segments of the inflation basket will soften rapidly, but tight labor markets and strong wage pressures imply that core segments of inflation will remain uncomfortably elevated, resulting in an incomplete disinflation process.

- The struggling macro backdrop signals a meaningful fall in earnings that is unaccounted for by markets - a headwind that will, inevitably, further extend the equity market drawdown.

- Central banks are likely nearing the completion of their tightening cycle, implying that bonds will be able to support portfolios both as recession approaches and during forthcoming periods of volatility and risk.

Key themes for 1Q 2023

- The global economy has avoided recession so far, but now must confront severe challenges. Strains are building, and the U.S. will likely enter recession in the second half of 2023. By then, Europe will likely be emerging from recession, while China and Emerging Asia may be enjoying a COVID-reopening-inspired recovery.

- Inflation is slowing only gradually and will remain above target in 2023, despite recession. Segments of the inflation basket will soften rapidly, but tight labor markets and strong wage pressures imply that core segments of inflation will remain uncomfortably elevated, resulting in an incomplete disinflation process.

- Central banks will hike further this year and will not provide any relief. Major central banks have now decelerated their tightening, but this isn’t a precursor to a less-hawkish stance. The stubborn inflation story means that policy rates are rising further and will not be cut, even as recession takes hold.

- First rate hikes, now earnings weakness: Equity markets face further challenges this year. The struggling macro backdrop signals a meaningful fall in earnings that is unaccounted for by markets - a headwind that will, inevitably, further extend the equity market drawdown.

- Fixed income, once again, can offer stability and income in a challenging economic backdrop. Central banks are likely nearing the completion of their tightening cycle, implying that bonds will be able to support portfolios both as recession approaches and during forthcoming periods of volatility and risk.

- The stubborn inflation picture implies that real assets outperformance is not yet exhausted. Their diversification benefits and defensive characteristics in this macro environment are particularly valuable, as the stubbornly high inflation backdrop should extend outperformance in commodities and infrastructure.

Investment Themes

From inflation concerns to growth concerns

Now that inflation is on a decelerating path, 2023 may not see a repeat of the frantic Federal Reserve (Fed) activity that characterized 2022. Yet, the slow and sticky nature of the inflation decline implies that policy rates almost certainly still have further to rise.

While it may not be evident yet, the most aggressive monetary tightening cycle since the 1980s will leave a visible imprint on the U.S. economy, with recession taking shape in the second half of 2023. Unfortunately, as history warns against prematurely calling victory over inflation, relief from the Fed will not be forthcoming. After reaching a peak rate of 5.25-5.5% in the first half of the year, Fed policy will have to remain restrictive throughout 2023 - even as the U.S. economy falls into recession. Against this backdrop, broad equities will likely remain challenged.

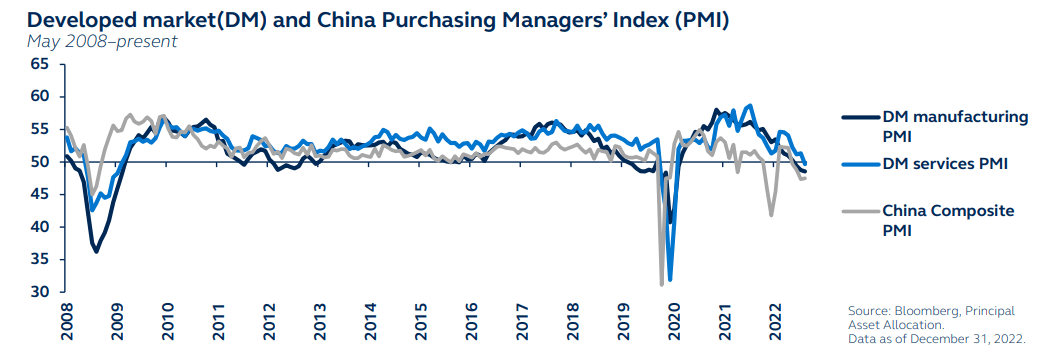

China: Unleashing the dragon

After two years of economic weakness, recent steps to ease China’s zero-COVID policy are filling investors with optimism.

A full reopening will not happen overnight. Yet, a roadmap for an end to China’s stringent COVID-19 measures should eventually provide the catalyst for a rebound in Chinese economic activity. The sustainability of the rebound and its potential positive impact on China’s major trading partners across Europe and Asia, however, will likely depend on Chinese policymakers’ resolve to add effective stimulus measures.

For much of 2023, U.S. economic challenges will likely inhibit significant risk taking. In such an environment, emerging market risk assets usually struggle. But if China is able to reopen smoothly and stimulate the economy, emerging markets should prove resilient against the headwinds.

Diversification is back in vogue

Unlike 2022, where stocks and bonds fell together, opportunities will likely be more forthcoming in 2023. While persistently restrictive monetary policy and the likely resulting U.S. recession will weigh on the broad equity market outlook, the relatively attractive valuations outside the U.S. suggest investors stand to gain through global diversification.

Fixed income’s diversification potential has also been restored. With many central banks nearing the completion of their tightening cycles, bonds may be able to support portfolios, providing income and more stability during periods of volatility and risk. Importantly, credit now offers more attractive yields than in recent years, meriting portfolio allocation.

Finally, with price pressures easing very slowly, inflation mitigation via real assets remains a key part of the playbook.

Consider the potential risks

Entrenched inflation: While the market appears to agree that inflation will fade this year, history suggests that there is a risk that meaningful inflation decline may not materialize. In such an event, after a short pause, the Fed and other central banks may need to resume policy hikes. Not only would that deliver additional headwinds to growth, but the negative shock to investor sentiment could set markets on a path to a deeper, more prolonged downturn.

Financial instability: The drastic rise in rates risks severe liquidity disruption. Violent, sudden price moves in one market can provoke a vicious loop of margin calls and forced sales of other assets, with unpredictable results. Markets have so far navigated the rate increases with minimal disruption, but there is no guarantee that 2023 will be as straightforward.

An unavoidable economic downturn

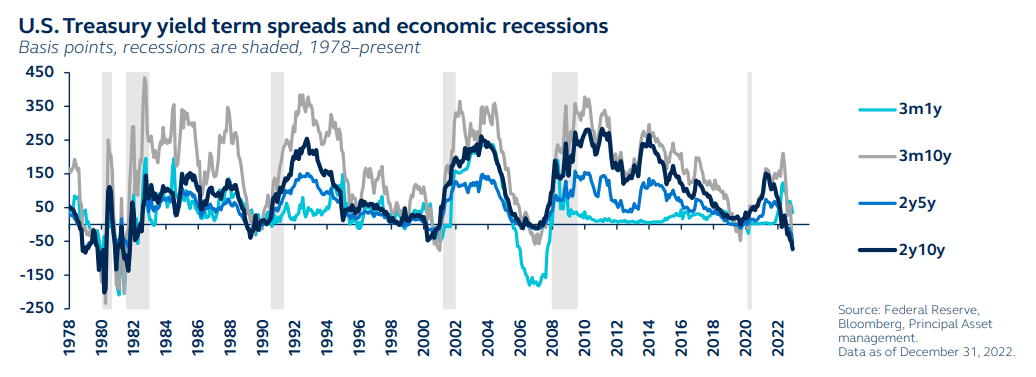

Despite the multiple headwinds that confronted the globe in 2022, most economies have so far avoided recession. Europe felt the economic brunt of the Russia/Ukraine conflict, yet growth has likely only just slid into contraction territory in 4Q. In the U.S., while manufacturing surveys have already fallen into recessionary territory, services sector activity remains more firm and the Atlanta Fed’s GDPNow tracker estimates GDP growth of around 4% in 4Q22.

Yet, it’s unlikely that the U.S. will evade recession in 2023. Strains are clearly building for consumers and corporates, while the Treasury yield curve has inverted - a historically reliable recession indicator. Not only is the 2s10s curve inversion material and sustained, but other segments of the yield curve are also inverted, including the 3-month 10-year curve which is typically consistent with recession risk within a 12-month period.

By contrast, China faces a more constructive outlook. The recent easing of COVID restrictions has been chaotic, but it should eventually unleash pent-up consumer demand, improving confidence and investment. If policymakers combine reopening with effective stimulus measures, there will likely be positive impacts for emerging Asia.

Although U.S. growth has been remarkably resilient so far, recession will likely hit in the second half of 2023, while Europe is likely already in recession. Once the COVID dust settles, China may face a more constructive outlook.

