ESGB - Global Asset Allocation Viewpoints Q2 2023: Navigating Increasingly Unstable Markets

2023-04-21 08:20:00 ET

Summary

- While U.S. growth has remained strong, even accelerating in early 1Q, leading indicators continue to signal recession. Tighter lending standards, as a result of the recent banking crisis, only increase the risk of a hard landing.

- Part of the inflation basket will soften rapidly in response to normalizing supply chains and energy prices, but other key segments still require considerable weakening in labor markets if there is any hope of approaching target.

- Each additional interest rate hike increases the risk of further market turmoil. Central bank policy rates will likely peak soon, but rate cuts are unlikely unless there is a severe and dangerous spike in financial system stress.

- While 2022 dynamics were driven by inflation and rates scares, 2023 is likely to be dominated by earnings and economic growth scares. Margin pressures will weigh on company profitability, leading equities lower.

Key themes for 2Q 2023

- Global economic growth has surprised to the upside, but U.S. recession risk is rising. Although U.S. growth has remained strong, even accelerating in early 1Q, leading indicators continue to signal recession. Tighter lending standards, as a result of the recent banking crisis, only increase the risk of a hard landing.

- Price pressures remain too elevated; in most economies, inflation will end the year above target. Part of the inflation basket will soften rapidly in response to normalizing supply chains and energy prices, but other key segments still require considerable weakening in labor markets if there is any hope of approaching target.

- Central banks are nearing the end of their tightening cycles as financial stability risks increase. Each additional interest rate hike increases the risk of further market turmoil. Central bank policy rates will likely peak soon, but rate cuts are unlikely unless there is a severe and dangerous spike in financial system stress.

- Although equities have been resilient, earnings weakness will threaten further drawdown. While 2022 dynamics were driven by inflation and rates scares, 2023 is likely to be dominated by earnings and economic growth scares. Margin pressures will weigh on company profitability, leading equities lower.

- High-quality fixed income offers stability and income in this challenging economic backdrop. Central banks are likely nearing the completion of their tightening cycle, implying that bonds will be able to support portfolios both as recession approaches and during forthcoming periods of volatility and risk.

- Alternatives provide important diversification against traditional equities and fixed income. While inflation is decelerating, it remains uncomfortably high, so portfolios still require allocations to real assets to mitigate inflation risks. Assets that perform well in elevated volatility environments should also be prized.

Investment themes

Price stability vs. financial stability

The recent U.S. banking failures and collapse of a major European bank have finally underscored the tensions between central banks’ efforts to tame inflation and growing concerns that further policy tightening will spark a crisis. With inflation still elevated but markets increasingly alert to the vulnerabilities within the financial system, central banks face a difficult balancing act - continue to target price stability or focus on maintaining financial stability?

The risk of central bank-driven financial stress, resulting in bank deposit outflows, rising bank funding costs, and sharp retrenching of lending, has raised the odds of a hard landing. Yet, if financial stress fears prompt central banks to end their tightening cycles prematurely, there will be higher risk of an inflation resurgence and even more aggressive rate hikes later down the line, also raising the odds of a hard landing.

Ultimately, financial conditions will tighten further - either via additional central bank tightening as they try to tame inflation, or via tightening credit conditions.

Lower returns, elevated volatility

The reversal in ultra-loose global central bank policy has led to an almost unrecognizable global investment landscape. Unlike the golden era of the past decade where low inflation and low interest rates were suppressing volatility and lifting asset prices, the higher interest rate environment is now uncovering market strains and raising volatility.

Investor behavior will need to adjust: expectations for returns need to be lowered and expectations for volatility need to be raised. Portfolios need to reallocate risk to both take advantage of market inefficiencies and to minimize exposure to macro-driven threats.

Diversification and quality

Unlike 2022, where stocks and bonds fell together, opportunities are already proving more forthcoming in 2023. While tightening in financial conditions and the likely resulting U.S. recession will weigh on the broad equity market outlook, the relatively attractive valuations outside the U.S. suggest investors stand to gain through global diversification.

Fixed income’s diversification potential has also been restored. With many central banks nearing the completion of their tightening cycles, bonds will likely be able to support portfolios, providing income and greater stability during periods of volatility and risk.

Finally, with price pressures only easing very slowly, inflation mitigation via real assets remains a key part of the playbook.

Consider the potential risks

Financial instability: The drastic rise in rates risks severe liquidity disruption. Violent, sudden price moves in one market can provoke a vicious loop of margin calls and forced sales of other assets, with unpredictable results. Markets have so far navigated the rate increases and banking crisis without too much disruption, but there is no guarantee that the remainder of 2023 will be as straightforward.

Price instability: While the market appears to agree that inflation will fade this year, history suggests that there is a risk the meaningful inflation decline may not materialize. In such an event, after a short pause, the Federal Reserve (Fed) and other central banks may need to resume policy hikes. Not only would that deliver additional headwinds to growth, but also add to financial instability risk.

Global growth: Here today, gone tomorrow?

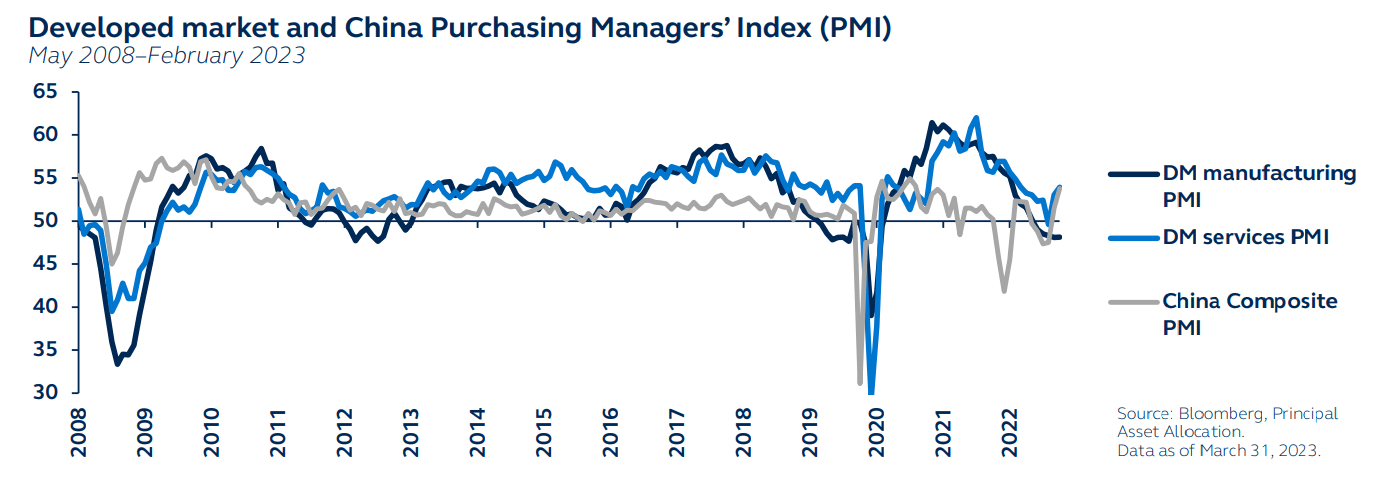

Global economic activity has continued to defy policy tightening and the multiple geopolitical shocks. Softness in economic data in late 2022 proved to be seasonal noise and, in fact, since the start of 2023, activity data has only emphasized the continued resilience of the global economy.

The stabilization in global manufacturing activity can be at least partially traced back to the reopening bounce in China, while the sharp drop in energy prices has given global consumers a boost. Historically tight labor markets are also contributing significantly to the broad economic strength across global regions.

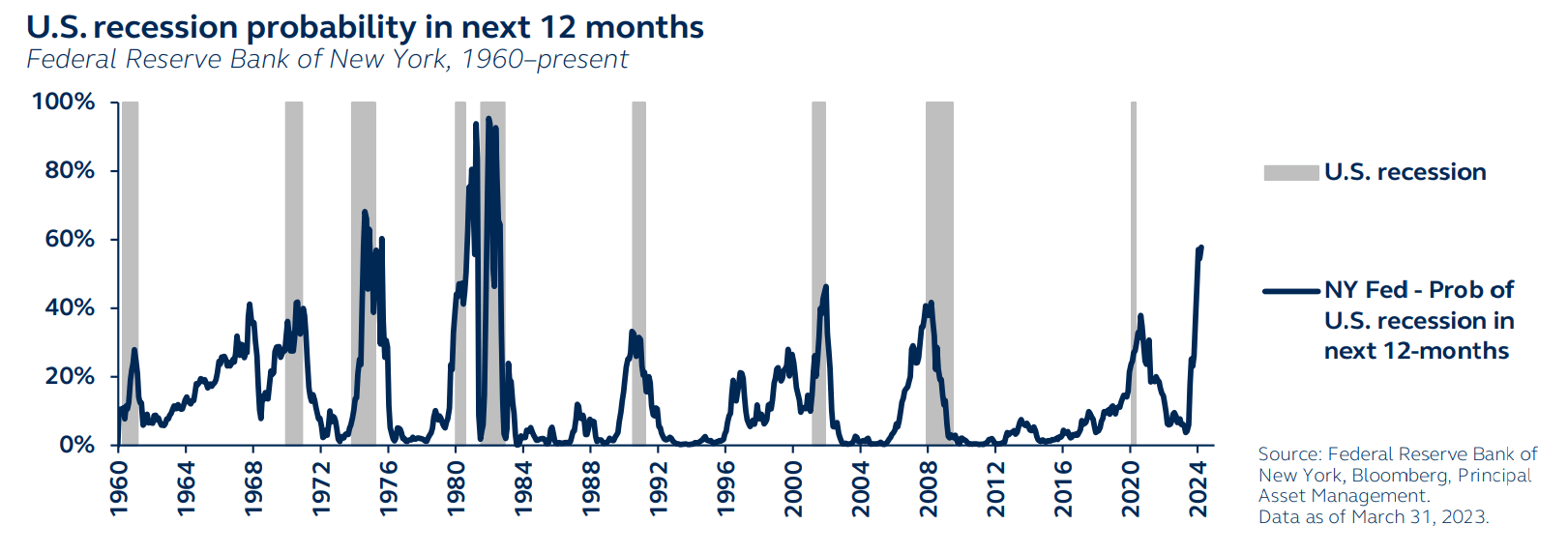

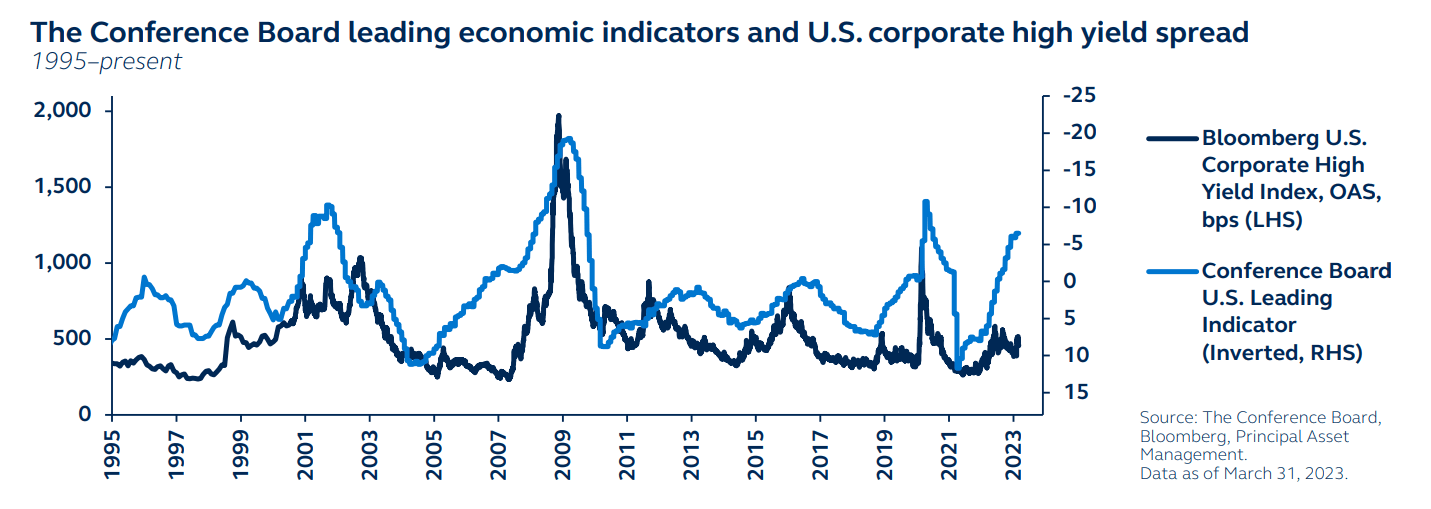

And yet, even as the global economy looks strong, leading indicators emphatically signal recession. The New York Fed’s own recession model suggests that the probability of recession within the next 12 months is the highest since the early 1980s. The Treasury yield curve remains deeply inverted - a historically reliable recession indicator. Not only is the 2s10s curve inversion material and sustained, but other segments of the yield curve are also inverted, including the 3-month 1-year curve, which is typically consistent with recession risk within a 12-month period.

While current economic conditions are supportive of above-trend growth, leading indicators are signaling elevated risks of recession later this year.

