PGJ - Global Asset Allocation Viewpoints Q1 2024 - Gentle Slope Not Cliff Edge

2024-01-11 03:41:00 ET

Summary

- Economic growth is now cooling as global monetary tightening gradually takes its toll.

- Most central bankers have now adopted a more dovish stance, and rate cuts are likely in 2024.

- Rate cuts failing to materialize may drive extended U.S. Treasury disappointment in 1Q.

By Todd Jablonski, CFA, CIO, Asset Allocation; Seema Shah, Chief Global Strategist; Brian Skocypec, CIMA, Director, Global Insights & Content Strategy; Han Peng, CFA, Director, Quantitative Strategist; Ben Brandsgard, Insights Strategist

Key themes for 1Q 2024

• Global growth is coming off the boil. Economic growth is now cooling as global monetary tightening gradually takes its toll. U.S. recession risk has diminished, although consumer headwinds are rising. China and Europe are likely to see another year of tepid growth.

• Global disinflation continues unabated. Price pressures have eased significantly, largely due to resolved supply chains. The last mile of disinflation toward central bank targets will require some economic slowdown and job market weakness.

• A central bank pivot is upon us. Most central bankers have now adopted a more dovish stance and rate cuts are likely in 2024. Yet, they may come slightly later than markets anticipate and will likely be gradual—unless economic growth surprises to the downside.

• Equities will likely see volatility in H1 followed by a rally in H2 as policy easing arrives. Falling bond yields have driven a sharp market rally, but this can only be sustained if earnings deliver. An economic slowdown in H1, coupled with slightly later than expected rate cuts, suggest some volatility.

• Fixed income credit spreads are very tight going into an economic slowdown. Rate cuts failing to materialize may drive extended U.S. Treasury disappointment in 1Q. Higher-quality credit should perform better than lower-quality credit as the economy slows, and as the maturity wall becomes more pressing.

• Alternatives provide important diversification against traditional equities and fixed income. Commodities are facing an unclear near-term future as investors weigh up geopolitical risks versus greater U.S. oil supply. With real bond yields likely having peaked, REITs are facing a much brighter outlook.

Central bank policy: Pause and pivot

Most global central banks have come to the end of their tightening cycles. Policymakers are eyeing the disinflation progress with great interest, gearing up for policy rate cuts as inflation approaches central bank targets. The last mile of inflation deceleration will not be straightforward. If economic growth remains above trend, price pressures will threaten to re-emerge. So, a cooling in economic momentum and a softening in labor market dynamics are required to ensure inflation is on a sustainable path back to target.

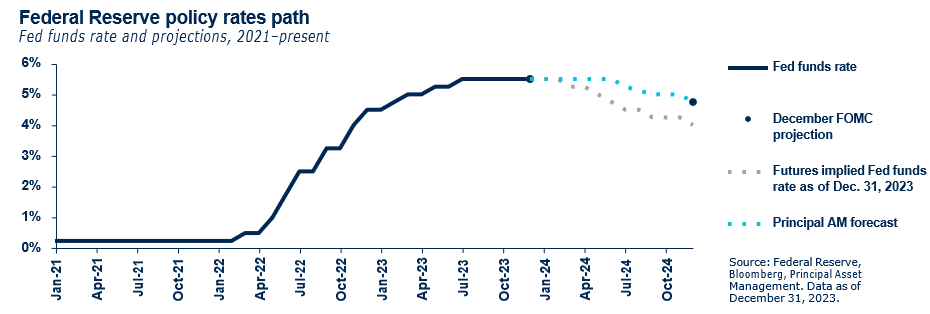

Although the market believes the Federal Reserve ((FED)) will be ready to ease policy as soon as March, today’s resilient economic backdrop suggests it may take slightly longer, around mid-year, before policymakers feel confident that the inflation genie is back in the bottle. Nonetheless the more important message is that there is a path to monetary easing in 2024. Uncertainty around the exact timing of cuts will add volatility, but it will not change the trend.

The wall of cash

The macro and market backdrop has been confusing over recent years, prompting many investors to flee to money market funds (MMFs), attracted by their higher-than-normal returns, as well as the additional stability they offer. 2024 should see many of the concerns and questions of recent years finally resolved. The long-awaited downturn should arrive and depart without leaving much destruction, inflation should continue to decelerate and, most importantly, the Fed is likely to open the door to rate cuts, reducing the attractiveness of MMFs. The substantial pool of cash currently being harvested in MMFs (almost $6 trillion) is poised to fuel a significant rally in risk assets, offering investors an opportunity to capitalize on improved sentiment and market dynamics.

A new regime

The post-GFC years characterized by sub-target inflation, quantitative easing and fiscal conservatism have evolved into a regime where above (as well as below) target inflation is possible, central bankers actively avoid ultra-easy policy, and fiscal stimulus is recognized as an effective policy tool. The broader financial system will take some time to adjust to this new regime given the upward impact on the cost of capital. Disorder and volatility in low quality credit is likely—bad management, zombie companies and over-exuberance will likely be gradually exposed.

For investors, equities should still benefit from reflationary conditions, although an enhanced screening process is important. Bonds will likely still preserve portfolios in disinflation shocks but will not help in inflationary shocks, so real assets will remain an important part of a portfolio. The new regime calls for investors to actively diversify, taking full advantage of the toolkit in the years ahead.

Consider the potential risks

Resurgent inflation: If economic growth fails to slow, it risks igniting a resurgence in price pressures. Central banks would have to respond by resuming policy tightening, tipping economies into deep downturns. Even worse, if growth slows but rising energy prices result in a de-anchoring of inflation expectations, central banks would still need to respond to the stagflationary environment by hiking rates further.

Financial market stress : Previous monetary tightening cycles have ended in financial turmoil. Despite economic and market resilience, investors should be alert to the elevated risk of financial markets stress, particularly if the impending credit maturity wall coincides with a renewed rise in bond yields.

Global economic growth comes off the boil

Investors were almost universally surprised by global growth last year—by the extent of U.S. resilience, the depth of China weakness, and the extent of global disinflation. Economic growth is now cooling in most parts of the world as monetary tightening gradually takes its toll, although timely data suggest a continuous U.S. weakness as opposed to other regions experiencing more pronounced setbacks. Indeed, strong support from consumer spending and the labor market has significantly reduced the risk of recession, although rising credit card delinquencies and reduced job postings suggest headwinds are building. Europe remains a weak link, with soft economic data suggesting that it is flirting with stagnation. In China, policy stimulus is likely insufficient to drive a significant economic recovery in 2024.

There will be strong contributions from other economies such as India and Japan. Yet, slowing growth in the U.S., China, and Europe implies a slowdown in overall global economic momentum. While it’s likely to be more of a gentle downward slope, it does render the global economy vulnerable to additional shocks. The good news is that the slowing growth environment should drain out the most stubborn of inflationary pressures, opening the door to gradual global policy easing in mid-2024.

The global economy is cooling now as monetary tightening gradually takes its toll. This will drain out the most stubborn of price pressures, opening the door to global policy easing.

{kind=link}

{kind=link}

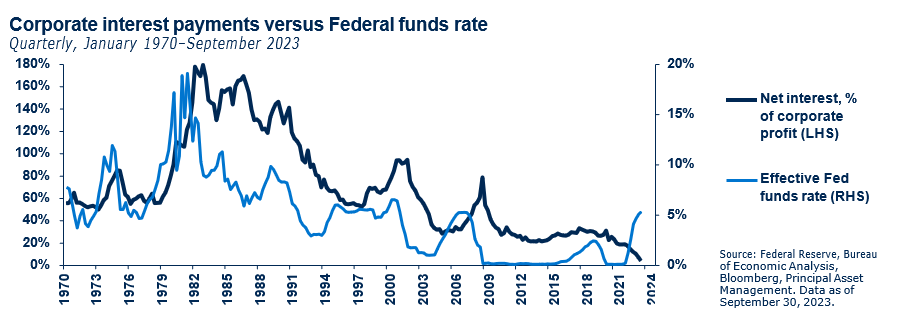

Powell pillow: Insulating the economy from his rate hikes

The U.S. economy’s resilience can be largely attributed to pandemic stimulus measures, which created an economy with unique defences against central bank tightening.