{kind=link}

{kind=link}

Consumer and labor market resilience is unsustainable

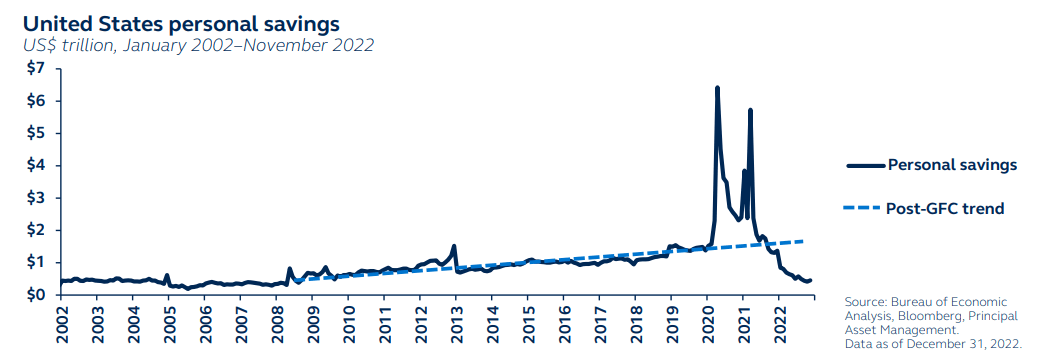

Despite U.S. consumer spending remaining strong, personal savings are dwindling and are well below the post-Global Financial Crisis ((GFC)) trend, resulting in consumers tapping into credit. New York Fed data shows that credit card balances saw a 15% year-over-year increase in 3Q 2022 - the largest rise in more than 20 years. These strains will ultimately weigh on consumer spending.

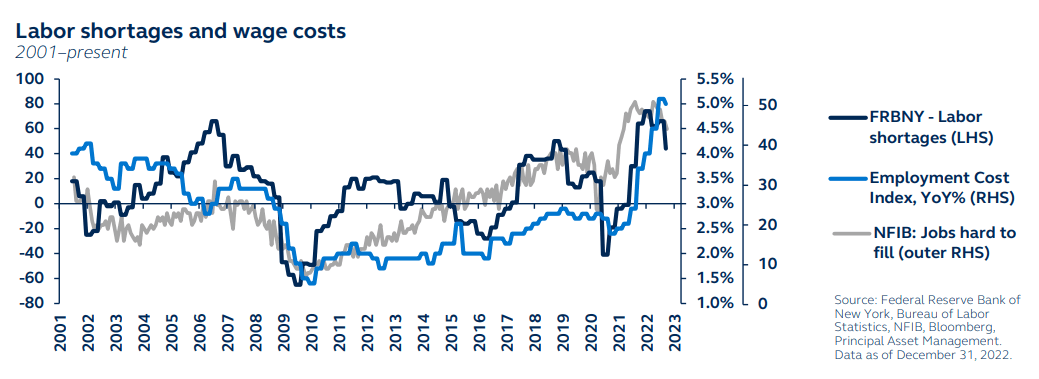

The labor market has cooled slightly but remains historically strong. Unemployment, at 3.5% as of December’s reading, remains very close to record lows and monthly payrolls are hovering around 275,000 - a level consistent with very strong labor demand. But as a labor supply shortfall has opened up since the pandemic, there is now a clear imbalance between labor demand and supply. In fact, there are around 4 million more job openings than there are unemployed workers, and employers continue to report considerable difficulty in filling available positions.

This imbalance is synonymous with wage pressures. The employment cost index, the Fed’s preferred measure of wages, is at a series high and is entirely inconsistent with the 2% inflation target. As such, the Fed needs to drive a moderation in labor demand to soften wage pressures.

The labor market remains historically strong, but this is contributing to inflation concerns. The Fed will need to weaken labor demand in order to relieve wage pressures.

{kind=link}

{kind=link}

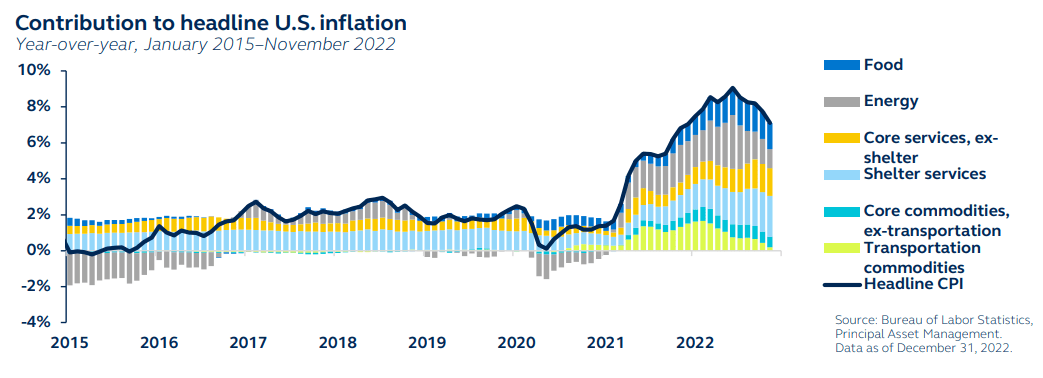

An incomplete disinflationary trend

Investor questions have shifted from whether inflation has peaked to where it will settle. The broad contour of recent declines suggests inflation will fall short of global central bank targets, continuing to trigger angst in policymakers. Indeed, the Fed expects PCE inflation to only fall to 3.1% by the end of 2023, the Bank of England ((BOE)) forecasts inflation at 5.2%, and the European Central Bank (ECB) is projecting 6.3% - all uncomfortably above their 2% targets.

In the U.S., there are segments of the inflation basket that will soften rapidly. Food and energy prices, for example, have fallen sharply, while the supply chain recovery is finally yielding relief for core commodities inflation.

For services, however, disinflation will be a slow process. Shelter services inflation typically responds to the slowing housing market with a long lag - but should start to decelerate in the coming months. Core services inflation accounts for 57% of the CPI basket and is the most important category for understanding the future path for inflation. As wages make up the largest cost in delivering these services, loosening in the labor market is required to push inflation toward 2%. Unfortunately, the resulting rise in job losses will almost inevitably lead to recession.

Although inflation is declining, the tight jobs market implies progress will be slow. Recession risk is high because it is a necessary condition for price stability.

{kind=link}

{kind=link}

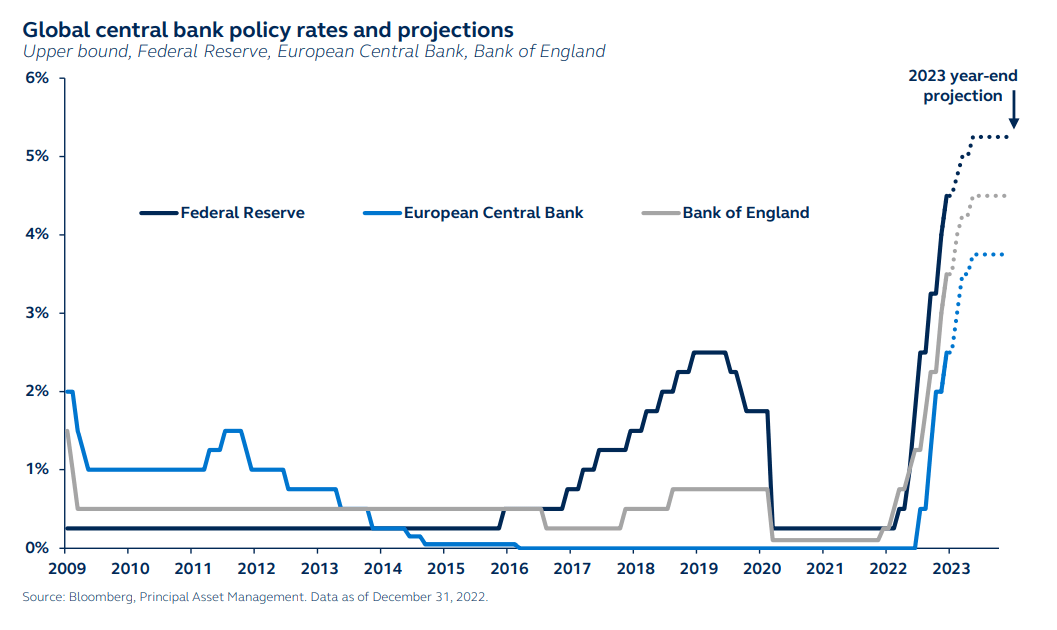

Monetary tightening: Slower, but higher, for longer

2022 experienced one of the most aggressive global tightening episodes in history, with the vast majority of global central banks hiking rates.