{kind=link}

{kind=link}

Strength at the top, problems at the bottom

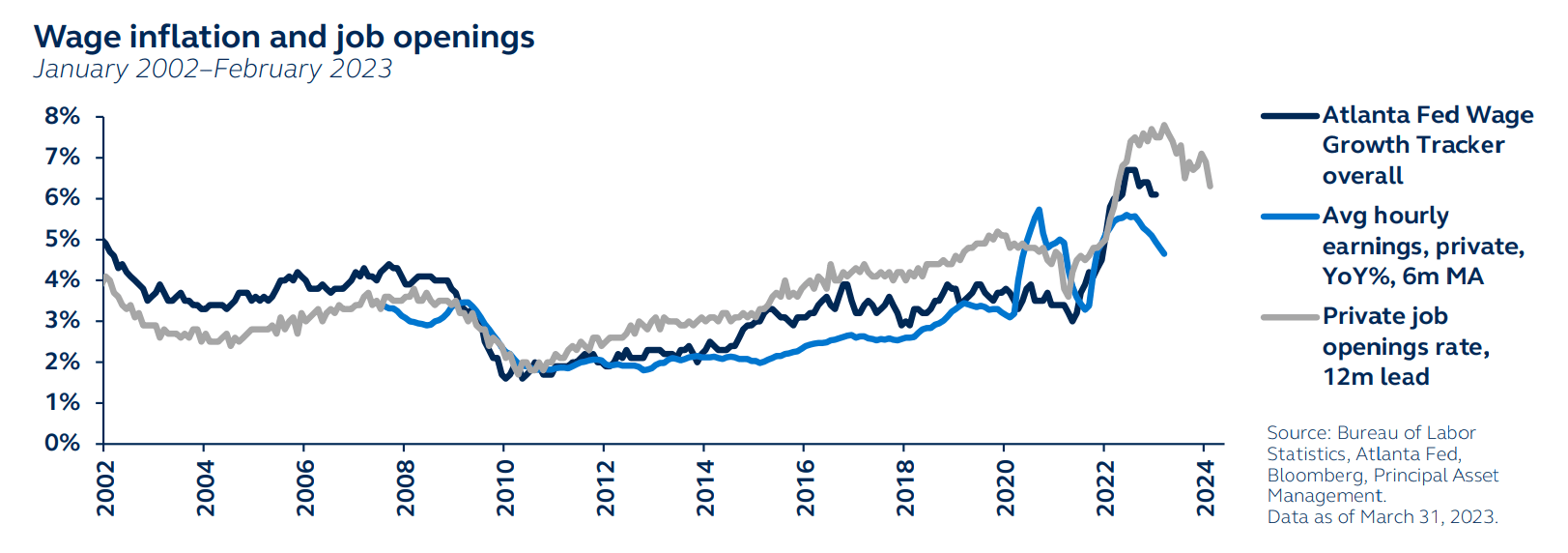

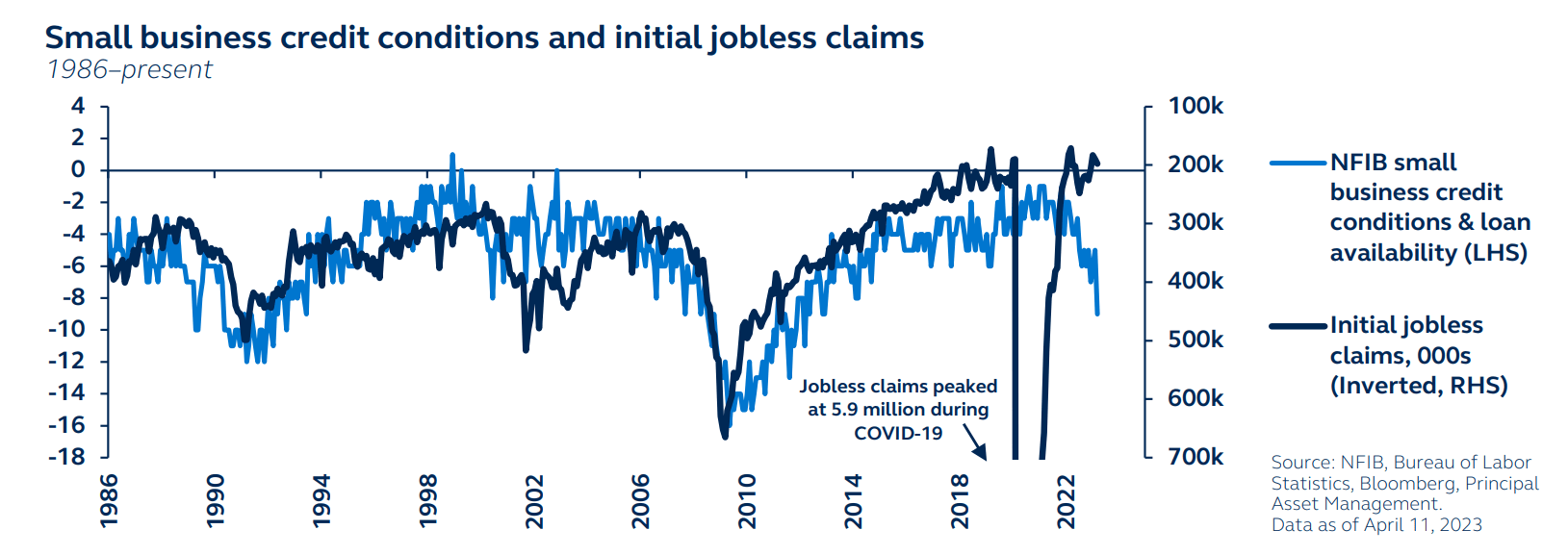

Leading indicators are picking up on concerning developments in the underlying economic data. The cushion of excess savings that has been supporting consumer activity is steadily being depleted. While credit could support consumption, banks have been trimming their lines of credit to households. At the same time, consumers themselves are pulling back - with demand for consumer loans weakening.

Labor markets remain very strong, and the U.S. unemployment rate sits close to 50-year lows. With nearly two job vacancies per unemployed worker, employers report considerable difficulties in filling available positions, maintaining upward pressure on wage growth. Robust jobs and wage growth have been key tailwinds for consumers.

However, recent turmoil in the banking sector suggests the labor market strength will prove short-lived. Small banks account for 30% of all loans in the U.S. economy. They will likely spend several quarters repairing their balance sheets, implying tighter lending standards for both firms and households. This will likely lead to greater job losses, fading wage growth, weaker consumer spending, and ultimately, a higher likelihood of recession.

As small and medium-sized banks respond to recent stress by reducing lending activity, consumers will be under pressure and job losses will likely increase.

{kind=link}

{kind=link}

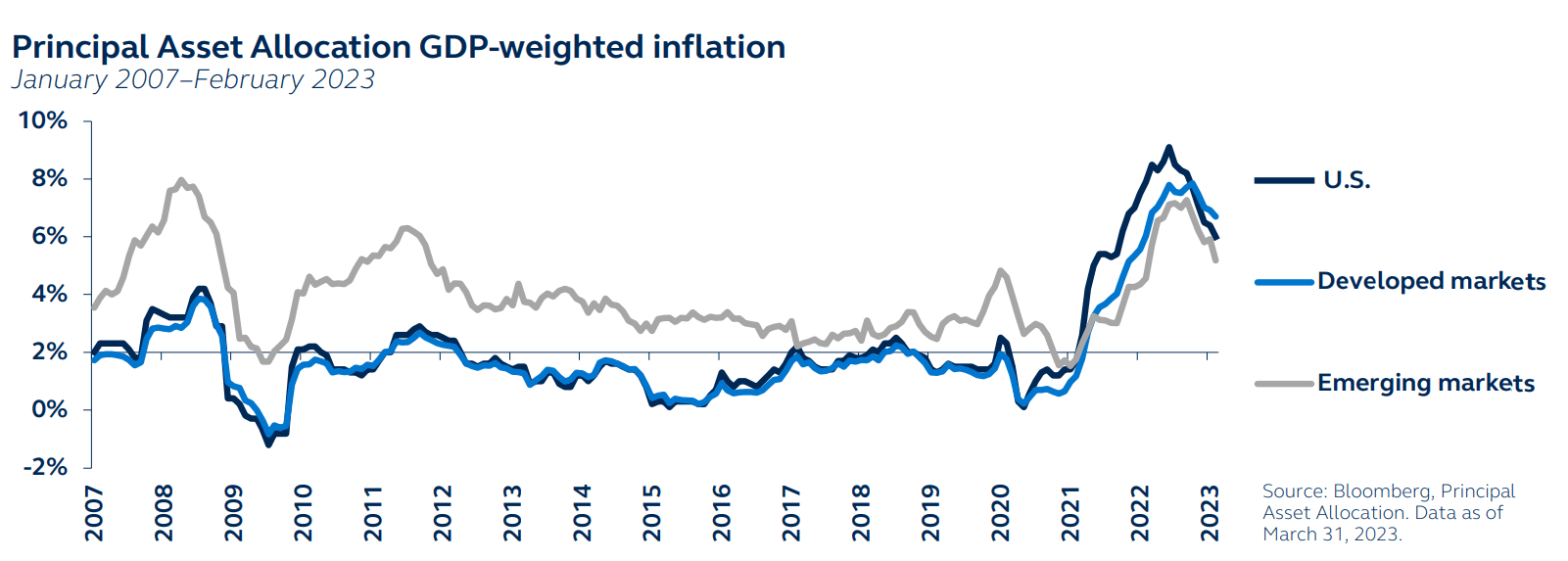

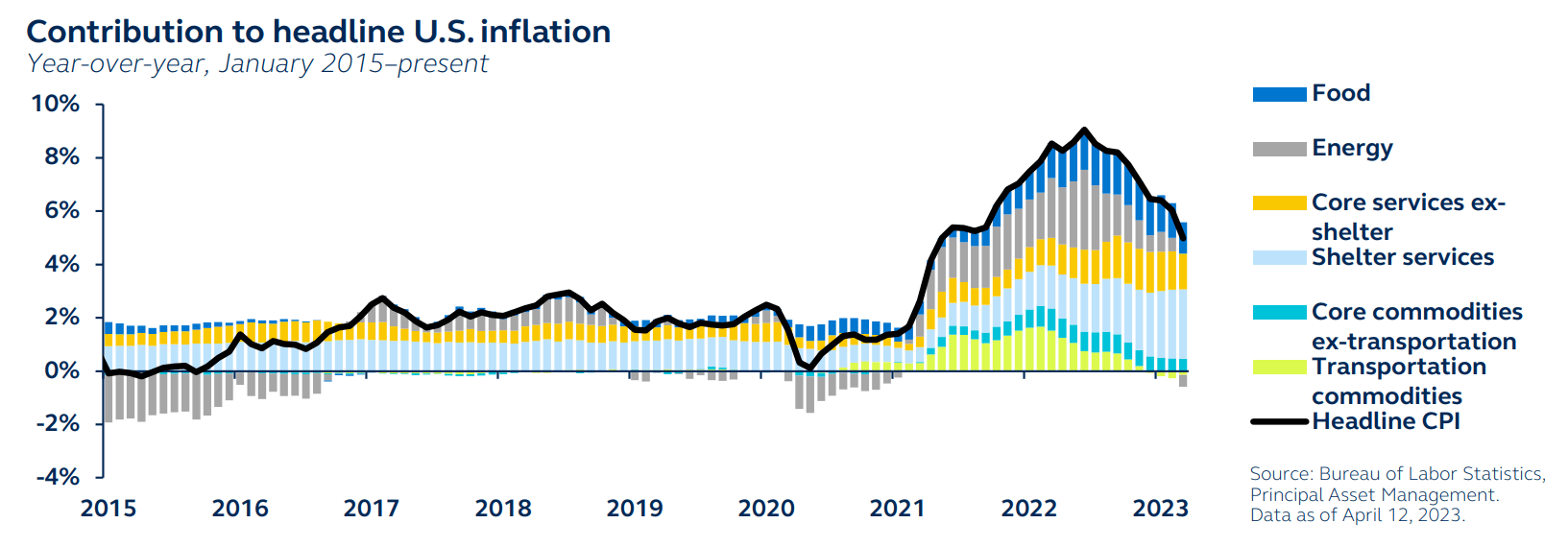

An incomplete disinflationary trend

Global inflation is moderating, but so far this deceleration has been largely driven by last year’s energy price spike unwind. Core inflation remains uncomfortably high and, in some economies, continues to rise. The broad inflation takeaway from 1Q is that global central banks have made less progress towards disinflation than they had hoped.

In the U.S., inflation is expected to decelerate further through the year, but only very slowly.

- Core goods inflation should decline as supply chains fully normalize, but has hit some road bumps recently.

- Shelter inflation will slow, but this deceleration may take longer to materialize if the economy remains resilient.

- Core services ex-housing, which Fed Chair Jerome Powell has drawn clear attention to, is closely related to wage growth. Slower economic activity and a looser labor market will be necessary to fade these pressures.

With recession likely starting in late 2023, inflation will slow but remain above central bank targets, complicating policy decisions. Indeed, while the focus on price stability may argue for additional monetary tightening, it could also result in further financial instability.

Central banks have made less progress towards disinflation than they had hoped. Inflation is likely to remain sticky and will still sit above central bank targets at year-end.