On the corporate side, the 2020 Fed lending program permitted corporations to take full advantage of record low rates, issuing debt at record levels and locking in low rates. As a result, even as Fed rates have risen to 22-year highs, corporate interest payments have dropped to the lowest levels seen in more than 50 years.

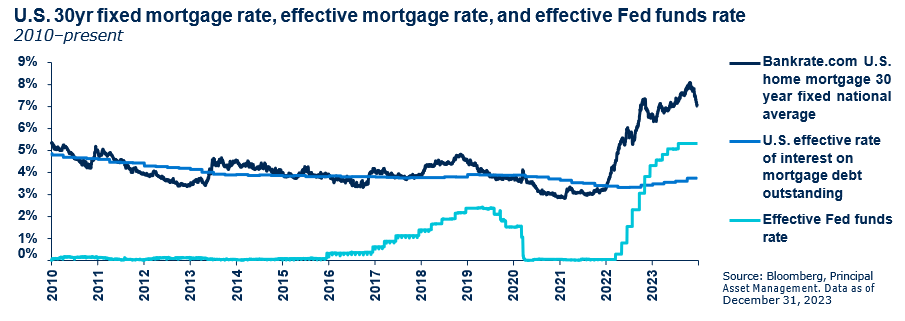

U.S. households also took advantage of the 2020 drop in interest rates to lock in record low mortgage rates. So even as a 30-year mortgage rate has soared to above 7.5%, the effective rate on the outstanding stock of mortgage debt is only sitting at around 3%.

These buffers have effectively insulated the U.S. economy from higher policy rates. Next year, however, a significant number of corporate bonds will mature, particularly for the most leveraged issues, requiring refinancing and at significantly higher rates than their existing loans. Growing numbers of mortgages will also come due for refinancing, but the numbers are not expected to be very onerous. The U.S. economy will finally face the reality of higher rates.

Pandemic era buffers will fade slightly in the year ahead, particularly on the corporate side. The U.S. economy’s defences against monetary tightening are fading.

{kind=link}

{kind=link}

2024 weakness: Good things never last forever

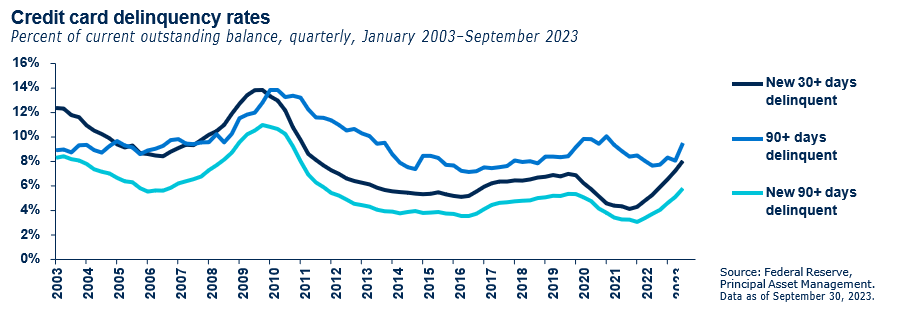

Consumers have continued to be a key backstop of the U.S. economy. While aggregate excess savings are getting consumed at a rapid pace, particularly for lower income groups, the build-up of such a significant cushion in earlier years has prevented household balance sheets from deteriorating significantly.

As a result, consumers enter 2024 in fairly good shape and better able to withstand headwinds from expiring mortgage terms, the resumption of student loan interest payments, and waning fiscal support. However, they are not entirely immune. Credit card lending has been steadily rising, as have delinquencies, suggesting a consumer slowdown ahead.

The labor market has remained robust, but it too is showing signs of softening which will weigh on households. As well as weaker payrolls growth, there are reduced job listings, growing numbers of firms announcing headcount reductions, and fewer people quitting jobs to take on others. Indeed, for those moving jobs, the associated pay jump for switching jobs has almost halved versus a year ago. The likely rise in unemployment will fall well short of previous downturns, but should be sufficient to drive an economic slowdown around mid-2024.

Consumers enter 2024 in strong shape. Yet, credit card delinquencies are rising, and the labor market is softening, suggestive of a modest slowdown ahead.

{kind=link}

{kind=link}

Global disinflation: Turns out inflation was a bit transitory

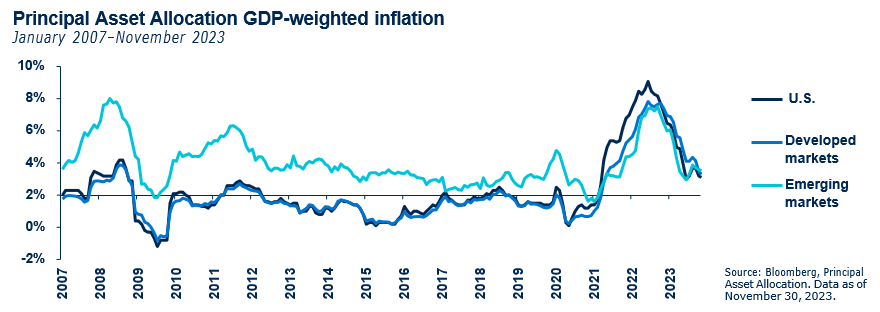

Global disinflation has made significant headway in 2024. In many countries, including the U.S., inflation has more than halved from its peak levels and continues to trend lower, despite continued economic resilience. In Europe, where the economy has already taken a more negative turn, inflation has actually fallen faster than it initially rose. There are a few notable exceptions: In Japan, inflation is rising at a healthy and welcome pace, and China, where inflation continues to fall short of the central bank’s target and, in fact, deflation remains a threat.

Supply chain normalization has been a major driver of global disinflation. Yet, with core commodities inflation now back to pre-pandemic levels, the last mile of inflation deceleration to target levels will require a rebalancing of labor market and an economic slowdown.

Note that inflation does not need to fall all the way to the 2% central bank targets. Policy easing will likely commence once there is sufficient confidence that inflation will sustainably settle near the 2% target. For now, however, with U.S. economic growth still firmly above trend, the threat of re-emerging price pressures cannot be ignored.

DM central banks have made encouraging disinflation progress. Yet, the final shift lower towards central bank targets would require a meaningful economic slowdown.

{kind=link}

{kind=link}

Central banks: pivot, pivot, PIVOT

Inflation is approaching central bank target levels, opening the door for a global policy pivot in 2024. Indeed, as slowing economic activity will put further downward pressure on price pressures over the coming quarters, the Fed will need to cut policy rates just to maintain the same level of monetary restriction in real terms.

The Fed and markets agree that rate cuts are coming, but less so on exactly when and by how much. The Fed will likely require the U.S. economy to show distinct signs of slowing before they can feel confident that inflation is on a sustainable path to target, and before turning to rate cuts. As such, the market’s expectation for policy easing to begin in March is likely a little optimistic. Yet, the more important message is that a path to rate cuts is emerging.

The European Central Bank (ECB) and Bank of England ((BOE)) are also set to cut rates. For the ECB, as the economy is already stagnating and disinflation is rapid, rate cuts will likely be more aggressive than for the Fed. The UK economy is struggling, but higher structural inflation suggests the BOE could be more hesitant. The Bank of Japan is the outlier: It is set to shift away from yield curve control, albeit cautiously and only if it has sufficient evidence of wage growth.

Fed policy rates are set to fall in 2024. Clear evidence of an economic slowdown likely needs to emerge before cuts can commence, likely around mid-year.