Today, most major central banks have decelerated their blistering pace of tightening. However, this isn’t a precursor to a less-hawkish stance. With inflation expected to remain stubbornly above target, central banks have pledged to take rates even further into restrictive territory in 2023.

What’s more, rate cuts in most developed markets are unlikely next year - despite elevated recession risk. Not only does history warn against prematurely calling victory over inflation, but recession is a necessary step in the path towards price stability for many economies. For the Fed, this implies policy rates rising above 5% in early 2023, and remaining there throughout the year. Market pricing for Fed policy still sees rate cuts in 2023 - setting up an uncomfortable reality check later in the year.

Even the Bank of Japan (BoJ) has made early moves to tighten policy. By effectively raising the cap on yields, the central bank has not only moved away from ultra-loose monetary policy, but it raises the prospect of a rate hike in 2023 - the first such move for Japan since 2007.

Policy rates in most major central banks will move further into restrictive territory in 2023 and will not be cut, even in the face of rising recession risk.

{kind=link}

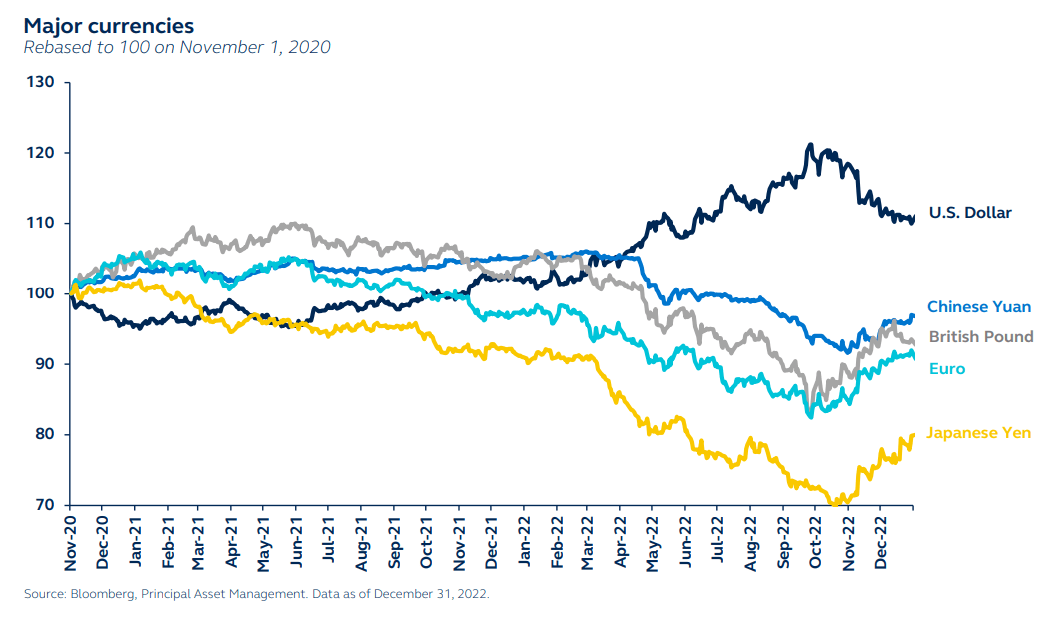

Relief from the U.S. dollar bull run is on its way

Despite its recent sharp pullback, U.S. dollar fundamentals remain supportive near term. With the Fed hiking rates further and remaining the most hawkish of all major central banks, the U.S. dollar may still enjoy near-term strength.

However, after a few more rate increases, a Fed pause should lead to a sustainably weaker U.S. dollar. This dollar-negative development should likely be supplemented by China ending its zero-COVID policy, as well as the end of the BoJ’s yield curve control monetary policy.

Such a precipitous ascent in the dollar often results in a crisis-type scenario - one that did not arise in 2022. Instead, many emerging market economies fared relatively well compared to history, helped by fiscal discipline and precautionary monetary policy. Therefore, once conditions improve, their recoveries could be fairly swift.

In addition, with a weaker dollar, many developed market central banks will have the space to recalibrate from currency defence and fighting inflation via demand destruction to more growth-supportive policies. Overall, U.S. dollar weakening should be an incremental positive for global growth, but is unlikely to develop until later in 2023.

The U.S. dollar may still see near-term strength given the Fed’s more hawkish resolve. Yet, with rates nearing their peak, dollar weakness is waiting in the pipeline.

{kind=link}

Financial conditions set the stage for another tough year

Financial conditions describe the way in which policy influences the economy through the intermediation of a wide range of market rates, risk premia, and spreads as well as the exchange rate. Unsurprisingly, given the breadth of central bank tightening, last year saw a sharp tightening in global financial conditions, driving a broad risk reversal.

Admittedly, 4Q 2022 was marked by a loosening in financial conditions as markets questioned central banks’ hawkish resolve. However, central banks’ reiteration of their intention to continue raising policy rates and hold at the peak rate for a sustained period should result in a re-tightening of financial conditions in 1Q 2023. The Fed will not permit financial conditions to loosen materially until it feels confident that inflation is on safer ground.

With financial conditions tightening, U.S. job losses set to increase, economic growth entering a clear downtrend, and earnings growth likely weakening, 2023 will see an even more unhospitable environment for risk assets.

The clear outlier may be China, where, once the post-COVID reopening chaos has passed, stimulus measures should be more effective in loosening financial conditions.

Tightening financial conditions have created a hostile backdrop for risk assets, which will only become more inhospitable as recessionary conditions become widespread.

{kind=link}

Equities

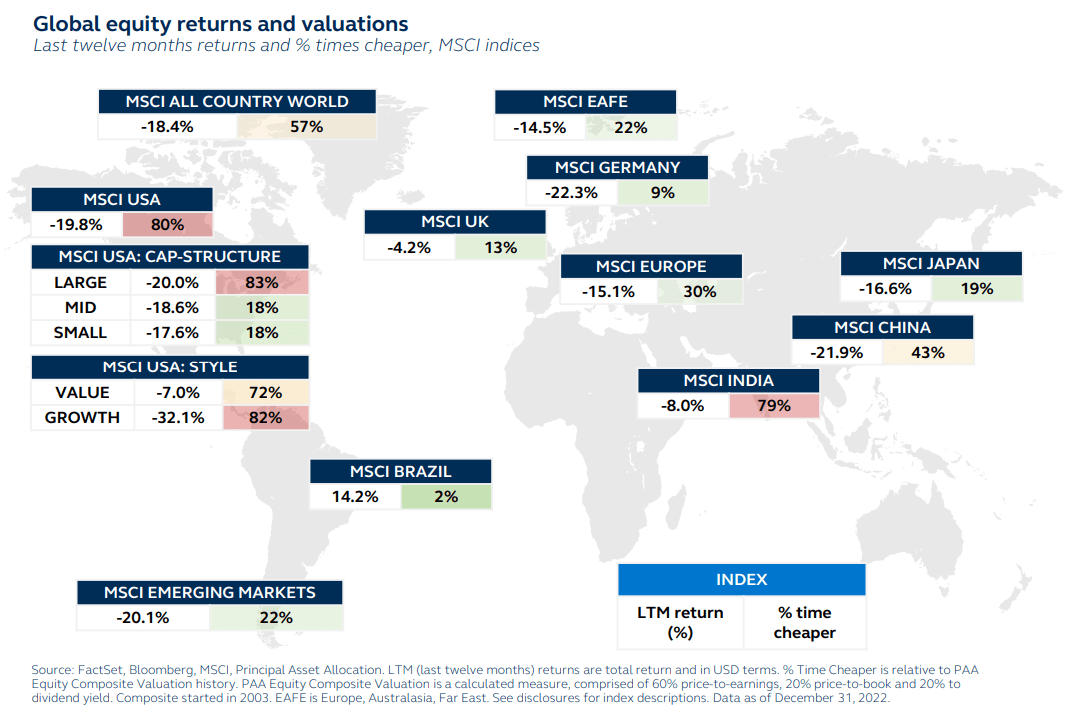

Global equity valuations: Spot the odd one out

2022 was undoubtedly a challenging year for equities. Sharply rising policy rates, much of which had not been anticipated by either investors or central banks, conspired with economic growth concerns to weigh heavily on global equities. At the end of 2022, equity indices were down as much as 29% across the world.

As a result, broad equity valuations have become more attractive and can even be considered historically cheap in a number of markets.