{kind=link}

{kind=link}

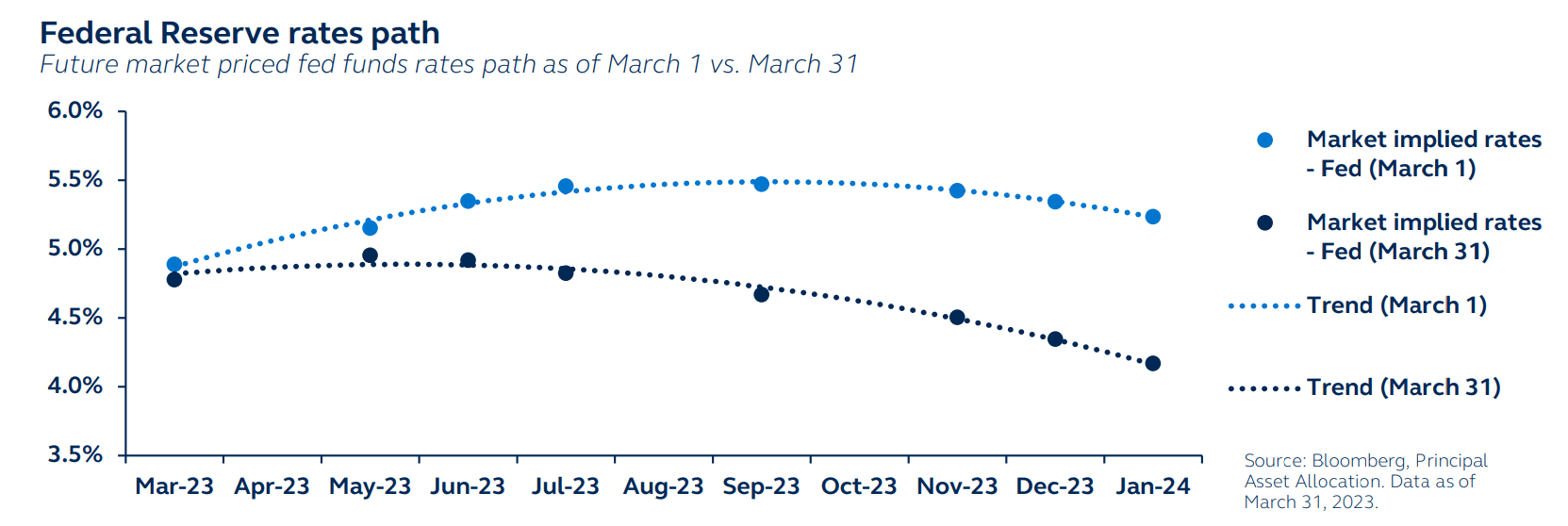

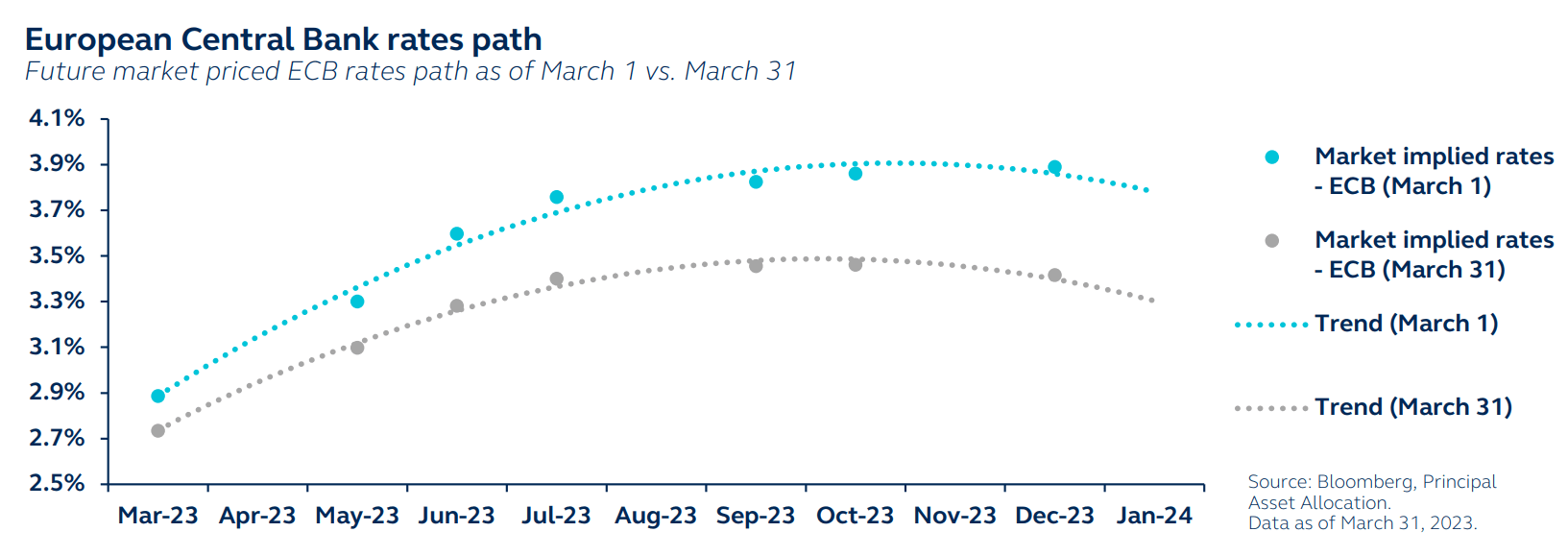

Central bank dilemma: Price stability vs. financial stability

Despite significant rate hikes to date, central bank tightening is yet to have its desired impact on inflation. In recognition of this, market expectations for Fed funds rates in early March were edging towards a 6% terminal rate for the Fed and no rate cuts through 2023. The European Central Bank (ECB) was expected to hike a further 100 bps through this year.

However, with recent bank failures sending the financial sector into disarray and emphasizing the need for central banks to put extra focus on the financial stability side of their mandates, rate expectations have fallen back significantly. Markets now expect no further Fed or ECB hikes, plus three Fed rate cuts this year.

Our Fed forecasts see a peak rate of 5.25-5.50% as the central bank continues to use its policy rate to target inflation, while using its balance sheet liquidity to target financial stability.

Both the timing and rate path to reach these outcomes are unclear. Not only is it difficult to estimate how much further banking stresses will extend, the extent of tightening in bank lending standards that will result from recent banking sector stress is also uncertain. These factors will be very important for determining the policy rate path.

Although central banks need to stay focused on fighting inflation, financial instability concerns could result in a lower policy rate path.

{kind=link}

{kind=link}

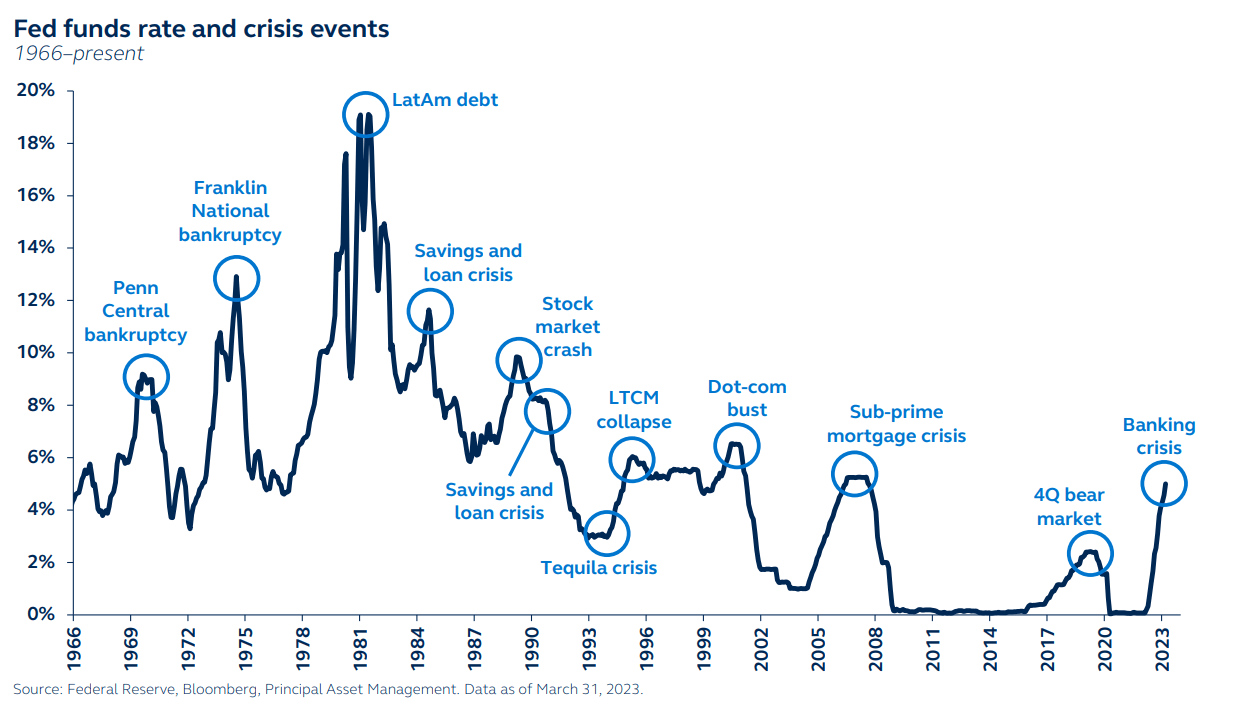

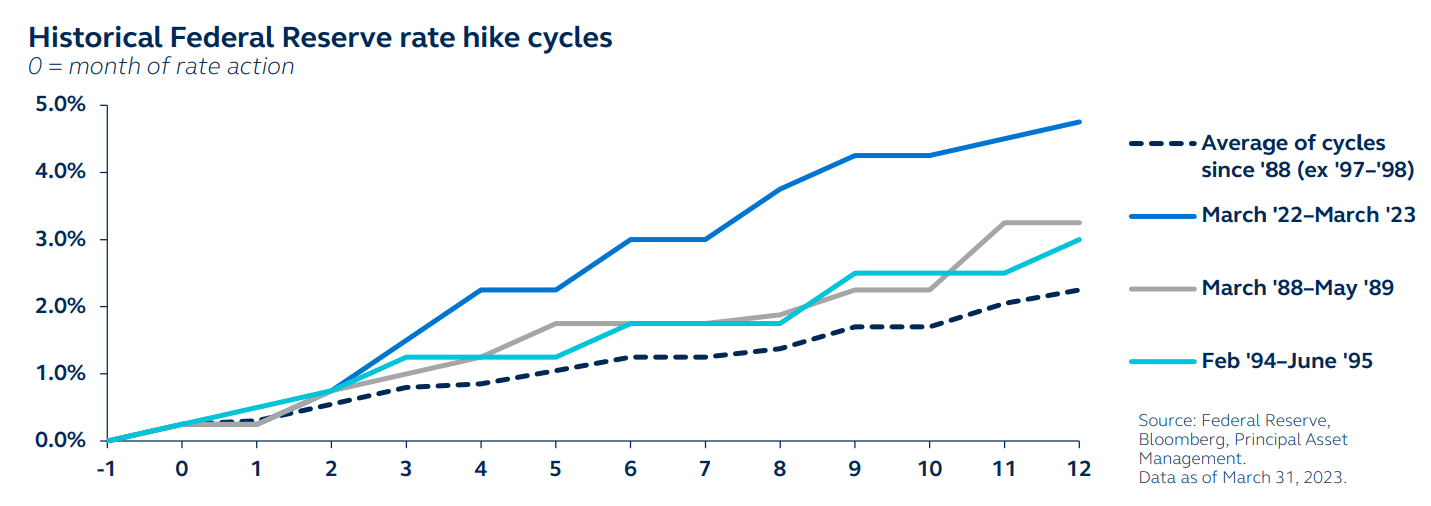

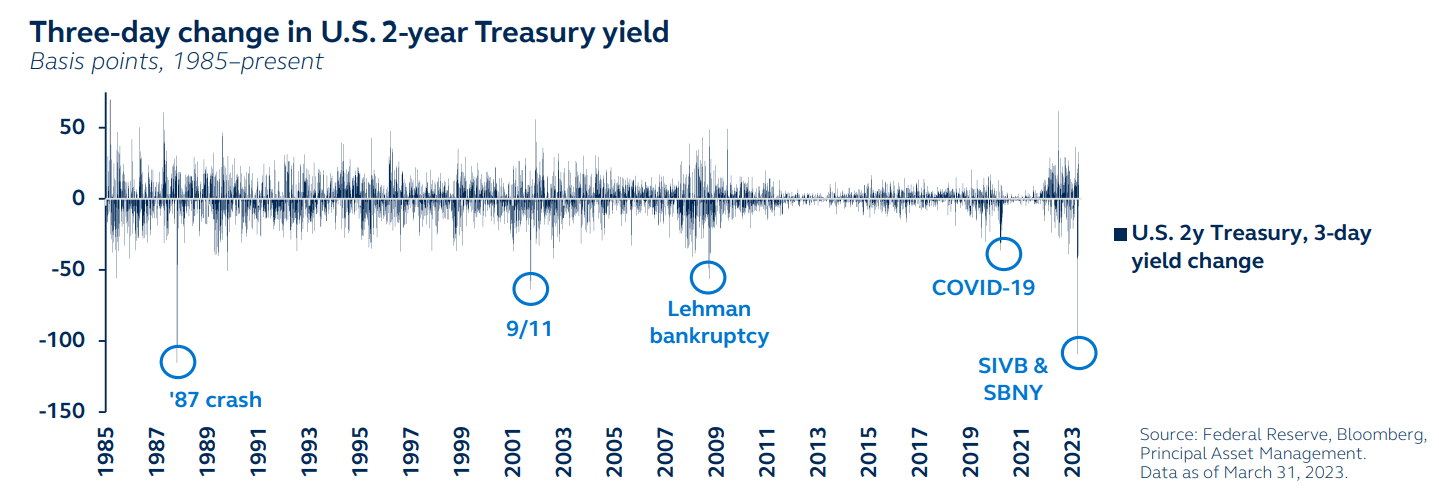

Fed tightening cycles: Something always breaks

In the space of 12 months, the Fed has raised policy rates by 475 bps, taking the Fed Funds rate up to 4.75-5.00%. Not only has this been the most aggressive pace of Fed tightening since 1980, but policy rates are now the highest since 2007, just before the Global Financial Crisis. Historically, whenever the Fed has raised rates significantly, it has resulted in some type of crisis.

In the current cycle, there have been several mini-crises, including the UK LDI crisis last October which threatened the UK pension system and, more recently, the collapse of two U.S. banks. Both events triggered sharp market turmoil but were rapidly contained by policymaker liquidity intervention, enabling central banks to continue raising policy rates. Unfortunately, each additional rate hike increases economic and financial pressures, raising the chances of further crises.

The Fed could respond to additional financial stress by cutting policy rates. Even then, by the time the Fed pivots, the economic damage is usually done and risk assets continue to struggle even as rates fall. What’s more, with inflation still elevated, an aggressive Fed response seems unlikely.

Historically, whenever the Fed has raised rates significantly, something breaks. While the recent banking crisis appears contained, the risk of further turmoil increases with each subsequent rate hike.