{kind=link}

{kind=link}

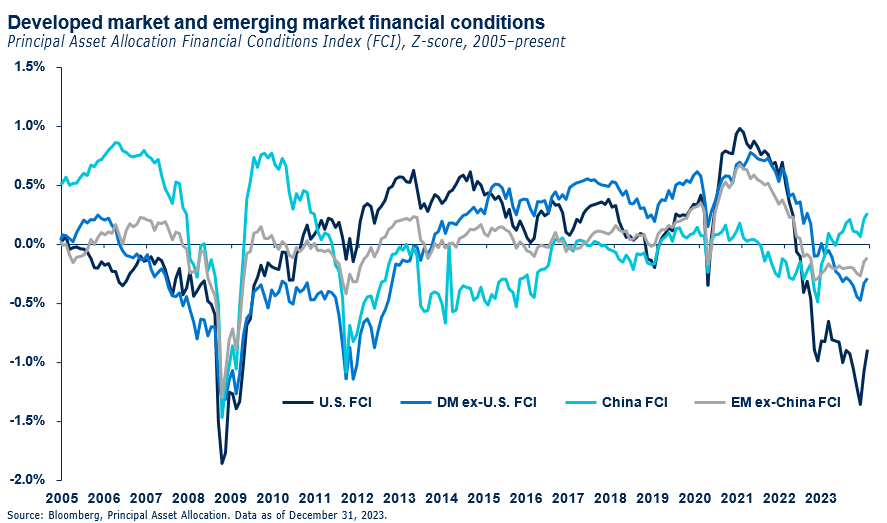

A shift in financial conditions sets up a constructive 2024

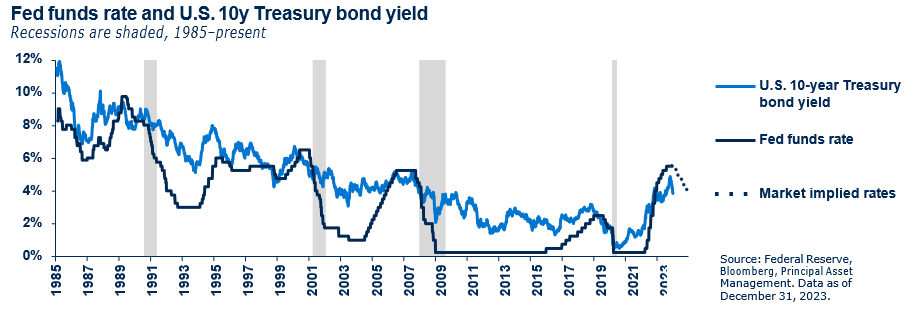

Global financial conditions initially tightened further in 4Q as global bonds sold off sharply, taking 10-year U.S. Treasury yields momentarily above 5% for the first time since 2007. However, a slight shift to more dovish language from the Fed in late October opened the door to an easing in financial conditions. This was further reinforced by a very clear signal from the Fed that rates have peaked and the next move will be a cut, driving Treasury yields back below 4%. Such a significant drop in bond yields permitted U.S. equities to rally sharply and regain their previous record highs.

The sharp easing of financial conditions in 4Q is unlikely to continue at the same pace. Near-term volatility as rate cut expectations are repriced may trigger a slight tightening in early 2024. But, provided core inflation continues to trend downwards, financial conditions should eventually re-ease.

Such a backdrop is typically conducive for risk assets. Yet, as falling rates will likely be accompanied by slowing economic growth, and considering that valuations across both equities and credit are expensive, investors will need to carefully seek out opportunities. Quality, earnings potential, and attractive valuations will be king.

Financial conditions may be volatile in early 2024 amidst market repricing of rate cut expectations. Even so, the general trend for 2024 will be easier financial conditions, suggestive of a generally constructive backdrop for risk assets.

{kind=link}

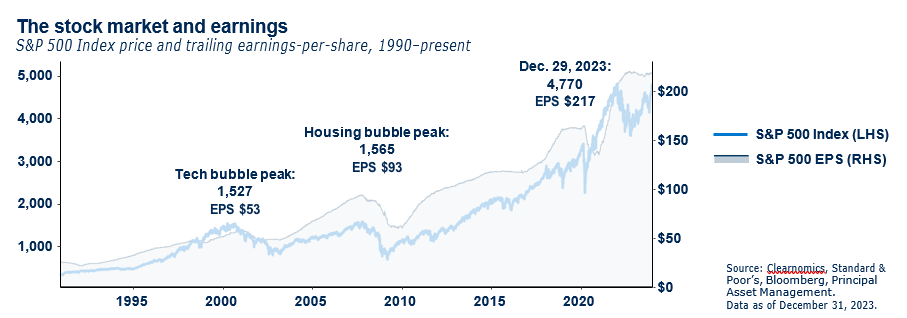

Global equity valuations remain stretched

Following a tepid 3Q, global equities marched higher in 4Q to close the year with a 22% gain. The rally was broad- based with U.S. and Latin America being the main regional outperformers, while China remained the laggard. Unsurprisingly, growth stocks were the main beneficiary of falling yields, but other styles also joined the rally at year- end, suggesting a goldilocks scenario of a U.S. soft landing with an early Fed pivot is increasingly priced in.

As a result, global equity valuations are generally more stretched. U.S. large-cap and growth remained the most expensive markets, while small- and mid-cap valuations were relatively appealing, albeit more expensive than in earlier quarters. Both Europe and Japan's valuations moved above their historical medians. Within Europe, Germany was valued at relatively attractive levels.

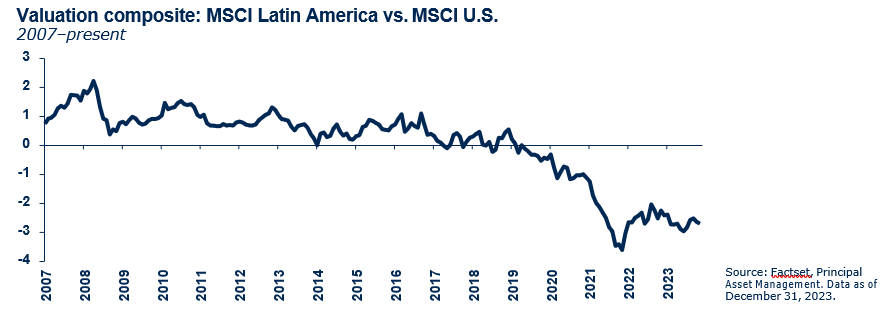

Emerging market valuations are also higher than their historical medians despite a continued China selloff. Regional divergence was significant. India's valuations are stretched and have been cheaper 89% of the time. By contrast, Latin America still looks attractive after the rally, with Brazil and Chile having been cheaper only 14% and 6% of the time, respectively.

Global equity valuations remained stretched. The U.S. remains the most expensive market globally, while Latin America has rarely been cheaper.

{kind=link}

U.S. equities: A year of two halves

Rich equity valuations, a soft economic landing, and a Fed pivot suggest that 2024 will likely be a year of two halves.

Plunging bond yields in 4Q permitted U.S. equities to regain their previous record highs. Yet, lower yields can support equities on a sustained basis only if earnings remain healthy. In H1, elevated earnings growth expectations will likely be tested by slowing consumer demand as excess savings erode, the labor market softens, and delinquencies rise.

Margins will also be under pressure given less opportunity for price padding in the lower inflation environment. These headwinds may challenge the strong equity narrative in H1.

However, equities should see renewed resurgence in H2. Not only will a recovering U.S. economy imply support for earnings growth, but contained price pressures mean that the Fed can likely begin monetary easing. Historically, U.S. equity returns during Fed easing cycles are not resoundingly positive. Yet, during the few easing cycles where recession has been avoided and, as a result, earnings growth has only weakened slightly, equity markets have reacted positively.

While the first half of 2024 may prove choppy, investors with longer-term horizons should identify good value opportunities and position for an equity market rally in H2.

Rich U.S. equity valuations will be challenged by economic headwinds in H1, but a Fed pivot and the ensuing economic recovery should support equities in H2.

{kind=link}

{kind=link}

U.S. market leadership: A broader story in the making

Last year’s equity market rally was unusually narrow, with the S&P 500 up 26% but the equal-weighted version up only 14%. Yet, U.S. equity market breadth showed signs of broadening out in 4Q, with the market-cap-weighted index delivering similar returns as the equal-weighted index. While mega-tech concentrated sectors such as IT, communication services, and consumer discretionary still recorded the best year-to-date returns, on a three months basis, traditional cyclical sectors made strong gains.

Early signs of the market broadening out suggest it has priced in continued economic resiliency. This may be temporarily tested in H1 when economic growth slows. In a soft-landing scenario, large-cap may still perform well due to their defensive nature, but small-cap likely would not underperform significantly either. This implies a more neutral stance may be warranted in the near term.