In Europe, Germany and the UK have only been cheaper 15% of the time. In emerging markets, China has been cheaper 40% of the time, while Brazil and Mexico have almost never been cheaper. However, there is one important exception: U.S. valuations are still expensive and have been cheaper almost 80% of the time.

While valuations are instructive for long-term trends, they are less important for short-term dynamics. Yet, once earnings and rates concerns have passed (likely in late 2023), this valuation picture will likely provide guidance as to where the best opportunities lie.

Global equity valuations have become more attractive, and most markets can even be considered historically cheap. The U.S. is the key exception, with still-expensive valuations.

{kind=link}

U.S. equities: Confronting the fallout from rate hikes

Although equity markets are in the midst of a prolonged downturn, their performance has been relatively sturdy considering the headwinds facing the economy. Indeed, despite 425 basis points (bps) of Fed monetary tightening in 2022 alone, the S&P 500 has “only” fallen 19% and is still considered historically expensive - likely supported by the fact that aggregate earnings estimates have only weakened slightly. If the drawdown were to end here, it would put this downturn broadly on par with the 2018 market decline. Back then, the Fed took three years to raise policy rates by just 225 bps, and the economy slowed only modestly.

In 2023, not only are further rate hikes expected, but the Fed is unlikely to deliver any rate cuts even as the economy falls into recession. As a result, investor fixation on inflation and the Fed will persist in 2023. In addition, markets will likely shift their attention to the next serious concern: earnings recession.

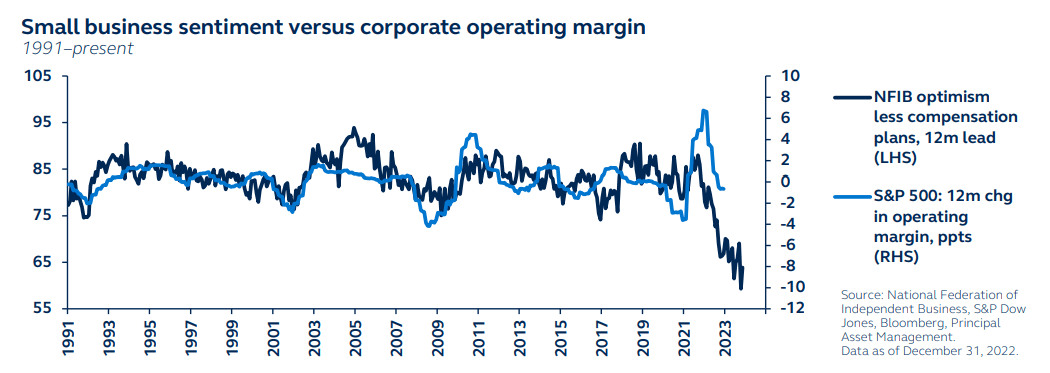

Gross margins are under threat, not just from tight financial conditions and hawkish banks but also tight labor markets. With wage growth so strong and consumer anxieties building, corporate profit margins are being squeezed from both sides. Earnings growth is under severe pressure.

Earnings growth is only just starting to show the impact of last year’s 425 basis points of Fed tightening, pointing to further equity market drawdown ahead.

{kind=link}

{kind=link}

U.S. equities: A downturn, but not a washout

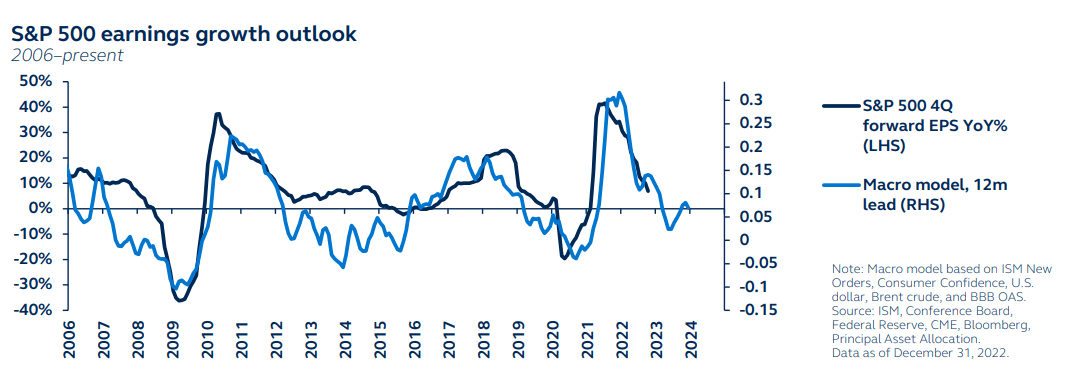

The macro backdrop, with consumer spending under pressure, manufacturing activity struggling, and further rate hikes to come, signals a meaningful fall in earnings that is unaccounted for by markets. In fact, stripping out energy already reveals underlying earnings weakness, with five sectors experiencing earnings contraction. A conservative model, which excludes interest rates, points to an earnings contraction in 2023 - a headwind that will, inevitably, further extend the equity market drawdown.

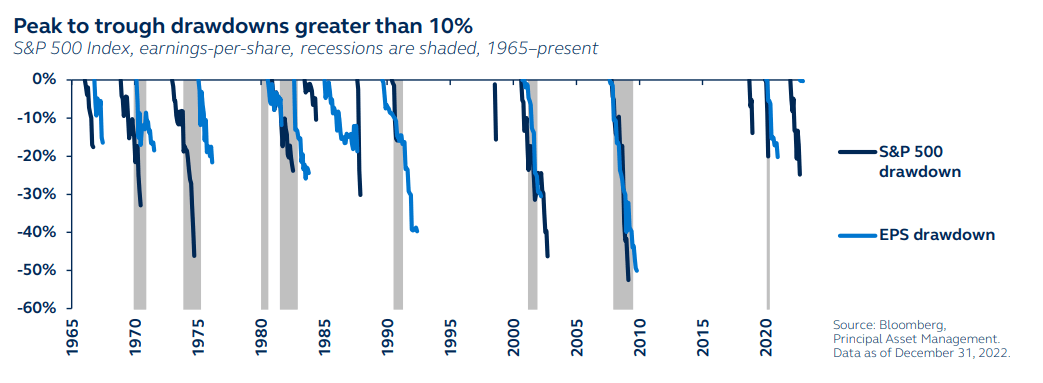

How deep will this bear market be? As a balance sheet recession is improbable, a 45% dot-com bust or even 50% GFC-type market fall is very unlikely. Yet, with the Fed having to prioritize its inflation fight this time, and therefore unlikely to deliver any monetary relief even as earnings forecasts are cut sharply, the equity market drawdown may rival the 1980s 30% decline.

Importantly though, the equity drawdown may not extend the full length of the earnings slowdown. Previous cycles have shown that equity markets typically trough before earnings growth hits its low. As such, while the first half of 2023 will likely be a deeply challenging period, the second half of the year may see a more constructive path forward.

Markets are yet to appreciate downside earnings risk. As Fed tightening transitions into a weaker growth backdrop, the S&P 500 is likely to re-test its September 2022 lows.

{kind=link}

{kind=link}

Mid-caps: Attractive value and defensively positioned

Small-cap valuations are undoubtedly very attractive, yet these cheaper valuations are offset by elevated earnings risk. While small-caps typically outperform in an early-cycle environment given their significant cyclical sector exposure, they face greater margin pressures and greater debt servicing costs when growth is declining.

Large-cap valuations are still very expensive, while their significant exposure to growth stocks implies they will continue to be challenged by high and rising policy rates.