{kind=link}

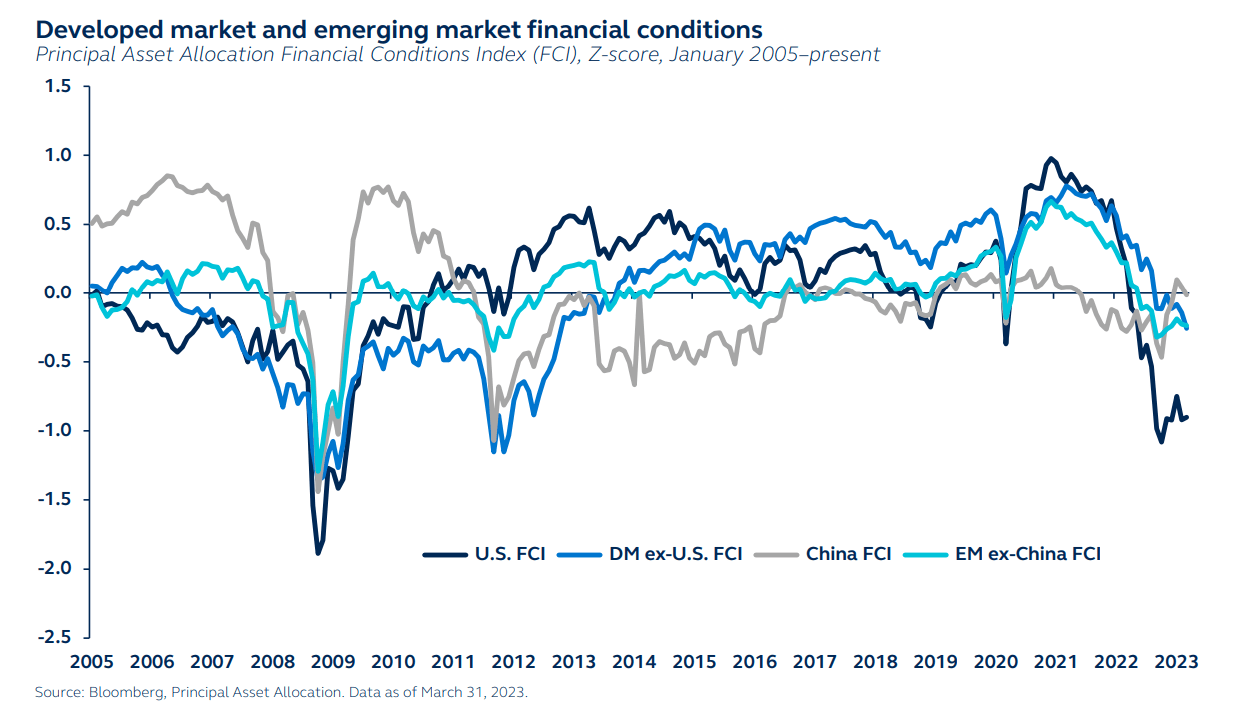

Financial conditions set the stage for another tough year

Financial conditions describe the way in which policy influences the economy through the intermediation of a wide range of market rates, risk premia, and spreads, as well as the exchange rate. Unsurprisingly, given the breadth of financial market stress, the first quarter of this year has seen a sharp tightening in developed market financial conditions. Some measures suggest that the tightening in lending standards through March is equivalent to a 150 bps increase in the Fed funds rate.

Conditions are set to worsen. Currently, bond markets are pricing in cuts in Fed funds by the July meeting, suggesting that there will be a rapid further deterioration in financial conditions through 2Q, which will force the Fed’s hand. Against this backdrop, recession risk is elevated and risk assets will likely struggle further.

By contrast, China’s financial conditions picture looks very different. China’s policymakers are maintaining easy monetary policy, adding modest stimulus as they encourage a robust economic recovery. However, if systemic risks reescalate, China and the broader EM space will not be immune and financial conditions there would also tighten.

{kind=link}

Equities

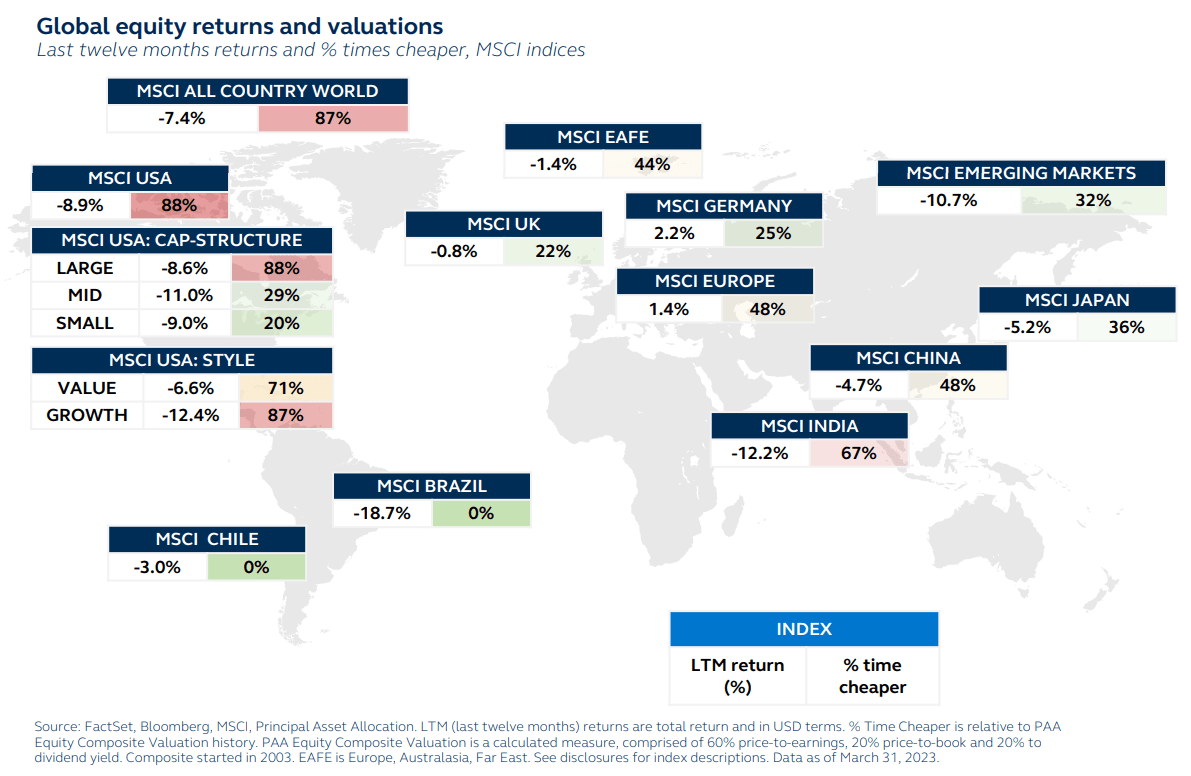

Global equity valuations: Spot the odd one out

The broad equity market performance in 1Q was fairly resilient, shrugging off concerns around banking sector stress and elevated recession risk. Although market turmoil around Credit Suisse ( CS ) weighed on the wider European banking sector in mid-March (resulting in a significant spike in volatility), Europe regained its balance by quarter-end. By contrast, China and emerging markets struggled to advance, as renewed dollar strength added to headwinds.

Following the quarter rally, global equity valuations have become less attractive, although most markets can still be considered relatively cheap following last year’s drawdown. In Europe, Germany and the UK remain attractive, while valuations in the European banking sector have only been cheaper during the Global Financial Crisis and the European Sovereign Debt Crisis.

Emerging markets can also be considered cheap, driven by significantly discounted valuations in Latin America. Indeed, Brazil is at its cheapest level in history. On the other hand, China’s valuations appear close to their historical average. The U.S. remains the most expensive market, especially large-cap and growth indices, which have been cheaper 88% and 87% of the time, respectively.

Global equity valuations have become slightly more expensive. The U.S. remained the most expensive market, whereas Germany and the UK have rarely been cheaper.

{kind=link}

U.S. equities: Confronting the fallout from rate hikes

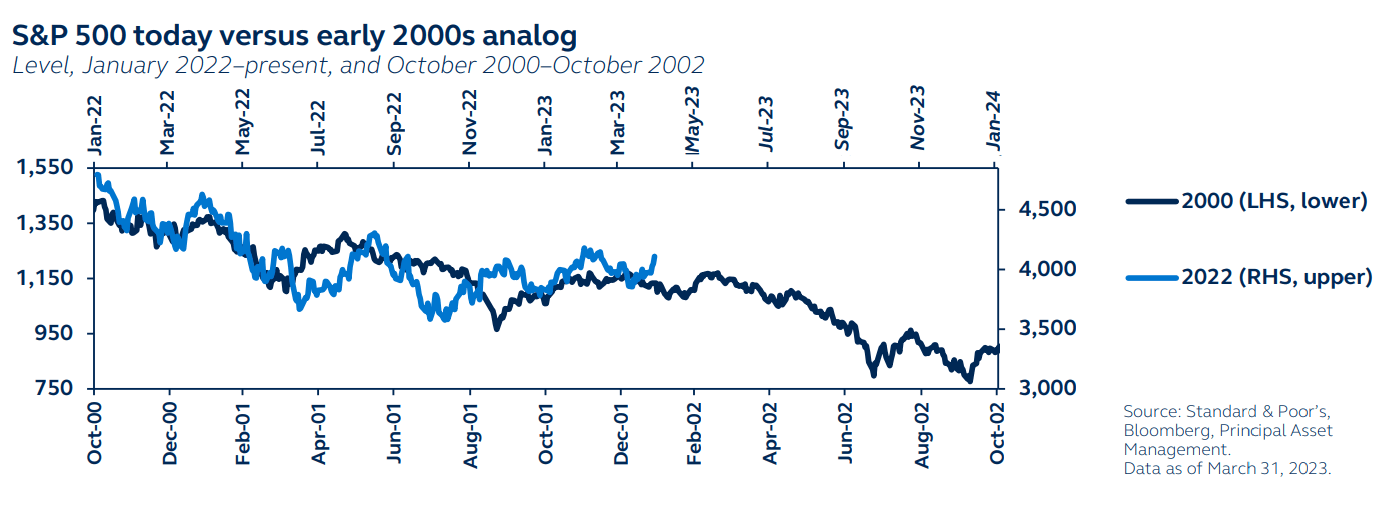

U.S. equities have proven fairly resilient, recording quarterly gains even as the Fed has persisted with its historically aggressive tightening cycle and as banking sector stress spiralled. In fact, the S&P 500 has tracked the path of the equity market during the 2000-2002 downturn, suggesting a further protracted path of weakness could lie ahead.

Fundamentally, there is strong reason to expect additional equity market drawdown. While 2022 dynamics were driven by inflation and rates scares, 2023 is likely to be dominated by earnings and economic growth scares.

Indeed, bond markets are increasingly pricing in a severe growth shock. Fed tightening has put significant stress on the economy and, with yield curves deeply inverted, bank profitability has been under pressure. In response, banks are raising credit standards and likely starting to limit credit flow, weighing on consumer spending and labor markets. An economic recession, with a clear negative impact on earnings growth, will likely have a serious impact on the already shaky footing of risk markets.

Although equities have so far shrugged off growth concerns, this apparent disconnect between equities and bonds likely won’t be prolonged from here.

The equity and bond market disconnect is unlikely to persist for much longer. Aggressive Fed tightening will ultimately weigh on economic growth, further challenging equity markets.

{kind=link}

{kind=link}

U.S. equities: Earnings recession to take its toll

Even in the unlikely scenario of the Fed engineering a soft landing, an earnings recession may already be in the cards. Reported S&P 500 earnings have been slowing since their peak in mid-2022 and contracted by -3.2% in 4Q. Without the energy sector’s support, this falls to a -7.4% contraction.

Earnings growth will be further challenged in the coming quarters. Record-high margins, initially padded by high inflation, are now facing headwinds as price pressures ease and wage demand plays catch-up. Even support from the energy sector is fading as oil prices revert to 2021 levels. A conservative model, which excludes interest rates, points to an earnings contraction in 2023.

Today, the stocks of the S&P 500 are valued at about 18.4x forward earnings, above the 15-year median of 16.1x, suggesting that positive earnings growth expectations remain embedded in price levels. As earnings disappoint and future earnings expectations are revised downward, this could then present a significant risk to equity levels.

Amid these challenging conditions, investors should prioritize margin resilience. Corporates that are able to preserve margins and top line growth via pricing power will likely become increasingly attractive.

Markets are yet to appreciate downside earnings risk. As macro conditions deteriorate, the S&P 500 is likely to re-test its September 2022 lows.

{kind=link}

{kind=link}

Styles to the side, re-focus on sectors

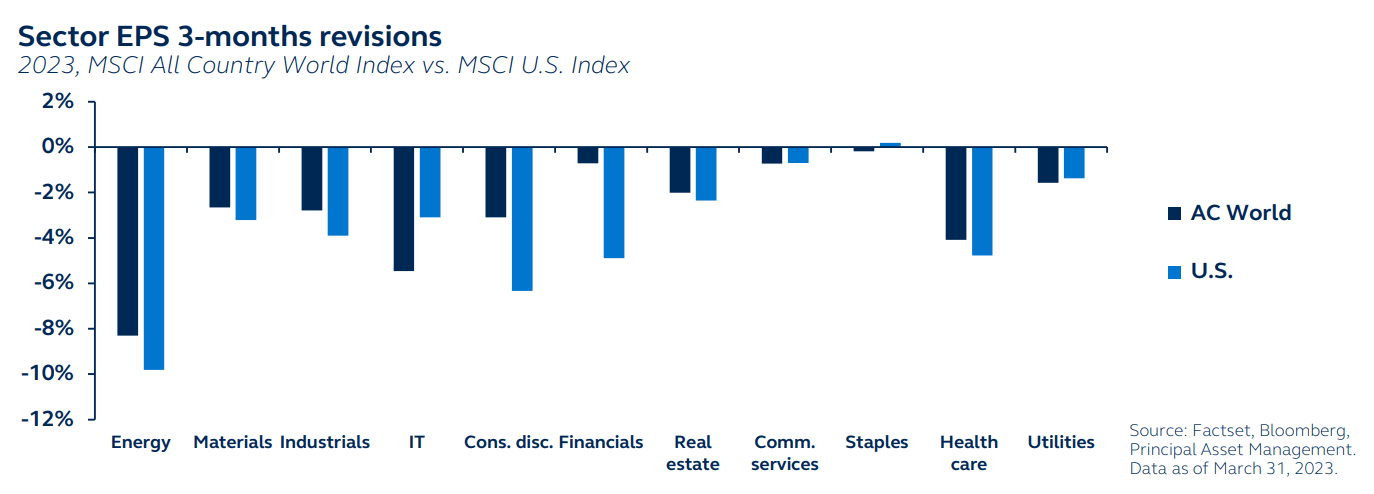

Value tends to be more cyclical and tied to the broader economy, so the expected economic slowdown would not typically favor value. By contrast, lower bond yields as the economy weakens benefits stretched valuations, more typical of growth. With growth companies heavily populating the large-cap space, its recent outperformance could extend. In the current environment of elevated bond volatility and increased focus on margin preservation, investors should also take closer consideration of sectors.