However, as the year progresses, a portfolio tilt towards small-cap is advised. Indeed, the valuation gap between large- caps and small-caps is still significant. Furthermore, history suggests that once the U.S. economy enters a new stage of recovery and the Fed starts a new rate cut cycle, small-cap could outperform in such an environment.

Equity market breadth broadening may be stalled by the economic slowdown. Small-cap could do well in the following recovery phase.

{kind=link}

{kind=link}

Japanese equities: Losing their allure

The macro themes between Japan and Europe remain desynchronised. Japan’s economy performed strongly in 2023 and, while set to decelerate in 2024, it is likely to remain robust, providing important support for earnings. Furthermore, while the Bank of Japan (BOJ) is likely to continue policy normalization, the pace should be gradual to prevent unnecessary volatility and market disorder.

Yet, there are concerns brewing. Overweight positioning in Japan has become a common trade, suggesting additional gains are becoming limited. In addition, while yen weakness acted as a strong tailwind for earnings in 2023, the risk of aggressive Fed cuts or a faster than expected BOJ pivot could drive yen appreciation in 2024 and, therefore, a weakened earnings outlook. It may be an opportune time for some profit taking.

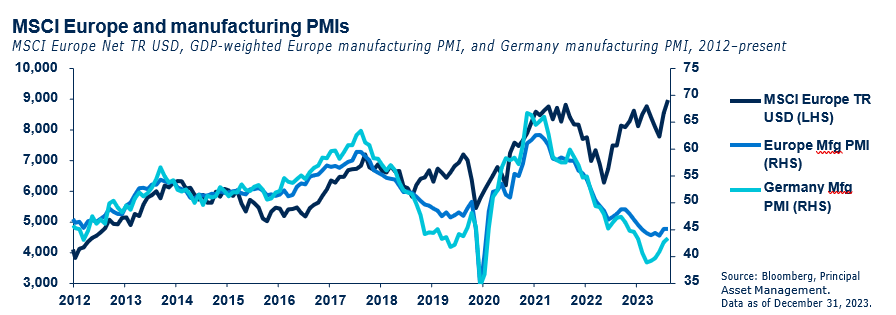

The macro environment is considerably dimmer in Europe. While the ECB is set to reduce policy rates in 2024, these expectations are accompanied by concerns for a persistently stagnant economic state. Earnings revisions momentum has started deteriorating amid the pessimistic outlook, but have further to fall before they become more realistic, suggesting further downside for European equities.

Japan remains a relative bright spot in the global economy, but yen appreciation risks suggest it is time to take profits. European earnings expectations remain too optimistic.

{kind=link}

{kind=link}

EM equities: Opportunities exist outside of China

Although China’s economic growth has showed some signs of stabilization in recent months, the property sector continues to struggle, in turn weighing on consumption. Policy stimulus has been recently ramped up and this positive momentum should extend into 2024. However, with policymakers still trying to balance supporting the beleaguered property sector and avoiding creation of a new asset bubble, a full-fledged credit expansion is still not the base case. As a result, a significant economic recovery is unlikely in 2024 and investor confidence is set to remain muted, continuing to weigh on China’s equity performance.

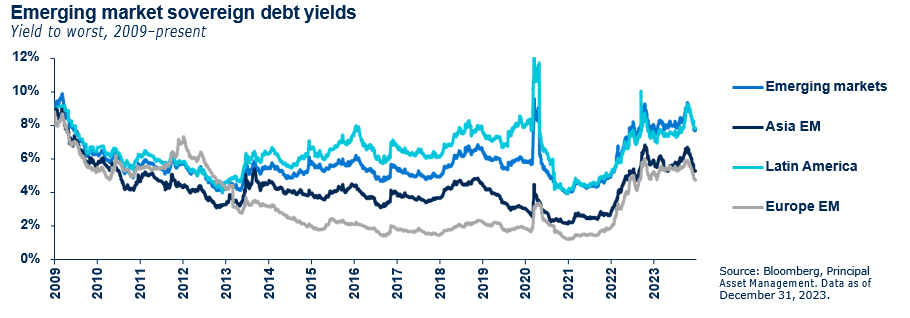

Despite persistent China weakness, there are several opportunities across the broader emerging market space. Latin America, in particular, has strong prospects. Not only are their central banks already cutting policy rates and set to continue easing in 2024, but political stability has also become more apparent in Brazil and Mexico, reducing a key risk for its investment outlook. The region also offers deep valuation discounts, with Chile and Brazil cheaper today than 90% of the time. From a more strategic perspective, Latin America stands to gain from the structural tailwinds of global supply-chain reshoring and the resulting increase in foreign direct investment.

While disappointing economic activity has prompted more policy stimulus in China, investors remained skeptical. Latin America remains a bright spot for EM investors.

{kind=link}

{kind=link}

Fixed income: Tight credit spreads will be challenged

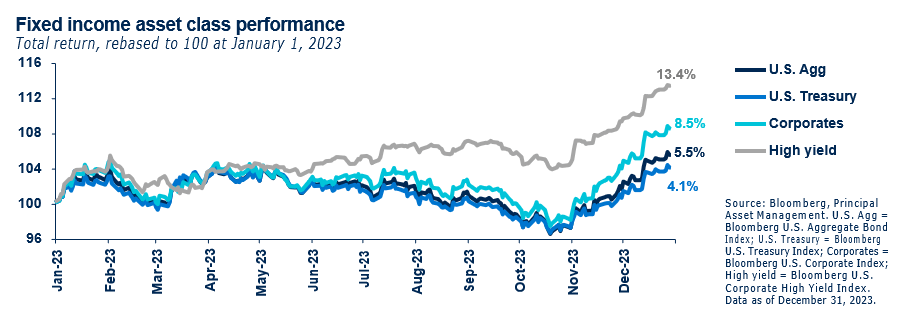

The U.S. fixed income market experienced a very volatile 2023. The U.S. Agg struggled for much of the year before a sharp rebound in 4Q delivered a strong quarterly return and, ultimately, the first positive annual return since 2020.

U.S. Treasurys were the top performer in 4Q, benefiting significantly from aggressive Fed cut expectations and reduced term premia. Within the credit space, longer duration assets, such as investment grade, outperformed shorter duration assets, such as high yield and leveraged loans, despite greater spread tightening in the low-quality space.

Global fixed income followed the U.S. Agg higher as the ECB also shifted to a more dovish tone and the BOJ pursued policy normalization less aggressively than expected. The weaker U.S. dollar provided an additional boost to unhedged global bonds.

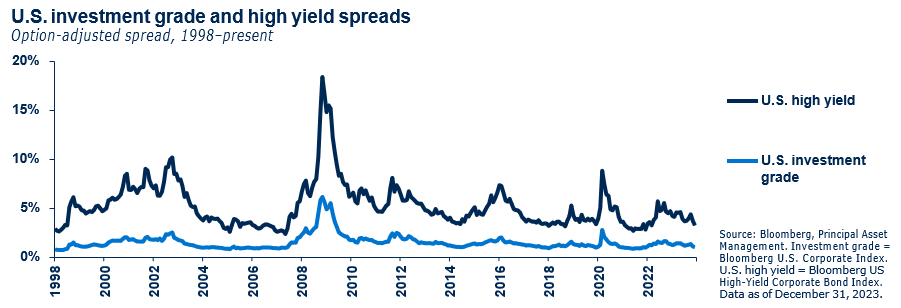

Looking to 2024, Treasury yields may have some near-term upside pressure if aggressive rate cut expectations fail to materialize, although slowing growth and inflation suggest that rates are unlikely to rise significantly from current levels. Credit faces some headwinds given that spreads are at their tightest levels since early 2022, pricing in a goldilocks scenario of a soft landing and a dovish Fed. The unfolding economic slowdown through 2024 will likely challenge these valuations.

Global bonds rallied in 4Q on Fed and ECB pivot hopes and a less aggressive BOJ. Yet with credit spreads historically tight, an economic slowdown in 2024 will challenge valuations.