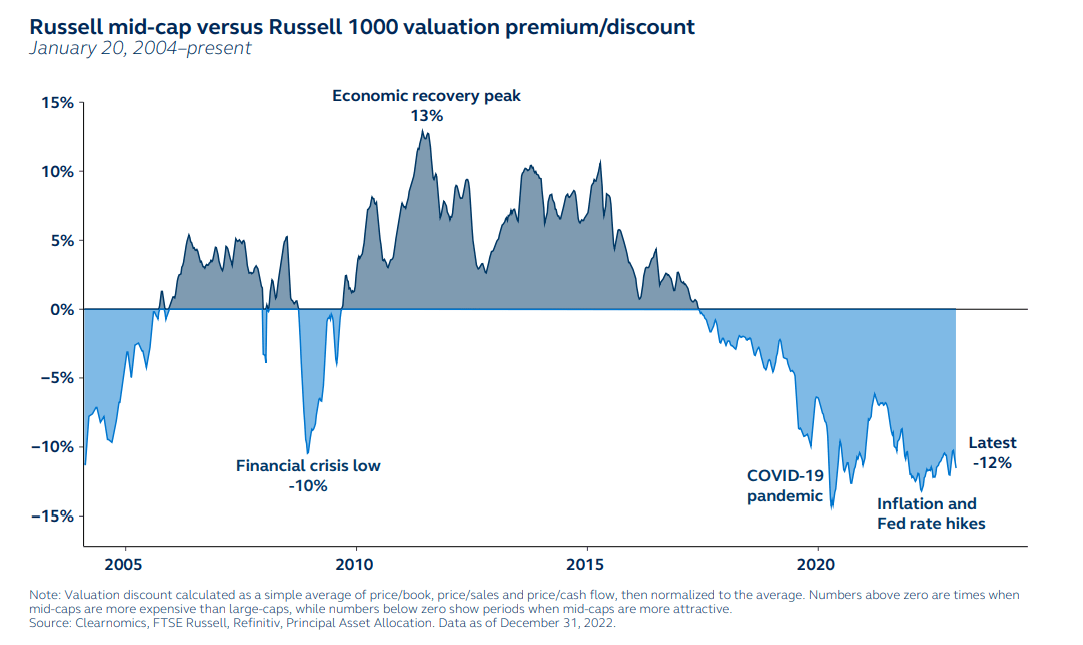

Mid-cap equities offer to bridge the gap between small- and large-caps. Not only are they trading at a meaningful discount to large-caps, but their greater defensive sector exposure means mid-caps are less vulnerable than small-caps to the tough economic backdrop.

With regard to styles, there may not be a clear outperformer. 2023 is likely to be a mixed year. While inflation and higher rates favor value over growth and quality, recession fears favor quality and growth over value. So, while value outperformance may extend into the first half of 2023, recession in the latter half of the year could bring a reversal.

Mid-caps are trading at a meaningful discount to large-caps. Their greater defensive sector exposure means they are less vulnerable to the tough economic backdrop than small-caps.

Russell Mid-Cap Vs. Russell 1000 Valuation Premium / Discount

{kind=link}

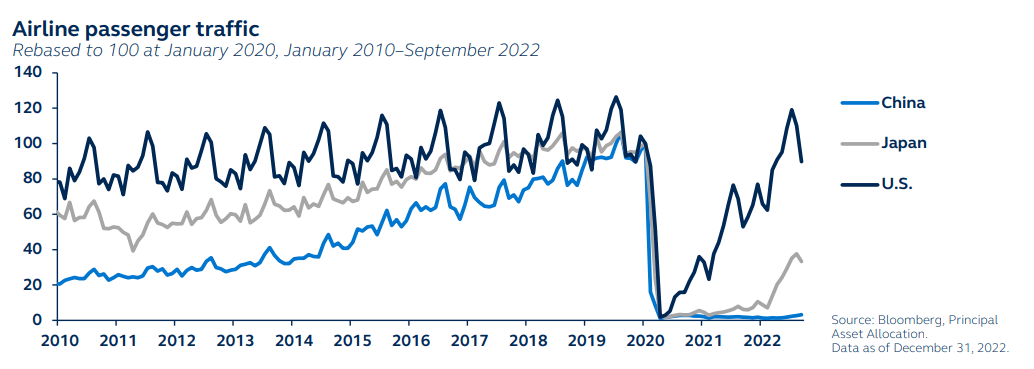

China: A bounce, but longer-term concerns linger

China’s equity market underperformance has lasted almost two years. Frequent lockdowns haven’t just deterred economic mobility (airline passenger traffic, for example, has been extremely depressed) but have also restricted the impact of stimulus on infrastructure investments, in turn worsening the property downturn.

With the true pain residing in the lack of demand, households and companies have not taken advantage of rate cuts or targeted relending. As such, China’s COVID reopening will likely unleash pent-up demand and improve employment, leading to confidence restoration among households and businesses, thereby enabling monetary stimulus to be more effective.

Once the chaos and setbacks of reopening passes, China will likely enjoy a strong bounce in economic activity.

Investor exuberance, however, may not be sustained. The government is still committed to avoiding credit-fuelled property and is unlikely to drop its focus on Common Prosperity goals, suggesting that future stimulus will be very measured. Expect uncertainty and growth concerns to likely return and challenge China’s investment story.

Although policymakers appear to have recognized the urgency for policy stimulus, they have only a narrow window to introduce important policy measures.

{kind=link}

{kind=link}

EM Asia and Europe stand to gain from China reopening

While U.S. markets are still expensive, valuations in most other parts of the world have become more attractive.

European valuations are not only attractive relative to the U.S. but also relative to its own history. Yet, European fundamentals are deeply concerning. Not only is the economy likely already in recession, but inflation concerns are driving the ECB to continue tightening policy at an aggressive pace. The spring may bring positive news with China’s reopening providing a strong boost to growth, but for now, weak fundamentals match cheap valuations, arguing for a neutral exposure to Europe.

In Latin America, growing concerns around fiscal discipline and a potential resurgence in inflation mean that weak fundamentals more than offset its attractive valuations.

In contrast, emerging Asia’s fundamentals are looking much stronger. Domestic demand is robust, and inflation is moderating. Furthermore, as China’s main trading partner, Asia’s growth engine will likely be jumpstarted by China’s reopening. Despite these encouraging developments, investors should retain some caution, as recession conditions and rising rates in developed markets may weigh on EM Asia’s performance in 2023.

China’s reopening should boost activity in its key EM Asia trading partners. But challenging conditions in developed markets will likely weigh on performance.

{kind=link}

{kind=link}

Fixed income

Fixed income: Back in fashion

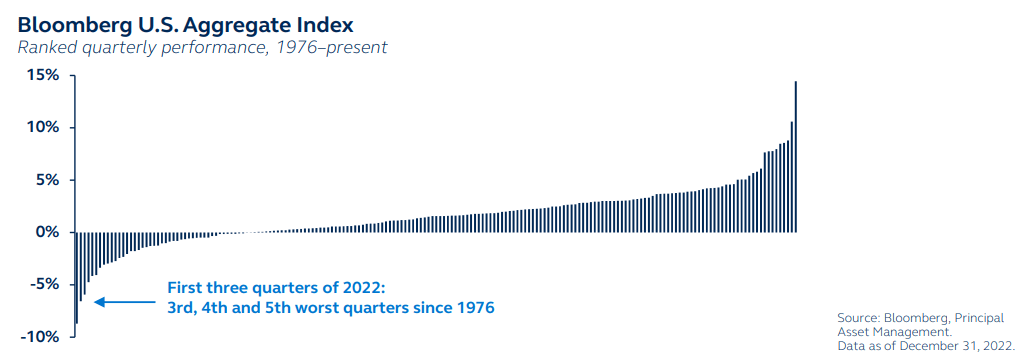

U.S. bonds suffered one of the deepest drawdowns in U.S. history in 2022. In fact, the Bloomberg U.S. Aggregate Index suffered its third, fourth, and fifth worst quarters since 1976. Fixed coupon rates, especially on longer-term bonds, failed to sufficiently compensate investors for raging inflation and a hawkish Fed, warranting a dramatic repricing and leading to painful capital losses for investors.

As markets adjusted to Fed hikes in 2022, the diversification benefits of bonds disappeared, with both stocks and bonds suffering significant declines. For the first time since the 19th century, U.S. equities and bonds simultaneously recorded double-digit yearly declines - a terrible year for 60/40 portfolios.

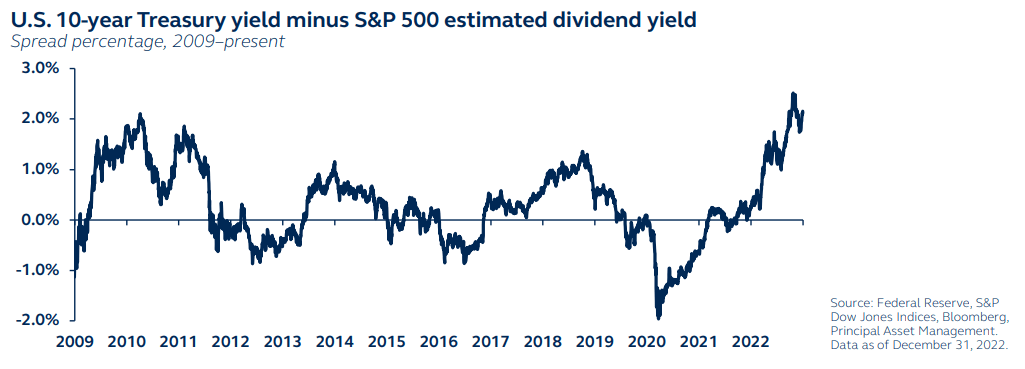

Entering 2023, U.S. 10-year Treasury bonds now yield more than twice the estimated dividend yield of the S&P 500 index. This presents investors with the opportunity to lock-in income with a less-volatile asset. What’s more, with yields having risen and inflation apparently slowing, bonds should provide risk mitigation during the coming economic slowdown. The negative correlation between stocks and bonds has reasserted itself, and the diversification benefit of bonds has been restored.