In 1Q, earnings expectations were revised lower across sectors. The downward revisions were particularly large in cyclical sectors, with 2023 EPS expectations turning sharply negative for energy and materials. There was also a significant downgrade to the U.S. consumer discretionary sector relative to other regions, highlighting the greater concerns for the U.S. economy. Defensive sectors, such as utilities and staples, saw fewer downward revisions.

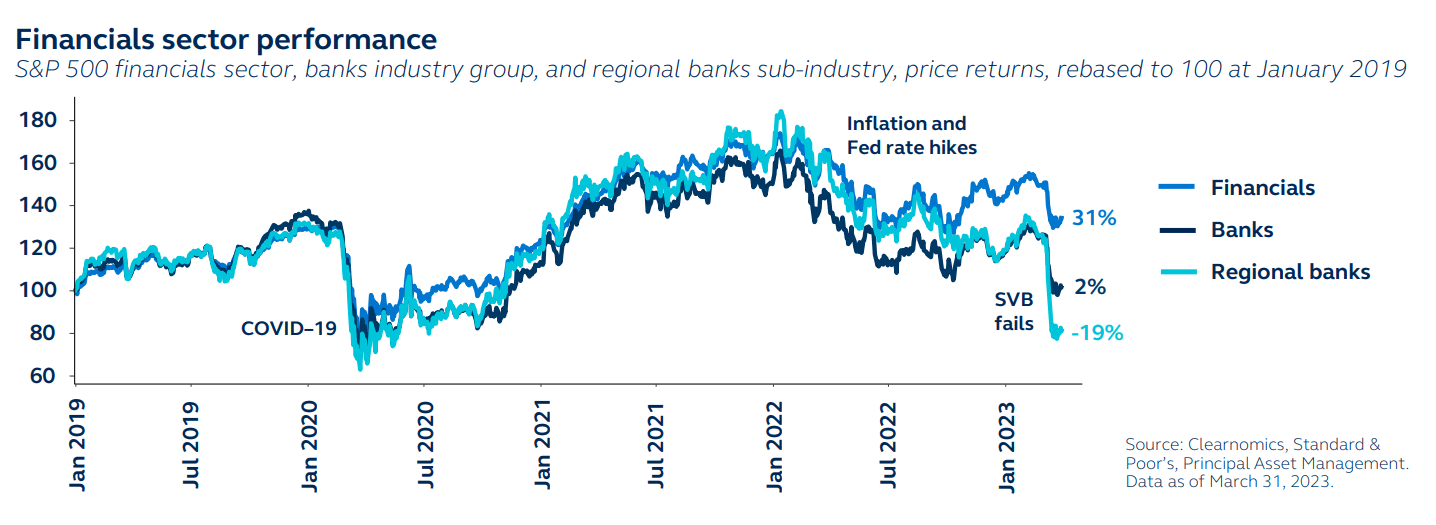

The U.S. financial sector was also subject to some downward revision, but this preceded the recent events in the banking space. Wavering confidence, tightening lending standards, particularly in regional banks as they look to shore up balance sheets, will likely result in further downgrades in this sector.

An uncertain macro environment and a volatile market suggest defensive sectors (utilities, staples, health care) could potentially outperform.

{kind=link}

{kind=link}

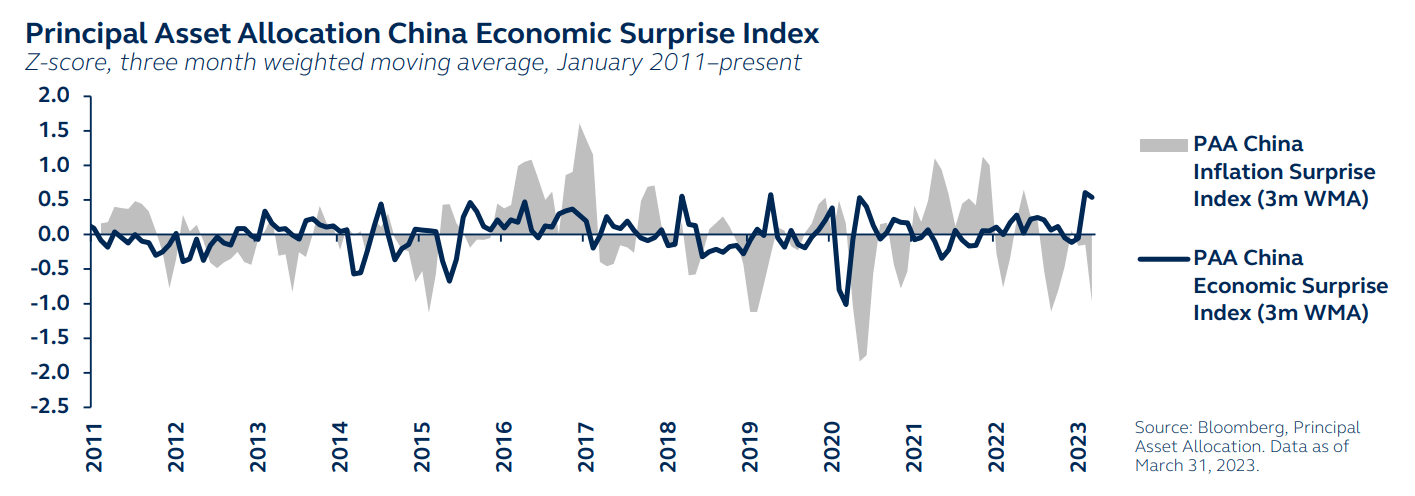

China and EM: Reopening is driving momentum

China’s economy is moving in a very different direction to most developed markets. The lifting of COVID restrictions in late 2022 has seen economic activity data beat expectations by the largest margin since April 2020. The release of considerable pent-up demand as consumer confidence grows should ensure a continuation of this positive economic performance.

In addition, China’s inflationary pressures have stayed muted, permitting its central bank to continue easing policy even as other major central banks tighten policy. However, incremental easing will likely be moderate. The government has set a benign 2023 growth target of 5.0%, lower than widely expected.

Broader EM is benefiting from China’s recovery, particularly its key trade partners, with the weaker U.S. dollar also supporting EM performance. Attractive EM valuations are coinciding with improving fundamentals.

China and the broader EM complex has also been somewhat isolated from the recent U.S. and European banking sector turmoil. However, if liquidity stress escalates, EM performance will likely struggle.

A strong economic recovery will continue to help China and EM equities, while China’s insulation from recent banking sector turmoil is an additional positive.

{kind=link}

{kind=link}

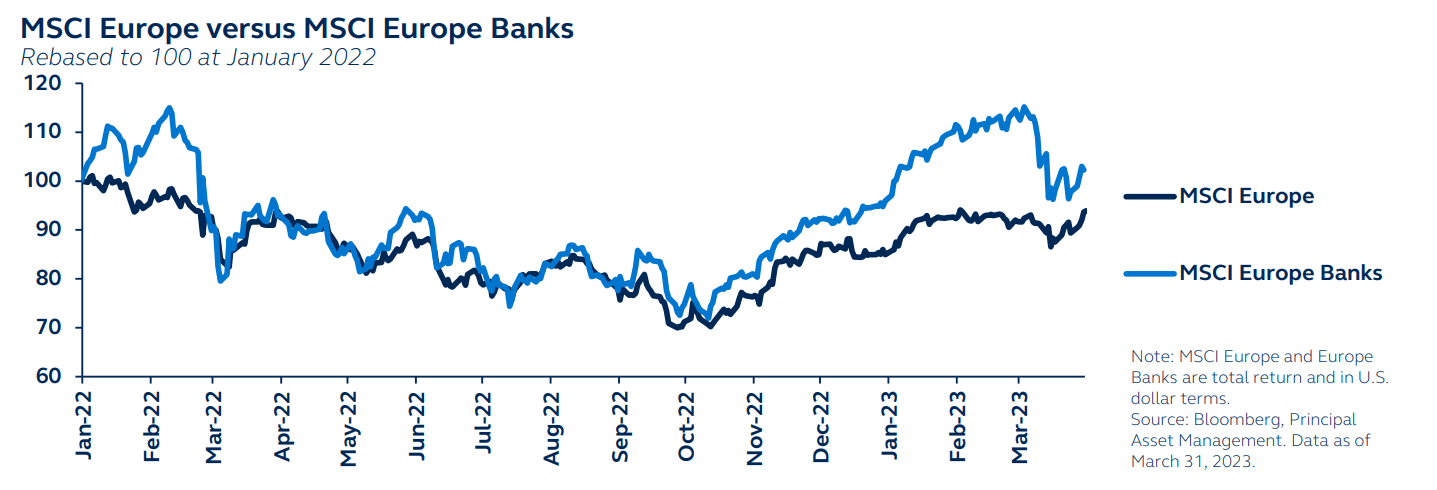

Europe’s banking crisis interrupts a strong story

European equities had been outperforming U.S. equities, modestly recovering some of the decades-long underperformance trend. This rally was initially catalyzed by the improved energy picture, as well as the expected benefits from China’s reopening. As European fundamentals strengthened, investors were able to take advantage of the historic discount of European equities relative to U.S. equities.

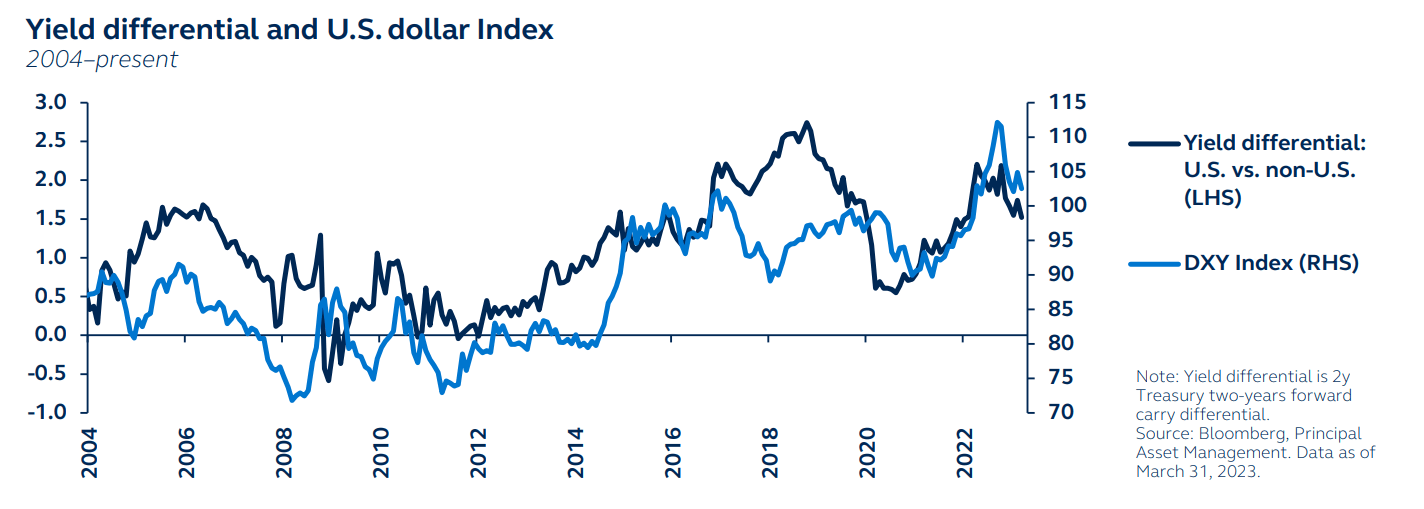

The weakening U.S. dollar has also been an important factor, with the recent slowing of Fed rate hikes, contrasted to the ECB’s accelerating rate hikes, precipitating the crack in the greenback’s historic rally. This change in dollar direction has been highly advantageous to foreign stock investors, and, if extended, adds to the non-U.S. investment story.

Earlier in 1Q, European banks sat in pole position, with investors finally appreciating the fact that they hold stronger liquidity positions and lower duration risk than U.S. banks and have valuation multiples meaningfully less stretched. However, the recent European banking crisis has knocked confidence, dimming the outlook for broad European equities.

In addition, Europe’s concerning inflation picture suggests that the ECB may continue raising rates aggressively, increasing the risk of renewed weakness in the future.

Although Europe outperformed in 1Q, concerns around its banking sector, as well as risks that the ECB will have to tighten considerably further, prompt a neutral outlook.