{kind=link}

{kind=link}

U.S. Treasurys: Playing the Fed pivot game

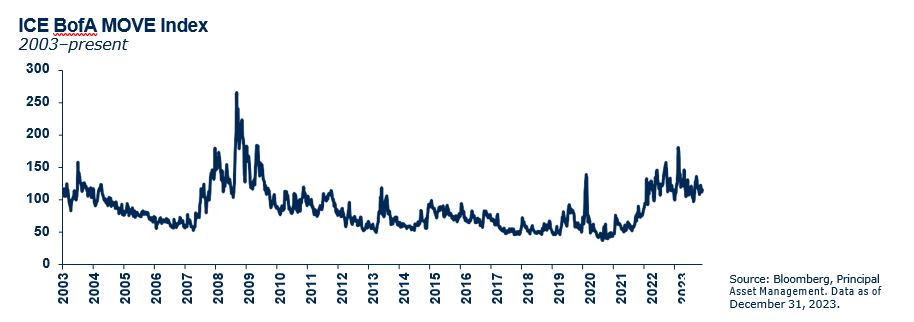

U.S. Treasury volatility remained elevated for most of 2023, with 10-year U.S. Treasury yields hitting a 16-year high at 4.99% before a perceived Fed pivot in 4Q drove yields significantly lower, closing the year at 3.88%. The Treasury market will likely remain volatile as the debate around the rates outlook rages on and investors continue to focus on fiscal stimulus and Treasury issuance plans in an election year.

Bond markets have priced in considerably more aggressive cuts than the latest Fed dot plot implied for 2024. If Fed cuts take a little longer to materialize than expected, some upward correction in yields is likely in the near term—inflation signals will be a key focus point for investors. Once the Fed does start cutting, likely around mid-2024, Treasury yields should resume a slight downward trend, weighed down by the cooling economy and more muted inflation.

However, it is worth noting that in the absence of a severe recession. Treasury yields are unlikely to revert to the ultra-low levels of recent years. Indeed, the Fed is keen to avoid taking rates near zero again, while structural inflation dynamics likely imply that global central banks will need to remain more alert to price pressures. In addition, shifting supply/demand dynamics in the Treasury space imply higher term premia.

Treasury volatility is likely to remain elevated as the Fed rate debate rages on. From a longer-term perspective, U.S. Treasury yields are likely to settle at a higher level than the last 10 years.

{kind=link}

{kind=link}

High-quality credit remains favorable ahead of slowdown

Investment grade credit performed strongly in 4Q as Fed pivot expectations drove down yields while soft-landing hopes compressed spreads. The fundamental outlook for core fixed income remains robust, supported by an upgrade cycle as well as diminished risks of a hard landing. However, IG credit spreads are historically tight and unlikely to compress much further given the broad market’s expectation for a soft landing.

There is a strong income argument for IG credit. Despite the recent bond rally, IG yields are still much higher than the average of recent decades and, with rates unlikely to fall all the way to the previous decade’s lows, the income segment should continue to attract investors. Agency MBS yields also offer attractive income compared to Treasurys yet, with prepayment risks now starting to rise as investors tentatively take advantage of the drop in yields, IG credit is more attractive.

Across the credit spectrum, high-quality bonds outperformed low-quality bonds during 4Q mainly due to duration impact. While credit markets currently appear to be inattentive to the risks of an economic downturn, historically, high-quality credit outperforms during even milder economic downturns, with relative total returns favoring U.S. investment grade over high yield issues.

Higher-quality spreads are historically tight, yet fundamentals continue to look robust. In even a mild economic slowdown, higher quality should outperform lower quality credit.

{kind=link}

{kind=link}

High yield: Less attractive valuations, but still resilient

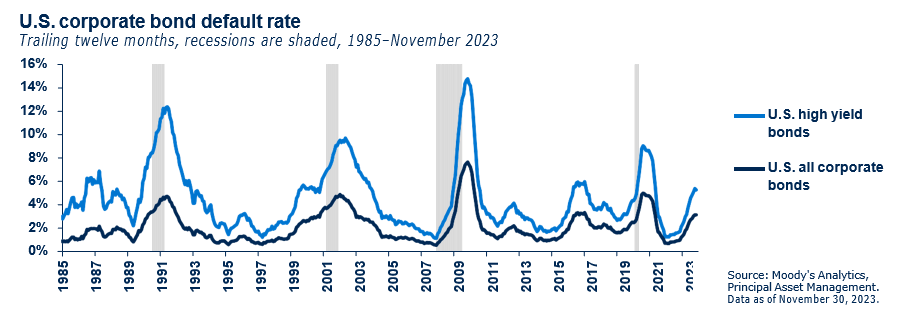

High yield bonds delivered strong returns in 4Q as spreads continued to tighten, closing in on a 21-month low, reflecting economic resilience and growing soft-landing optimism for the U.S. economy. Default rates have continued to rise, yet they have not spiked and are only slightly above their historical average. With only a mild economic slowdown likely in 2024, future defaults could be lower than would be typically expected heading into economic downturns.

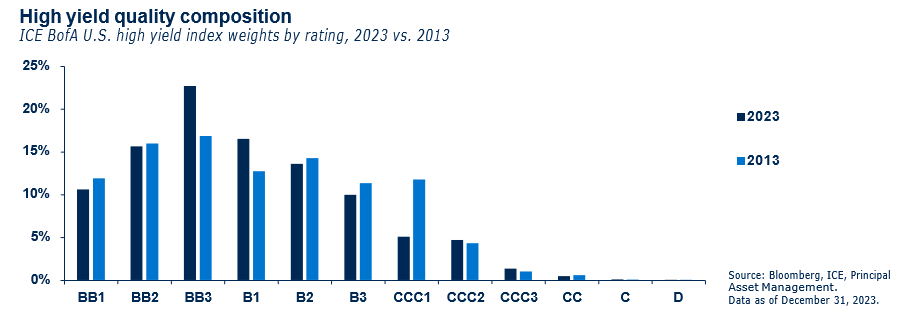

Moreover, the credit quality of the high yield index today is well above historical norms—supportive of favorable recovery rates in the event of defaults.

Yet, risks are growing. Low refinancing pressure helped spread compression in 2023, but those tailwinds are gradually turning into headwinds. High yield bond issuers typically need to refinance one year before their maturities. In the U.S., maturities begin to ramp up in 2Q 2025, implying that issuers will need to refinance by 2Q 2024 or face more credit risk thereafter. As such, refinancing pressure will start to accelerate in the coming months.

Overall, high yield should remain broadly resilient during the upcoming downturn considering their carry advantage and better quality, but the spread tightening trend will likely reverse, denting their total returns.

Stronger high yield credit quality is mitigating the typical risks associated with an approaching economic slowdown, but refinancing pressure will increase from 2Q 2024.

{kind=link}

{kind=link}

EM debt: A robust outlook despite its pro-cyclicality

Given the pro-cyclical nature of emerging market debt ((EMD)), the asset class usually performs poorly during downturns and tighter credit conditions. However, EMD is entering 2024 under-owned, with risks sufficiently priced in and clearly exposed.

Desynchronized economic cycles suggest EMD may weather an expected U.S. slowdown relatively unscathed. The economic story for many EMs is strong, as growth and fiscal balances have held up better than most expectations. The default events and macro stresses have remained mostly confined to countries with unmanageable debt loads or obvious policy credibility issues and, therefore, were well-flagged.

Many EM central banks are already easing monetary policy, thereby creating strong investment opportunities in local currency bonds. Global disinflation, a slowdown in U.S. growth, and a Fed pivot suggest that the U.S. dollar has peaked for this cycle. Yet, while that is supportive for EMD, with most global central banks also set to cut rates this year, rate differentials suggest that any U.S. dollar weakness will be limited.

Risks remain. Investors should continue to watch closely for signs of a deep liquidity crisis, while a resurgence in global inflationary pressures would also significantly challenge EMD.

Emerging market debt should escape a U.S. slowdown mostly unscathed. Faster inflation normalization in EMs is allowing their central banks to start loosening policy interest rates.

{kind=link}

{kind=link}

Commodities: Confronting geopolitics and strong demand

Commodities had a mixed performance in 4Q, with precious metals continuing their upward march while energy prices defied geopolitical tensions to sink lower. Near-term dynamics for commodities are mixed. Precious metals demand should remain robust given that only a mild global economic slowdown is expected.