Having soared in 2022 as markets re-priced Fed expectations, bond yields finally present an investment opportunity, and have regained their diversification benefits.

US 10-Year Treasury Yield Minus S&P 500 Estimated Dividend Yield

{kind=link}

{kind=link}

U.S. Treasurys: Playing an important role in portfolios

As global growth slows and yield curves invert, the stopwatch has been started on a likely recession. Many sectors of the economy have already begun to contract, especially the more rate-sensitive ones, such as manufacturing.

Notably, the rise in bond yields (and drawdown in bond values) seldom maintains amid such an economic slowdown. As such, it is highly likely that, as the economic slowdown continues, the real value of fixed income will be re-priced, permitting bonds to flourish in 2023. Indeed, there has rarely ever been a third year of declines in U.S. Treasurys. So, after two consecutive years of Treasury bond declines, 2023 is trending toward a year of recovery.

A focus on credit quality will also be important as the economy slows, where certainty of cash flows is increasingly valued.

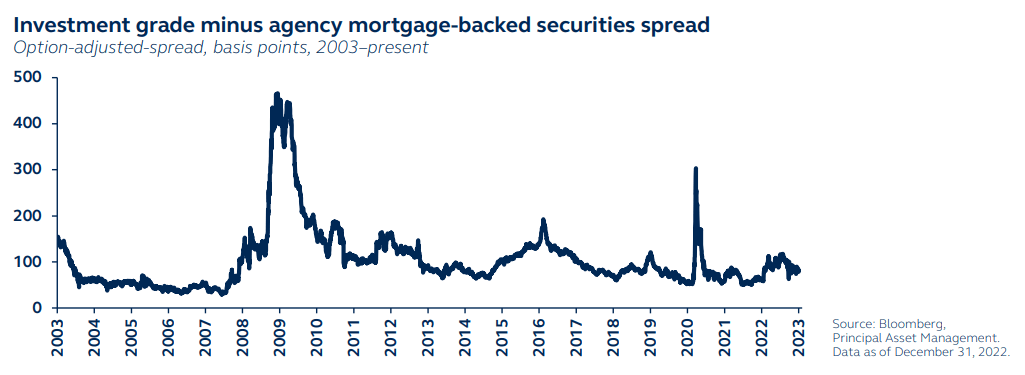

Agency mortgage-backed securities deliver favorable characteristics. Not only are they underwritten by the U.S. government and therefore considered high-quality credit, but agency MBS have a longer duration. These longer-dated, high-quality securities will likely be rewarded as the economy weakens and inflation slows.

Treasurys should perform well as recession approaches, while securitized debt typically shows a greater ability to withstand weakening growth than other credit segments.

Investment Grade Minus Agency Mortgage-Backed Securities Spread

{kind=link}

{kind=link}

Investment grade: More than just a defense play

Traditional fixed income, particularly high-quality credit, may finally be an attractive investment proposition.

Firstly, with the days of cheap funding and abundant liquidity behind us, plus the elevated risk of corporate earnings recession in multiple regions, a growing premium will likely be placed on solid earnings performance. This will be reflected in disparate performance of high- versus low-quality credits.

IG fundamentals are also broadly healthy, with balance sheets still more cash-rich than pre-COVID levels. So, provided the recession is not too severe, IG credit should have sufficient buffer to weather the storm.

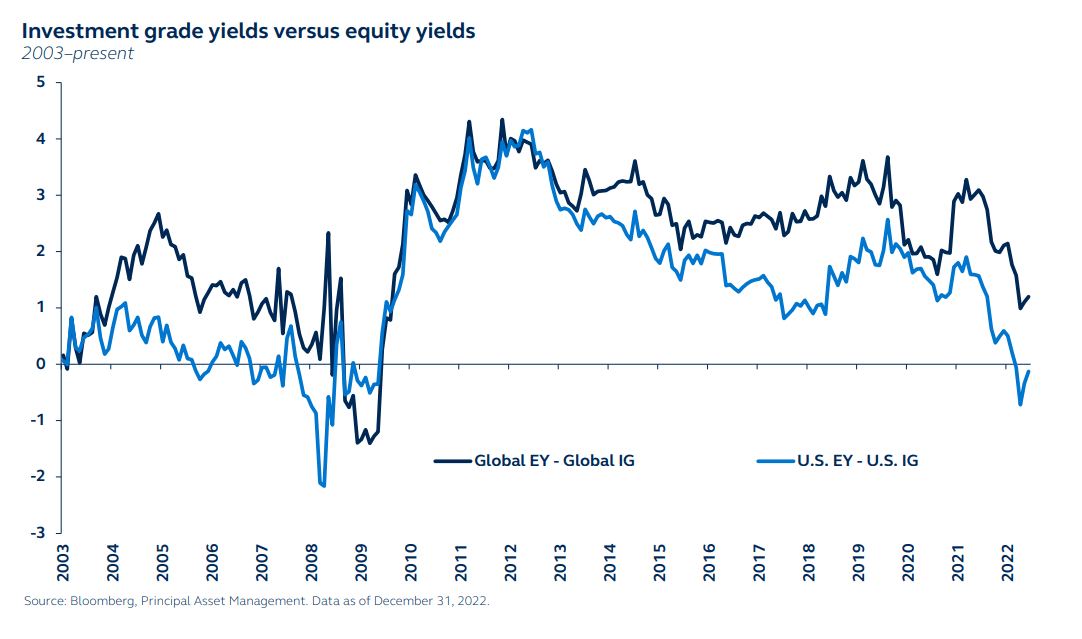

In addition, the case for high-quality credit is more than just defending portfolios from the difficult economic environment: Valuations are also attractive. After a sharp yield reset in 2022, U.S. investment-grade yields have not been so competitive against equity earnings yield since the GFC. Global investment-grade yields have also become relatively more attractive than equity yields, although not to the same extent as in the U.S.

Investment-grade valuations have become more attractive, and higher-quality exposure will be increasingly important as recession approaches.

{kind=link}

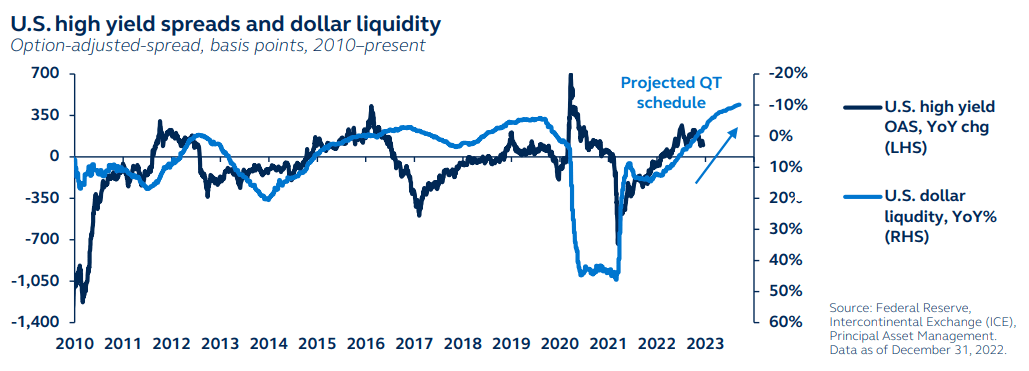

High yield spreads are still bracing for a full unwind

Both the sudden shift in the Fed’s policy stance in early 2022 and historically high inflation left high- and low-quality credit with historically painful drawdowns in 2022.

The Federal Reserve has now begun slowing the pace of its rate hikes, and a Fed pause is increasingly expected in the first half of 2023. Typically, credit does well after the last Fed hike and brings relief to rate-sensitive assets which have suffered the most under rate hikes. Investment-grade bonds, specifically, often outperform given their higher duration and higher quality versus high-yield credit.