{kind=link}

{kind=link}

Fixed income

Fixed income: Still in fashion

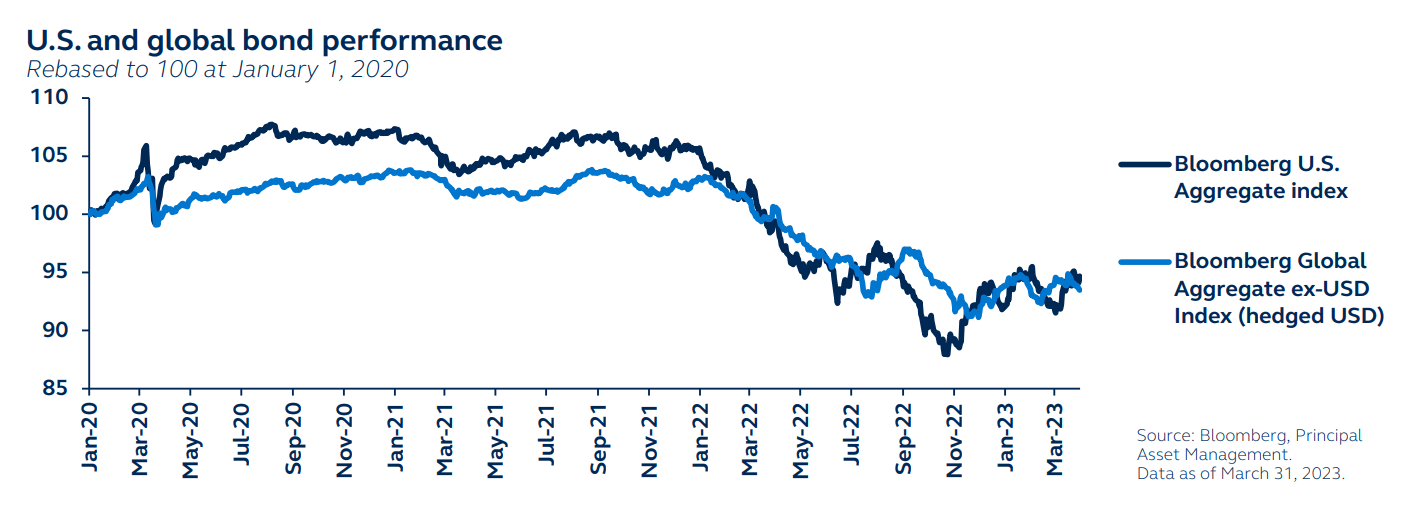

After suffering one of the deepest drawdowns in U.S. history in 2022, U.S. bonds started the year strong, even ending 1Q with modest gains, despite a rather eventful quarter. Fears of aggressive hikes due to persistent inflation initially sent bond yields soaring, with 2-year Treasury yields hitting a post-2007 high of 5.1% in early March. However, inflation fears swiftly gave way to growth and financial stability concerns as U.S. regional banks came under significant stress, sending yields plummeting. The result was a net decline of Treasury yields in 1Q, which offset credit spread widening for U.S. investment grade and high yield bonds.

Both the U.S. and Global Aggregate Bond Index earned modest gains in 1Q, albeit through a fickle journey. Bond diversification benefits were clear, especially as bank liquidity concerns drove U.S. spreads wider, driven mostly by lower sovereign yields. Global Agg spreads also widened, but less so, as European banks also came under pressure. Hard currency EM debt showed resilience, exempted from DM banking risks, to also end up with modest gains.

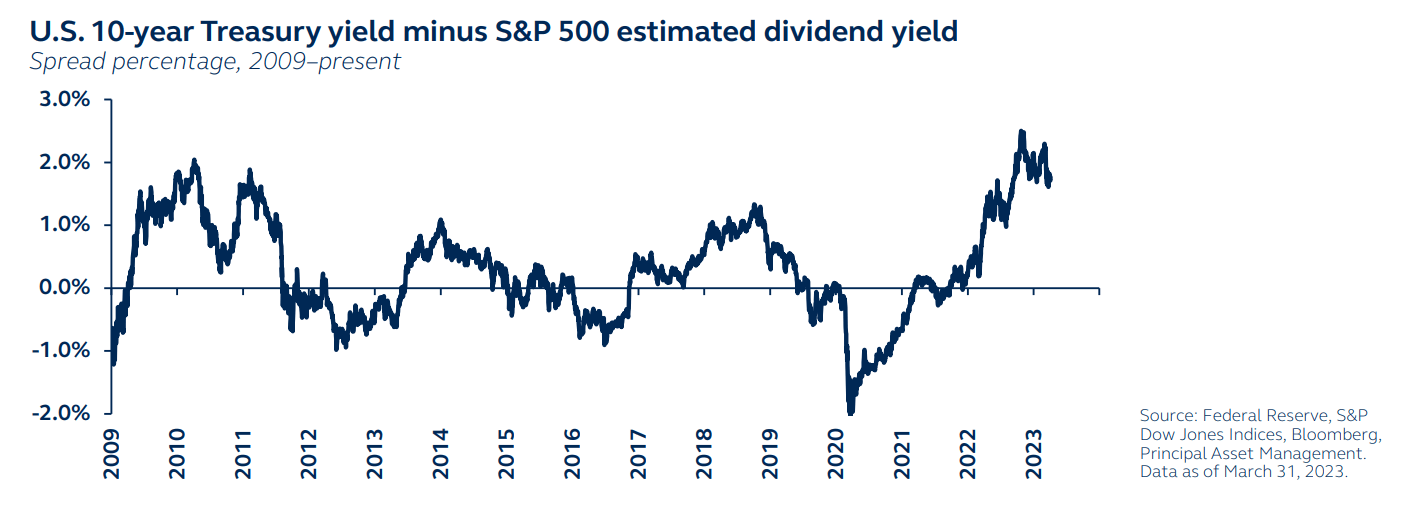

Despite the recent rally, bonds remain favorable. 10-year U.S. Treasurys yield more than twice the estimated dividend yield of the S&P 500, presenting investors an opportunity to lock in income with a generally less-volatile asset.

With growth and financial stability concerns outweighing inflation fears, and valuations remaining attractive, the investment thesis for fixed income is getting stronger.

{kind=link}

{kind=link}

U.S. Treasurys: Playing an important role in portfolios

The most pristine collateral in the global financial system is U.S. Treasurys, and their liquidity and quality was recently demonstrated amid U.S. regional bank concerns. Investor fears precipitated a flight-to-quality, liquidity-seeking episode of historic market volatility.

This episode has proven the important diversification benefits of holding fixed income securities in a portfolio as a hedge against both volatility and market illiquidity. While the abysmal 2022 performance of the asset class caused some to question fixed income’s ability to provide diversification, 1Q 2023 restored that characteristic.

Not only does fixed income now pay a historically high coupon rate, its cash flows are typically more stable than risk assets. As the economy slows and corporate earnings likely come under pressure, the reliability of fixed income coupons will become more highly valued.

Indeed, as economic weakness permeates over the coming quarters, market interest rates will likely recede to recessionary levels. This will also provide for capital appreciation for bond holders.

Security, diversification, reliable cash flows, and upside potential make a compelling case for holding U.S. Treasurys.

{kind=link}

{kind=link}

Navigate credit headwinds with high-quality assets

As recession approaches, high-quality credit will become a more attractive investment proposition. A growing premium will likely be placed on solid earnings performance, and this will be reflected in disparate performance of high- versus low-quality credits.

Historically, the risk-adjusted returns of agency MBS are some of the most attractive, with lower volatility compared to similar high-quality U.S. fixed income sectors. They are also backed by guarantees from U.S. government-sponsored enterprises.

Corporate credit spreads to U.S. Treasurys have remained tight, however, recent volatility stemming from U.S. regional banking concerns have led to some spread widening. These could be expected to widen further as macro and liquidity conditions deteriorate and lending standards tighten further.

Investors have been comforted by the so-called funding wall, which postpones the need for corporates to refinance maturing bonds, insulating credit from market stress. However, the refinancing requirements are set to gradually rise over coming quarters, and less-than-favorable coupon resets could deliver illiquid market conditions. Consequently, investors should tilt toward liquidity as well as quality when selecting credit asset classes.

Higher-quality fixed income assets, such as agency MBS and investment grade credit, should outperform as lending standards tighten and the economy slows.

{kind=link}

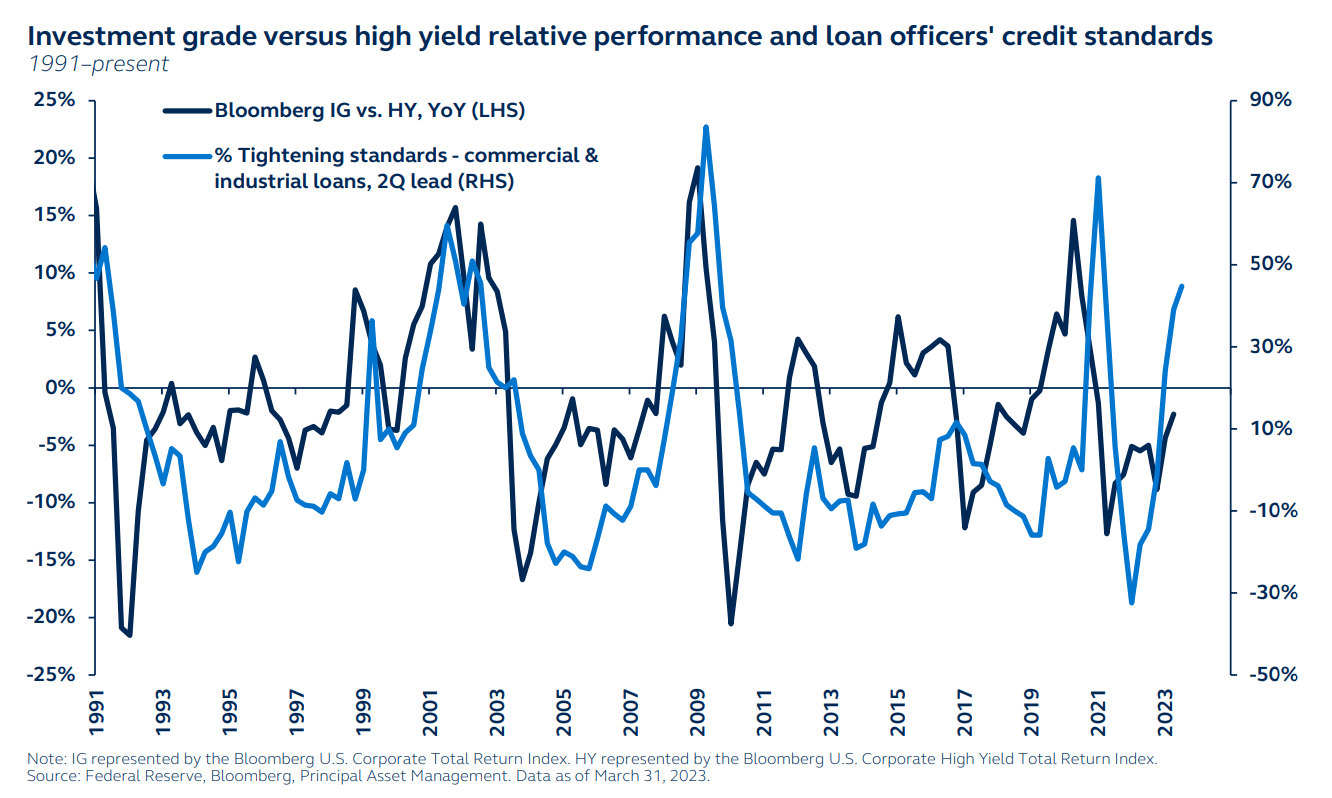

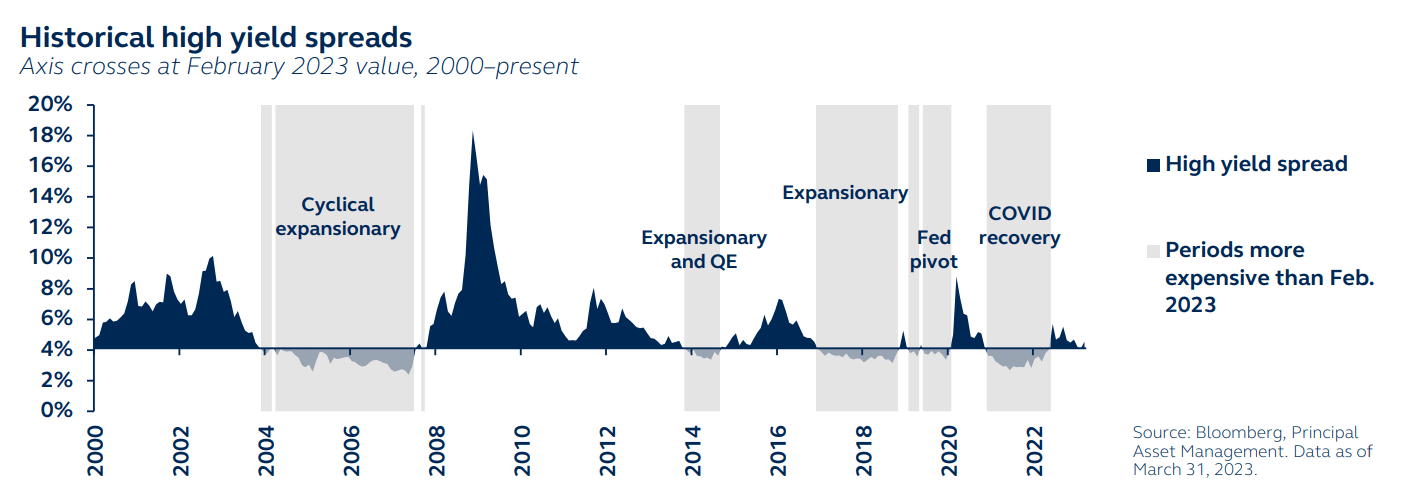

High yield: Time to face the music

High yield delivered relatively resilient performance in early 1Q, with spreads tightening despite economic slowdown concerns. But by the end of February, alarm bells were ringing. Since 2000, high yield had been more expensive 40% of the time. While this doesn’t immediately seem worrying, each of those more expensive periods either featured economic expansions or a dovish Fed, neither of which is the case currently. High yield was overdue a negative hit. In the end, the turmoil in U.S. and European banks delivered a strong dent to risk appetite, driving a widening in credit spreads. Yet, while U.S. high yield spreads now exceed the 2010-2022 average of 468 bps, they could widen further on the back of fresh liquidity issues in the banking sectors. Investor caution is likely to grow as the slowing economy and hawkish central banks come into tension. 2020’s flood of new issuance brought forward years of new bond supply, and has limited issuance since. This produced a so-called funding wall, where annual issuance has been depressed and corporates have been immunized from rollingover debt amid rising yields. However, issuance is expected to pick up in coming periods, and difficulties could arise as new debt faces higher rates and more risk-averse investors.

High yield spreads could widen further on fresh liquidity issues in the banking sector and as economic slowdown concerns deepen.