For energy, the demand prospects are equally positive. Indeed, while the broader market is pricing in a soft landing, the energy market is pricing in a recession, suggesting that a repricing is overdue in the commodity space.

Supply dynamics are more mixed. While the various geopolitical tensions have not broadened out to impact energy, the threat is ever present and suggests some upside risks to oil prices. On the other hand, the unexpected increase in U.S. oil output will likely continue to put downward pressure on oil prices. This makes for an uncertain near-term environment.

The long-term outlook, however, remains more constructive. Global demand for fossil fuels is continuously rising and is unmatched by capital expenditure. This implies that commodities will likely remain in a long-term state of structural supply deficits that will support prices.

While the near-term commodity outlook is unclear, structural supply deficits mean that long-term trends are clearer and more constructive.

{kind=link}

{kind=link}

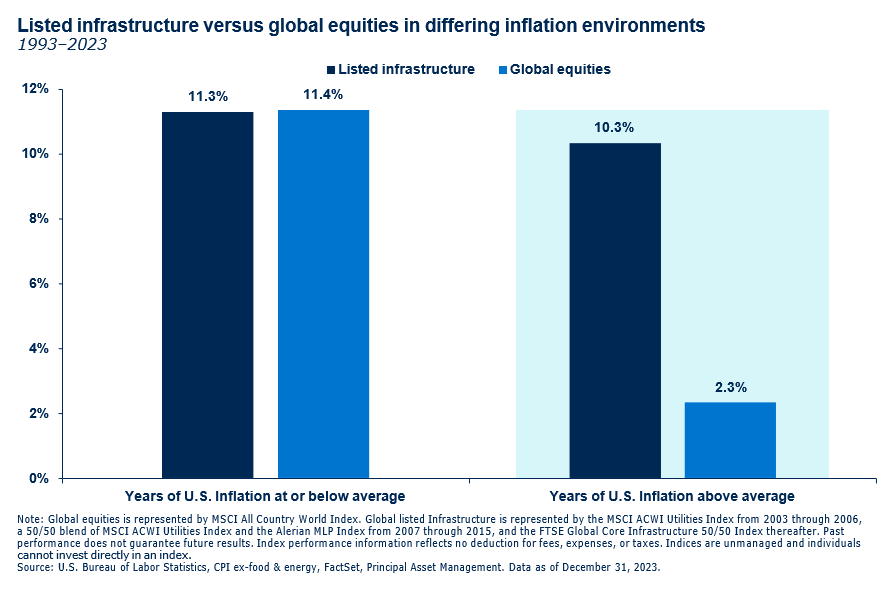

Infrastructure: Down but not out

Defensive stocks have borne the brunt of market fears over higher-for-longer rates in 2023, and listed infrastructure has been no exception. Infrastructure now screens at historically cheap levels versus global equities.

Typically, the most opportune environment for infrastructure is when inflation is sticky and rising. By contrast, infrastructure may struggle if inflation continues to soften. While this implies that infrastructure is unlikely to perform as strongly as in recent years, from a relative perspective and considering that the economy is likely to slow in 2024, infrastructure’s equity beta and the companies’ resilient fundamentals suggest that infrastructure may perform broadly in line with global equities, thereby deserving a neutral position. Furthermore, an inflation resurgence is a continued threat, and, as a result, infrastructure’s inflation mitigation properties are still required in a portfolio.

In addition, infrastructure investments can offer more

stability within a well-diversified portfolio, typically having predictable cash flows associated with the long-lived assets. They also provide exposure to the global theme of de- carbonization, which presents a multi-decade tailwind for utilities and renewable infrastructure companies.

While the economic backdrop is no longer as constructive for infrastructure, its predictable cash flows will be important.

{kind=link}

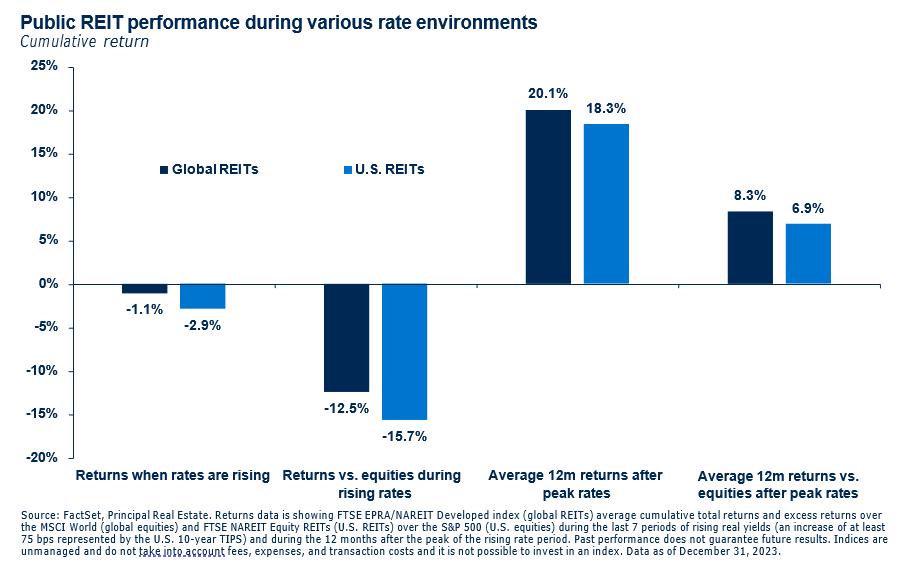

REITs: Attractive valuations and fundamentals collide

After facing significant headwinds for the past two years, REITs are once again a compelling investment proposition. Historically, the peak in long-term real yields is the catalyst for REITs market outperformance and this cycle is proving no different, with the significant bond market rally in 4Q opening the door for meaningful gains for global REITs. These gains should extend into 2024.

Notably, the valuations of public REITs have corrected sharply since the Fed rate hike cycle started, and look attractive compared to broader equity markets.

Fundamentals are also looking more constructive. When macro conditions become more challenging, REITS are often beneficiaries of investor rotation into risk assets that feature long-duration, quality, and durable cash flows. With the global economy likely to slow somewhat in 2024, these defensive characteristics should drive strong REITs performance.

Office REITs remain the weak spot. Yet, investors should note that traditional office space accounts for only 3% of the overall U.S. REIT market and 6% of the global market. As such, office exposure itself should not deter investors.

REITs have been challenged over the past two years and are now deeply discounted. With real yields having peaked, we shift to an overweight.

{kind=link}

Diversified asset allocation: Sticking to neutral but with shifts below the surface

Source: Principal Asset Allocation. Alternatives asset class include commodities, natural resources, infrastructure, REITs, and hedge funds. Allocations across the investment outlook can be proportionately adjusted so magnitudes across categories do not have to net to neutral.

Data as of December 31, 2023

Equities:

Our equities positioning remains at neutral. Rich equity valuations are likely to be challenged in early 2024 as elevated earnings growth expectations are tested by slowing consumer demand and margin pressure. However, in acknowledgement of the improved U.S. outlook and strong potential for rate cuts, we shift U.S. equities to overweight. Within U.S. equities, attractive small-cap valuations and potential for improving growth in 2Q prompt an upgrade to neutral. Our exposure to ex-U.S. developed markets remains at an underweight, weighed down by worries about European growth as well as concerns that a rapidly appreciating yen could hurt earnings and trigger profit taking. We move our EM position to neutral, concerned about China’s outlook, but also with tilts towards Latin America as both valuations and fundamentals are attractive.

Fixed income:

Our fixed income positioning also remains at neutral. After a strong 4Q, Treasury yields are likely to remain volatile in 1Q and may even see some upward pressure if rate cut expectations prove optimistic. Within credit, we keep our core bonds position at a slight overweight. Investment grade spreads are narrow, but they are supported by resilient economic growth and subdued default risk. High yield remains at neutral but could be pressured by rising default risks. Local currency emerging market debt remains at an overweight as central bank rate cuts should enhance returns—but we acknowledge that the U.S. dollar is unlikely to provide much of a tailwind, while a deeper than expected U.S. downturn would hurt the outlook.