If the Fed keeps rates on hold for a prolonged period, companies with leveraged balance sheets will inevitably struggle. While high-yield credits have been somewhat protected through the tightening cycle because the maturity wall has been so low, this cushion will fade the longer the Fed resists cutting rates.

In addition, although the Fed will likely stop hiking rates within the next six months, it will continue to withdraw liquidity via quantitative tightening. Higher-quality credit typically weathers challenging liquidity conditions better than lower-quality credit.

Typically, credit does well after the last Fed hike. But if rates are held at an elevated level for a prolonged period, high yield will likely face a difficult operating environment.

Monthly Performance Relative To The Last Rate Hike In A Hiking Cycle

{kind=link}

{kind=link}

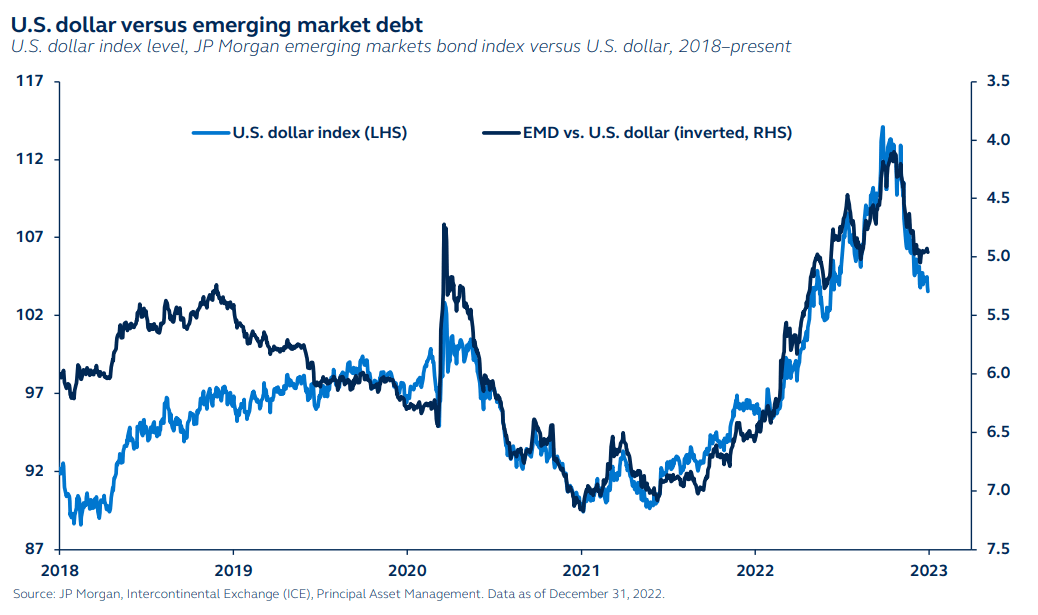

EM debt: Still waiting for its time in the sun

Most emerging markets ((EM)) experienced a year of extreme weakness in 2022. U.S. dollar strength, rising interest rates, high food prices, and geopolitical tensions all weighed on the asset class.

Since U.S. inflation has started to rollover, allowing the Fed to slow the pace of its rate hikes, the U.S. dollar has also begun to show signs of weakening. This presents the potential for optimism for EM, with external debt levels and balance of payments composition key to finding potential outperformance. China’s reopening may also improve the outlook for its key EM trade partners, particularly if combined with effective stimulus measures.

These benefits will likely take some time to materialize. China’s reopening is already proving to be chaotic, so the economic benefits may not be reaped for several months. In addition, the U.S. dollar is likely to be subject to intermittent upward pressure until the Fed finally stops raising rates. As all developed central banks have expressed their intent to further tighten financial conditions into 2023, albeit at a reduced pace, emerging markets are not yet out of the woods.

U.S. dollar weakness and China’s reopening should present potential for EM outperformance. However, tight financial conditions in developed markets mean these tailwinds may take some time to materialize.

{kind=link}

Preferred securities: In a favorable position

The macro environment in 2022 was challenging for the whole of fixed income as central banks around the world aggressively raised rates to fight inflation. But with policy rates now approaching their peak and growth starting to slow, the outlook for preferred and capital securities has improved for several reasons.

Price: Preferred securities are trading at a notable discount to par and are offering attractive valuations.

Yield: They demonstrate relatively competitive yields, even compared to lower-quality fixed-income assets.

Quality: Preferred securities are typically investment-grade quality and, over the past 10 years, have demonstrated lower default rates than high yield. In a slowing growth environment, high-quality should outperform low-quality.

Structure: "Fixed to floating," "fixed to variable" rate structures may help a long-term investor as rates continue to rise.

Financials will be impacted during a downturn. Yet, the strong health of U.S. banks and consumer-focused lenders means financials should remain relatively resilient over the coming challenging months.

We remain slightly overweight preferred securities. Not only are yields relatively attractive, even compared to lower-quality fixed-income assets, but the structure can be ideal in the current environment of still raising rates.

{kind=link}

Alternatives

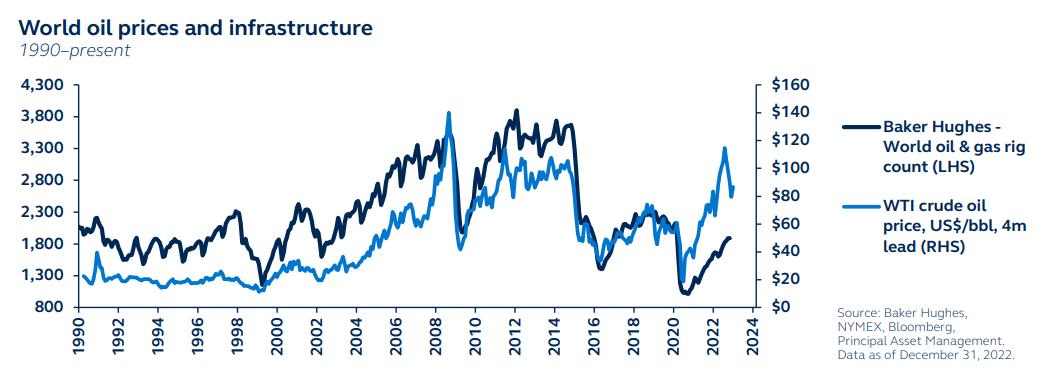

Commodities: Focusing on long-term tailwinds

The commodity complex was the standout performer in 2022, one of the few asset classes to post consistent positive gains for the year. Yet, 4Q saw some of the gains being unwound as fears of fading global economic strength drove prices lower. Industrial metals and agriculture are down around 29% and 12% from their respective peaks, while prices for oil and natural gas are off their peaks 33% and 54% respectively.

Near-term commodity price dynamics are unclear. China's reopening is expected to boost demand, driving prices higher, but spiking infection rates and broader global recession fears may offset those upward pressures. Geopolitical factors impacting commodities supply will also be unpredictable.

Given the difficulty of predicting the short-term outlook for commodity prices, investors should focus on long-term factors. Oil refiners displayed a very muted supply response to near-record prices in 2022, suggesting a decrease in the price elasticity of oil supply. Limited capital expenditure in fossil fuels capacity implies that commodities are likely to remain in a long-term state of structural supply deficits that will be supportive of commodity prices.

While the short-term commodity outlook is uncertain, long-term trends are clearer. Limited capital expenditure is driving structural supply deficits that should be supportive of commodity prices in the long term.