{kind=link}

{kind=link}

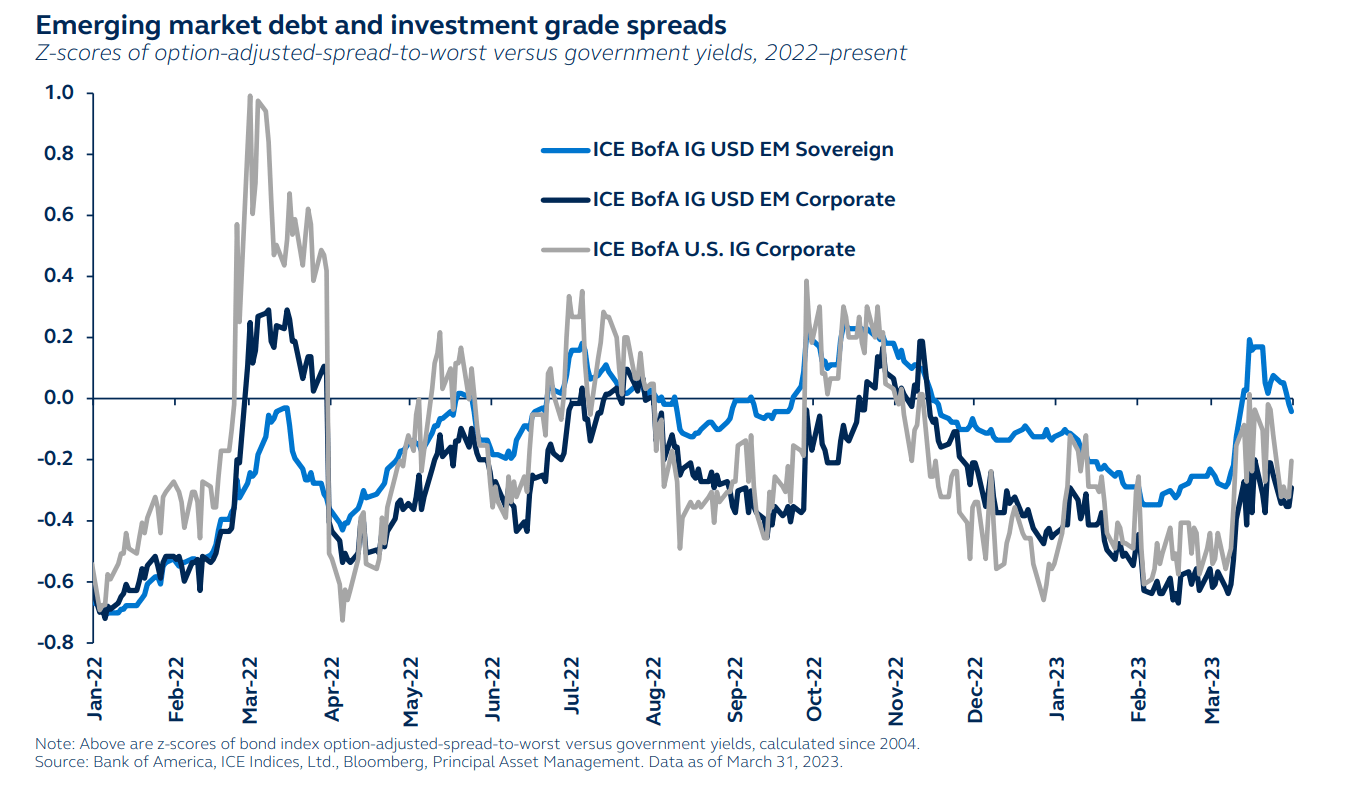

EM debt: Improved outlook but with lingering risks

In 2022, emerging market debt was hit hard by a confluence of headwinds, including China’s COVID lockdowns and property crisis, the Russia-Ukraine war, and a spectacular USD rally fuelled by one of the most aggressive hiking cycles in history.

Three months into 2023, many of those headwinds have either become tailwinds or have at least abated:

- China’s reopening went smoother than expected, with a strong economic rebound and continued policy stimulus.

- Energy prices have fallen following a mild winter in Europe, fading some of the immediate EM economic constraints.

- The U.S. dollar has started to weaken as the end of the Fed’s rate hiking cycle approaches, giving EM central banks the space to ease policy and ignite domestic growth (inflation permitting).

As well as improving fundamentals, EM sovereigns provide historically favorable spreads, and are also attractive relative to both EM and U.S. corporates. However, EM debt would not be entirely immune to a spike in liquidity strains if U.S. banking concerns return.

EM headwinds have broadly become tailwinds, improving the picture for EM debt. However, with global liquidity concerns continuing to threaten, a neutral position is advised.

{kind=link}

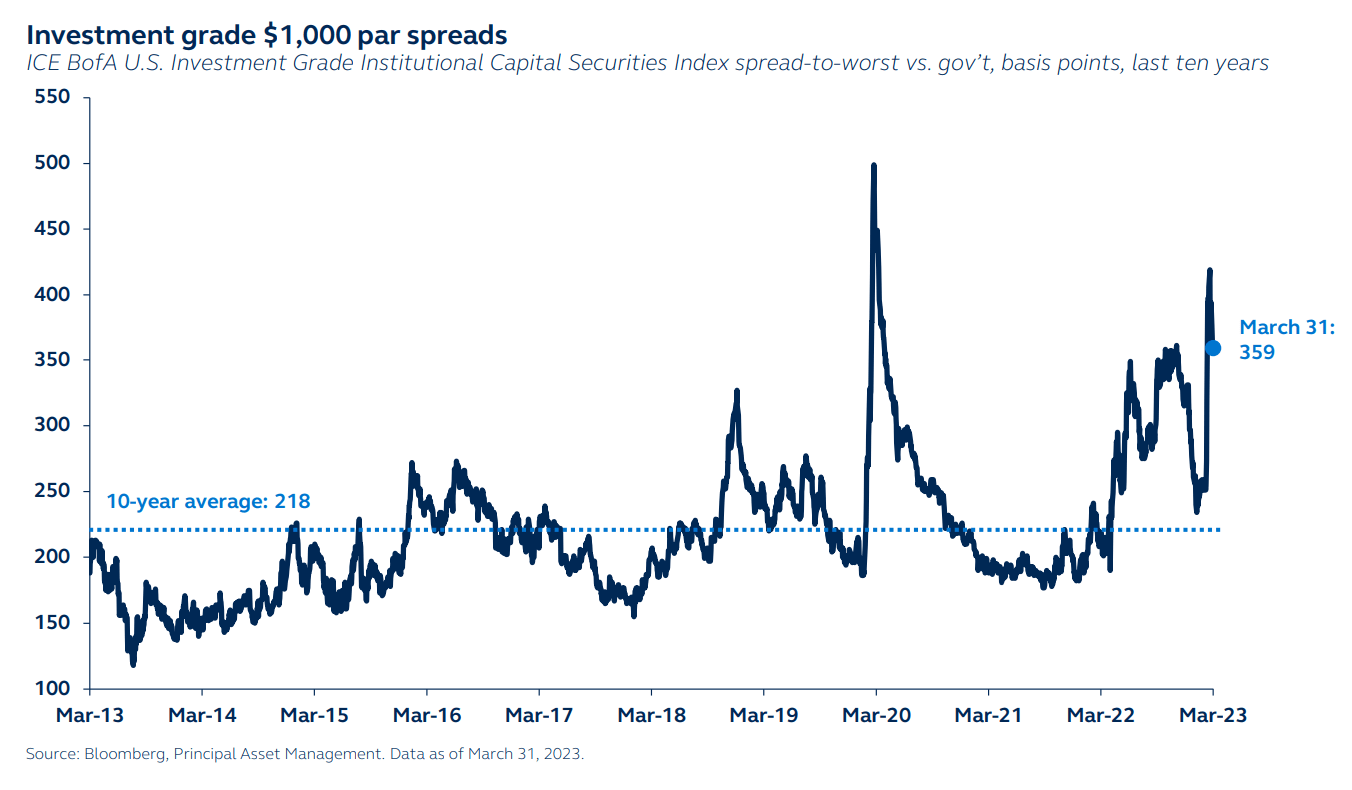

Preferred securities: A market dislocation opportunity

The recent banking crisis created significant turmoil in preferred and capital securities - hybrid securities that have features of both stocks and bonds and sit between the two in the capital structure. Yet, with the crisis seemingly now contained, the extra risk attached to the hybrid assets is likely overdone, creating a compelling investment case:

- The U.S. banks that collapsed were unique to the broader banking sector - and the risks have been further reduced by recent federal regulatory support and a new Federal Reserve lending program.

- The decision by Swiss regulators to wipe out Credit Suisse Additional Tier 1 (AT1) bondholders ahead of equity holders in the UBS merger initially had the market perplexed, triggering significant selling of the AT1 and contingent capital (CoCo) market. However, European regulators have since confirmed that, for banks outside Switzerland, AT1 bonds only take losses after equity holders, thereby removing a key source of investor concern.

- Following the banking crisis, yields are near their highest levels in more than 10 years, and spreads to yields on risk-free Treasurys are historically wide.

These assets offer a yield advantage over core bonds and, with regulators and policymakers intent on containing bank risks, have a more attractive risk profile than high yield.

{kind=link}

Alternatives

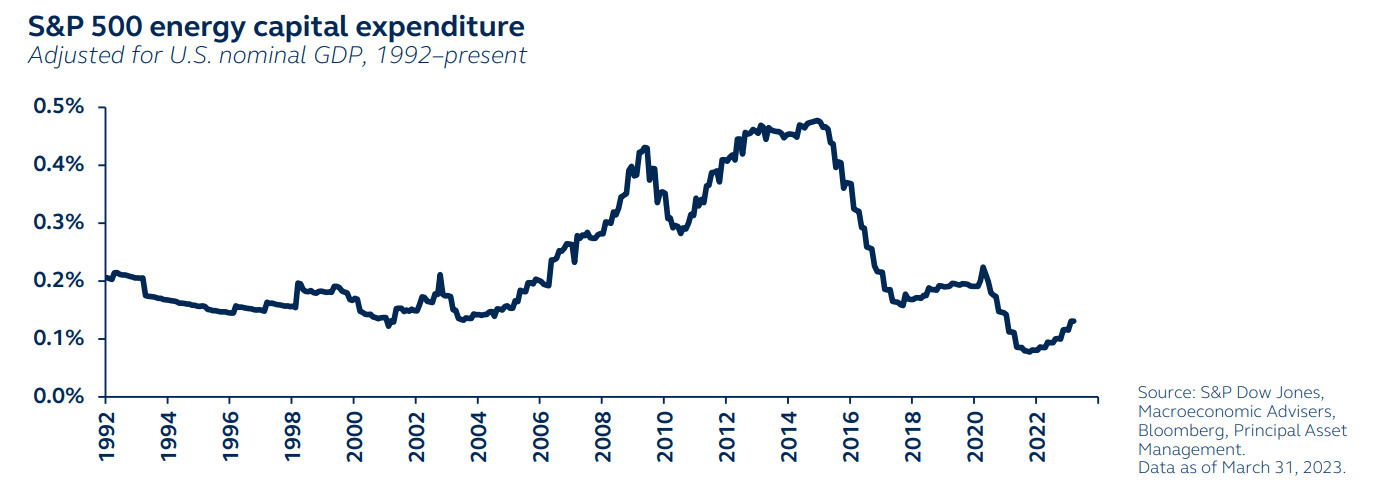

Commodities: Caught in the global cross-currents

After being the standout performer in 2022, commodities have been under severe pressure and underperformed most traditional asset classes in 1Q as concerns about economic growth have come to the forefront.

The near-term outlook for the asset class remains challenged. While China’s reopening is expected to boost demand, limited government stimulus policy actions suggest that the bounce in economic growth will be more reassuring than spectacular. The positive China reopening dynamic is broadly offset by rising fears around U.S. economic growth, resulting in significant uncertainty around the commodity demand outlook. Renewed geopolitical risks could result in a surge in commodity prices if supplies are disturbed (as shown by OPEC’s recent decision to cut supplies). However, geopolitics is particularly difficult to predict. Ultimately, the short-term outlook is shrouded in uncertainty.

The long-term outlook, however, remains more constructive. Limited capital expenditure in fossil fuels capacity over recent years implies that commodities are likely to remain in a long-term state of structural supply deficits that will be supportive of commodity prices.

The short-term commodity outlook is highly uncertain, as China growth hopes are offset by U.S. growth fears. Long-term trends are clearer and more constructive.

{kind=link}

{kind=link}

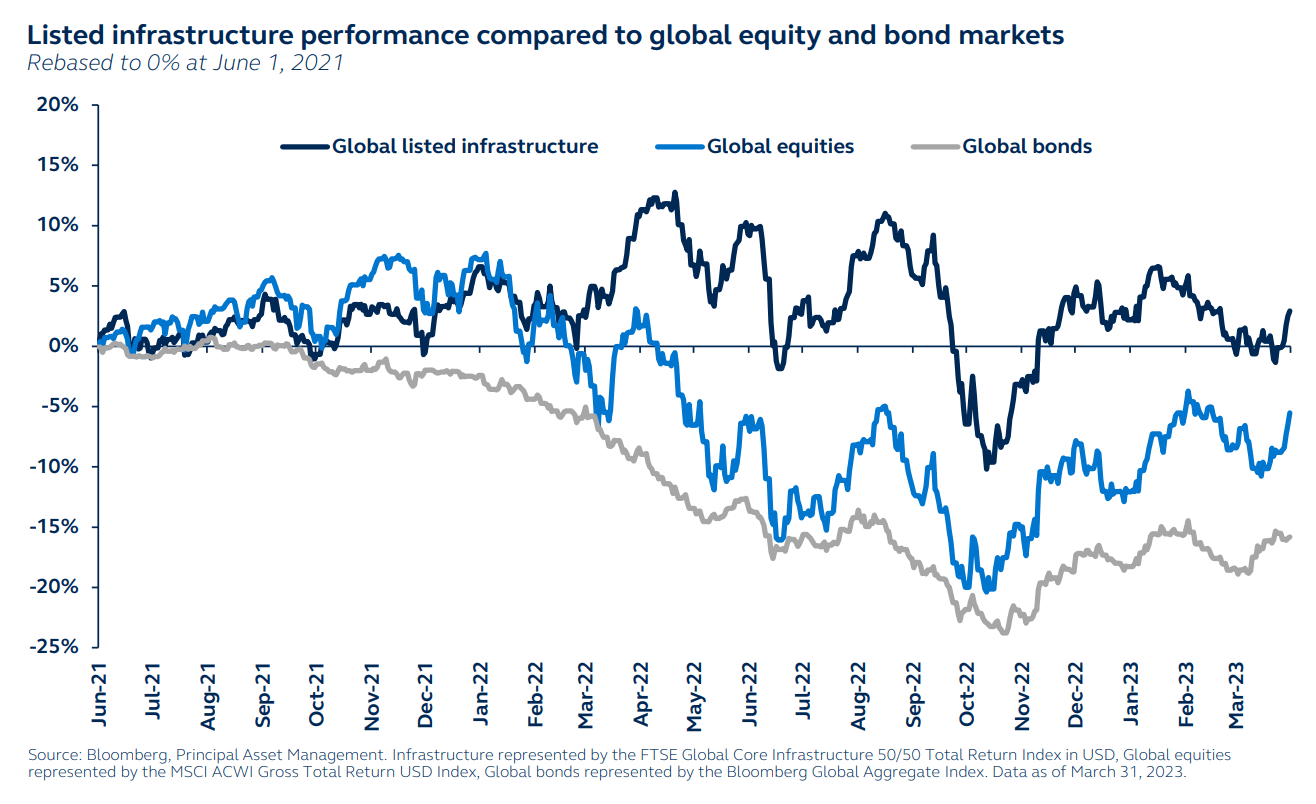

Infrastructure’s valuable defensive characteristics

A continued constructive view on alternatives conveys not only their diversification benefits in this macro environment, but also their fundamental strengths and defensive characteristics. Indeed, through the recent banking sector stress, which resulted in turmoil for the broader market, listed infrastructure performed strongly - true to its defensive nature.