Alternatives:

Alternatives remain at a neutral weighting. Commodities and natural resources remain at neutral given the contrasting impacts from geopolitical risk and increased U.S. oil supply. Infrastructure remains at neutral given the more resilient economic backdrop and continued disinflation trend, while it should benefit from its equity beta. REITs valuations have improved significantly and, with real yields having peaked, there is a strong case for a REITs overweight. Hedge funds shift to overweight, as higher correlations coupled with expected high volatility presents a favorable environment for hedge fund strategies.

Equities

Reduce risk appetite and focus on U.S. large-cap and quality factor.

Position toward certainty:

- Exposure to quality within equities can potentially offer risk mitigation during pullbacks.

- Attractive international valuations suggest opportunities outside the U.S.

- Favorable valuations in U.S. small-cap and mid-cap stocks.

- Position for potential equity market rallies in latter 2024 after Fed pivot.

How to implement:

- Large-cap U.S. strategies

- Well-diversified and active international managers

- Quality-biased active managers

- Active mid- and small-cap strategies

Fixed income

Increase exposure to high-quality credit.

High-quality, core fixed income and total return positioning:

- Core fixed income to hide out in during a mild slowdown.

- Increasing duration bias across the asset class.

- Emerging market debt may offer total return potential with central bank easing.

- High yield maintains a substantial carry advantage for income-seeking investors.

How to implement:

- IG credit heavy core fixed income

- Agency MBS strategies

- Flexible emerging market debt strategies

- Active high yield strategies

Alternatives

Pursue less correlated real asset exposures.

Real assets:

- Real return-focused strategies gain attractiveness when nominal growth slows.

- Infrastructure offers resiliency, inflation mitigation, and attractive valuations.

- A mild slowdown should keep demand elevated broadly.

- REITs offer attractive valuations and constructive fundamentals.

How to implement:

- Diversified real asset strategies (infrastructure, natural resources)

- Private real estate markets

- Proven REIT strategies

Index Descriptions

Bloomberg Commodity Total Return index is composed of futures contracts and reflects the returns on a fully collateralized investment in the BCOM. This combines the returns of the BCOM with the returns on cash collateral invested in 13 week (3 Month) U.S. Treasury Bills.

Bloomberg Global Aggregate Bond Index comprises global investment grade debt including treasuries, government-related, corporate, and securitized fixed-rate bonds from developed and emerging market issuers. There are four regional aggregate benchmarks that largely comprise the Global Aggregate Index: the US Aggregate, the Pan-European Aggregate, the Asian-Pacific Aggregate, and the Canadian Aggregate Indices. The Index also includes Eurodollar, Euro-Yen, and 144A Index-eligible securities and debt from other local currency markets not tracked by regional aggregate benchmarks

Bloomberg U.S. Agency Bond Index is composed of agency securities that are publicly issued by U.S. government agencies, and corporate and non-U.S. debt guaranteed by the U.S. government. Bloomberg U.S. Aggregate Bond Index is the most widely followed broad market U.S. bond index. It measures the investment grade, US dollar-denominated, fixed-rate taxable bond market.

Bloomberg U.S. High-Yield Corporate Bond Index is a rules-based, market-value-weighted index engineered to measure publicly issued non-investment grade USD fixed-rate, taxable and corporate bonds.

Bloomberg U.S. Corp High Yield 2% Issuer Capped Index is an unmanaged index comprised of fixed rate, non-investment grade debt securities that are dollar denominated. The index limits the maximum exposure to any one issuer to 2%.

Bloomberg U.S. Corporate Investment Grade Index includes publicly issued U.S. corporate and specified foreign debentures and secured notes that meet the specified maturity, liquidity and quality requirements. To qualify, bonds must be SEC-registered. The corporate sectors are industrial, utility and finance, which include both U.S. and non-U.S. corporations.

Bloomberg U.S. Treasury Index measures U.S. dollar-denominated, fixed-rate, nominal debt issued by the U.S. Treasury. Treasury bills are excluded by the maturity constraint. STRIPS are excluded from the index because their inclusion would result in double-counting.

FTSE Global Core Infrastructure 50/50 Total Return Index comprises securities in developed countries which provide exposure to core infrastructure businesses, namely transportation, energy and telecommunications, as defined by FTSE's International Benchmark Classification.

The FTSE Nareit All Equity REITs Index is a free-float adjusted, market capitalization-weighted index of U.S. equity REITs.

HFRI 500 Fund Weighted Composite Index is a global, equal-weighted index of the largest hedge funds that report to the HFR Database which are open to new investments and offer quarterly liquidity or better.

ICE BofA Emerging Markets Corporate Plus Index, which tracks the performance of US dollar ((USD)) and Euro denominated emerging markets non-sovereign debt publicly issued within the major domestic and Eurobond markets. ICE BofA MOVE index, or Merrill Lynch Option Volatility Estimate Index, is a crucial gauge of interest rate volatility in the U.S. Treasury market.

ICE BofA U.S. High Yield Index tracks the performance of US dollar denominated below investment grade rated corporate debt publicly issued in the US domestic market.

ICE BofA U.S. Investment Grade Institutional Capital Securities Index tracks the performance of US dollar denominated investment grade hybrid capital corporate and preferred securities publicly issued in the US domestic market. ICE BofA U.S. Corporate Index consists of investment-grade corporate bonds that have a remaining maturity of greater than or equal to one year and have $250 million or more of outstanding face value.

J.P. Morgan Emerging Markets Bond Index Global Core tracks liquid, U.S. dollar emerging market fixed and floating-rate debt instruments issued by sovereign and quasi sovereign entities. ISM manufacturing index is a leading economic indicator that measures the growth in the manufacturing sector in the United States.

MSCI ACWI Index includes large and mid cap stocks across developed and emerging market countries.

MSCI ACWI Utilities Index captures large and mid cap representation across 23 Developed Markets ((DM)) and 24 Emerging Markets ((EM)) countries*. All securities in the index are classified in the Utilities sector as per the Global Industry Classification Standard (GICS®).

Market indices have been provided for comparison purposes only. They are unmanaged and do not reflect any fees or expenses.

Individuals cannot invest directly in an index.

MSCI Brazil Index is designed to measure the performance of the large and mid cap segments of the Brazilian market.

MSCI China Index captures large and mid cap representation across China A shares, H shares, B shares, Red chips, P chips and foreign listings (e.g. ADRs).

MSCI EAFE Index is listed for foreign stock funds (EAFE refers to Europe, Australasia, and Far East). Widely accepted as a benchmark for international stock performance, the EAFE Index is an aggregate of 21 individual country indexes.

MSCI Emerging Markets Index consists of large and mid cap companies across 24 countries and represents 10% of the world market capitalization. The index covers approximately 85% of the free float-adjusted market capitalization in each country in each of the 24 countries.

MSCI Europe Index captures large and mid cap representation across 15 Developed Markets ((DM)) countries in Europe.

MSCI Europe Banks Index is composed of large and mid cap stocks across 15 Developed Markets countries in Europe. All securities in the index are classified in the Banks industry group (within the Financials sector) according to the Global Industry Classification Standard (GICS®).

MSCI Germany Index is designed to measure the performance of the large and mid cap segments of the German market. MSCI India Index is designed to measure the performance of the large and mid cap segments of the Indian market.

MSCI Japan Index is designed to measure the performance of the large and mid cap segments of the Japanese market. MSCI United Kingdom Index is designed to measure the performance of the large and mid cap segments of the UK market.

MSCI USA Growth Index captures large and mid cap securities exhibiting overall growth style characteristics in the U.S. The growth investment style characteristics for index construction are defined using five variables: long-term forward EPS growth rate, short-term forward EPS growth rate, current internal growth rate and long-term historical EPS growth trend and long-term historical sales per share growth trend.

MSCI USA Index is a market capitalization weighted index designed to measure the performance of equity securities in the top 85% by market capitalization of equity securities listed on stock exchanges in the United States. MSCI USA Large Cap Index is designed to measure the performance of the large cap segments of the U.S. market.

MSCI USA Mid Cap Index is designed to measure the performance of the mid cap segments of the U.S. market.