{kind=link}

{kind=link}

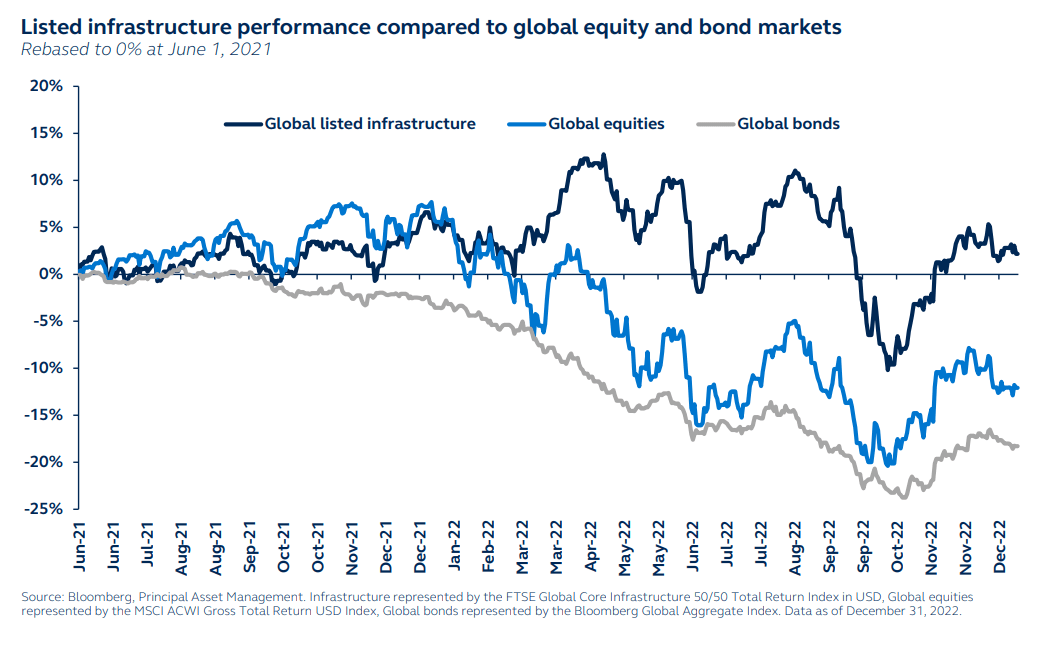

Infrastructure typically shines during high inflation

Our continued constructive view on alternatives conveys not only their diversification benefits in this macro environment, but also their fundamental strengths and defensive characteristics. Infrastructure investments, in particular, are one of the few asset classes that can potentially outperform in the current slowing growth, high inflation environment.

Since demand for critical services is less sensitive to inflation, owners of certain infrastructure assets can sustain and increase prices without significantly impacting demand, offering potentially resilient returns. Listed infrastructure has historically delivered meaningfully higher returns than global equities during periods of higher inflation.

Furthermore, infrastructure investments typically have predictable cash flows associated with the long-lived assets, with historically attractive yields. They also offer exposure to the global theme of de-carbonization, which presents a multi-decade tailwind for utilities and renewable infrastructure companies.

Infrastructure continues to offer important diversification benefits, as well as inflation mitigation and stable income streams.

Listed Infrastructure Performance Compared To Global Equity And Bond Markets

{kind=link}

An environment ripe for real asset outperformance

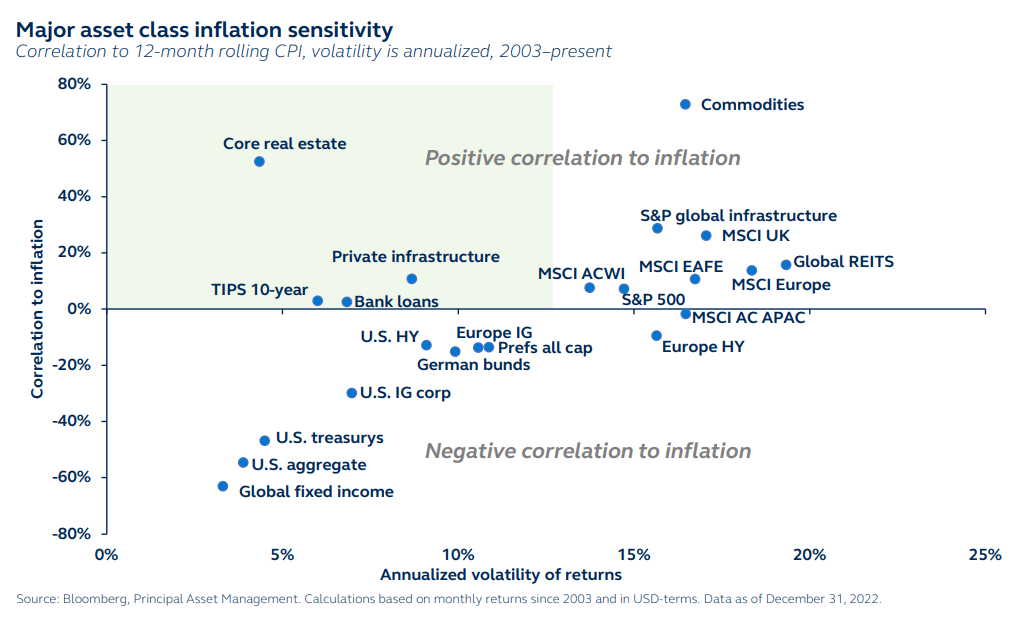

Investors may struggle to find clear opportunities in the current environment. With inflation still elevated and likely to decline very gradually, investors should seek assets with high return correlation to inflation.

At the same time, with economic conditions becoming increasingly difficult, investors ought to have some exposure to low-volatility assets. Assets in the north-west quadrant - low-volatility and high inflation correlation assets - meet this requirement.

- Core real estate and private infrastructure may provide mitigation against elevated inflation.

- Treasury inflation-protected securities ((TIPS)) also work as an inflation-resilient diversifier.

Although returns from commodities and listed infrastructure may be volatile, they historically outperform in inflationary environments, and can help diversify equity exposure. Ultimately, holding a diversified basket of high inflation correlated assets, some low- and some high- volatility, may provide inflation mitigation.

Investors wanting to preserve portfolios against still-elevated inflation, while also seeking to reduce volatility, would be well-suited to add real asset exposure.

{kind=link}

Investment implications

Diversified asset allocation: Underweight equities, overweight bonds, with real assets providing inflation mitigation.

Equities

We keep equities underweight as weakening earnings growth will likely bring further declines, even as the Fed stops hiking. We have no preference for the U.S. over other developed market and emerging market regions given that many of the factors driving U.S. outperformance are fading. Within the U.S., we stay overweight mid-caps given their exposure to defensive sectors and relatively attractive valuations. We keep our neutral exposure to both Europe and EM. While U.S. dollar weakness and China’s reopening may deliver a strong boost, their performances will inevitably be impacted by U.S. recession and broad market weakness.

Fixed income

Our fixed income positioning moves to an overweight, with bonds likely providing risk mitigation during the coming economic slowdown. We further increase our exposure to U.S. Treasurys and shift our exposure to investment-grade from underweight to overweight. Not only does IG offer more attractive yields than in recent years, but the longer-duration, high-quality profile of investment-grade should deliver as the economy slows. By contrast, we keep high yield at an underweight, expecting further spread widening given recession and liquidity fears. Preferred securities remain at overweight due to favorable yields, low default rates and exposure to high-quality companies. EM debt remains an underweight given concerns about global risk appetite.

Alternatives

Our continued constructive view on alternatives conveys not only their diversification benefits in this macro environment but also their fundamental strengths and defensive characteristics. We maintain our overweight to infrastructure, encouraged by its inflation protection characteristics, stability of cash flows, and exposure to the structural de-carbonization trend. Despite short-term demand concerns, we also maintain our overweight preference to commodities, as medium-/long-term structural supply shortages should continue to support performance. With the outlook looking increasingly volatile in 2023, we increase our exposure to hedge funds.

Principal Asset Allocation, Data as of December 31, 2022

Alternatives asset class include commodities, natural resources, infrastructure, REITs, and hedge funds. Allocations across the investment outlook can be proportionately adjusted so magnitudes across categories do not have to net to neutral.

| Equities Reduce risk appetite and focus on U.S. mid-cap and quality factor. |

| Position toward certainty • Exposure to quality within equities can potentially offer risk mitigation during pullbacks. • Attractive international valuations suggest opportunities outside the U.S. • U.S. mid-cap offers stronger geographical revenue exposure and more attractive valuations. |

| How to implement • Mid-cap U.S. strategies • Quality-biased active managers • Well-diversified strategies across DM and EM markets |

| Fixed income Increase exposure to high-quality credit. |

| Core fixed income and preferred securities • Core fixed income to hide out in as recession risk rises • Recommend increasing duration bias across the asset class. • Preferred securities provide potential yield and exposure to high quality. |

| How to implement • IG credit heavy core fixed income for stability • Preferred securities strategies • Agency MBS strategies |

| Alternatives Pursue less correlated real asset exposures. |

| Real assets • Real return-focused strategies gain attractiveness when nominal growth slows. • Infrastructure offers more stable cash flows with potentially attractive yield. • Real assets can help mitigate inflation risk. |

| How to implement • Diversified real asset strategies (infrastructure, natural resources) • Private real estate markets |

Editor's Note: The summary bullets for this article were chosen by Seeking Alpha editors.

For further details see:

Global Asset Allocation Viewpoints, Q1 2023: Half Agony, Half Hope