Infrastructure investments, in particular, are one of the few asset classes that can potentially outperform in the current slowing growth, elevated inflation environment. Since demand for critical services is less sensitive to inflation, owners of certain infrastructure assets can sustain and increase prices without significantly impacting demand, offering potentially resilient returns. Listed infrastructure has historically delivered meaningfully higher returns than global equities during periods of elevated inflation.

Furthermore, infrastructure investments typically have predictable cash flows associated with the long-lived assets, with historically attractive yields. They also offer exposure to the global theme of de-carbonization, which presents a multi-decade tailwind for utilities and renewable infrastructure companies

Infrastructure continues to offer important diversification benefits, as well as inflation mitigation and a more stable income stream.

{kind=link}

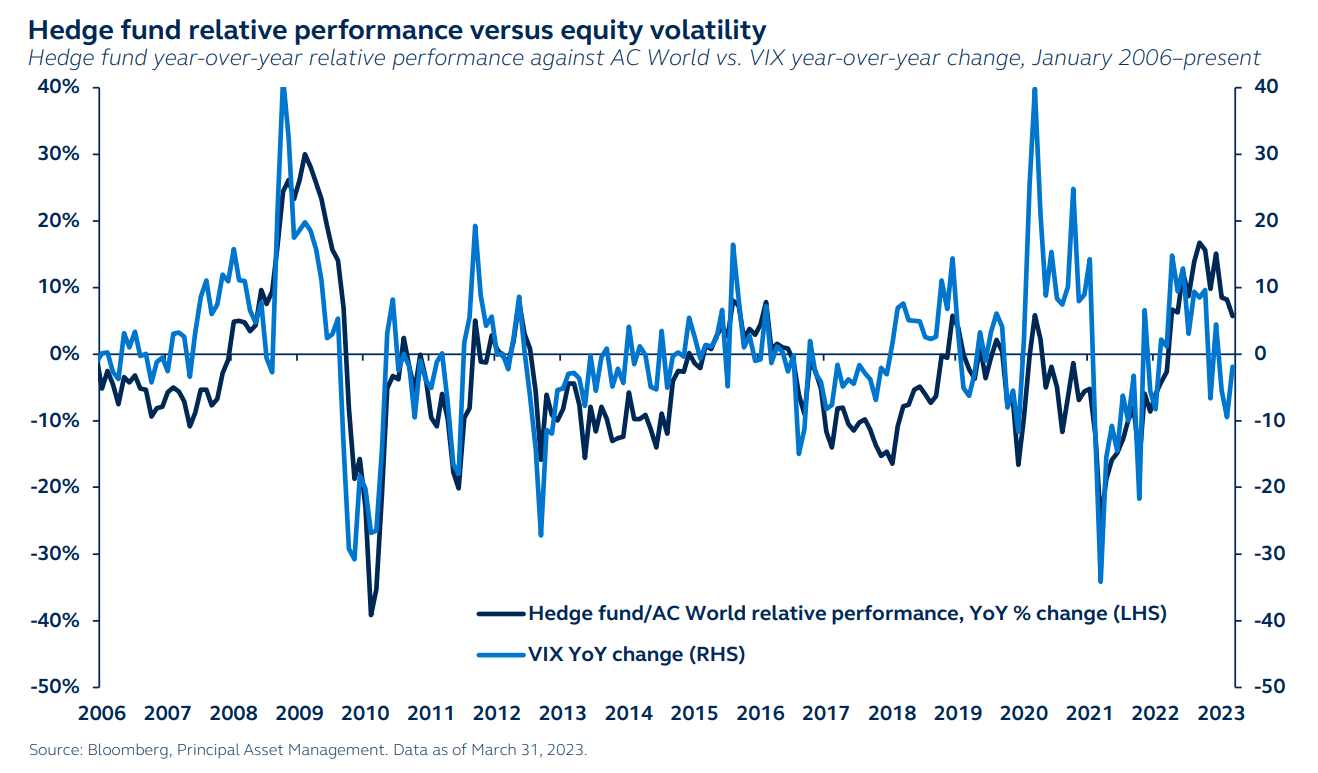

Hedge funds: Riding the volatility

With the shift away from the low-inflation, low-interest rate environment of the past decade, the macroeconomic backdrop has become more uncertain. Persistent, elevated inflation is coinciding with tightening lending standards, rising recession risks, and early cracks in the financial system, clouding the future path of monetary policy.

Economic policy uncertainty often leads to elevated market volatilities and more pronounced idiosyncratic risks - an investment landscape that presents headwinds to most risk assets.

Hedge funds, however, with their low beta exposure and high alpha potential, could potentially do well in such an environment. Historically, hedge funds’ outperformance against global equities goes hand in hand with rising volatilities, making them attractive today for investors seeking alpha, while also averting market risks.

Strong manager selection remains imperative in order to identify the outperformers, as divergence among hedge funds tends to be significant.

Policy uncertainty, as is the case in the current environment, tends to lead to rising market volatilities, which supports hedge funds' outperformance against equities.

{kind=link}

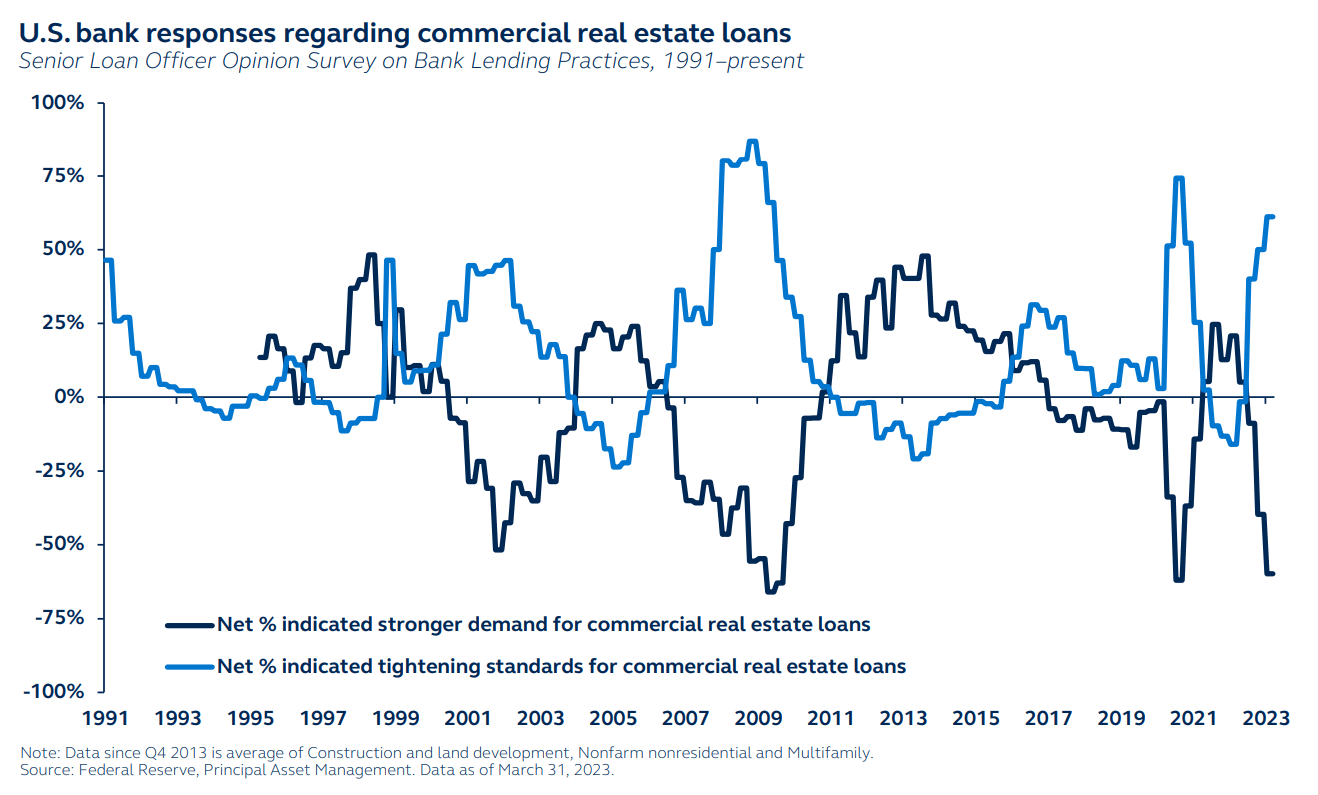

REITs vulnerable to recent banking sector strains

Typically, as economic growth weakens, defensive sectors outperform. REITs, a traditionally defensive, low-volatility sector would usually perform well in the current low-growth, high-volatility environment. In addition, as a very rate-sensitive sector, with a high negative correlation to real bond yields, REITs should benefit from the recent drop in bond yields.

However, REITs (particularly U.S. REITs) have faced intense pressure from the recent banking crisis. While systemic financial risk has been contained, the closure of two large regional lenders has raised concerns around banks’ commercial real estate ((CRE)) exposure. U.S. banks are the largest holders of CRE debt, with CRE loans representing about 20% of loans outstanding at U.S. banks, so any stress to bank balance sheets or tightening in financial conditions filters directly through to the CRE market.

With small/regional banks likely to reduce their lending appetite, and more scarce and expensive debt likely to pressure transaction volumes, a further pullback in commercial real estate - and therefore REITs - is likely in the coming months.

As a result of the recent banking crisis, REITs will face further pressure from a likely reduction in small/regional banks’ appetite for commercial real estate loans.

{kind=link}

Investment implications

Diversified asset allocation: Underweight equities, overweight bonds and alternatives.

Equities

We keep equities underweight, as weakening earnings growth will likely bring further declines even as Fed rates approach their peak. The growing risk of U.S. recession and expensive U.S. valuations means we have a preference for other markets over the U.S. Within the U.S, large-cap equities should fare well as bond yields drop as the economy slows. Outside the U.S, we have a preference for emerging markets. Not only will EM benefit from China’s stronger growth outlook and the weakening U.S. dollar, but emerging markets should remain relatively insulated from the recent banking crises, provided severe liquidity strains do not emerge.

Fixed income

Our fixed income positioning remains at an overweight, with bonds likely providing more stability during the coming economic slowdown. We neutralize all our regional positions. Within the U.S, we keep our overweight exposure to U.S. Treasurys, mortgages and investment grade, recognizing that the longer-duration, high-quality profile of these fixed income assets should outperform as the economy slows. By contrast, we keep high yield at an underweight, expecting further spread widening given recession and liquidity fears. Preferred securities remain at overweight, as concerns about the sector have likely been overdone. (Indeed, their bias is towards high-quality companies, while banks generally remain ring-fenced.) Emerging market debt moves to a neutral position as the various headwinds have transitioned to tailwinds.

Alternatives

Our continued constructive view on alternatives conveys not only their diversification benefits in this macro environment but also their fundamental strengths and defensive characteristics. We maintain our overweight to infrastructure, encouraged by its inflation protection characteristics, stability of cash flows, and exposure to the structural de-carbonization trend. With the outlook looking increasingly volatile in 2023, we maintain our overweight exposure to hedge funds. We shift our commodities position to neutral due to short-term uncertainty, while REITs remain at an underweight given growing concerns around commercial real estate.

Alternatives asset class include commodities, natural resources, infrastructure, REITs, and hedge funds. Allocations across the investment outlook can be proportionately adjusted so magnitudes across categories do not have to net to neutral.

| Equities Reduce risk appetite and focus on U.S. large-cap and quality factor. |

| Position toward certainty • Exposure to quality within equities can potentially offer risk mitigation during pullbacks. • Attractive international valuations suggest opportunities outside the U.S. • U.S. large-cap offers the potential for stronger downside protection as recession risks loom and the broader economy slows. |

| How to implement • Large-cap U.S. strategies • Quality-biased active managers • Well-diversified and active international managers |

| Fixed income Increase exposure to high-quality credit. |

| Core fixed income and preferred securities • Core fixed income to hide out in as recession risk rises. • Recommend increasing duration bias across the asset class. • Preferred securities provide potential yield and exposure to high quality. |

| How to implement • IG credit heavy core fixed income for stability • Preferred securities strategies |

| Alternatives Pursue less correlated real asset exposures. |

| Real assets • Real return-focused strategies gain attractiveness when nominal growth slows. • Infrastructure offers more stable cash flows with potentially attractive yield. • Real assets can help mitigate inflation risk. |

| How to implement • Diversified real asset strategies (infrastructure, natural resources) • Private real estate markets |

Editor's Note: The summary bullets for this article were chosen by Seeking Alpha editors.

For further details see:

Global Asset Allocation Viewpoints, Q2 2023: Navigating Increasingly Unstable Markets