MSCI USA Quality Index aims to capture the performance of quality growth stocks by identifying stocks with high quality scores based on three main fundamental variables: high return on equity ((ROE)), stable year-over-year earnings growth and low financial leverage. The MSCI Quality Indexes complement existing MSCI Factor Indexes and can provide an effective diversification role in a portfolio of factor strategies.

MSCI USA Small Cap Index is designed to measure the performance of the small cap segment of the U.S. equity market.

MSCI USA Value Index captures large and mid cap U.S. securities exhibiting overall value style characteristics. The value investment style characteristics for index construction are defined using three variables: book value to price, 12-month forward earnings to price and dividend yield.

Russell 2000 Index is a small-cap U.S. stock market index that makes up the smallest 2,000 stocks in the Russell 3000 Index.

Standard & Poor's 500 Index is a market capitalization-weighted index of 500 widely held stocks often used as a proxy for the stock market.

U.S. dollar index (USDX) is a measure of the value of the U.S. dollar relative to a basket of foreign currencies.

Market indices have been provided for comparison purposes only. They are unmanaged and do not reflect any fees or expenses. Individuals cannot invest directly in an index.

For Public Distribution in the United States.

For Institutional, Professional, Qualified and/or Wholesale Investor Use Only in other Permitted Jurisdictions as defined by local laws and regulations.

Risk considerations

Important Information

Investing involves risk, including possible loss of principal. Past performance is no guarantee of future results. Asset allocation and diversification do not ensure a profit or protect against a loss. Equity investments involve greater risk, including higher volatility, than fixed-income investments. Fixed-income investments are subject to interest rate risk; as interest rates rise their value will decline. International and global investing involves greater risks such as currency fluctuations, political/social instability and differing accounting standards. Potential investors should be aware of the risks inherent to owning and investing in real estate, including value fluctuations, capital market pricing volatility, liquidity risks, leverage, credit risk, occupancy risk and legal risk. Non-investment grade securities offer a potentially higher yield but carry a greater degree of risk. Risks of preferred securities differ from risks inherent in other investments. In particular, in a bankruptcy preferred securities are senior to common stock but subordinate to other corporate debt. Emerging market debt may be subject to heightened default and liquidity risk. Risk is magnified in emerging markets, which may lack established legal, political, business, or social structures to support securities markets. Small and mid-cap stocks may have additional risks including greater price volatility. Treasury inflation-protected securities ((TIPS)) are a type of Treasury security issued by the

U.S. government. TIPS are indexed to inflation in order to help investors from a decline in the purchasing power of their money. As inflation rises, rather than their yield increasing, TIPS instead adjust in price (principal amount) in order to maintain their real value. Inflation and other economic cycles and conditions are difficult to predict and there Is no guarantee that any inflation mitigation/protection strategy will be successful. Contingent Capitals Securities may have substantially greater risk than other securities in times of financial stress. An issuer or regulator’s decision to write down, write off or convert a CoCo may result in complete loss on an investment. Real assets include but not limited to precious metals, commodities, real estate, land, equipment, infrastructure, and natural resources. Each real asset is subject to its own unique investment risk and should be independently evaluated before investing. As an asset class, real assets are less developed, more illiquid, and less transparent compared to traditional asset classes.

Important Information

This material covers general information only and does not take account of any investor’s investment objectives or financial situation and should not be construed as specific investment advice, a recommendation, or be relied on in any way as a guarantee, promise, forecast or prediction of future events regarding an investment or the markets in general. The opinions and predictions expressed are subject to change without prior notice. The information presented has been derived from sources believed to be accurate; however, we do not independently verify or guarantee its accuracy or validity. Any reference to a specific investment or security does not constitute a recommendation to buy, sell, or hold such investment or security, nor an indication that the investment manager or its affiliates has recommended a specific security for any client account. Subject to any contrary provisions of applicable law, the investment manager and its affiliates, and their officers, directors, employees, agents, disclaim any express or implied warranty of reliability or accuracy and any responsibility arising in any way (including by reason of negligence) for errors or omissions in the information or data provided.

This material may contain ‘forward-looking’ information that is not purely historical in nature and may include, among other things, projections and forecasts. There is no guarantee that any forecasts made will come to pass. Reliance upon information in this material is at the sole discretion of the reader.

This material is not intended for distribution to or use by any person or entity in any jurisdiction or country where such distribution or use would be contrary to local law or regulation.

This document is intended for use in:

- The United States by Principal Global Investors, LLC, which is regulated by the U.S. Securities and Exchange Commission.

- Europe by Principal Global Investors (Ireland) Limited, 70 Sir John Rogerson’s Quay, Dublin 2, D02 R296, Ireland. Principal Global Investors (Ireland) Limited is regulated by the Central Bank of Ireland. Clients that do not directly contract with Principal Global Investors (Europe) Limited ("PGIE") or Principal Global Investors (Ireland) Limited (“PGII”) will not benefit from the protections offered by the rules and regulations of the Financial Conduct Authority or the Central Bank of Ireland, including those enacted under MiFID II. Further, where clients do contract with PGIE or PGII, PGIE or PGII may delegate management authority to affiliates that are not authorised and regulated within Europe and in any such case, the client may not benefit from all protections offered by the rules and regulations of the Financial Conduct Authority, or the Central Bank of Ireland. In Europe, this document is directed exclusively at Professional Clients and Eligible Counterparties and should not be relied upon by Retail Clients (all as defined by the MiFID).

- United Kingdom by Principal Global Investors (Europe) Limited, Level 1, 1 Wood Street, London, EC2V 7 JB, registered in England, No. 03819986, which is authorized and regulated by the Financial Conduct Authority ("FCA").

- United Arab Emirates by Principal Global Investors LLC, a branch registered in the Dubai International Financial Centre and authorized by the Dubai Financial Services Authority as a representative office and is delivered on an individual basis to the recipient and should not be passed on or otherwise distributed by the recipient to any other person or organization.

- Singapore by Principal Global Investors (Singapore)Limited (ACRA Reg. No. 199603735H), which is regulated by the Monetary Authority of Singapore and is directed exclusively at institutional investors as defined by the Securities and Futures Act 2001. This advertisement or publication has not been reviewed by the Monetary Authority of Singapore.

- Australia by Principal Global Investors (Australia) Limited (ABN 45 102 488 068, AFS Licence No. 225385), which is regulated by the Australian Securities and Investments Commission and is only directed at wholesale clients as defined under Corporations Act 2001.

- This document is marketing material and is issued in Switzerland by Principal Global Investors (Switzerland) GmbH.

- Hong Kong SAR (China ) by Principal Asset Management Company ((ASIA)) Limited, which is regulated by the Securities and Futures Commission. This document has not been reviewed by the Securities and Futures Commission.

- Other APAC Countries/Jurisdictions , this material is issued for institutional investors only (or professional/sophisticated/qualified investors, as such term may apply in local jurisdictions) and is delivered on an individual basis to the recipient and should not be passed on, used by any person or entity in any jurisdiction or country where such distribution or use would be contrary to local law or regulation.

- Nothing in this document is, and shall not be considered as, an offer of financial products or services in Brazil. This presentation has been prepared for informational purposes only and is intended only for the designated recipients hereof. Principal Global Investors is not a Brazilian financial institution and is not licensed to and does not operate as a financial institution in Brazil.

Insurance products and plan administrative services provided through Principal Life Insurance Co. Principal Funds, Inc. is distributed by Principal Funds Distributor, Inc. Securities are offered through Principal Securities, Inc., 800 547-7754, Member SIPC and/or independent broker/dealers. Principal Life, Principal Funds Distributor, Inc., and Principal Securities are members of the Principal Financial Group®, Des Moines, IA50392.

© 2024, Principal Financial Services, Inc. Principal Asset ManagementSM is a trade name of Principal Global Investors, LLC. Principal®, Principal Financial Group®, Principal Asset Management, and Principal and the logomark design are registered trademarks and service marks of Principal Financial Services, Inc., a Principal Financial Group company, in various countries around the world and may be used only with the permission of Principal Financial Services, Inc.

For further details see:

Global Asset Allocation Viewpoints, Q1 2024 - Gentle Slope, Not Cliff Edge